Question: by hand or python code The expected returns of 3 assets are the following: The variance-covariance matrix between the assets () 3.2.3 Markowitz portfolio The

by hand or python code

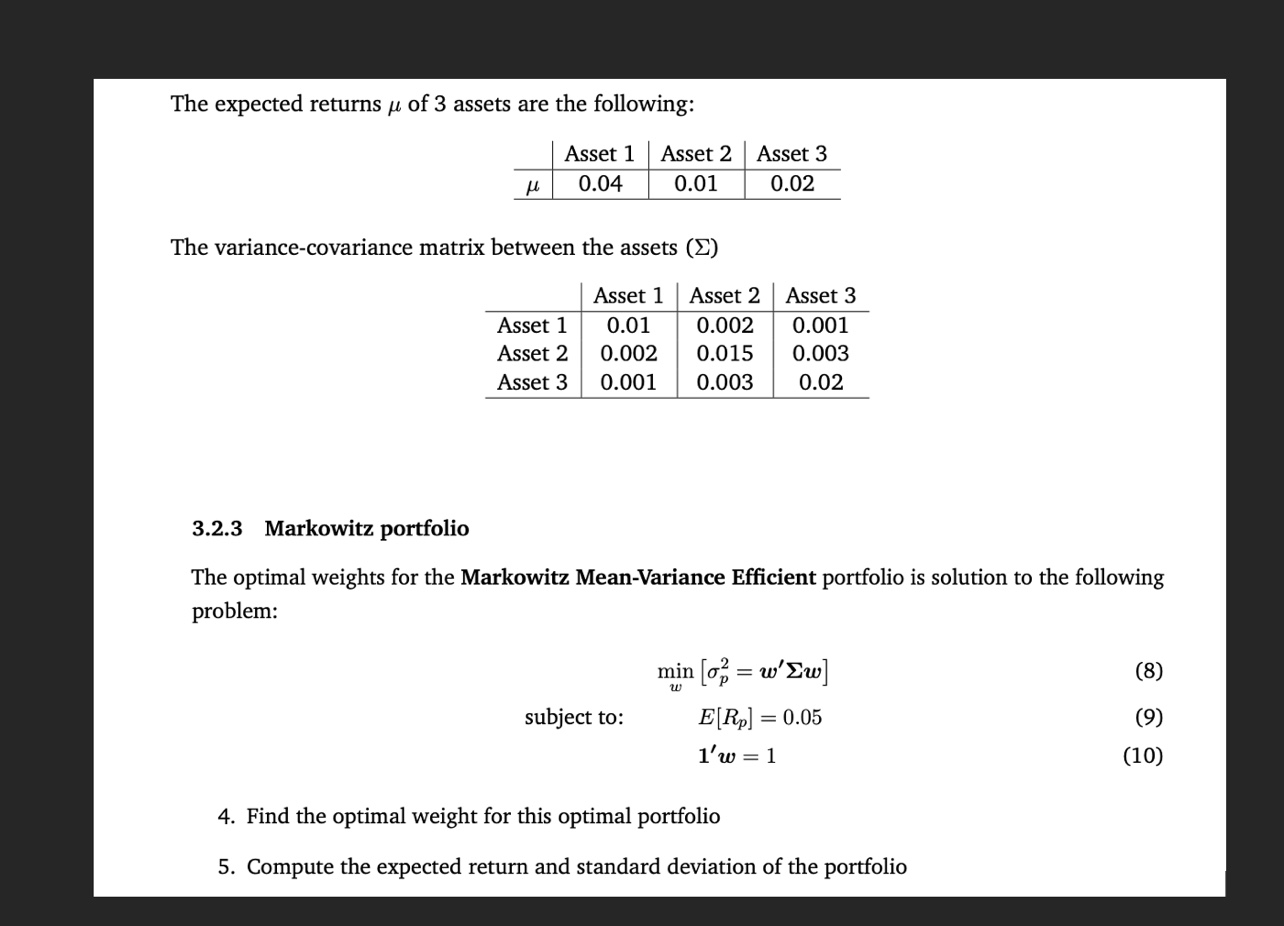

The expected returns of 3 assets are the following: The variance-covariance matrix between the assets () 3.2.3 Markowitz portfolio The optimal weights for the Markowitz Mean-Variance Efficient portfolio is solution to the following problem: subjectto:minw[p2=ww]E[Rp]=0.051w=1 4. Find the optimal weight for this optimal portfolio 5. Compute the expected return and standard deviation of the portfolio The expected returns of 3 assets are the following: The variance-covariance matrix between the assets () 3.2.3 Markowitz portfolio The optimal weights for the Markowitz Mean-Variance Efficient portfolio is solution to the following problem: subjectto:minw[p2=ww]E[Rp]=0.051w=1 4. Find the optimal weight for this optimal portfolio 5. Compute the expected return and standard deviation of the portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts