Hickory Industries, a North Carolina-based firm, makes quality oak furniture (living room sets) and sells it to

Question:

Hickory Industries, a North Carolina-based firm, makes quality oak furniture (living room sets) and sells it to retailers throughout the eastern US. The firm is thinking about expanding to produce enough furniture to enter western markets. CFO Camila Garcia has come to you seeking help in analyzing the alternatives. In order to enter the western market, Garcia estimates that Hickory Furniture will need to increase its output by 60%. With existing production plants, Hickory can produce and sell 80,000 sets per year. While small increases in output are possible with the existing plant, an increase in output of 60% will necessitate building an additional plant. Two plans have been prepared. One plan calls for Hickory Furniture to build a new plant about 40 miles from the current plant (in North Carolina). The other plan calls for Hickory to build a plant closer to the large western markets in the southwest (New Mexico). Both plans will take some time to build and start production in year 2.

VP – Production Jon Snow wants to build the facility nearby. He feels he can adequately oversee both plants with the addition of two management level employees to his administrative staff. Of course, additional plant staff would be required. Once the new plant starts producing in year 2, Snow estimates that labor costs would run 33% of sales for this new plant (including all production workers plus the two new managers). VP – Marketing Anthony Williams has supported the alternative plan calling for a new plant to be built in New Mexico near several native American reservations.

Williams believes that the poor economy in the area will lower labor costs to 30% of sales. Fixed costs of administration and production of $25 million (measured in today’s $) will be incurred on an annual basis at the new plant in North Carolina. Snow contends that he will need to expand his staff further to undertake the New Mexico plan, and that he could incur additional costs for the new administrative staff and travel for the staff between New Mexico and corporate headquarters in Hickory. He estimates that this will raise fixed production costs to $31 million in today’s $ and on an annualized basis. These fixed costs are expected to increase at two-thirds of the inflation rate which is 2.5%. Materials costs are expected to be 18% of sales for either plant location. You will need additional net operating working capital of 15% of sales in each year to support the new operations, regardless of where you build the plant. In year 18, the remaining working capital will be liquidated at the book value and no tax needs to pay.

Williams points out that significant transportation costs will be entailed under Snow’s plan. Transporting completed furniture will add to the costs of operation (8% of sales). If the plant were built close to the populated western markets, you estimate that costs of transporting finished furniture would only be 5% of sales. Offsetting, this, however, is the cost of moving cut trees to the plant. There are no abundant forests of the right types of trees in the vicinity of any of the potential plant sites in the west; so cut trees would have to be transported from the Nantahala area to the western plant. Garcia tells you that it is much cheaper to transport cut trees than finished furniture. She suggests that transporting cut trees to the western plant is likely to cost 3% of sales. By comparison she says that transporting cut trees to the North Carolina sight ought to cost about 1% based on today’s rates.

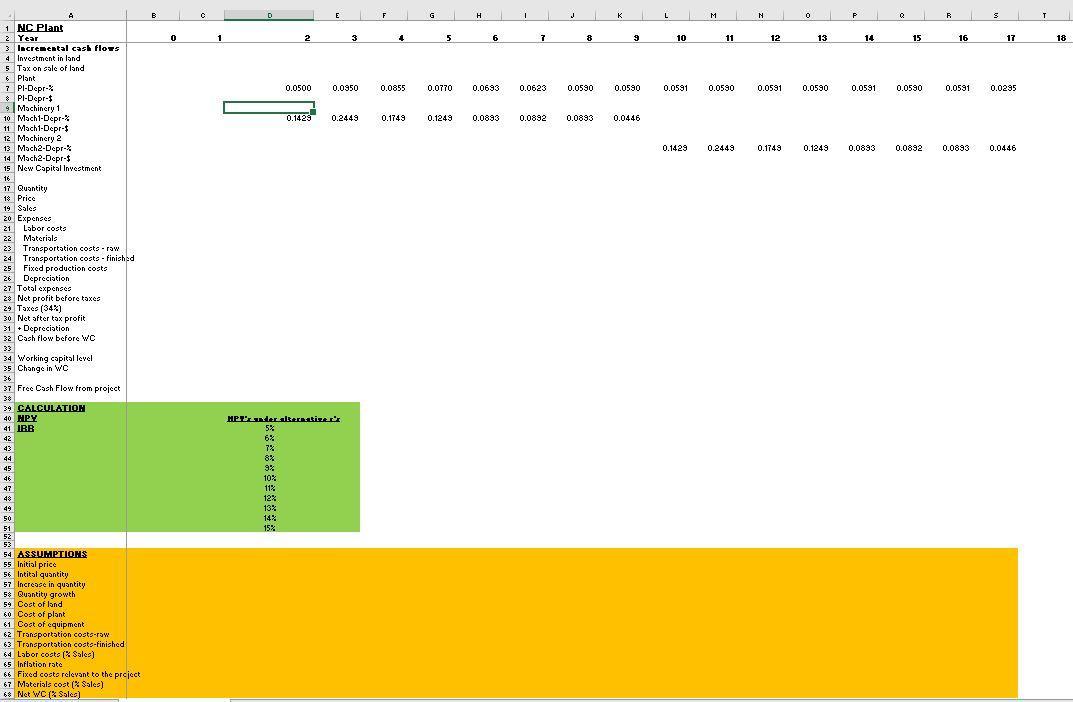

The land on which to build the plan will cost $12 million in North Carolina and $9 million in New Mexico, assuming that the firm acquires the required land immediately. The cost of building the plant will be $39 million in both places. A quarter of the cost of plant construction will be incurred immediately regardless of where the plant is built, one half of the cost will be incurred at the end of one year, and the final quarter of the cost will be incurred in year two. Regardless of where the plan is built, it will be depreciated beginning in year 2 based on the 15 year asset class. Assume the plant will shut down at that point (i.e., at the end of year 17) and the land can be sold the next year for its initial value adjusted for inflation. The company will need to pay tax on the capital gains on land. The plant will worth $0 and no additional cost or tax will need to be paid on the plant. Assume the gain on the land will be taxed at Hickory’s marginal tax rate of 34%.

Hickory will need $15 million of equipment at the end of year 1 to start production in year 2. The equipment will be depreciated over 7 years following the schedule attached. Hickory will purchase the equipment at time 1 so that it can used the equipment in production during year 2 and will claim the first year’s depreciation for year 2’s tax filing (the first year of operations). Hickory will need to replace the equipment in year 9. Assume that the cost of the equipment will rise at the expected rate of inflation of 2.5% and then the second equipment will also be depreciated on the 7-year schedule starting next year.

The plant will make no production in year 1 and will reach its full production in year 2. After year 2, the quantity is projected to grow at a rate of 3%. The 3% growth will last for 4 years. Due to market saturation and the expected performance of the west coast housing market, the output quantity will not grow between years 7 to 11 and will decrease at a rate of 2% per year beginning in year 12. The furniture set’s price in year 1 will be $2,000 and will increase at the inflation rate each year thereafter.

Compute free cash flow for each relevant year, and also NPV and IRR for both plans. Put them on different sheets and submit the excel file. Assume the required return for this project is 13%.

Depreciation Schedule Table:

TEMPLATE:

Expert Answer:

NPV CALCULATIONS North carolina plant YEAR 2 3 4 6 8 9 10 11 12 13 14 15 OutputUnits Rate Total sale... View the full answer

Macroeconomics

ISBN: 978-1464168505

5th Canadian Edition

Authors: N. Gregory Mankiw, William M. Scarth