Question: Do exactly like the example. do all the steps and explain answer c+ Ke-IT = p + So The price of a non-dividend paying stock

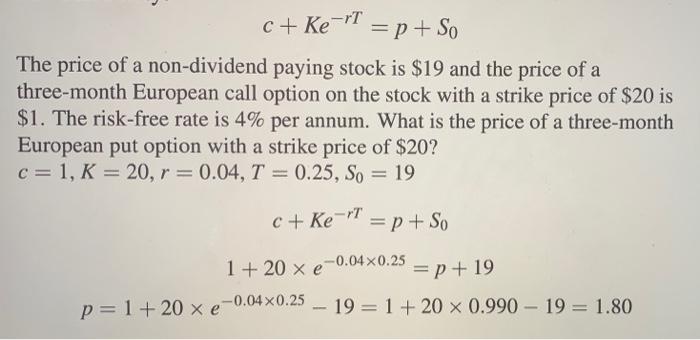

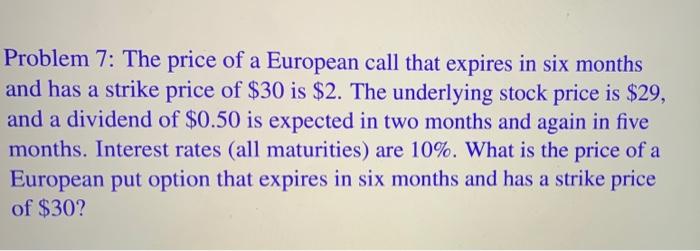

c+ Ke-IT = p + So The price of a non-dividend paying stock is $19 and the price of a three-month European call option on the stock with a strike price of $20 is $1. The risk-free rate is 4% per annum. What is the price of a three-month European put option with a strike price of $20? c=1, K = 20, r=0.04, T = 0.25, So = 19 c + Ke -'T = p + So 1+ 20 x e-0.04x0.25 = p + 19 p=1+20 x e-0.04x0.25 -- 19 = 1 + 20 x 0.990 19 = 1.80 Problem 7: The price of a European call that expires in six months and has a strike price of $30 is $2. The underlying stock price is $29, and a dividend of $0.50 is expected in two months and again in five months. Interest rates (all maturities) are 10%. What is the price of a European put option that expires in six months and has a strike price of $30

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts