Question: CIUL wrap Text General Paste Clear B I U Merge % ) ,00 .00 2.0 Cong Form J20 A D F H K L 1

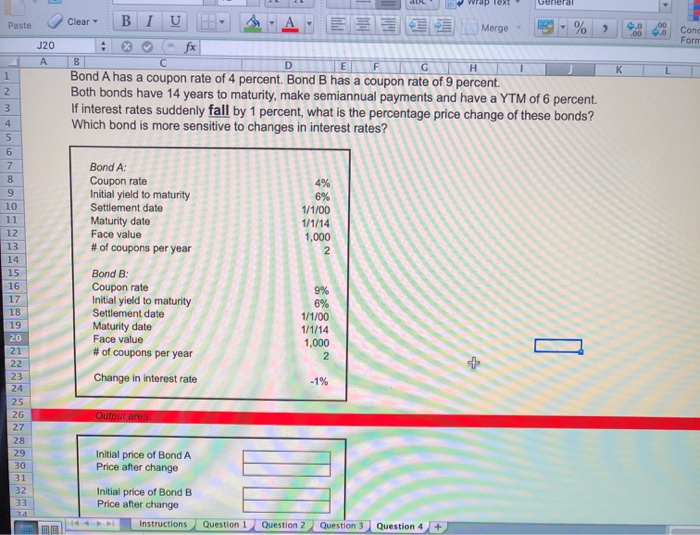

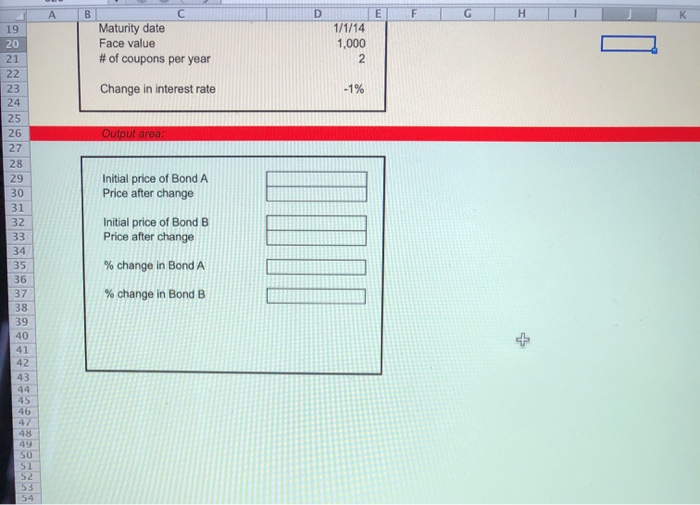

CIUL wrap Text General Paste Clear B I U Merge % ) ,00 .00 2.0 Cong Form J20 A D F H K L 1 2 Bond A has a coupon rate of 4 percent. Bond B has a coupon rate of 9 percent. Both bonds have 14 years to maturity, make semiannual payments and have a YTM of 6 percent. If interest rates suddenly fall by 1 percent, what is the percentage price change of these bonds? Which bond is more sensitive to changes in interest rates? Bond A: Coupon rate Initial yield to maturity Settlement date Maturity date Face value # of coupons per year 4% 6% 1/1/00 1/1/14 1,000 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 Bond B: Coupon rate Initial yield to maturity Settlement date Maturity date Face value # of coupons per year Change in interest rate 9% 6% 1/1/00 1/1/14 1,000 2 - 1% Output area Initial price of Bond A Price after change Initial price of Bond B Price after change Instructions DE Question 1 Question 2 Question 3 Question 4 + A B D E F G K Maturity date Face value # of coupons per year 1/1/14 1,000 2 Change in interest rate -1% Output area: Initial price of Bond A Price after change 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 Initial price of Bond B Price after change % change in Bond A % change in Bond B 49 50 51 52 53 54

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts