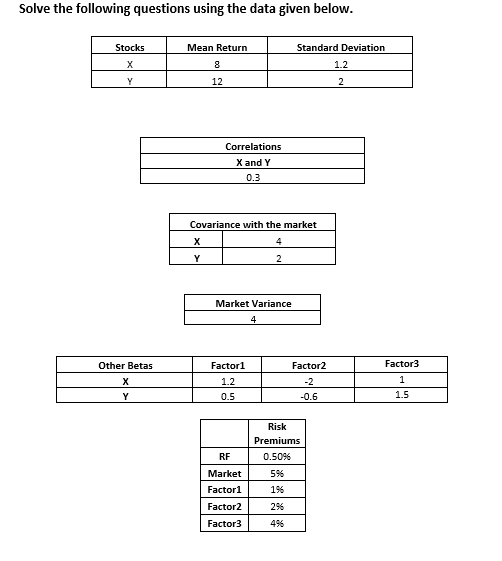

Question: Please help!!! Solve the following questions using the data given below. Stocks Mean Return Standard Deviation X 1.2 12 2 Correlations X and Y 0.3

Please help!!!

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock