Question: DO NOT use code 3.1 Exercise: Portfolio Optimization The expected returns of 2 assets are the following: The variance-covariance matrix between the assets () 3.1.1

DO NOT use code

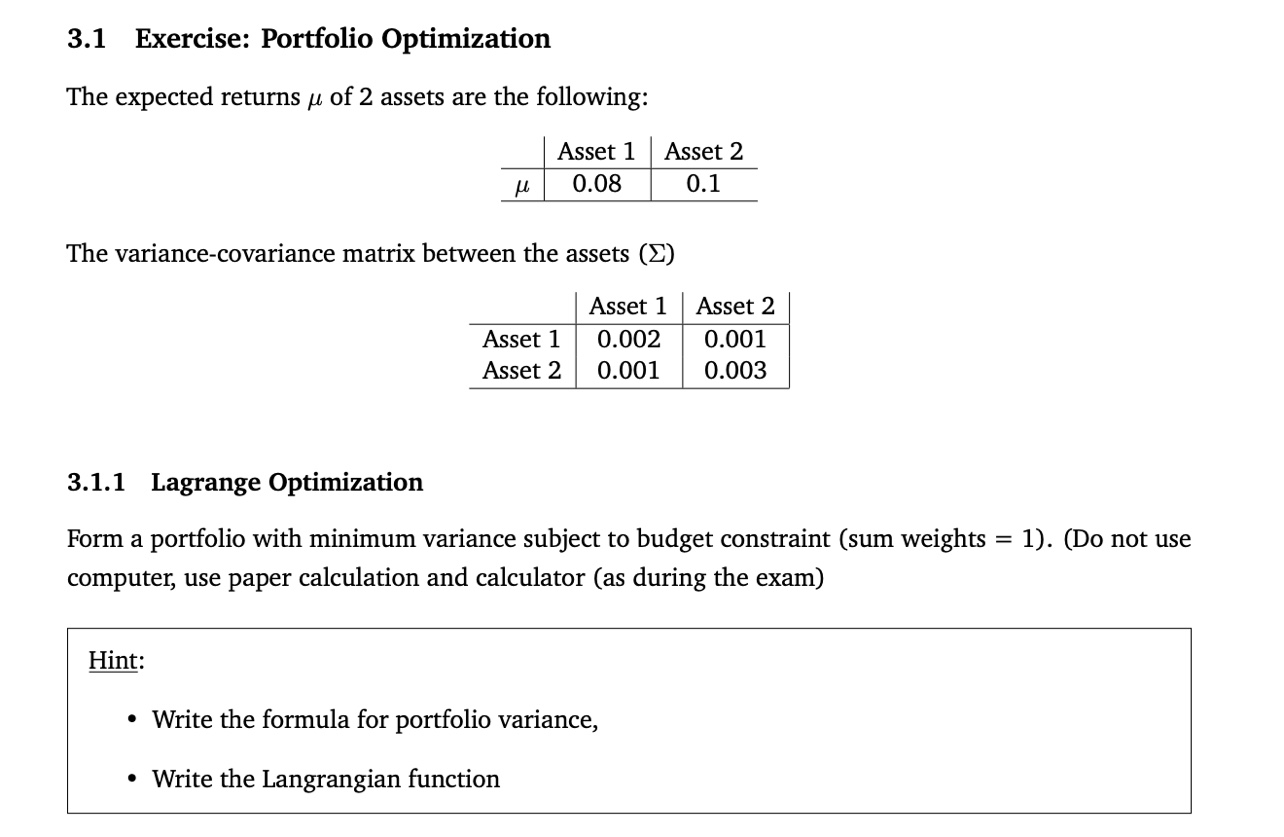

3.1 Exercise: Portfolio Optimization The expected returns of 2 assets are the following: The variance-covariance matrix between the assets () 3.1.1 Lagrange Optimization Form a portfolio with minimum variance subject to budget constraint (sum weights =1 ). (Do not use computer, use paper calculation and calculator (as during the exam) Hint: - Write the formula for portfolio variance, - Write the Langrangian function

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock