Question: https://www.chegg.com/homework-help/questions-and-answers/hand-python-code-q112721362?new=true 3.2 Computation: Portfolio Optimization The expected returns of 3 assets are the following: The variance-covariance matrix between the assets () 3.2.1 Equally weighted portfolio

https://www.chegg.com/homework-help/questions-and-answers/hand-python-code-q112721362?new=true

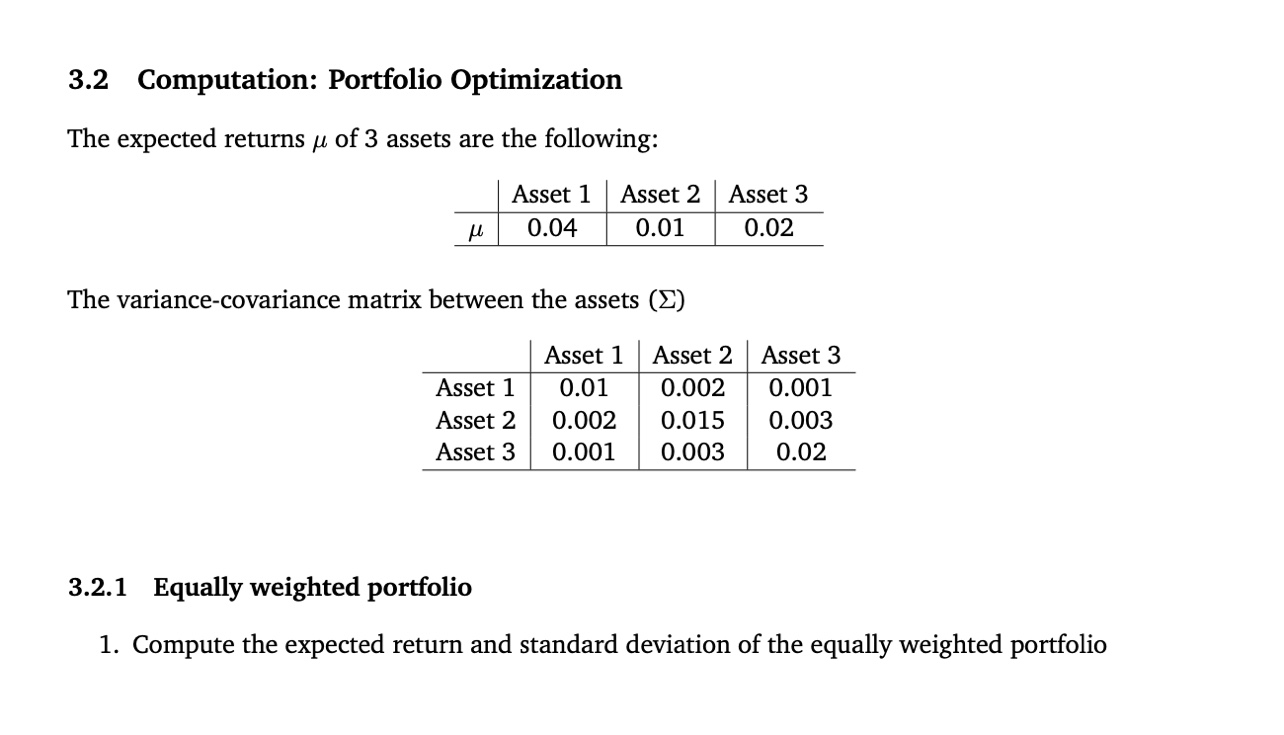

3.2 Computation: Portfolio Optimization The expected returns of 3 assets are the following: The variance-covariance matrix between the assets () 3.2.1 Equally weighted portfolio 1. Compute the expected return and standard deviation of the equally weighted portfolio 3.2 Computation: Portfolio Optimization The expected returns of 3 assets are the following: The variance-covariance matrix between the assets () 3.2.1 Equally weighted portfolio 1. Compute the expected return and standard deviation of the equally weighted portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock