New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

advanced financial accounting

Advanced Financial Accounting 5th Edition Richard E. Baker, Valdean C. Lembke, Thomas E. King - Solutions

Route Manufacturing purchased 80 percent of the stock of Hampton Mines Inc. in 20X3. In preparing the consolidated financial statements at the end of 20X5, the controller of Route discovered that Route Manufacturing had purchased \(\$ 75.000\) of raw materials from Hampton Mines during the year and

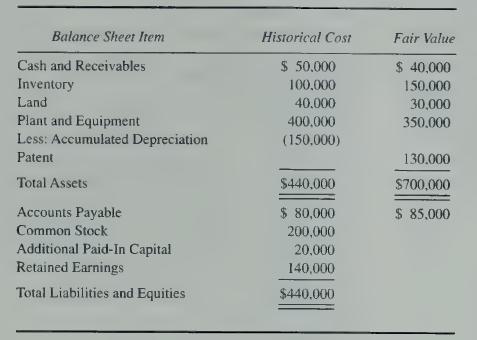

Fineline Pencil Company purchased 100 percent of the stock of Smudge Eraser Corporation on January 2. 20X3, for \(\$ 150,000\) cash. Summarized balance sheet data for the companies on December 31, 20X2, are as follows:\section*{Required}Prepare a consolidated balance sheet immediately following the

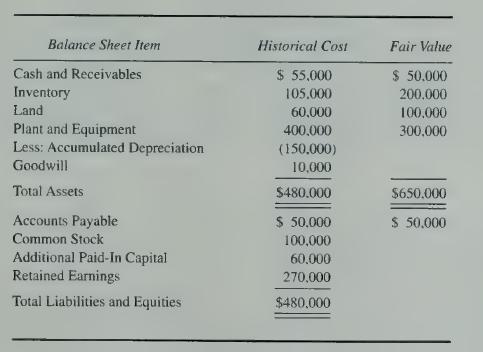

Byte Computer Corporation purchased 100 percent of the stock of Nofail Software Company on January 2, 20X3, by issuing bonds with par value of \(\$ 140,000\) and a fair value of \(\$ 150,000\) in exchange for the shares. Summarized balance sheet data presented for the companies just before the

Byte Computer Company purchased 100 percent of the common stock of Nofail Software Company on January 2, 20X3, by issuing preferred stock with a par value of \(\$ 6\) per share and a market value of \(\$ 10\) per share. A total of 15,000 shares of preferred stock was issued. Balance sheet data for

Frazer Corporation owns 70 percent of the stock of Messer Company. In the 20X9 consolidated income statement, the noncontrolling interest was assigned \(\$ 18,000\) of income.\section*{Required}What amount of net income did Messer Company report for 20X9?

The accountant for Belchfire Motors was called away after completing only half of the consolidated statements at the end of \(20 \mathrm{X} 4\). The data left behind included the following:\section*{Required}a. Belchfire Motors purchased shares of Premium Body Shop at underlying book value on

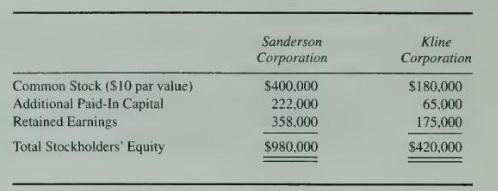

Sanderson Corporation purchased 70 percent of the common stock of Kline Corporation on January \(1,20 \times 7\), for \(\$ 294,000\) in cash. The stockholders' equity accounts of the two companies at the date of purchase are:\section*{Required}a. What amount will be assigned to the noncontrolling

Ambrose Corporation owns 75 percent of the common stock of Kroop Company, acquired at underlying book value on January 1, 20X4. The income statements for Ambrose and Kroop for 20X4 include the following amounts:Ambrose uses the cost method in accounting for its ownership of Kroop. Kroop paid

Tall Corporation purchased 75 percent of the voting common stock of Light Corporation on January \(1,20 \times 2\), at underlying book value. Noncontrolling interest was assigned income of \(\$ 8,000\) in Tall's consolidated income for \(20 \mathrm{X} 2\) and a balance of \(\$ 65,500\) in Tall's

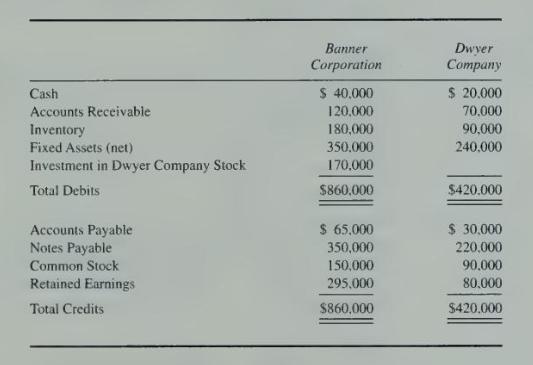

Banner Corporation purchased all of the common stock of Dwyer Company at underlying book value and uses the equity method in accounting for its investment. Balance sheet information provided by the companies at December \(31,20 \mathrm{X} 8\), is as follows:\section*{Required}Prepare a consolidated

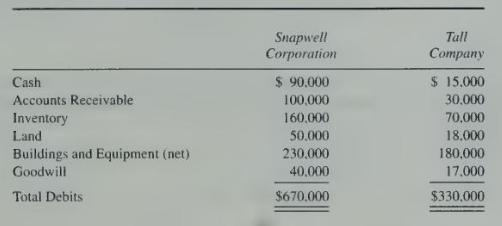

Snapwell Corporation acquired all of the common stock of Tall Company on January 1, 20X1, by issuing 6,400 shares of its \(\$ 5\) par value common stock. Balance sheet data for Snapwell and Tall at December \(31,20 \mathrm{X} 0\), are as follows:On December 31, 20X0, Tall Company owed Snapwell

Noway Manufacturing owns 75 percent of the stock of Positive Piston Corporation. During 20X9. Noway and Positive reported sales of \(\$ 400,000\) and \(\$ 200,000\) and expenses of \(\$ 280,000\) and \(\$ 160,000\), respectively.\section*{Required}Compute the amount of total revenue, total

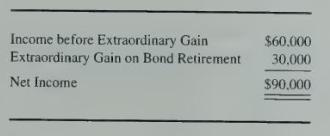

Rank Corporation purchased 60 percent of the stock of Fresh Company on December 31, 20X4. In preparing the consolidated financial statements at December \(31,20 X 4\), goodwill of \(\$ 240,000\) was reported. The goodwill is attributable to Rank's purchase of Fresh Company shares, and the parent

Garwood Corporation purchased 75 percent of the voting common stock of Zorn Company on January 1, 20X4. At the time of acquisition, Zorn reported buildings and equipment at book value of \(\$ 240,000\) : however, an appraisal indicated a fair value of \(\$ 290,000\).\section*{Required}If

Placer Corporation purchased 80 percent of the voting common stock of Billings Company on January 1, 20X4, at underlying book value. Placer Corporation and Billings Company reported total revenue of \(\$ 410,000\) and \(\$ 200,000\), and total expenses of \(\$ 320,000\) and \(\$ 150,000\),

Select the correct answer for each of the following questions.1. What is the theoretically preferred method of presenting a noncontrolling interest in a consolidated balance sheet?a. As a separate item within the liability section.b. As a deduction from (contra to) goodwill from consolidation, if

Knight Corporation owns 100 percent of the voting shares of Spahn Company. During 20X6, Spahn Company purchased inventory items for \(\$ 20,000\) and sold them to Knight Corporation for \(\$ 50,000\). Knight Corporation continues to hold the items in inventory on December 31, 20X6. Sales for the

River Products Corporation purchases all its inventory from its wholly owned subsidiary. Clayborn Corporation. In 20X2. Clayborn produced inventory at a cost of \(\$ 10.000\) and sold it to River Products for \(\$ 25,000\). The parent held all the items in inventory on January 1, 20X3. During 20X3,

Placer Corporation purchased 75 percent of the common stock of Murdokk Enterprises on January \(1,20 \mathrm{X} 1\), for \(\$ 20,000\) more than underlying book value. The excess payment is assigned to increased value of equipment which had a remaining life of eight years at the date of the

Consolidated net income of \(\$ 164,300\) was reported for \(20 \mathrm{X} 2\) by Tally Corporation and its subsidiary. Tally had purchased 60 percent of the common shares of its subsidiary at underlying book value. Noncontrolling interest was assigned income of \(\$ 15.200\) in the consolidated

Slender Products Corporation purchased 80 percent ownership of LoCal Bakeries on January 1, 20X3, for \(\$ 40,000\) more than its portion of LoCal's underlying book value. The full additional payment is assigned to depreciable assets with an eight-year economic life. Income statement data for the

\section*{P3-27 Incomplete Company and Consolidated Data}Beryl Corporation purchased 100 percent of the common stock of Stargel Enterprises on December 31. 20X4. At that date, the book values and fair values of Stargel's identifiable assets and liabilities were identical. Balance sheet data for the

Potash Company owns 100 percent of the common stock of Bortz Corporation, which it acquired on December 31, 20X4, at underlying book value. Potash uses the equity method in accounting for its investment in Bortz. On December 31. 20X6, Potash sold equipment with a book value of \(\$ 85,000\) to

Quoton Corporation purchased 80 percent of the common stock of Tempro Company on December 31. 20X5, at underlying book value. The following trial balance data was provided by Tempro Company at December 31, 20X5:\section*{Required}a. How much did Quoton Corporation pay in purchasing its shares of

Smart Corporation acquires 100 percent of the common stock of Wisner Company on January 1, 20X8, by issuing 50,000 shares of \(\$ 4\) par value common stock. Smart Corporation shares are selling for \(\$ 11\) at the time of issue. Balance sheet data of the two companies just before the acquisition

Exacto Company reported net assets of \(\$ 260,000\) on January 1, 20X5, and reported the following net income and dividends for the years indicated:True Corporation purchased 75 percent of the common stock of Exacto Company on January 1 . 20X5, and reported a balance in its investment account of

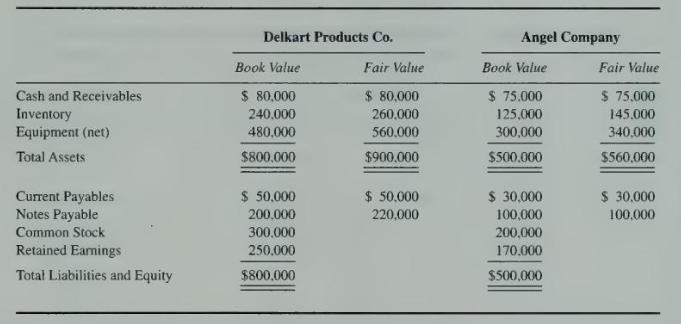

Delkart Products Company acquired 100 percent of the common shares of Angel Company on January \(1,20 \times 2\), by issuing 6,000 shares of its \(\$ 10\) par common stock. At the time of the business combination, Delkart's stock was selling for \(\$ 70\) per share. Balance sheets for the two

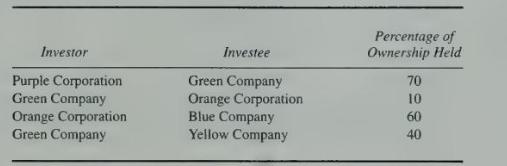

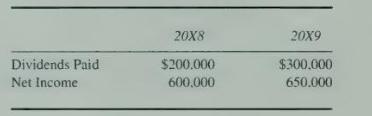

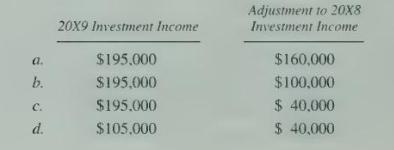

Purple Corporation recently attempted to expand by purchasing ownership in Green Company. The following ownership structure was reported on December 31, 20X9:The following income from operations (excluding investment income) and dividend payments were reported by the companies during \(20

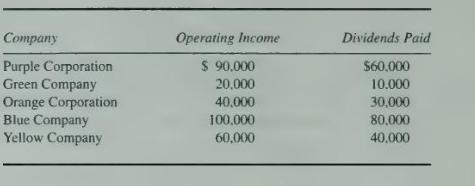

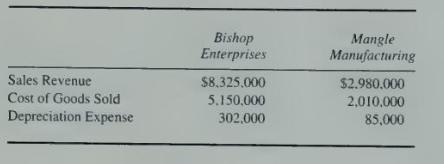

Bishop Enterprises purchased 100 percent of the common shares of Mangle Manufacturing Company on January \(1,20 \mathrm{X} 7\), for \(\$ 1,250,000\), a price that was \(\$ 55,000\) in excess of the book value of the shares acquired. All of the excess of the cost over book value was related to

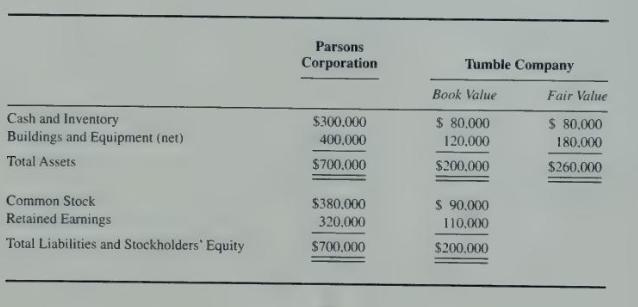

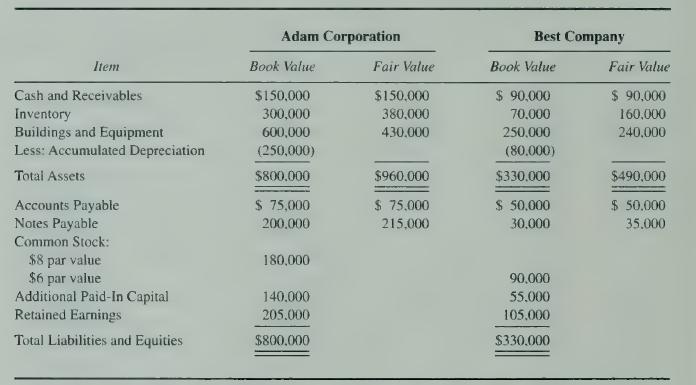

Parsons Corporation purchased 75 percent ownership of Tumble Company on December 31. 20X7, for \(\$ 210,000\). Summarized balance sheet amounts for the companies on December 31, 20X7, prior to the purchase, were as follows: Parsons Corporation Book Value Tumble Company Fair Value $ 80,000 120,000

What is negative goodwill? How is negative goodwill reported in the consolidated balance sheet?

How is it possible for there to be a positive purchase differential but negative goodwill on a purchase of the stock of another company?

What portion of the balances of subsidiary stockholders' equity accounts are included in the consolidated balance sheet?

What portion of the fair value of the net assets of a subsidiary normally is included in the consolidated balance sheet following a purchase-type business combination?

What happens to the purchase differential in the consolidation workpaper prepared as of the date of combination? How is it reestablished so that the proper balances can be reported the following year?

Does a noncontrolling shareholder have access to any information other than the consolidated financial statements to determine how well a subsidiary is doing? Explain.

Explain why consolidated financial statements become increasingly important when the purchase differential is very large.

There is a noncontrolling interest balance reported in the consolidated balance sheet of Worldwide Corporation. Why must the noncontrolling interest be reported in the consolidated balance sheet?

How is the amount assigned to noncontrolling interest in the consolidated balance sheet normally determined?

What effect does a negative retained earnings balance on the subsidiary's books have on the consolidation procedures?

At a recent staff meeting, the vice president of marketing appeared confused. He had been assured by the controller that the parent company and each of the subsidiary companies had properly accounted for all transactions during the year. After several other questions, he finally asked, "If it has

The owners of Small Corporation recently offered to sell 60 percent of their ownership to Large Corporation for \(\$ 450,000\). The business manager of Large Corporation was told that the book value of Small Corporation was \(\$ 300,000\), and she estimates the fair value of its net assets at

Although Sloan Company had good earnings reports in 20X5 and 20X6, it had a negative retained earnings balance on December 31, 20X6. Jacobs Corporation purchased 80 percent of the common stock of Sloan on January 1, 20X7.\section*{Required}a. Indicate how the negative retained earnings balance of

Crumple Car Rentals is planning to expand into the western part of the United States and needs to acquire approximately 400 additional automobiles for rental purposes. Because Crumple's cash reserves were substantially depleted in replacing the bumpers on existing automobiles with new "fashion

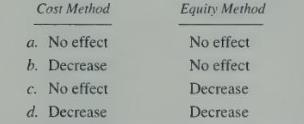

Select the correct answer for each of the following questions.1. Peel Company received a cash dividend from a common stock investment. Should Peel report an increase in the investment account if it uses the cost method or equity method of accounting?\begin{tabular}{llll}a. & Nost & &

Select the correct answer for each of the following questions.1. Green Corporation owns 30 percent of the outstanding common stock and 100 percent of the outstanding noncumulative nonvoting preferred stock of Axel Corporation. In 20X1, Axel declared dividends of \(\$ 100,000\) on its common stock

\section*{E2-3 Multiple-Choice Questions on Equity-Method Reporting [AICPA Adapted]}Select the correct answer for each of the following questions.1. On January 1, 20X5, the Swing Company purchased at book value 100,000 shares ( 20 percent) of the voting common stock of Harpo Instruments Inc. for

Roller Corporation purchased 20 percent ownership of Steam Company on January 1, 20X5, for \(\$ 70,000\). On that date, the book value of net assets reported by Steam Company was \(\$ 200,000\). The excess over book value paid is attributable to depreciable assets with a remaining useful life of 10

Winston Corporation purchased 40 percent of the stock of Fullbright Company on January 1, 20X2, at underlying book value. The companies reported the following operating results and dividend payments during the first three years of intercorporate ownership:\section*{Required}Compute the net income

Phillips Company bought 40 percent ownership in Jones Bag Company on January 1, 20X1, at underlying book value. In 20X1, 20X2, and 20X3, Jones Bag reported net income of \(\$ 8,000\), \(\$ 12,000, \$ 20,000\), and dividends of \(\$ 15,000, \$ 10,000\), and \(\$ 10,000\), respectively. The balance

Ravine Corporation purchased 30 percent ownership of Valley Industries for \(\$ 90,000\) on January 1, 20X6, when Valley had capital stock of \(\$ 240,000\) and retained earnings of \(\$ 60,000\). The following data were reported by the companies for the years 20X6 through

Power Corporation purchased 35 percent of the common stock of Snow Corporation on January 1, 20X2, by issuing 15,000 shares of its \(\$ 6\) par value common stock. The market price of Power's shares at the date of issue was \(\$ 24\). Snow Corporation reported net assets with a book value of \(\$

Best Corporation acquired 25 percent of the voting common stock of Flair Company on January 1. 20X7, by issuing bonds with a par value and fair value of \(\$ 170.000\) and making a cash payment of \(\$ 26,000\). At the date of acquisition, Flair Company reported assets of \(\$ 740,000\) and

Capital Corporation purchased 40 percent of the stock of Cook Company on January 1, 20X4, for \(\$ 136,000\). On that date Cook Company reported net assets of \(\$ 300,000\) valued at historical cost and \(\$ 340,000\) stated at fair value. The difference was due to the increased value of buildings

Brindle Company purchased 25 percent of the voting common stock of Monroe Company for \(\$ 162,000\) on January 1,20X4. At that date, Monroe reported assets of \(\$ 690,000\) and liabilities of \(\$ 230,000\). The book values and fair values of Monroe were equal except for land which had a fair

Spone Corporation purchased 40 percent of the voting common stock of Hall Corporation on January 1, 20X8, for \(\$ 133,400\). Hall Corporation reported net income of \(\$ 55,000\) for \(20 \mathrm{X} 8\) and paid dividends of \(\$ 25,000\) on December 30. 20X8. At the date of acquisition, Hall

Branch Corporation purchased 30 percent of the common stock of Hardy Company on January 1, 20X5, and paid \(\$ 28,000\) above book value. The full amount of the additional payment was attributed to amortizable assets with a life of eight years remaining at January 1, 20X5. During 20X5 and 20X6.

Scott Company purchased 30 percent of the ownership of Earnest Enterprises on January 1, 20X2, at underlying book value. In \(20 \mathrm{X} 2\) Earnest Enterprises reported net income of \(\$ 60,000\) and paid dividends of \(\$ 15,000\), and in \(20 \mathrm{X} 3\) reported a loss of \(\$ 40,000\)

During review of the adjusting entries to be recorded on December 31, 20X8. Grand Corporation discovered that it had inappropriately been using the cost method in accounting for its investment in Case Products Corporation. Grand Corporation purchased 40 percent ownership of Case Products on January

Rod Corporation purchased 30 percent ownership of Stafford Corporation on January 1, 20X4, for \(\$ 65,000\), which was \(\$ 10,000\) above the underlying book value. Half the additional amount was atributable to an increase in the value of land held by Stafford Corporation, and half was due to an

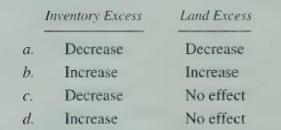

Turner Corporation reported the following balances at January 1, 20X9:On January 1, 20X9, Chad Corporation purchased 40 percent of the stock of Turner Corporation. All tangible assets had a remaining economic life of 10 years at January 1, 20X9. Both companies use the FIFO inventory method. Turner

The North Company has supplied you with information regarding two investments that were made during 20X5, as follows:On January 1, 20X5, North purchased for cash 40 percent of the 500,000 shares of voting common stock of the York Company for \(\$ 2,400,000\), representing 40 percent of the net

Grandview Company purchased 40 percent of the stock of Spinet Corporation on January 1, 20X8, at underlying book value. Spinet recorded the following income for \(20 \times 9\) :\section*{Required}Prepare all journal entries on Grandview's books for 20X9 to account for its investment in Spinet.

Reden Corporation purchased 45 percent of the common stock of Montgomery Company on January 1, 20X9, at underlying book value of \(\$ 288,000\). The balance sheet of Montgomery Company contained the following stockholders' equity balances:Montgomery's preferred stock is cumulative and pays a 10

Callas Corporation paid \(\$ 380,000\) to acquire 40 percent ownership of Thinbill Company on January 1, 20X9. The amount paid was equal to underlying book value. During 20X9, Thinbill Company reported operating income of \(\$ 45,000\), an increase of \(\$ 10,000\) in the market value of trading

Baldwin Corporation purchased 25 percent of the common stock of Gwin Company on January 1. 20X8, at underlying book value. In 20X8 Gwin reported a net loss of \(\$ 20,000\) and paid dividends of \(\$ 10,000\), and in \(20 \times 9\) reported net income of \(\$ 68,000\) and paid dividends of \(\$

On January 2, 20X0. Cristol Corporation acquired 95 percent of the common stock of Glenco Inc. in a business combination treated as a pooling of interests. At the date of combination, Glenco had common stock outstanding with a total par value of \(\$ 400,000\), additional paid-in capital of \(\$

Denbow Corporation reported a deferred tax liability of \(\$ 37800\) in its balance sheet dated December 31, 20X1. Denbow's only temporary difference resulted from its use of the equity method to report its 25 percent investment in Crabapple Industries, acquired at underlying book value on December

Select the correct answer for each of the following questions.1. On July 1, 20X3, Barker Company purchased 20 percent of the outstanding common stock of Acme Company for \(\$ 400,000\) when the fair value of Acme's net assets was \(\$ 2,000,000\). Barker does not have the ability to exercise

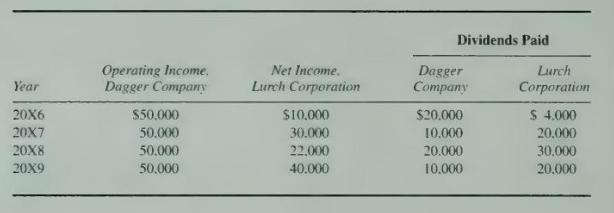

Dagger Company purchased 25 percent of the voting common stock of Lurch Corporation on July \(1,20 \times 6\) at \(\$ 10.000\) over underlying book value. The excess all relates to amortizable assets with a remaining life of 10 years. Both companies report on a calendar-year basis and pay dividends

Ball Corporation purchased 30 percent of the common stock of Krown Company on January 1. 20X5, by issuing preferred stock with a par value of \(\$ 50.000\) and a market price of \(\$ 120.000\). The following amounts relate to the balance sheet items of Krown Company at that date:Buildings and

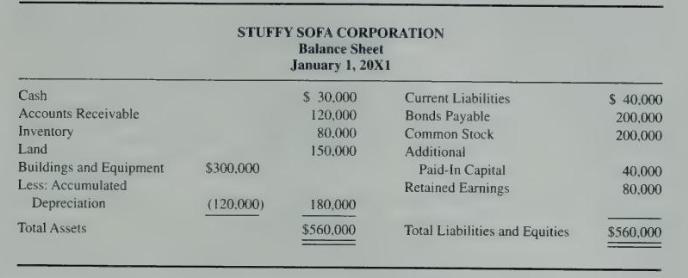

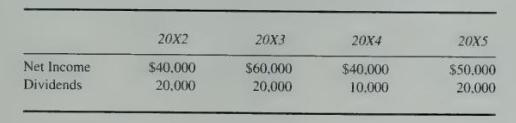

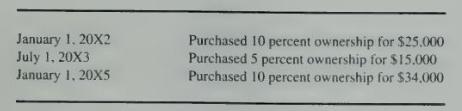

Easy Chair Company purchased 40 percent ownership of Stuffy Sofa Corporation on January 1, \(20 \mathrm{X} 1\), for \(\$ 150.000\). The balance sheet of Stuffy Sofa Corporation at the time of acquisition was as follows:During 20X1 Stuffy Sofa Corporation reported net income of \(\$ 30.000\) and

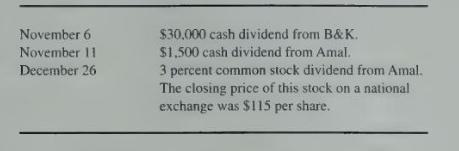

Idle Corporation has been acquiring shares of Fast Track Enterprises at book value for the last several years. Data provided by Fast Track Enterprises included the following:Fast Track Enterprises declares and pays its annual dividend on November 15 each year. Its net book value on January 1, 20X2,

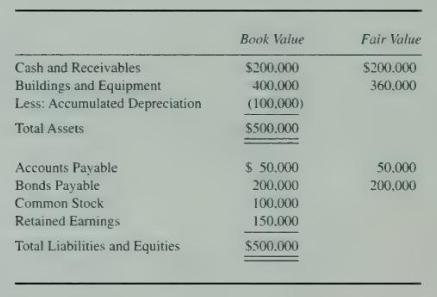

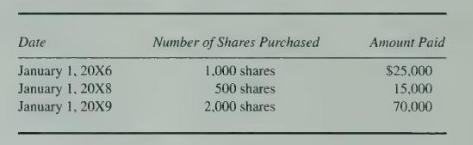

Jackson Corporation purchased shares of Phillips Corporation in the following sequence:The book value of Phillips's net assets at January 1, 20X6, was \(\$ 200,000\). Each year since Jackson first purchased shares, Phillips has reported net income of \(\$ 70,000\) and paid dividends of \(\$

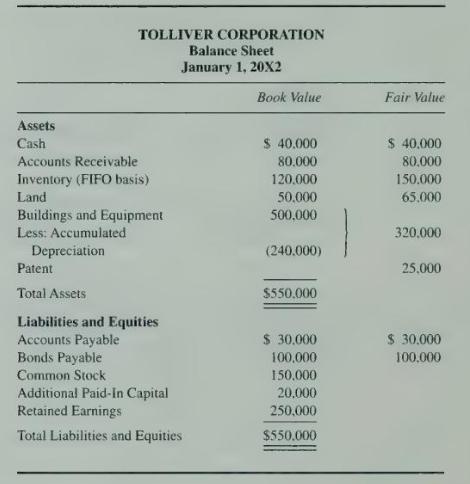

Essex Company issued common shares with a par value of \(\$ 50,000\) and a market value of \(\$ 165,000\) in exchange for 30 percent ownership of Tolliver Corporation on January 1, 20X2. Tolliver reported the following balances on that date:The estimated economic life of the patents held by

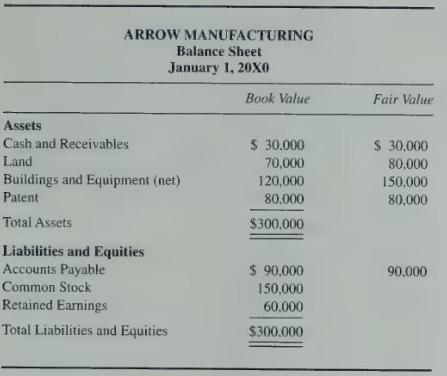

On January 1, 20X0, Hunter Corporation issued 6,000 of its \(\$ 10\) par value shares to acquire 45 percent of the shares of Arrow Manufacturing. The balance sheet of Arrow Manufacturing immediately before the acquisition contained the following items:On the date of the stock acquisition, Hunter

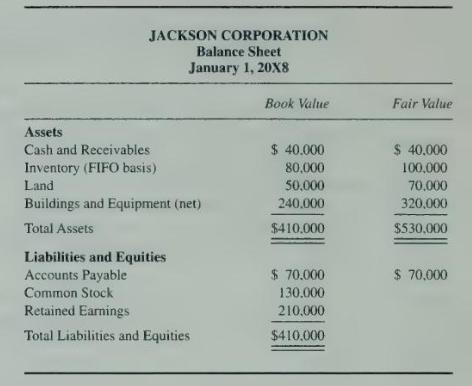

Ennis Corporation acquired 35 percent of the stock of Jackson Corporation on January 1, 20X8. by issuing 25,000 shares of its \(\$ 2\) par value shares. The balance sheet for Jackson Corporation immediately before the acquisition contained the following items:Shares of Ennis Corporation were

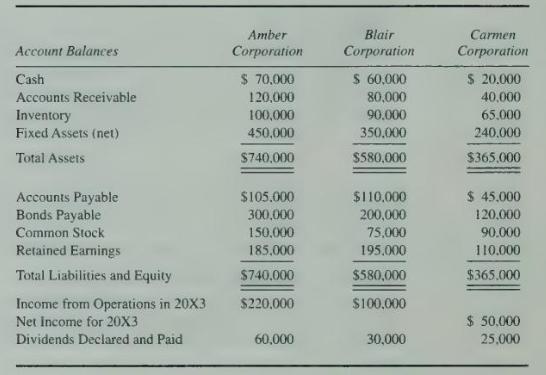

Balance sheet and summarized income statement data for Amber Corporation, Blair Corporation, and Carmen Corporation at January 1, 20X3, were as follows:On January 1, 20X3, Amber Corporation purchased 40 percent of the voting common stock of Blair Corporation by issuing common stock with a par value

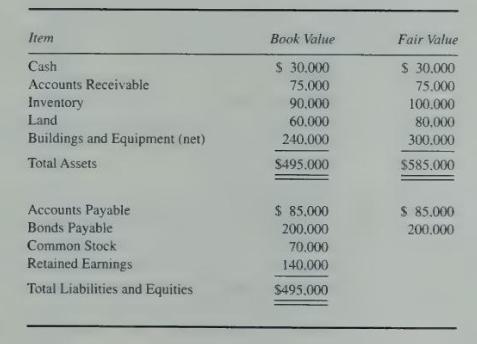

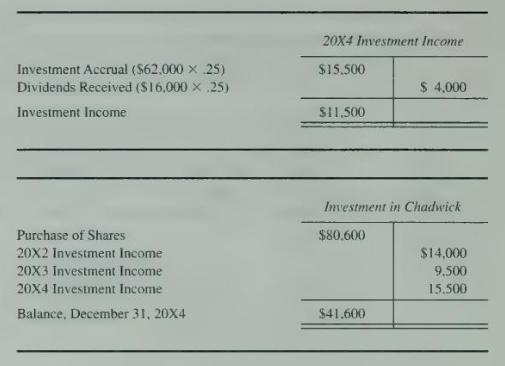

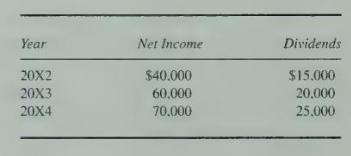

Blanch Corporation purchased 25 percent of the voting common shares of Chadwick Company on January 1, 20X2, for \(\$ 80,600\). At January 1, 20X2, Chadwick Company reported the following balance sheet amounts and fair values:At January 1, 20X2, the estimated remaining economic life of buildings and

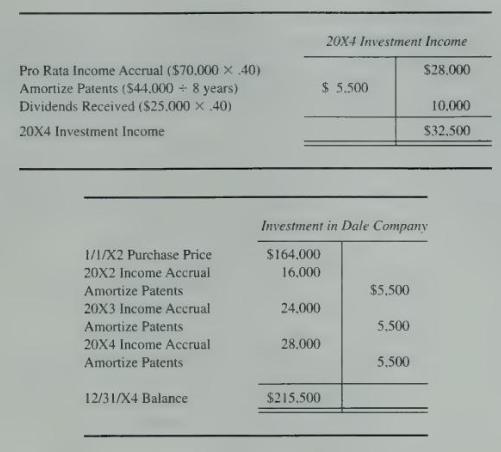

Hill Company paid \$164,000 to acquire 40 percent ownership of Dale Company on January 1, 20X2. Net book value of Dale's assets on that date was \(\$ 300,000\). Book values and fair values of net assets held by Dale were the same, except for equipment and patents. Equipment held by Dale Company had

Dewey Corporation owns 30 percent of the common stock of Jimm Company, which it purchased at underlying book value on January 1, 20X5. Dewey reported a balance of \(\$ 245,000\) for its investment in Jimm Company on January 1, 20X5, and \(\$ 276,800\) at December 31, 20X5. During 20X5, Dewey and

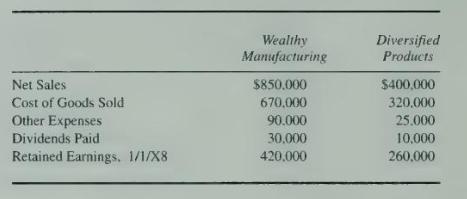

Wealthy Manufacturing Company purchased 40 percent of the voting shares of Diversified Products Corporation on March 23, 20X4. On December 31, 20X8, the controller of Wealthy Manufacturing Company attempted to prepare income statements and retained earnings statements for the two companies using

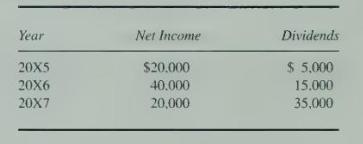

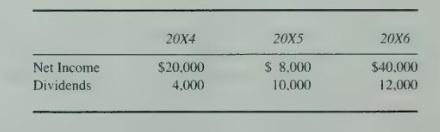

Swan Products Inc. owns 25 percent of the common stock of Computech Computer Company, purchased December \(28,20 \times 3\), at book value. During the three years subsequent to the acquisition of its stock by Swan Products, Computech reported the following net income and dividends:Swan Products has

A reader of the consolidated financial statements of Gigantic Company received copies from another source of the financial statements of the individual companies included in the consolidation. He is confused by the fact that the total assets in the consolidated balance sheet differ rather

A reader of the consolidated financial statements of Gigantic Company received copies from another source of the financial statements of the individual companies included in the consolidation. He is confused by the fact that the total assets in the consolidated balance sheet differ rather

Crumple Car Corporation produces fuel-efficient automobiles and sells them through a vast dealer network. It has two wholly owned subsidiaries. One subsidiary provides financing for approximately 70 percent of all automobile sales of the parent company and its dealers. The other subsidiary

Sharp Company will acquire 90 percent of Moore Company in a business combination. The total consideration has been agreed upon. The nature of Sharp's payment has not been fully agreed upon. Therefore, it is possible that this business combination might be accounted for as either a purchase or a

Many well-known products and names come from companies that may be less well known or may be known for other reasons. In some cases, an obscure parent company may have well-known subsidiaries, and often familiar but diverse products may be produced under common ownership.\section*{Required}a.

During previous merger booms, a number of companies acquired many subsidiaries that often were in businesses unrelated to the acquiring company's central operations. In many cases, the management of the acquiring company was unable to manage effectively the many diverse types of operations found in

The use of proportionate or pro rata consolidation generally has not been acceptable in the United States. Normally, a significant investment in the common stock of another company must either be fully consolidated or reported using the equity method.\section*{Required}a. What method does Amerada

Select the correct answer for each of the following questions.1 . Goodwill represents the excess of the cost of an acquired company over the:a. Sum of the fair values assigned to identifiable assets acquired less liabilities assumed.b. Sum of the fair values assigned to tangible assets acquired

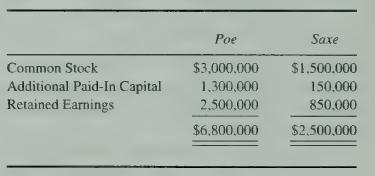

Select the correct answer for each of the following questions.1. On December 31. 20X3, Saxe Corporation was merged into Poe Corporation. In the business combination, Poe issued 200,000 shares of its $10 par common stock, with a market price of $18 a share, for all of Saxe's common stock. The

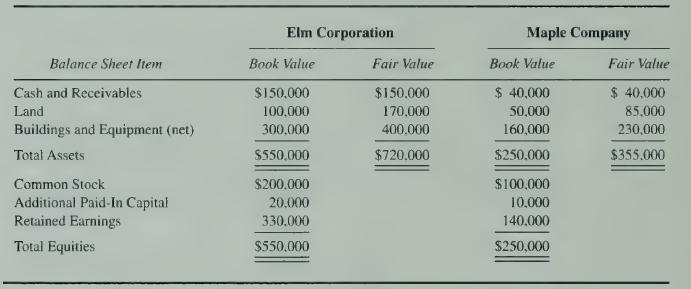

Elm Corporation and Maple Company have announced terms of an exchange agreement under which Elm will issue 8,000 shares of its $10 par value common stock to acquire all the assets of Maple Company. Elm shares currently are trading at $50, and Maple $5 par value shares are trading at $18 each.

Spur Corporation reported the following balance sheet amounts on December 3 1 . 2 0X1Required Blanket Company purchases the assets and liabilities of Spur Corporation for $670,000 cash on December 31, 20X1. Give the entry made by Blanket Company to record the purchase. Balance Sheet Item Cash and

Musial Corporation used debentures with a par value of $580,000 to acquire 100 percent of the net assets of Sorden Company on January 1 , 2 0X2. On that date, the fair value of the bonds issued by Musial Corporation was $564,000, and the following balance sheet data were reported by Sorden

Grant Company acquired all of the assets and liabilities of Bedford Corporation on January 1 , 2 0X2, in a business combination recorded as a purchase. At that date, Bedford reported assets with a book value of $624,000 and liabilities of $356,000. Grant noted that Bedford had $40,000 of research

Allsap Company was acquired by Dunyain Corporation on January 1, 20X1, through an exchange of common shares in a business combination recorded as a purchase. All of Allsap's assets and liabilities were immediately transferred to Dunyain Corporation. Dunyain reported total par value of shares

The following balance sheets were prepared for Adam Corporation and Best Company on January 1, 20X2. just before they entered into a business combination:Adam acquired all of the assets and liabilities of Best Company on January 1, 20X2, in an exchange of common shares treated as a purchase. Adam

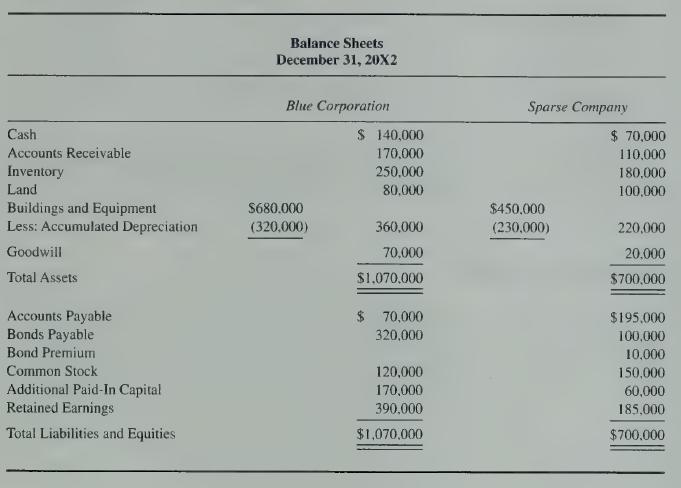

The following financial statement information was prepared for Blue Corporation and Sparse Company at December 3 1 . 2 0X2:Blue Corporation and Sparse Company agreed to combine as of January 1, 20X3. In completing the merger. Blue Corporation paid finder's fees of $30,000, audit fees of $15,000,

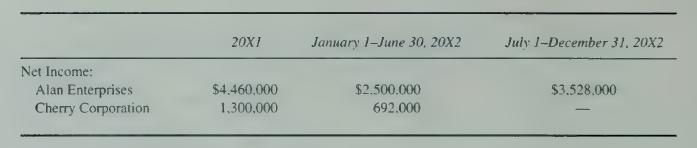

On July 1 , 2 0X2, Alan Enterprises merged with Cherry Corporation through an exchange of stock and subsequent liquidation of Cherry. Alan issued 200,000 shares of its stock to effect the combination. The book values of Cherry's assets and liabilities were equal to their fair values at the date of

Showing 700 - 800

of 2939

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers