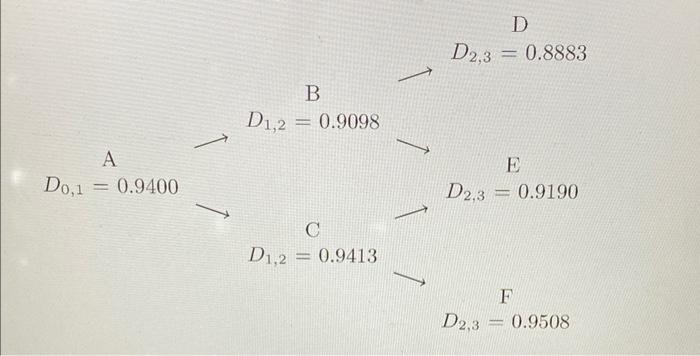

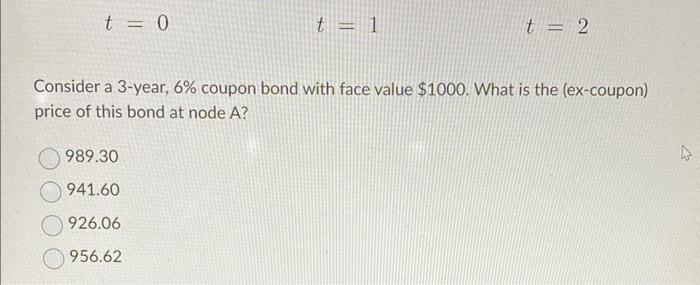

Question: Using the following short-term discount factor tree implied by the Ho-Lee model: DD2,3=0.8883BAD1,2=0.9098D0,1=0.9400D2,3=0.9190D1,2=0.9413FD2,3=0.9508 t=0t=1t=2 Consider a 3-year, 6% coupon bond with face value $1000. What

Using the following short-term discount factor tree implied by the Ho-Lee model:

DD2,3=0.8883BAD1,2=0.9098D0,1=0.9400D2,3=0.9190D1,2=0.9413FD2,3=0.9508 t=0t=1t=2 Consider a 3-year, 6\% coupon bond with face value $1000. What is the (ex-coupon) price of this bond at node A ? 989.30941.60926.06956.62

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock