Question: Please DO NOT use Excel! Portfolio Analysis 1) Imagine that you have 10,000 to invest. What would be the combination of Asset A and Asset

Please DO NOT use Excel!

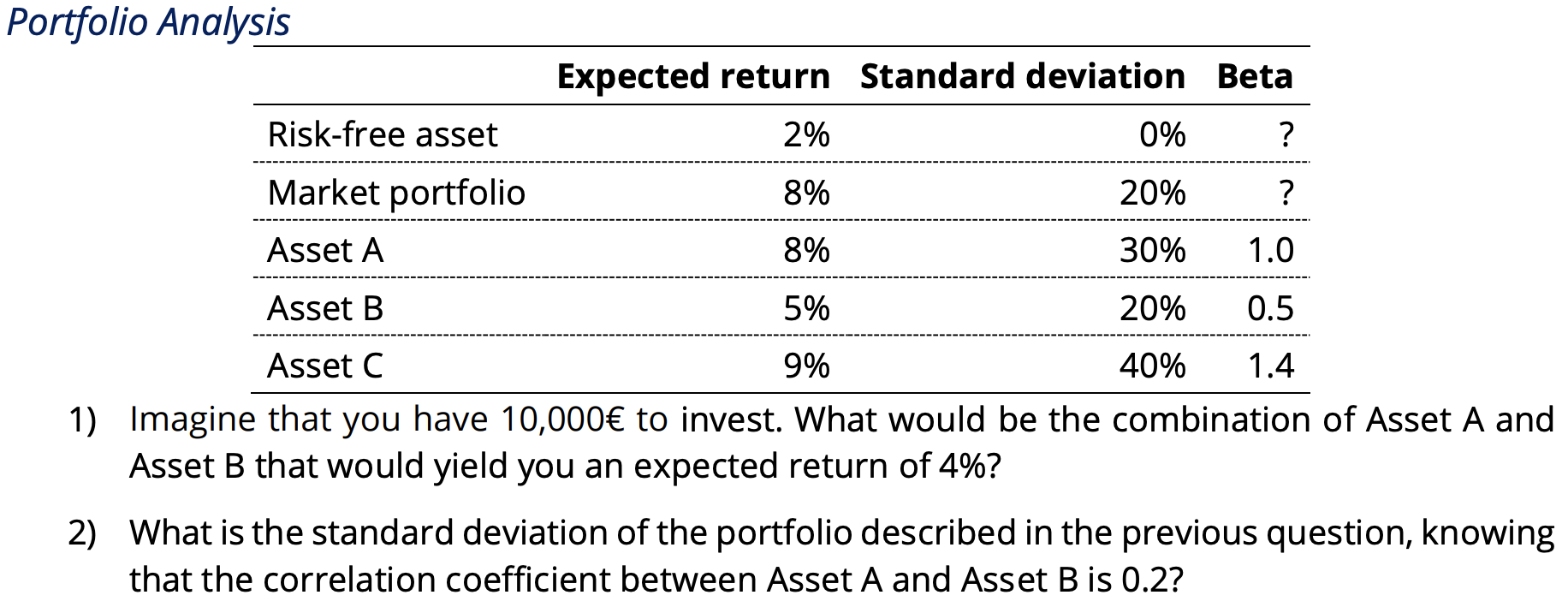

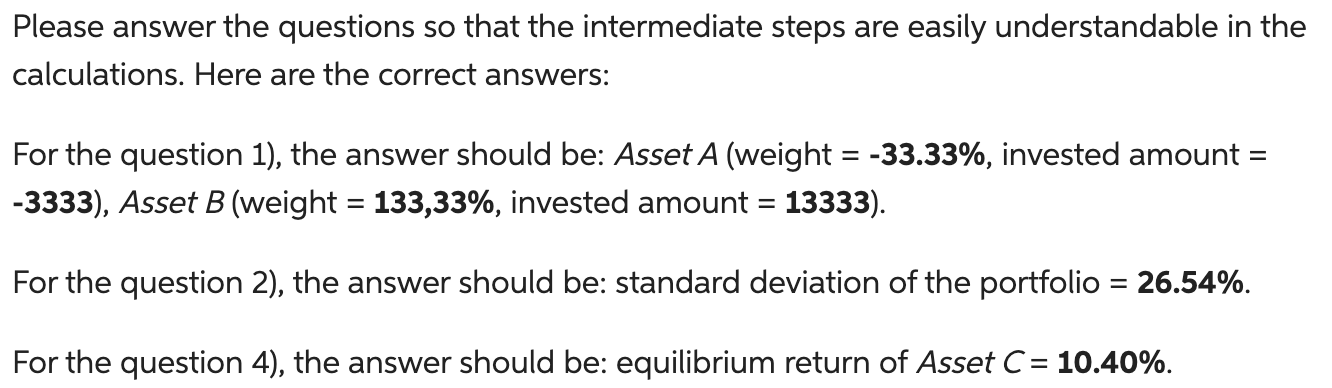

Portfolio Analysis 1) Imagine that you have 10,000 to invest. What would be the combination of Asset A and Asset B that would yield you an expected return of 4% ? 2) What is the standard deviation of the portfolio described in the previous question, knowing that the correlation coefficient between Asset A and Asset B is 0.2? Is asset C in equilibrium? Explain what will happen to the value of the asset, including your detailed rationale, assuming that the market is efficient. Please answer the questions so that the intermediate steps are easily understandable in the calculations. Here are the correct answers: For the question 1), the answer should be: Asset A (weight =33.33%, invested amount = -3333), Asset B (weight =133,33%, invested amount =13333 ). For the question 2), the answer should be: standard deviation of the portfolio 26.54%. For the question 4), the answer should be: equilibrium return of AssetC=10.40%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts