Question: Please show workings so I can understand how you got the answer - thank you ! 7. You are valuing a fixed-floating swap established 2

Please show workings so I can understand how you got the answer - thank you !

Please show workings so I can understand how you got the answer - thank you !

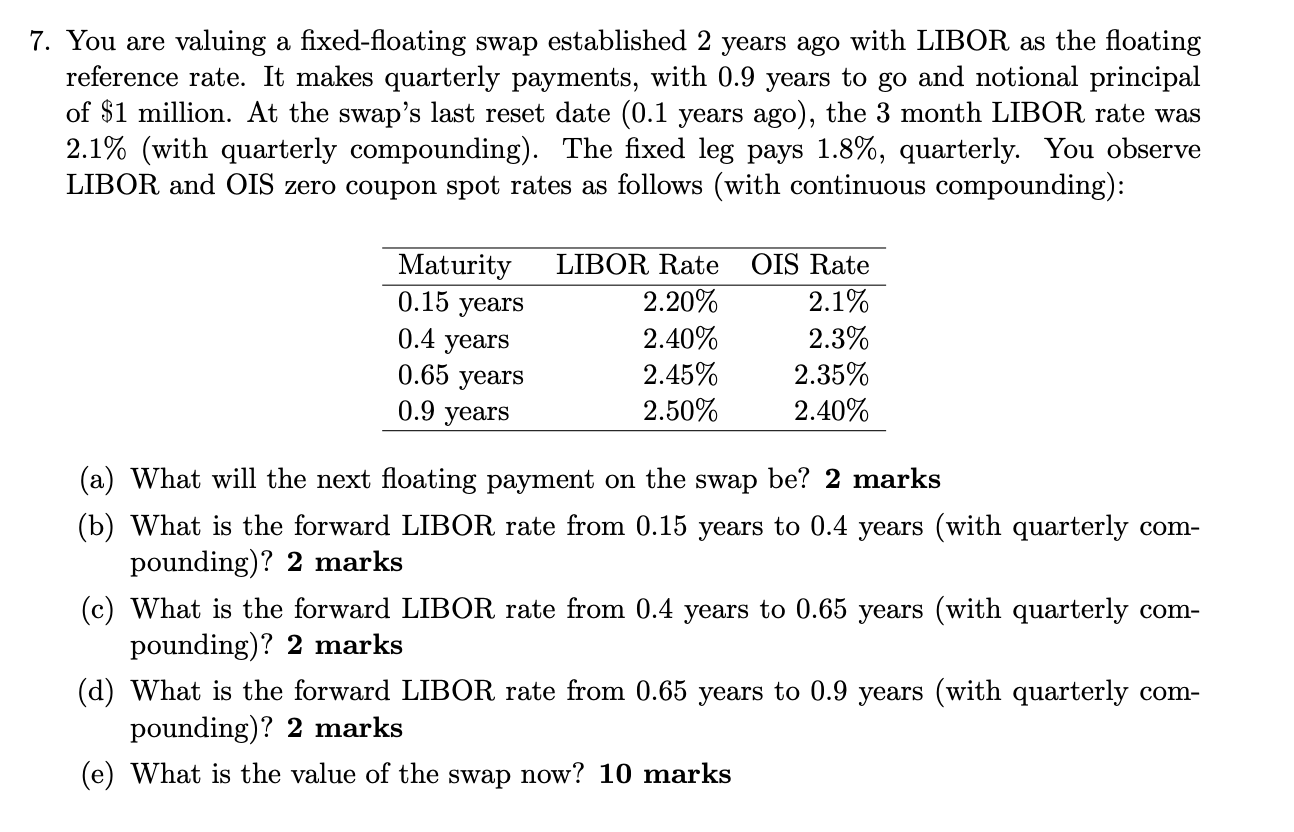

7. You are valuing a fixed-floating swap established 2 years ago with LIBOR as the floating reference rate. It makes quarterly payments, with 0.9 years to go and notional principal of $1 million. At the swap's last reset date (0.1 years ago), the 3 month LIBOR rate was 2.1% (with quarterly compounding). The fixed leg pays 1.8%, quarterly. You observe LIBOR and OIS zero coupon spot rates as follows (with continuous compounding): (a) What will the next floating payment on the swap be? 2 marks (b) What is the forward LIBOR rate from 0.15 years to 0.4 years (with quarterly compounding)? 2 marks (c) What is the forward LIBOR rate from 0.4 years to 0.65 years (with quarterly compounding)? 2 marks (d) What is the forward LIBOR rate from 0.65 years to 0.9 years (with quarterly compounding)? 2 marks (e) What is the value of the swap now? 10 marks 7. You are valuing a fixed-floating swap established 2 years ago with LIBOR as the floating reference rate. It makes quarterly payments, with 0.9 years to go and notional principal of $1 million. At the swap's last reset date (0.1 years ago), the 3 month LIBOR rate was 2.1% (with quarterly compounding). The fixed leg pays 1.8%, quarterly. You observe LIBOR and OIS zero coupon spot rates as follows (with continuous compounding): (a) What will the next floating payment on the swap be? 2 marks (b) What is the forward LIBOR rate from 0.15 years to 0.4 years (with quarterly compounding)? 2 marks (c) What is the forward LIBOR rate from 0.4 years to 0.65 years (with quarterly compounding)? 2 marks (d) What is the forward LIBOR rate from 0.65 years to 0.9 years (with quarterly compounding)? 2 marks (e) What is the value of the swap now? 10 marks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts