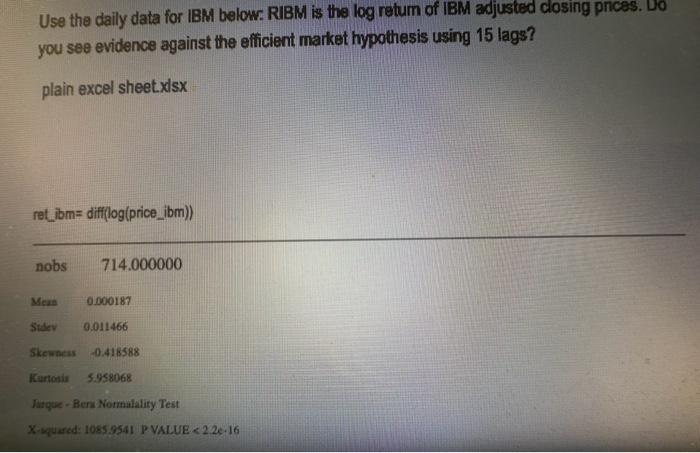

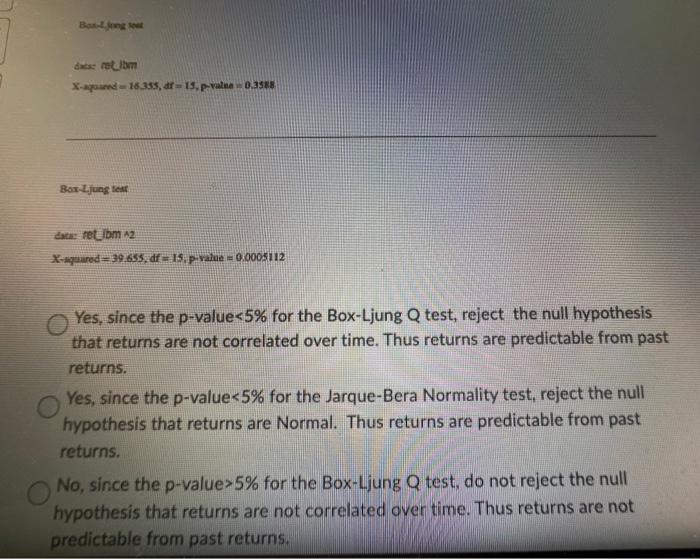

Question: Use the daily data for IBM below. RIBM is the log retum of IBM adjusted closing prices. Lo you see evidence against the efficient market

Use the daily data for IBM below. RIBM is the log retum of IBM adjusted closing prices. Lo you see evidence against the efficient market hypothesis using 15 lags? plain excel sheet x ssx ret__bm= difflog(price_ibm)) dacse tek olvert x-apournd =18.355, df =19,p valne w0,3518 Box-t.jung text Late: Fet Ion 12 K-MMured =39.655,df=15, piratue =0.0005112 Yes, since the p-value 5% for the Box-Ljung Q test, reject the null hypothesis that returns are not correlated over time. Thus returns are predictable from past returns. Yes, since the p-value 5% for the BoxLjung,Q test, do not reject the null hypothesis that returns are not correlated over time. Thus returns are not Use the daily data for IBM below. RIBM is the log retum of IBM adjusted closing prices. Lo you see evidence against the efficient market hypothesis using 15 lags? plain excel sheet x ssx ret__bm= difflog(price_ibm)) dacse tek olvert x-apournd =18.355, df =19,p valne w0,3518 Box-t.jung text Late: Fet Ion 12 K-MMured =39.655,df=15, piratue =0.0005112 Yes, since the p-value 5% for the Box-Ljung Q test, reject the null hypothesis that returns are not correlated over time. Thus returns are predictable from past returns. Yes, since the p-value 5% for the BoxLjung,Q test, do not reject the null hypothesis that returns are not correlated over time. Thus returns are not

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts