Question: DO NOT use code 3.1 Exercise: Portfolio Optimization The expected returns of 2 assets are the following: The variance-covariance matrix between the assets () 3.1.2

DO NOT use code

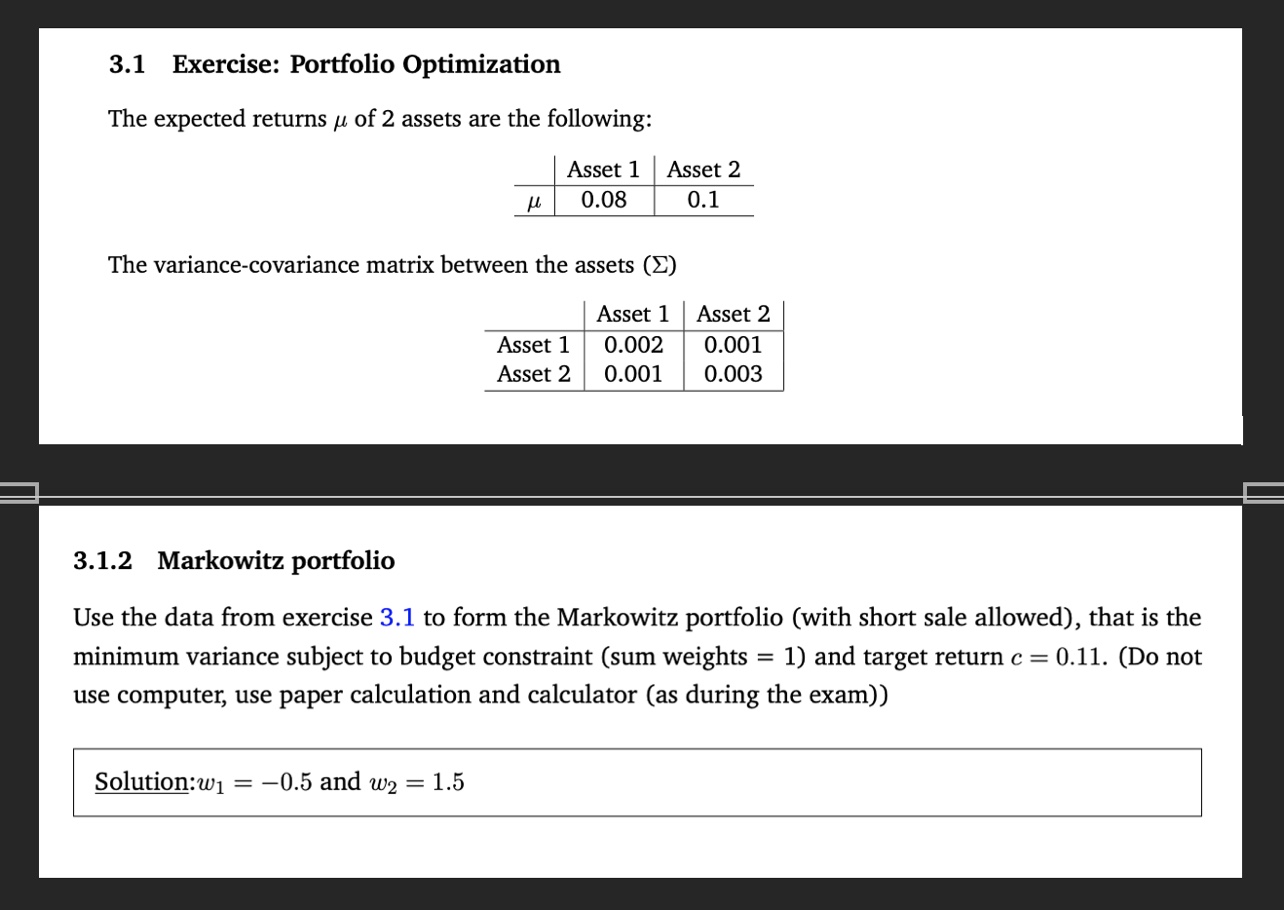

3.1 Exercise: Portfolio Optimization The expected returns of 2 assets are the following: The variance-covariance matrix between the assets () 3.1.2 Markowitz portfolio Use the data from exercise 3.1 to form the Markowitz portfolio (with short sale allowed), that is the minimum variance subject to budget constraint (sum weights =1 ) and target return c=0.11. (Do not use computer, use paper calculation and calculator (as during the exam))

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock