Question: help solve please solve the damn problem U.S. Dellar-Euro. The table. indicates that a 1-year cal option on euros at a strike rate of $1.2502=61.00

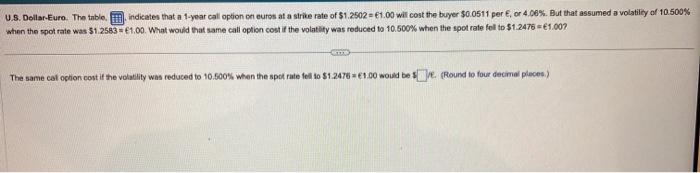

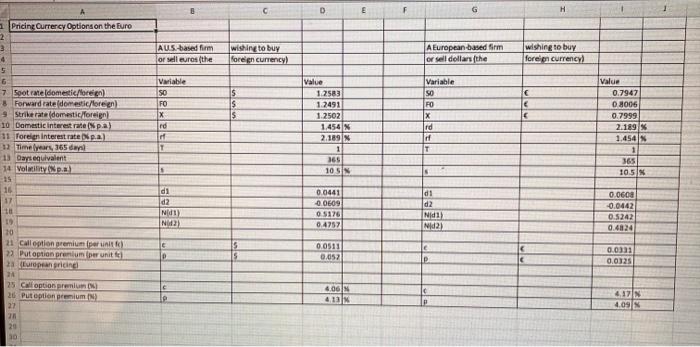

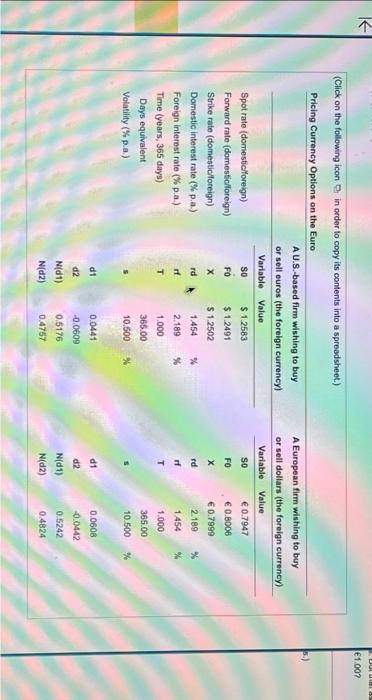

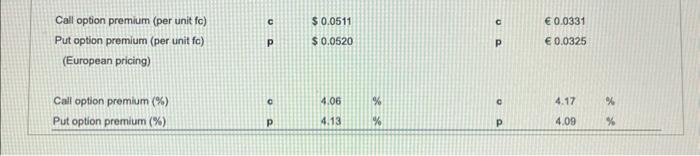

U.S. Dellar-Euro. The table. indicates that a 1-year cal option on euros at a strike rate of $1.2502=61.00 will cost the buyer $0.0511 per , or 4.06%. But that assumed a volatilicy of 10.500% when the spot rate was $1.2583=61.00. What would that same call option cost if the volatily was roduced to 10.500% when the spot rate fel to $1.2476=61.00? The same cat option cont if the volatility was reduced to 10.500% when the spot rate fell to $1.2476=61.00 would be 1 e. (Round to four decimal pleces.) (Click on the following icon , in order to copy its contents into a spreadsheet.) Call option premium (per unit fc) Put option premium (per unit fo) (European pricing) c $0.0511 p $0.0520 c 0.0331 p 0.0325 Call option premium (\%) Put option premium (\%) - 4.06 c 4.17 p 4.13 p 4.09 %

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts