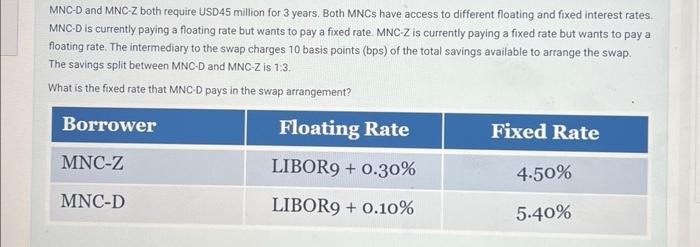

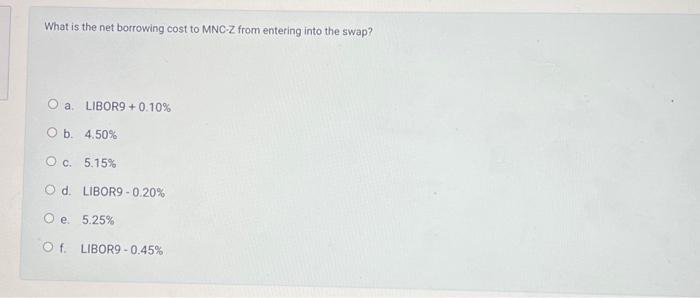

Question: MNC-D and MNC-Z both require USD 45 million for 3 years. Both MNCs have access to different floating and fixed interest rates. MNC-D is currently

MNC-D and MNC-Z both require USD 45 million for 3 years. Both MNCs have access to different floating and fixed interest rates. MNC-D is currently paying a floating rate but wants to pay a fixed rate. MNC-Z is currently paying a fixed rate but wants to pay a floating rate. The intermediary to the swap charges 10 basis points (bps) of the total savings available to arrange the swap. The savings split between MNC-D and MNC-Z is 1:3. What is the fixed rate that MNC.D pays in the swap arrangement? What is the net borrowing cost to MNC-Z from entering into the swap? a. LIBOR 9+0.10% b. 4.50% C. 5.15% d. LIBOR9-0.20\% e. 5.25% f. LIBOR90.45%

Step by Step Solution

There are 3 Steps involved in it

To solve this problem we need to analyze the interest rates and the swap structure considering the c... View full answer

Get step-by-step solutions from verified subject matter experts