Question: Please explain.... Suppose an investor with utility function u(R) = E(RP)0.5, where E (RP) is the expected return on the portfolio P. The investor wishes

Please explain.... Suppose an investor with utility function u(R) = E(RP)0.5, where E (RP) is the expected return on the portfolio P. The investor wishes to invest in a portfolio that combines the three stocks from Exhibit 7.2a Will he or she prefer an equal-weighted average of the three stocks to holding stocks 2 and 3 only. with corresponding portfolio weights (0;1/4;3/4)?

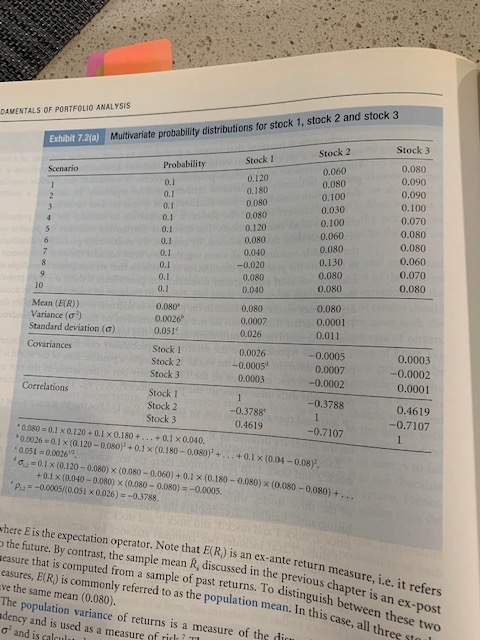

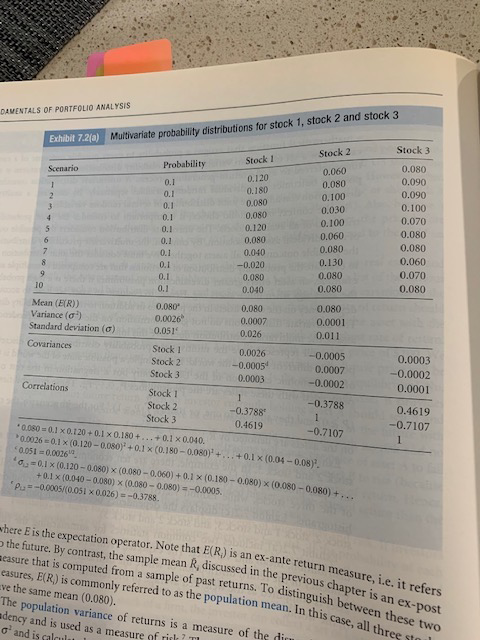

DOUCHTAL'S OF PORTFOLIO ANALYSIS `I !`#` ! Multivariate probability distributions for stock; 1 . stock ?' and stock } Probability Stock ! Stock 2) 1 . 1 21. 120 \1.1 0. 180 Q.OBD 1. 1 0. 10.0 121 1.030 1. 1.010 1 1. !` 0. 120 \1.1 0.040 01 . 130 1 . 1 1 . 980 1. 1 Variance / {`! 2.05.15 1.01 1 Stock ?` - 17 . 010.05^ Correlations* Stock !) Stock ?) Stock }} - 01. 37 8BY 0. 1619 '```` = 1.1 * 0. 120 + 0. 1 x 0.150 + ... + 0. 1 {``ID.` 101. 4619 - 0. 7107 -0. 7107 1 \} }In` = 1500^ #` = 0.1*: 10.120 - 1. 0401 x condo - 1. 4Adj + 0. 1 x 10.180 - 1.ob`^ ^`so - O. JBoj + ... where Eis the expectation operator . Note that Elm` is an ex- anke return measure , i.e. it refers " the future . By contrast , the simple mean { discussed in the previous chapter is an ex - post Frasure that is computed from a sample of past returns . To distinguish between these two I've the same mean ( 1 . 080) . abures , EIRI is commonly referred to as the population mean . In this case, all themap ^ The population variance of returns is a measure of the if "dency and is used as a measure fif ! I and is calm

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts