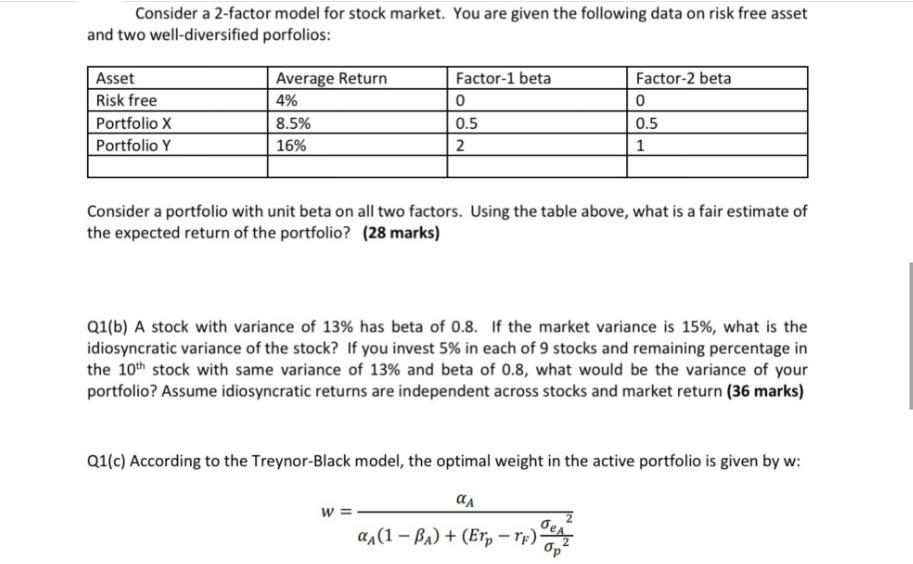

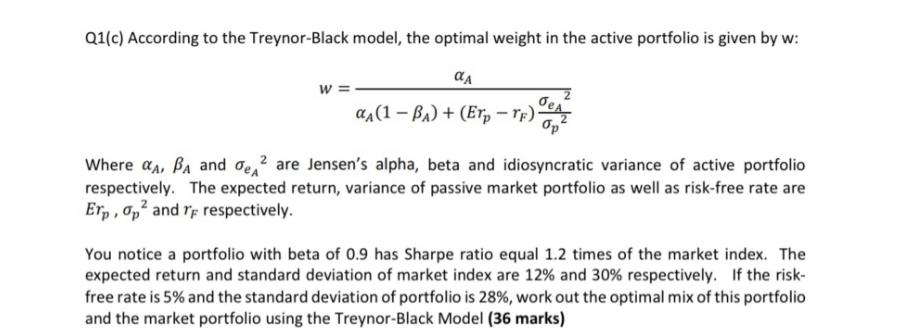

Consider a 2-factor model for stock market. You are given the following data on risk free...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: