New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

advanced financial accounting

Advanced Financial Accounting 5th Edition Richard E. Baker, Valdean C. Lembke, Thomas E. King - Solutions

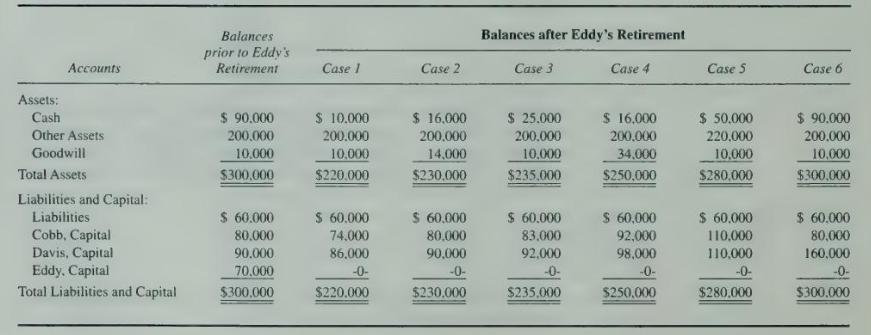

On January 1, 20X1. Eddy decides to retire from the partnership of Cobb, Davis, and Eddy, who share profits and losses in the ratio of \(3: 2: 1\) respectively. The following condensed balance sheets present the account balances immediately before and, for six independent cases, after Eddy's

Debra and Merina sell electronic equipment and supplies through their partnership. They wish to expand their computer lines and decide to admit Wayne to the partnership. Debra's capital is \(\$ 200,000\), Merina's capital is \(\$ 160,000\), and they share income in a ratio of \(3: 2\),

C. Eastwood, A. North, and M. West are manufacturers' representatives in the architecture business. Their capital accounts in the ENW partnership for \(20 \mathrm{X} 1\) were as follows:\section*{Required}For each of the following independent income-sharing agreements, prepare an income

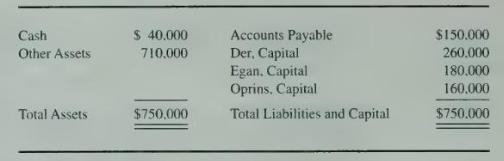

The following condensed balance sheet is presented for the partnership of Der. Egan, and Oprins, who share profits and losses in the ratio of \(4: 3: 3\), respectively.Assume that the partnership decides to admit Snider as a new partner with a one-fourth interest.\section*{Required}For each of the

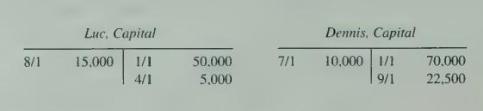

The Champion Play Company is a partnership that sells sporting goods. The partnership agreement provides for 10 percent interest on invested capital, salaries of \(\$ 24,000\) to Luc and \(\$ 28,000\) to Dennis and a bonus for Luc. The 20X3 capital accounts were as follows:\section*{Required}For

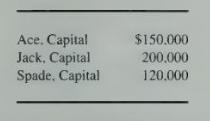

The partnership of Ace, Jack, and Spade has been in business for 25 years. On December 31, 20X5, Spade decided to retire from the partnership. The partnership balance sheet reported the following capital balances for each partner at December 31, 20X5:The partners allocate partnership income and

Select the correct answer for each of the following questions.1. When property other than cash is invested in a partnership, at what amount should the noncash property be credited to the contributing partner's capital account?a. Contributing partner's tax basis.b. Contributing partner's original

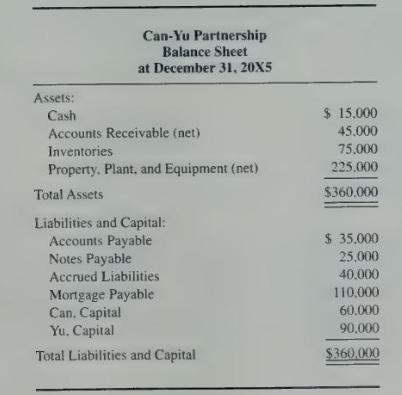

The balance sheet of the Can-Yu Partnership at December 31, 20X5, appears below:Can and Yu share profits and losses in the ratio 30:70. On January 1, 20X6. Sea was admitted into the partnership.\section*{Required}Prepare journal entries for the admission of Sea for each of the following independent

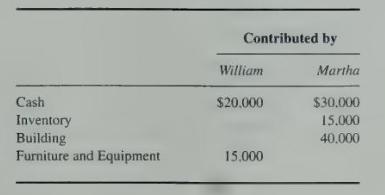

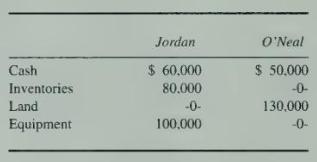

The partnership of Jordan and O'Neal began business on January 1, 20X7. The following assets were contributed by each partner (the noncash assets are stated at their fair values on January 1, 20X7):The land was subject to a \(\$ 50,000\) mortgage, which the partnership assumed on January 1, 20X7.

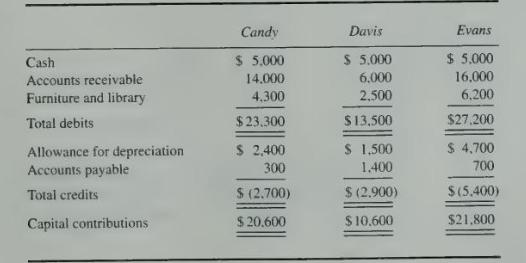

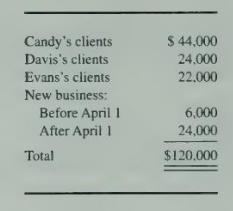

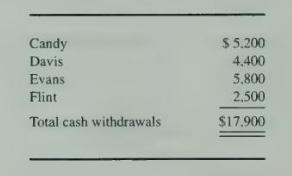

Candy, Davis, and Evans, who are accountants, agreed to combine their individual practices into a partnership as of January 1,20X3. The partnership includes the following features.1. Each partner's capital contribution was the net amount of assets and liabilities taken over by the partnership,

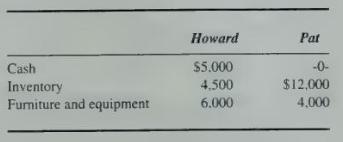

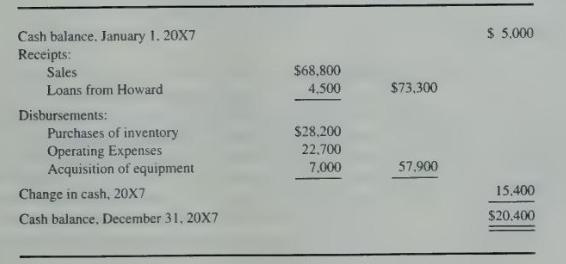

The Glidden Manufacturing Company was organized as a partnership by Howard and Pat on January 1, 20X7, and has operated for one year. At the time the partnership was formed, Howard and Pat made the following investments:Howard and Pat share profits and losses equally. On December 31, 20X7, they

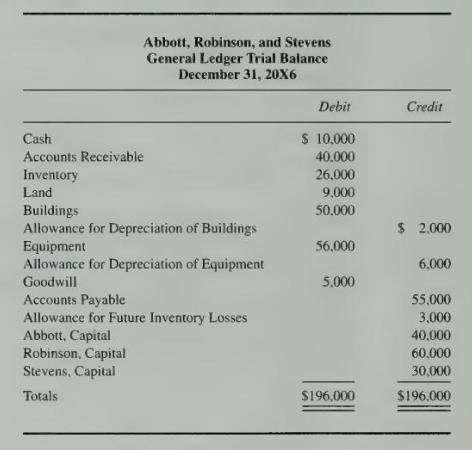

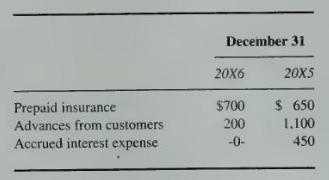

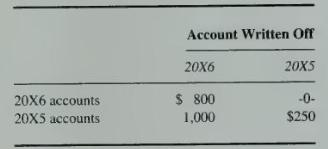

The partnership of Abbott, Robinson, and Stevens engaged you to adjust its accounting records and convert them uniformly to the accrual basis in anticipation of admitting Kingston as a new partner. Some accounts are on the accrual basis and others are on the cash basis. The partnership's books were

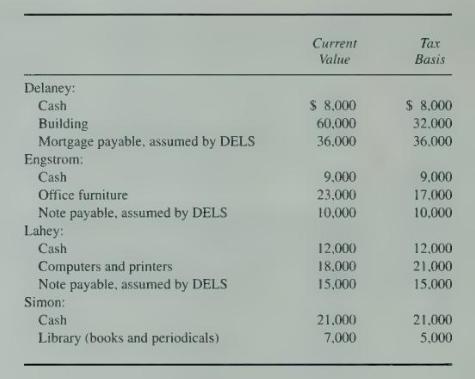

The DELS partnership was formed by combining individual accounting practices on May 10, 20X1. The initial investments were as follows:\section*{Required}a. Prepare the journal entry to record the initial investments, using GAAP accounting.b. Calculate the tax basis of each partner's capital if

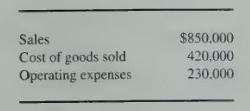

Chemax Inc. manufactures a wide variety of pharmaceuticals, medical instruments, and other related medical supplies. Eighteen months ago the company developed and began to market a new product line of antihistamine drugs under various trade names. Sales and profitability of this product line during

Periodic reporting adds complexity to accounting by requiring estimates, accruals, deferrals, and allocations. Interim reporting creates even greater difficulties in matching revenue and expenses.\section*{Required}a. Explain how revenue, product costs, gains, and losses should be recognized for

Bennett Inc. is a publicly held corporation whose diversified operations have been separated into five industry segments. Bennett is in the process of preparing its annual financial statements for the year ended December 31,20X5. The following information has been collected for the preparation of

A major producer of cereal breakfast foods had been reporting in its annual reports just one dominant product line (cereals) in only the U.S. domestic geographic area. The company had no other separately reportable segments. For several years, the U.S. company had a Canadian subsidiary that

The manager you work for has asked you to perform some research to determine what types of information public companies are providing on their Internet home pages. The public company you work for is considering establishing their own home page. In particular the manager wants you to note how these

The company you work for is considering going public. Your current position is within the external financial reporting group. The manager you work for wants you to review some public company quarterly reports. Form 10-Qs, to see what type of information is disclosed. The manager does not want you

Amalgamated Products has seven operating segments. Data on the segments are as follows:Included in the \(\$ 105,000\) revenue of the Bicycles segment are sales of \(\$ 25.000\) made to the Sporting Goods segment.\section*{Required}a. Indicate which segments are reportable.b. Do the reportable

Select the correct answer for each of the following questions.1. Barbee Corporation discloses supplementary operating segment information for its two reportable segments. Data for \(20 \mathrm{X} 5\) are available as follows:Additional \(20 \mathrm{X} 5\) expenses are as follows:Appropriately

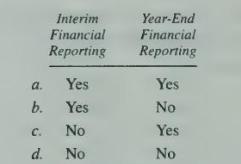

Select the correct answer for each of the following questions.1. In considering interim financial reporting, how did the Accounting Principles Board conclude that such reporting should be viewed?a. As a "special" type of reporting that need not follow generally accepted accounting principles.b. As

During June, Kissick Hardware, which uses a perpetual inventory system, sold 920 units from its LIFO-base inventory, which had originally cost \(\$ 12\) per unit. The replacement cost is expected to be \(\$ 21\) per unit. Kissick is reducing inventory levels, and expects to replace only 640 of

Comeback Company, a calendar-year entity, had 9,000 medical instruments in its beginning inventory for \(20 \mathrm{X} 2\). On December 31. 20X1, the instruments had been adjusted down to \(\$ 10.20\) per unit, which was the lower of average cost or market, from an actual average cost of \(\$

Select the correct answer for each of the following questions.1. According to APB Opinion No. 28, "Interim Financial Reporting," income tax expense in an income statement for the first interim period of an enterprise's fiscal year should be computed by:a. Applying the estimated income tax rate for

Information about the domestic and foreign operations of Radon Inc. is as follows:\section*{Required}Prepare schedules showing appropriate tests to determine which countries are material, using a 10 percent materiality threshold. Sales to unaffiliated Geographic Area United States Britain Brazil

Sales by Knight Inc. to major customers are as follows:\section*{Required}If worldwide sales total \(\$ 43,000,000\) for the year, which of Knight's customers should be disclosed as major customers? Customer State of Illinois Sales Reporting Segment $2.700,000 Computer hardware Cook County,

World Inc. estimates total federal and state tax rates to be 50 percent. World's first-quarter earnings are \(\$ 300,000\) and expected annual earnings are \(\$ 1,500,000\). For the year, premiums for life insurance on officers will be \(\$ 60,000\), and dividend exclusions are expected to be \(\$

Tem Technology has a first-quarter operating loss of \(\$ 100,000\) and expects the following income for the other three quarters:Tem estimated the effective annual tax rate at 40 percent at the end of the first quarter and changed it to 45 percent at the end of the third quarter. The company has a

Badger Corporation has prepared the following data, in thousands of dollars, for its industry segments for the year ended December 31, 20X4:\section*{Required}a. Apply the three 10 percent significance tests to determine which of the segments are separately reportable. The chief operating decision

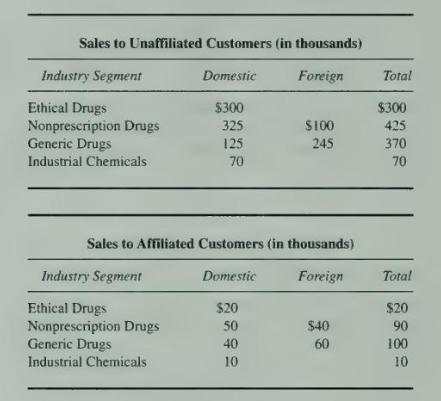

The Symbiotic Chemical Company has four major industry segments and operates both in the U.S. domestic market and in several foreign markets. Information about its revenue from the specific industry segments and its foreign activities for the year \(20 \times 2\) is as follows:All the foreign

Listed below are six independent cases on how accounting facts might be reported on an individual company's interim financial reports.a. Bean Company was reasonably certain it would have an employee strike in the third quarter. As a result. the company shipped heavily during the second quarter but

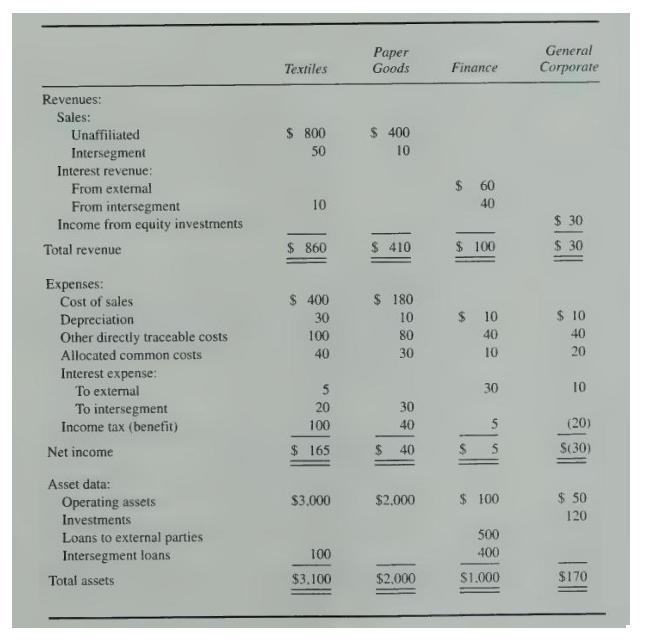

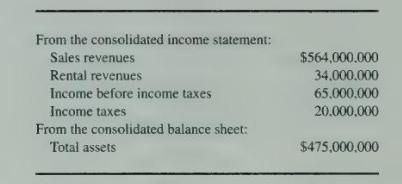

West Corporation reported the following consolidated data for \(20 \mathrm{X} 2\) :Data reported for West's four operating divisions are as follows:Intersegment sales are priced at cost, and all goods have been subsequently sold to nonaffiliates. Some joint production costs are allocated to the

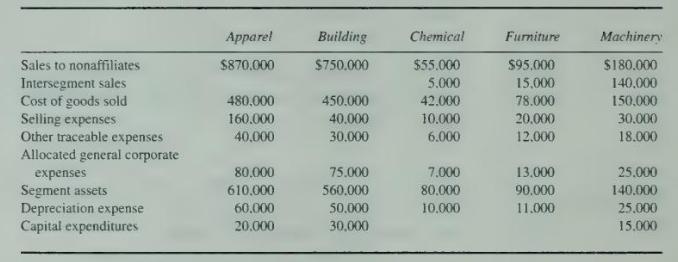

Calvin Inc. has operating segments in five different industries: apparel, building, chemical, furniture, and machinery. Data for the five segments for 20X1 are as follows:1. The corporate headquarters had general corporate expenses totaling \(\$ 235,000\). For internal reporting purposes, \(\$

Chris Inc. has accumulated information for its second-quarter income statement for 20X2:1. First-quarter income before taxes was \(\$ 100,000\), and the estimated effective annual tax rate was 40 percent. At the end of the second quarter, expected annual income is \(\$ 600,000\), and a dividend

At the end of the second quarter of 20X1, Malta Corporation assembled the following information:1. The first quarter resulted in a \(\$ 90,000\) loss before taxes. During the second quarter, sales were \(\$ 1,200,000\); purchases were \(\$ 650,000\); and operating expenses were \(\$ 320,000\).2.

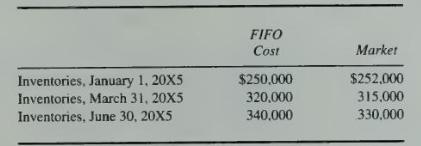

Burrows Company is in the process of preparing its income statement for the quarter ended June 30, 20X5. The following information was assembled for the period April 1 through June 30, 20X5-the second quarter of the year:1. The management of Burrows believes that the \(\$ 100,000 \mathrm{LIFO}\)

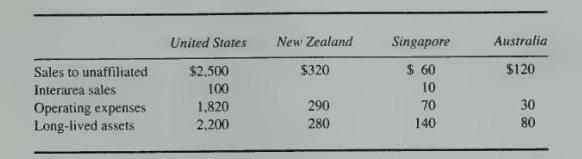

For many years, the Clark Company operated exclusively in the United States, but recently it expanded its operations to the Pacific Rim countries of New Zealand, Singapore, and Australia. After a modest beginning in these countries, recent successes have resulted in an increased level of operations

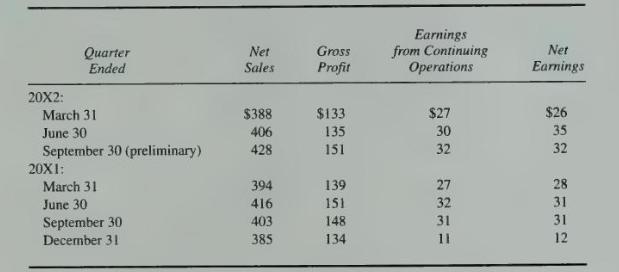

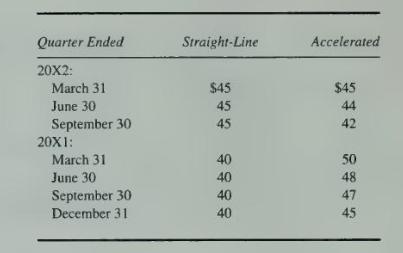

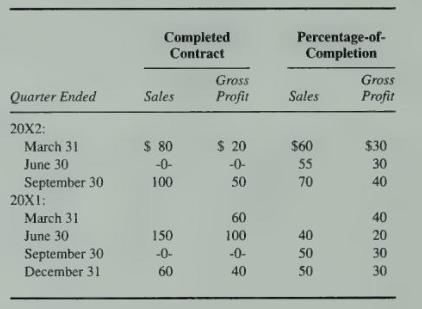

During the third quarter of its \(20 \mathrm{X} 2\) fiscal year, the Square Q Company is considering the methods of accounting for accounting changes on its interim statements. Preliminary data are available for the third quarter of \(20 \times 2\), ending on September 30, 20X2, prior to any

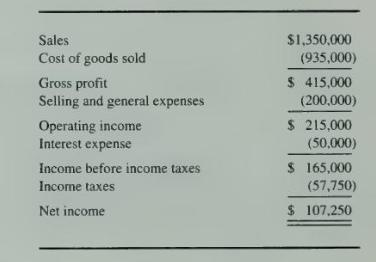

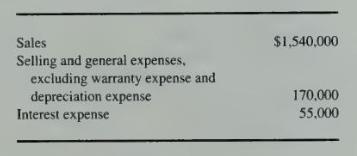

Burnell Inc. reported the following income statement for the quarter ended March 31, 20X5:The following events occurred during the second quarter:1. Burnell warranties its products for one year after sale. The company has accrued warranty expense at the rate of 3 percent of sales, and \(\$ 40,500\)

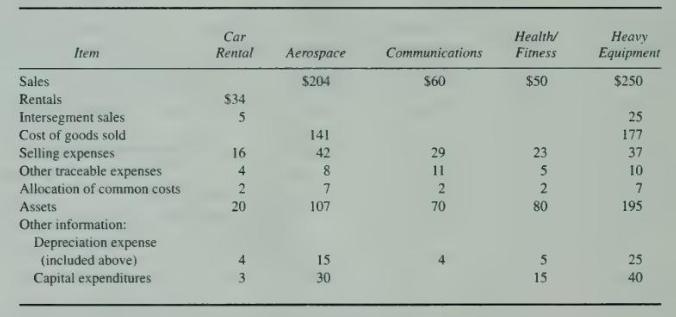

Multiplex Inc., a public company whose stock is traded on a national stock exchange, reported the following information on its consolidated financial statements for 20X5:The management of Multiplex determined that it had the following operating segments during 20X5: (1) car rental, (2) aerospace,

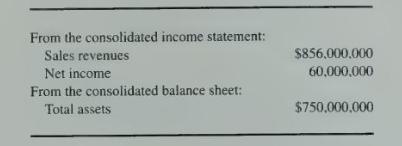

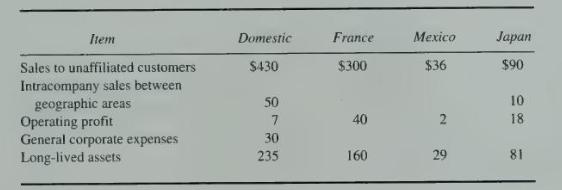

Watson Inc., a multinational company, has operating divisions in France, Mexico, and Japan as well as in the United States. The company reported the following information on its consolidated financial statements for 20X5:The following additional information was assembled for Watson's domestic and

Which securities act-the 1933 or 1934 act-regulates the initial registration of securities? Which regulates the periodic reporting of publicly traded companies?

What are the objectives of the integrated disclosure system?

Present the five major items included in the basic information package.

What types of public offerings of securities are exempted from the comprehensive registration requirements of the \(\mathrm{SEC}\) ?

When can a company use a Form S-1 registration form? In what circumstances must the company use a Form S-3 registration form?

Define the following terms, which are part of the SEC terminology: (a) customary review, (b) comment letter, (c) red herring prospectus, (d) shelf registration.

What types of items are reported on Form 8-K?

Describe Parts I and II of the Foreign Corrupt Practices Act. What is the impact of this act on companies and public accountants?

\({ }^{*}\) What role has the SEC played in defining the relationship between public accountants (external. independent auditor) and publicly traded companies?

During the late 1920s, approximately 55 percent of all personal savings in the United States were used to purchase securities. Public confidence in the business community was extremely high as stock values doubled and tripled in short periods of time. The road to wealth was believed to be through

The development of accounting theory and practice has been influenced directly and indirectly by many organizations and institutions. Two of the most important institutions have been the Financial Accounting Standards Board (FASB) and the Securities and Exchange Commission (SEC).The FASB is an

The U.S. Securities and Exchange Commission (SEC) was created in 1934 and consists of five commissioners and a staff of approximately 1,900. The SEC professional staff is organized into five divisions and several principal offices. The primary objectives of the SEC are to support fair securities

The Securities and Exchange Commission has the authority to regulate proxy solicitations. This authority is derived from the Securities and Exchange Act of 1934 and is closely tied to the disclosure objective of this act. Regulations established by the SEC require corporations to mail a proxy

Bandex Inc. has been in business for 15 years. The company has compiled a record of steady but not spectacular growth. Bandex's engineers have recently perfected a product that has an application in the small computer market. Initial orders have exceeded the company's capacity and the decision has

The Jerford Company is a well-known manufacturing company with several wholly owned subsidiaries. The company's stock is traded on the New York Stock Exchange, and the company files all appropriate reports with the Securities and Exchange Commission. Jerford Company's financial statements are

The purpose of the Securities Act of 1933 is to regulate the initial offering of a firm's securities by ensuring that investors are given full and fair disclosure of all pertinent information about the firm. The Securities Exchange Act of 1934 was passed to regulate the trading of securities on

The company that employs you is a U.S. publicly traded corporation that manufactures chemicals. You are in the external financial reporting department, and your position requires that you keep current on all the new accounting requirements. While you realize that Staff Accounting Bulletins (SABs)

Currently, you are an experienced senior working at a public accounting firm. For the upcoming busy season you received a new client, a publicly traded corporation. The manager on this client is someone you have not worked with before. You hope to impress this manager because you hear that she

For each of the seven cases presented below, work the case twice and select the best answer. First assume that the foreign currency is the functional currency; then assume that the U.S. dollar is the functional currency.1. Certain balance sheet accounts in a foreign subsidiary of Shaw Company on

The following information should be used for questions 1,2 , and 3 . Select the best answers under each of two alternative assumptions: (a) the LCU is the functional currency and the translation method is appropriate; and \((b)\) the U.S. dollar is the functional currency and the remeasurement

Use the following information for questions 1, 2, and 3.Bartell Inc., a U.S. company, acquired 90 percent of the common stock of a French company on January 1,20X5, for \(\$ 160,000\). The net assets of the French subsidiary amounted to 680,000 francs on the date of acquisition. On January 1, 20X5,

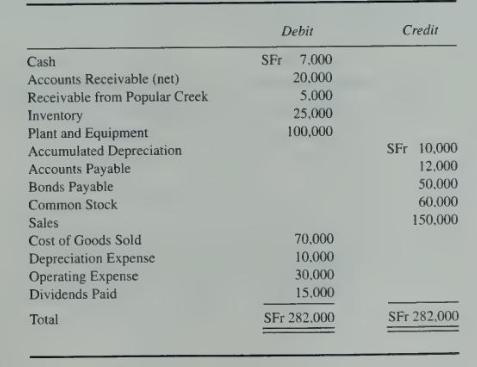

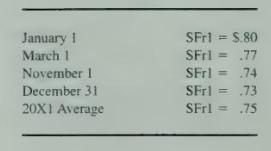

On January 1, 20X1, Popular Creek Corporation organized RoadTime Company as a subsidiary in Switzerland with an initial investment cost of SFr 60,000. RoadTime's December 31, 20X1, trial balance in Swiss francs (SFr) is as follows:1. The receivable from Popular Creek is denominated in Swiss francs.

Refer to the data in exercise 12-5.Requireda. Prepare a proof of the translation adjustment computed in exercise 12-5.b. Where is the translation adjustment reported on the consolidated financial statements of Popular Creek Corporation and its foreign subsidiary?

Refer to the data in exercise 12-5, but assume that the dollar is the functional currency for the foreign subsidiary.Required Prepare a schedule remeasuring the December 31. 20X1, trial balance from Swiss francs to dollars.

Refer to the data in exercises 12-5 and 12-7\section*{Required}a. Prepare a proof of the remeasurement gain or loss computed in exercise 12-7.b. How should this remeasurement gain or loss be reported on the consolidated financial statements of Popular Creek Corporation and its foreign subsidiary?

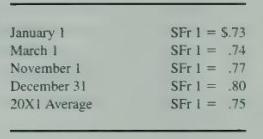

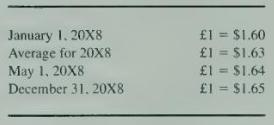

Refer to the data in exercise 12-5, but now assume that the exchange rates were as follows:The receivable from Popular Creek Corporation is denominated in Swiss francs. Popular Creek's books show a payable to RoadTime at \(\$ 3,650\).Assume the Swiss franc is the functional

Refer to the data in exercise \(12-5\), but now assume that the exchange rates were as follows:The receivable from Popular Creek Corporation is denominated in Swiss francs. Popular Creek's books show a payable to RoadTime at \(\$ 3,650\).Assume the U.S. dollar is the functional

Duff Company is a subsidiary of Rand Corporation and is located in Madrid, Spain, where the currency is the Spanish peseta (P). Data on Duff's inventory and purchases are as follows:The beginning inventory was acquired during the fourth quarter of \(20 \mathrm{X} 6\), and the ending inventory was

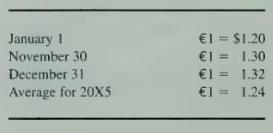

The Thames Company is located in London, England. The local currency is the British pound ( \(£\) ).On January 1, 20X8. Dek Company purchased an 80 percent interest in Thames Company for \(\$ 400,000\), which resulted in an excess of cost-over-book value of \(\$ 48,000\) due solely to a trademark

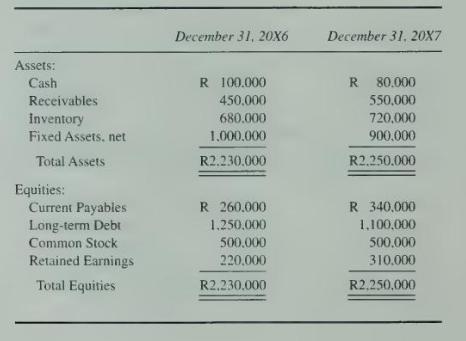

The Bentley Company owns a subsidiary in India. The subsidiary's balance sheets for the last two years are presented below, in rupees \((\mathrm{R})\) :The Bentley Company formed the subsidiary on January 1, 20X6, when the exchange rate was 30 rupees for 1 U.S. dollar. On December 31, 20X6, the

On December 31, 20X2, your company's Mexican subsidiary sold land at a selling price of \(3,000,000\) pesos. The land had been purchased for \(2.000,000\) pesos on January 1, 20XI, when the exchange rate was 10 pesos to 1 U.S. dollar. On December 31, 20X1, the exchange rate was 11 pesos to 1 U.S.

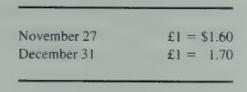

Hawk Company sold inventory to United Ltd., an English subsidiary. The goods cost Hawk \(\$ 8,000\) and were sold to United for \(\$ 12,000\) on November 27, payable in British pounds. The goods are still on hand at the end of the year on December 31. The British pound ( \(£\) ) is the functional

On January 1, 20X1. Par Company purchased all the outstanding stock of North Bay Company, located in Canada, for \(\$ 120.000\). On January 1, 20X1, the direct exchange rate for the Canadian dollar ( \(\mathrm{C} \$\) ) was \(\mathrm{C} \$ 1=\$ .80\). The book value of North Bay Company on January

On January 1, 20X5, Taft Company acquired all of the outstanding stock of Bordeaux Inc., a French company at a cost of \(\$ 151.200\). The net assets of Bordeaux on the date of acquisition were 700,000 francs. On January 1, 20X5, the book and fair values of the French subsidiary's identifiable

Refer to the information contained in problem 12-17. Assume the U.S. dollar is the functional currency, not the franc.\section*{Required}a. Prepare a schedule remeasuring the trial balance from French francs into U.S. dollars.b. Assume that Taft uses the basic equity method. Record all journal

Refer to the information presented in problem 12-17, and to your answer to part \(a\) of problem \(12-17\).\section*{Required}Prepare a schedule providing a proof of the translation adjustment.

Refer to the information given in problem 12-17, and your answer to part \(a\) of problem 12-18.\section*{Required}Prepare a schedule providing a proof of the remeasurement gain or loss. For this part of the problem, assume that the French subsidiary had the following monetary assets and

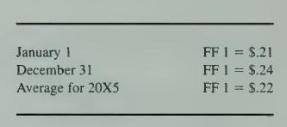

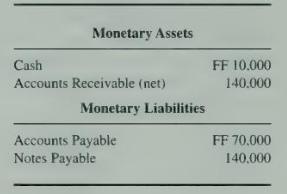

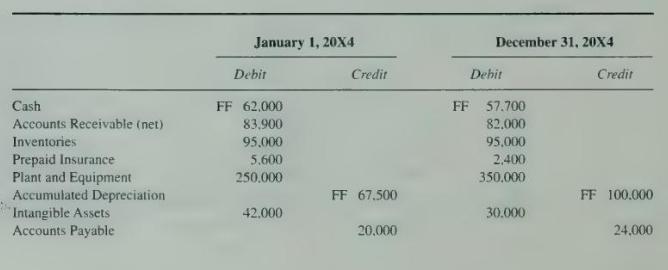

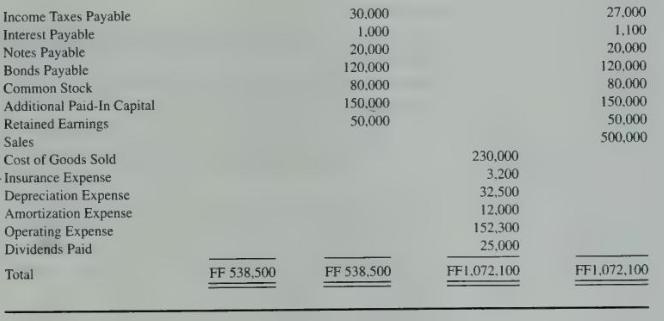

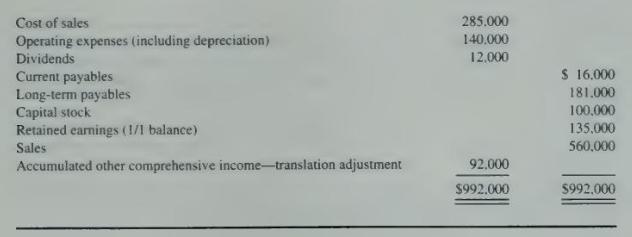

On January 1, 20X4, Alum Corporation acquired Franco Company, a French subsidiary, by purchasing all the common stock at book value. Franco's trial balances on January 1, 20X4, and December 31, 20X4, expressed in French francs (FF), are as follows:1. Franco uses FIFO inventory valuation. Purchases

Refer to the information in problem 12-21. Assume that the dollar is the functional currency.\section*{Required}a. Prepare a schedule remeasuring the December 31, 20X4, trial balance of Franco Company from francs to dollars.b. Prepare a schedule providing a proof of the remeasurement gain or loss.

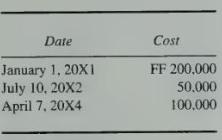

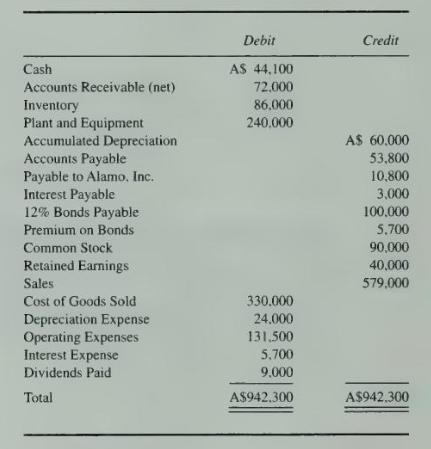

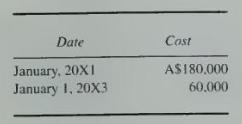

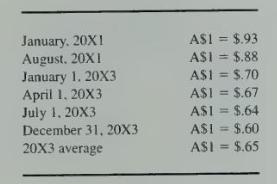

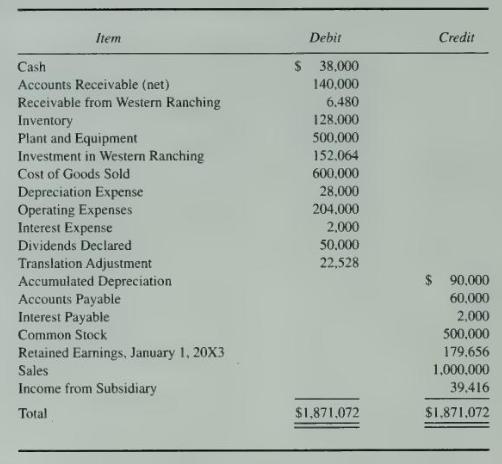

Alamo Inc. purchased 80 percent of the outstanding stock of Western Ranching Company, a company located in Australia, on January 1, 20X3. The purchase price was A \(\$ 200,000\), and A \(\$ 40,000\) of the differential was allocated to plant and equipment which is amortized over a 10 year period.

Refer to the information given in problem 12-23 for Alamo and its subsidiary, Western Ranching. Assume that the Australian dollar ( \(\mathrm{A} \$\) ) is the functional currency and that Alamo uses the basic equity method for accounting for its investment in Western Ranching

Refer to the information given in problems 12-23 and 12-24 for Alamo and its subsidiary, Western Ranching. Assume that the Australian dollar (A\$) is the functional currency and that Alamo uses the basic equity method for accounting for its investment in Western Ranching Company. A December 31,

Refer to the information in problem 12-23. Assume the U.S. dollar is the functional currency.\section*{Required}a. Prepare a schedule remeasuring the December 31, 20X3, trial balance of Western Ranching Company from Australian dollars to U.S. dollars.b. Prepare a schedule providing a proof of the

Refer to the information given in problems 12-23 and 12-26* for Alamo and its subsidiary, Western Ranching. Assume that the U.S. dollar is the functional currency and that Alamo uses the basic equity method for accounting for its investment in Western Ranching Company.\section*{Required}Prepare the

Refer to the information given in problems 12-23 and 12-27 for Alamo and its subsidiary, Western Ranching. Assume that the U.S. dollar is the functional currency and that Alamo uses the basic equity method for accounting for its investment in Western Ranching Company. A December 31, 20X3, trial

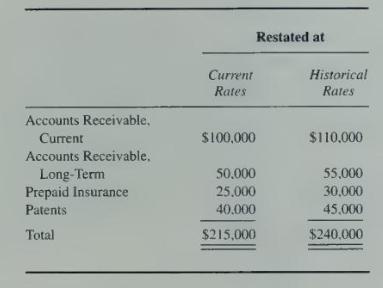

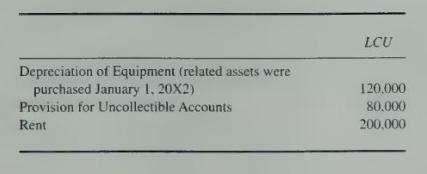

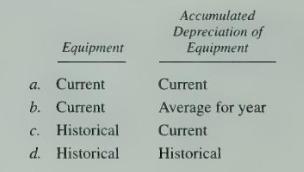

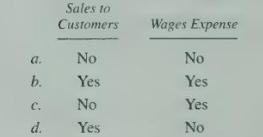

On January 1, 20X1, the Kiner Company formed a foreign subsidiary that issued all its currently outstanding common stock on that date. Selected accounts from the balance sheets, all of which are shown in local currency units, are as follows:1. Exchange rates are as follows:2. An analysis of the

Refer to the information in problem 12-29 for Kiner Company and its foreign subsidiary.\section*{Required}Prepare a schedule translating the selected accounts into U.S. dollars as of December 31, 20X1, and December \(31,20 \times 2\), respectively, assuming that the local currency unit is the

What are the three 10 percent significance tests used to determine reportable segments under FASB 131? Give the numerator and denominator for each of the tests.

A company has 10 industry segments, of which the largest five account for 80 percent of the combined revenues of the company. What considerations are important in determining the number of segments that are separately reportable? How are the remaining segments reported?

Only two materiality tests are used to determine separately reportable foreign operations. What are these two tests? Why isn't the third test, the profit or loss test, used to assess foreign operations?

Describe the process of updating the estimate of the effective tax rate in the second quarter of a company's fiscal year.

The Allied Company made a change in depreciation accounting during the third quarter of its fiscal year. This change is a cumulative-effect type of accounting change. Describe the effect of this accounting change on prior interim reports and on the third quarter's interim report.

Following are descriptions of several independent situations.1. Rockford Company has a subsidiary in Argentina. The subsidiary does not have much debt, because of the high interest costs resulting from the average annual inflation rate exceeding 100 percent. Most of its sales and expense

Petie Products Company was incorporated in Wisconsin in 20X0 as a manufacturer of dairy supplies and equipment. Since incorporating, Petie has doubled in size about every three years and is now considered one of the leading dairy supply companies in the country.During January 20X4, Petie

Wahl Company's 20X5 consolidated financial statements include two wholly owned subsidiaries. Wahl Company of Australia (Wahl A) and Wahl Company of France (Wahl F). Functional currencies are the U.S. dollar for Wahl A and the franc for Wahl F.\section*{Required}a. What are the objectives of

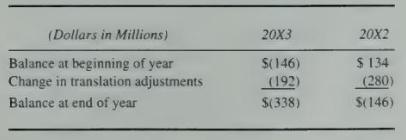

Dundee Company owns 100 percent of a subsidiary located in Ireland. The parent company uses the Irish pound as the subsidiary's functional currency. At the beginning of the year, the debit balance in the accumulated other comprehensive income-translation adjustment account, which was the only item

The following footnote was abstracted from a recent annual report of Johnson \& Johnson Company: \(\square\)\section*{Footnote 7: Foreign Currency Translation}For translation of its international currencies, the Company has determined that the local currencies of its international subsidiaries

Many larger U.S. companies have significant investments in foreign operations. For example, McDonald's Corporation, the food service company, obtains 47 percent of its consolidated revenues, 44 percent of its operating income, and has 45 percent of its invested assets in non-U.S locations. Unisys,

Showing 200 - 300

of 2939

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers