New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

advanced financial accounting

Advanced Financial Accounting 5th Edition Richard E. Baker, Valdean C. Lembke, Thomas E. King - Solutions

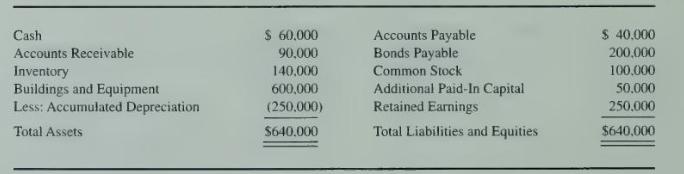

Swan Corporation acquired 90 percent of the stock of United Mining Company in a business combination recorded as a pooling of interests on January 1, 20X0. United Mining Company reports the following balances on January 1, 20X2:Swan Corporation uses the basic equity method in accounting for its

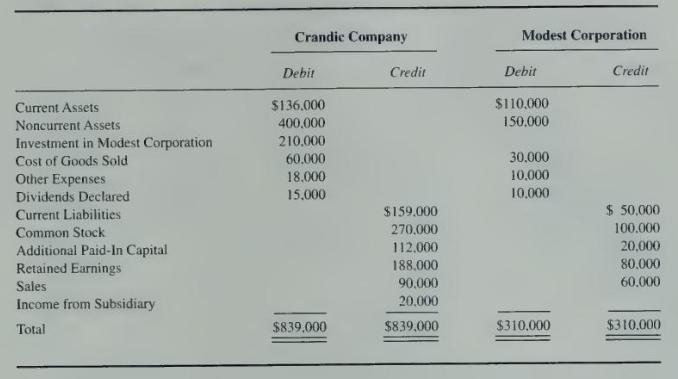

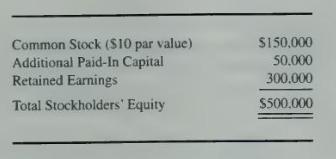

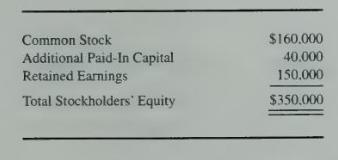

Crandic Company and Modest Corporation joined together on January 1, 20X2, in a business combination treated as a pooling of interests. Simplified trial balances for the two companies on December \(31,20 \times 2\), are as follows:The pooling of interests was accomplished by Crandic Company's

Summarized balance sheets for Blue Star Corporation and Select Soup Company as of December \(31,20 \times 2\), are presented below. The two companies plan to join together in a pooling of interests involving an exchange of 5,000 shares of Blue Star Corporation \(\$ 10\) par value stock for 18,000

Yarn Manufacturing Corporation issued stock with a par value of \(\$ 67,000\) to acquire 95 percent of the stock of Spencer Corporation in a pooling of interests completed on August 30, 20X1. On January 1, 20X1. Spencer Corporation reported the following stockholders' equity balances:Spencer

Yam Manufacturing Corporation issued stock with a par value of \(\$ 67,000\) and a market value of \(\$ 503.500\) to purchase 95 percent of the stock of Spencer Corporation on August 30, 20X1. On January 1, 20X1, Spencer Corporation reported the following stockholders' equity balances:Spencer

Highbeam Corporation paid \(\$ 319,500\) to purchase 90 percent ownership of Copper Company on April 1, 20X2. On January 1, 20X2, Copper Company reported the following stockholders' equity balances: \(\square\)Operating results and dividend payments by Copper Company for \(20 \mathrm{X} 2\) were as

Highbeam Corporation exchanged 35,000 shares of its \(\$ 5\) par value common stock for 90 percent ownership of Copper Company on April 1, 20X2, in a business combination recorded as a pooling of interests. On January 1, 20X2, Copper Company reported the following stockholders' equity

Springdale Corporation holds 75 percent of the voting shares of Holiday Services Company. During 20X7 Springdale sold inventory costing \(\$ 60,000\) to Holiday Services for \(\$ 90,000\), and Holiday Services resold one-third of the inventory in 20X7. Also in 20X7, Holiday Services sold land with

Springdale Corporation holds 75 percent of the voting shares of Holiday Services Company. During 20X7 Springdale sold inventory costing \(\$ 60.000\) to Holiday Services for \(\$ 90,000\), and Holiday Services resold one-third of the inventory in 20X7. The remaining inventory was resold in 20X8.

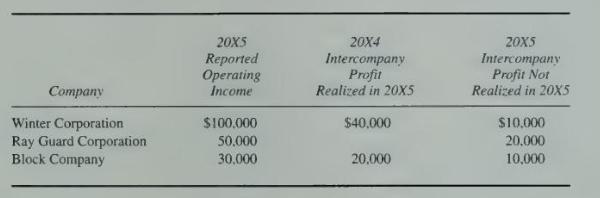

Winter Corporation owns 80 percent of the stock of Ray Guard Corporation and 90 percent of the stock of Block Company. The companies file a consolidated tax return each year and in 20X5 paid a total tax of \(\$ 80,000\). Each of the companies is involved in a number of intercompany inventory

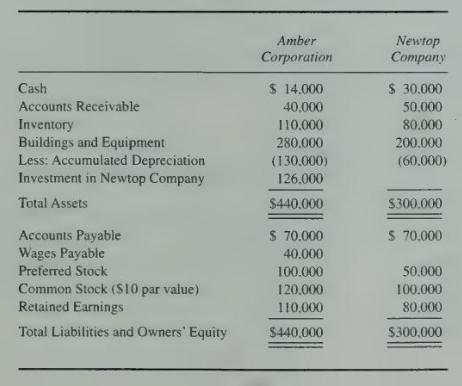

Amber Corporation holds 70 percent of the voting common shares of Newtop Company, but none of its preferred shares. Summary balance sheets for the companies on December 31, 20X1, are as follows:Neither of the preferred issues is convertible. Amber Corporation's preferred pays a 9 percent annual

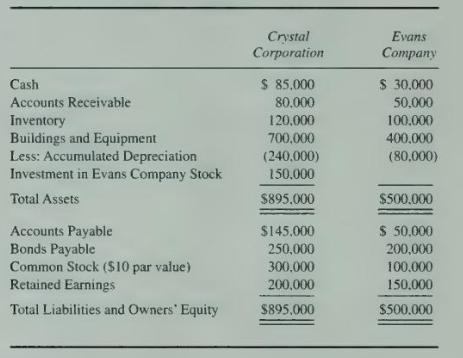

Crystal Corporation owns 60 percent of the common shares of Evans Company. Balance sheet data for the companies on December 31, 20X2, are as follows:The bonds of Crystal Corporation and Evans Company pay annual interest of 8 percent and 10 percent, respectively. The bonds of Crystal Corporation are

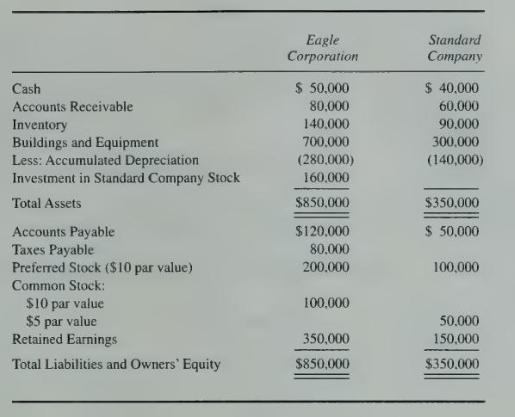

Eagle Corporation holds 80 percent of the common shares of Standard Company. The following balance sheet data are reported by the companies for December 31, 20X1:An 8 percent annual dividend is paid on the Eagle Corporation preferred stock and a 12 percent dividend is paid on the Standard Company

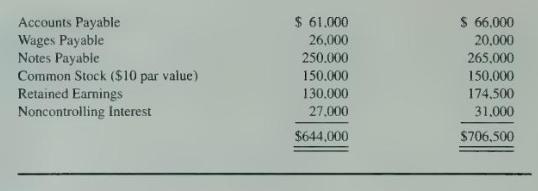

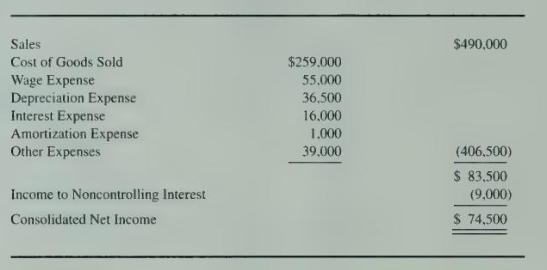

Metal Corporation acquired 75 percent ownership of Ocean Company on January 1, 20X1. Consolidated balance sheets at January 1, 20X3, and December 31, 20X3, are as follows:The consolidated income statement for \(20 \times 3\) contained the following amounts:Metal Corporation and Ocean Company paid

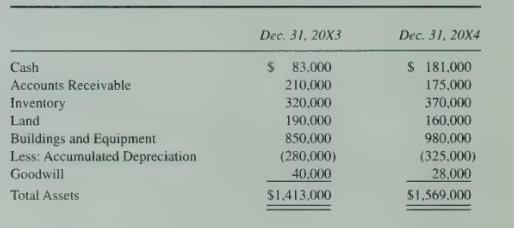

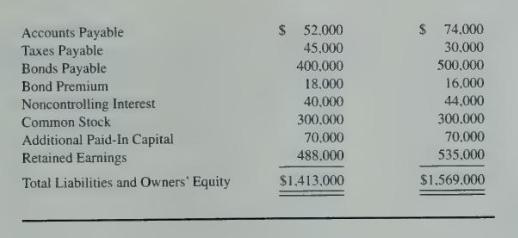

Traper Company holds 80 percent ownership of Arrow Company. The consolidated balance sheets as of December 31, 20X3, and December 31, 20X4, are as follows:The 20X4 consolidated income statement contained the following amounts:Traper purchased its investment in Arrow on January 1, 20X2, for \(\$

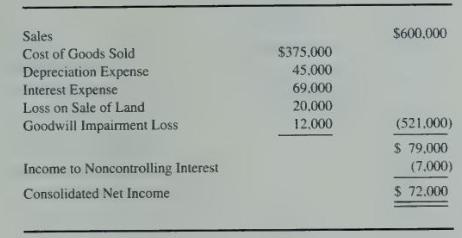

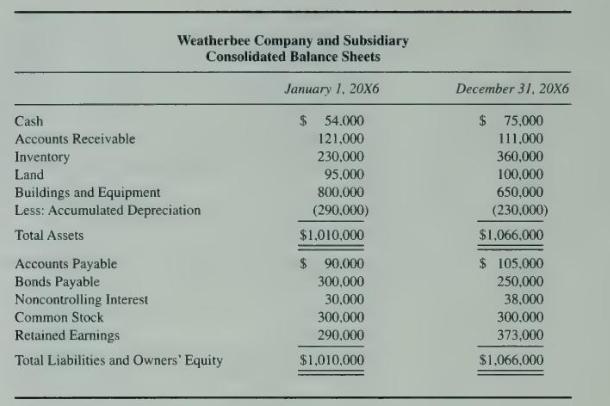

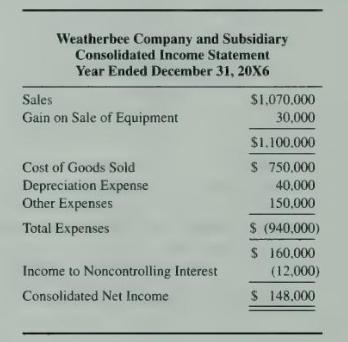

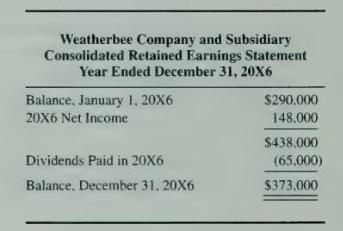

Sun Corporation was created on January 1, 20X2, and quickly became successful. On January 1, 20X6, the owner sold 80 percent of the stock to Weatherbee Company at underlying book value. Weatherbee continued to operate the subsidiary as a separate legal entity and used the equity method in

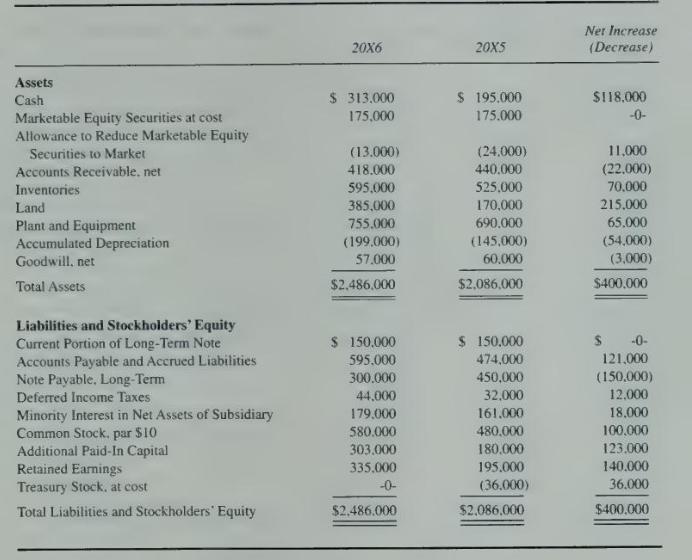

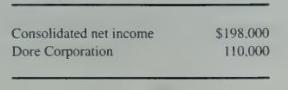

Presented below are the consolidated balance sheet accounts of Brimer Inc. and its subsidiary, Dore Corporation, as of December 31, 20X6 and 20X5.1. On January \(20,20 \mathrm{X} 6\), Brimer Inc. issued 10,000 shares of its common stock for land having a fair value of \(\$ 215.000\).2. On February

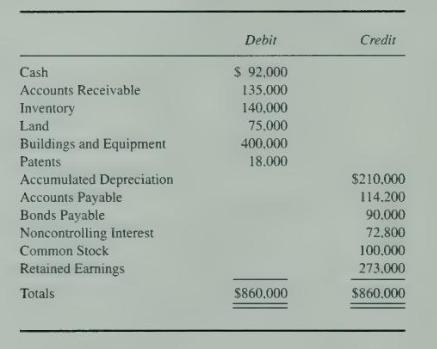

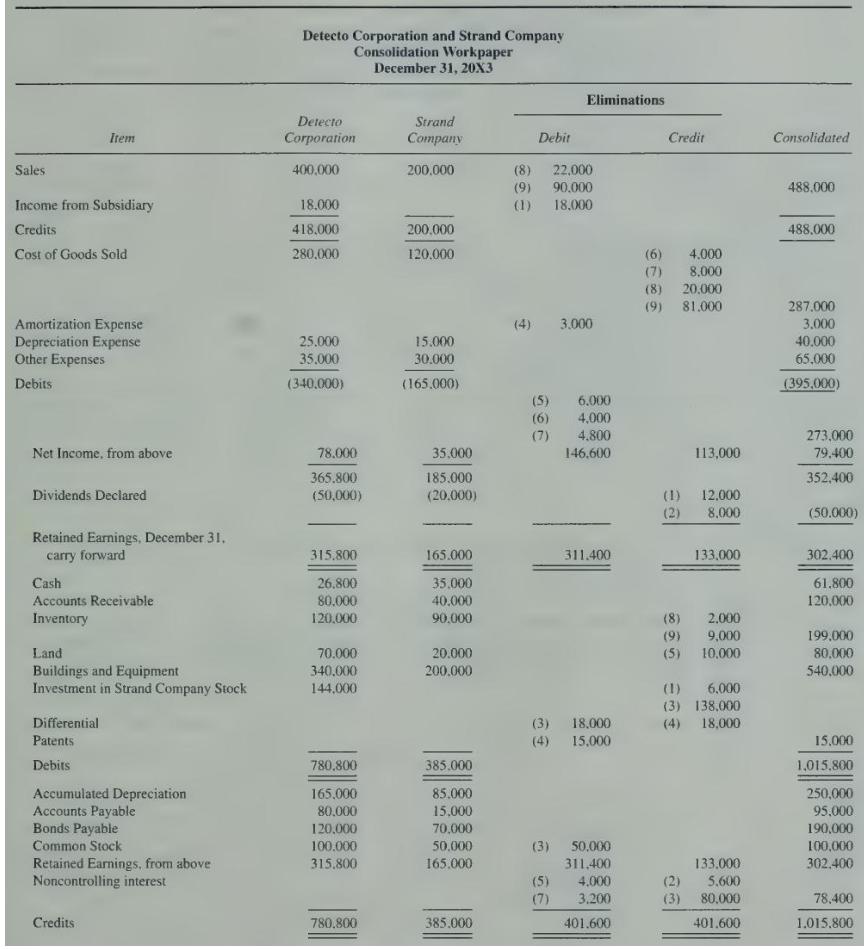

Detecto Corporation purchased 60 percent of the outstanding shares of Strand Company on January \(1,20 \mathrm{X} 1\), for \(\$ 24,000\) more than book value. The full amount of the excess payment is considered related to patents and is being amortized over an eight-year period. In 20X1, Strand

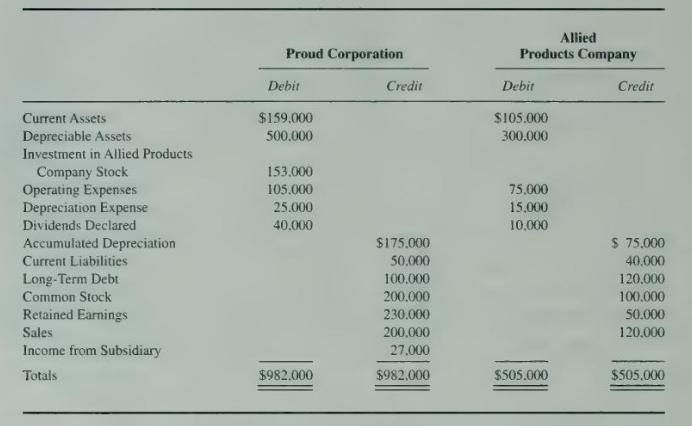

Proud Corporation acquired 90 percent of the voting shares of Allied Products Company in a business combination recorded as a pooling of interests on January 1, 20X2. Proud Corporation uses the equity method in accounting for its ownership of Allied Products. On December 31, 20X3, the trial

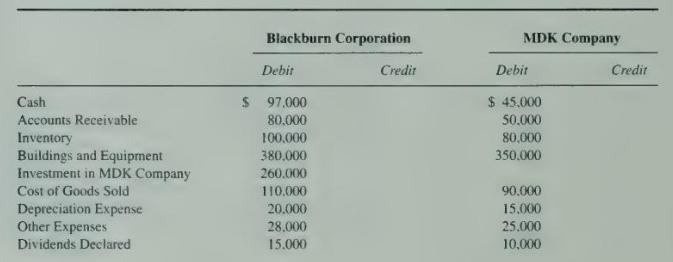

Blackbum Corporation acquired 100 percent ownership of MDK Company on May 13, 20X0, in a business combination recorded as a pooling of interests. Trial balances for the companies on December 31, 20X2, are as follows:Blackburn Corporation uses the equity method in accounting for its ownership of MDK

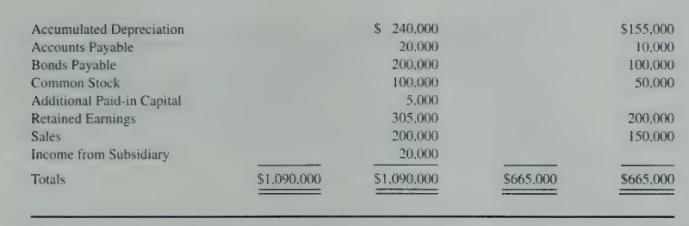

Richardson Corporation was created to develop computer software. On January 1, 20X3. Wealthy Company acquired 90 percent of the common stock of Richardson Corporation in a business combination recorded as a pooling of interests. Wealthy Company continued to operate Richardson Corporation as a

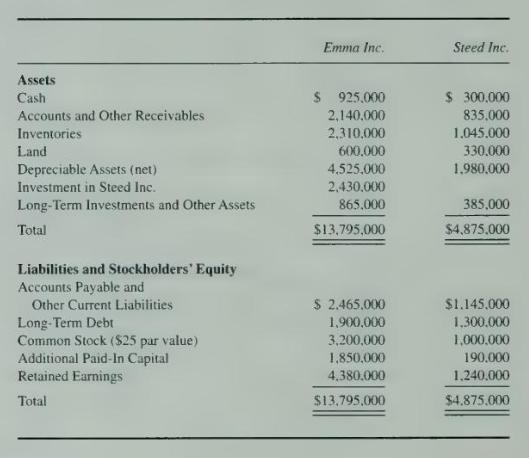

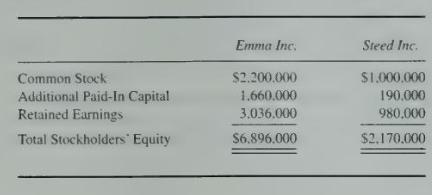

Emma Inc. acquired all the outstanding \(\$ 25\) par value common stock of Steed Inc. on June 30, \(20 X 7\), in exchange for 40,000 shares of its \(\$ 25\) par value common stock. The business combination meets all conditions for a pooling of interests. On June 30, 20X7, Emma's common stock closed

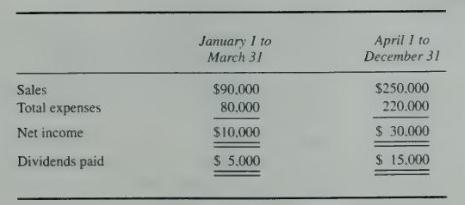

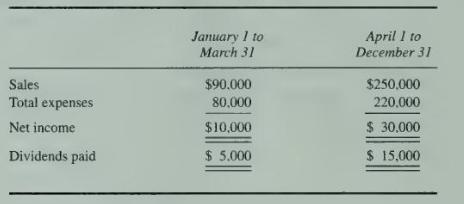

Blase Company operates on a calendar-year basis, reporting the results of operations quarterly. For the first quarter of \(20 \mathrm{XI}\). Blase reported net income of \(\$ 60,000\) and paid a dividend of \(\$ 10,000\). On April 1. Starstruck Theaters Inc. purchased 85 percent of the common stock

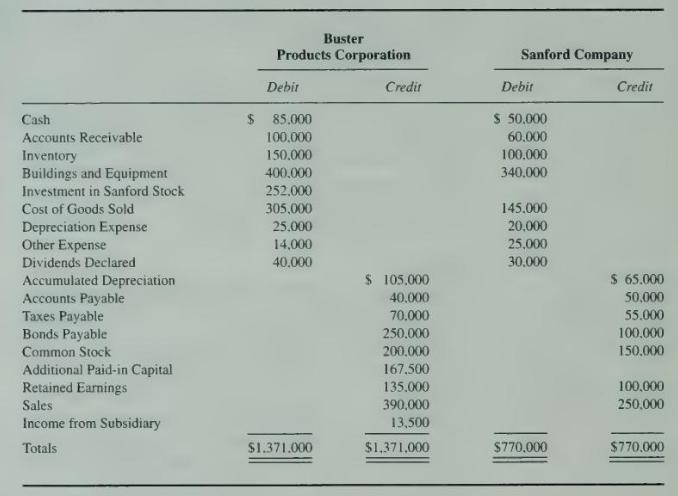

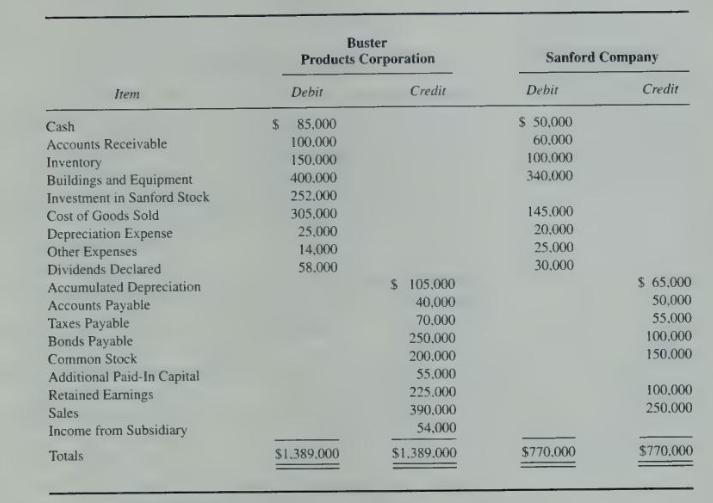

Buster Products Corporation acquired 90 percent ownership of Sanford Company on October 20. 20X2. through an exchange of voting shares in a transaction recorded as a purchase. Buster Products issued 8,000 shares of its \(\$ 10\) par stock to acquire 27,000 shares of Sanford Company \(\$ 5\) par

Buster Products Corporation acquired 90 percent ownership of Sanford Company on October 20, \(20 \mathrm{X} 2\), through an exchange of voting shares in a transaction qualifying as a pooling of interests. Buster Products issued 8.000 shares of its \(\$ 10\) par stock to acquire 27.000 shares of

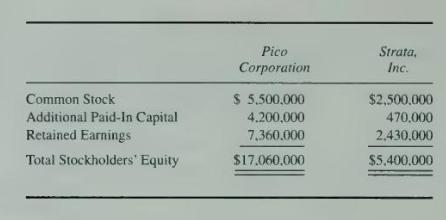

Pico Corporation issued 200,000 shares of its \(\$ 10\) par common stock on March 31, 20X0, to acquire all the outstanding \(\$ 25\) par value common stock of Strata Inc. The business combination meets all conditions for a pooling of interests. On March 31, 20X0, the market price of Pico's common

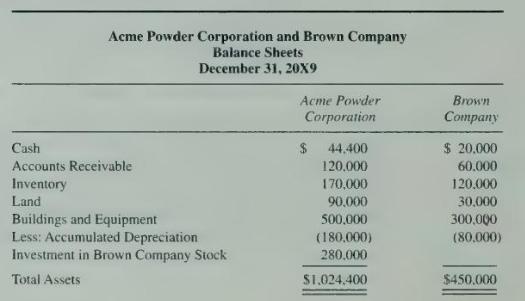

Acme Powder Corporation purchased 70 percent of the stock of Brown Company on December 31, 20X7, at underlying book value. The balance sheets of the two companies on December 31, 20X9, are as follows:On December 31, 20X9, Acme Powder Corporation holds inventory purchased from Brown Company for \(\$

Broom Manufacturing used cash to purchase 75 percent of the voting stock of Satellite Industries on January 1, 20X3, at underlying book value. Broom accounts for its investment in Satellite using the basic equity method.Broom Manufacturing had no inventory on hand on January 1, 20X5. During 20X5

Hardtack Bread Company holds 70 percent of the common shares of Custom Pizza Corporation. Trial balances for the two companies on December 31, 20X7, are as follows:At the beginning of \(20 \times 7\), Hardtack held inventory purchased from Custom Pizza Corporation containing unrealized profits of

Branch Manufacturing Corporation owns 80 percent of the common shares of Short Retail Stores. The balance sheets of the companies as of December 31,20X4, were as follows:The 8 percent preferred stock of Short Retail is convertible into 12,000 shares of common stock, and Short's 10 percent bonds are

Mighty Corporation holds 80 percent of the common stock of Longfellow Company. The following balance sheet data are presented for December 31, 20X7:Longfellow Company reported net income of \(\$ 115,000\) in \(20 \times 7\) and paid dividends of \(\$ 60,000\). The Longfellow Company bonds have an

Select the correct answer for each of the following questions.1. Perez Inc. owns 80 percent of Senior Inc. During 20X2, Perez sold goods with a 40 percent gross profit to Senior. Senior sold all of these goods in 20X2. For 20X2 consolidated financial statements, how should the summation of Perez

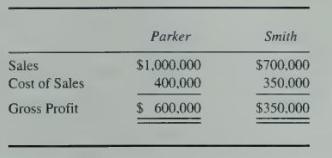

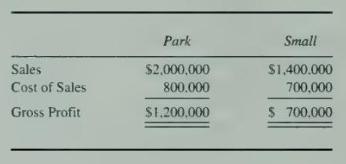

Select the correct answer for each of the following questions.1. During 20X3. Park Corporation recorded sales of inventory costing \(\$ 500,000\) to Small Company, its wholly owned subsidiary, on the same terms as sales made to third parties. At December 31, 20X3, Small held one-fifth of these

Select the correct answer for each of the following questions.Blue Company purchased 60 percent ownership of Kelly Corporation in 20X1. On May 10. 20X2, Kelly purchased inventory from Blue for \(\$ 60,000\). Kelly sold all of the inventory to an unaffiliated company for \(\$ 86,000\) on November

Select the correct answer for each of the following questions.Lorn Corporation purchased inventory from Dresser Corporation for \(\$ 120,060\) on September 20. 20X1, and resold 80 percent of the inventory to unaffiliated companies prior to December 31 . 20X1, for \(\$ 140,000\). Dresser Corporation

Select the correct answer for each of the following questions.Showtime Corporation holds 80 percent of the stock of Movie Productions Inc. During 20X4, Showtime purchased an inventory of snack bar items for \(\$ 40,000\) and resold \(\$ 30,000\) to Movie Productions Inc. for \(\$ 48,000\). Movie

Nordway Corporation purchased 90 percent of the voting shares of stock of Olman Company in 20X1. During 20X4, Nordway purchased 40,000 Playday doghouses for \(\$ 24\) each and sold 25,000 of the doghouses to Olman for \(\$ 30\) each. Olman sold all of the doghouses to retail establishments prior to

Nordway Corporation purchased 90 percent of the voting shares of stock of Olman Company in 20X1. During 20X4, Nordway purchased 40,000 Playday doghouses for \(\$ 24\) each and sold 25,000 of the doghouses to Olman for \(\$ 30\) each. Olman sold 18,000 of the doghouses to retail establishments prior

Karlow Corporation owns 60 percent of the voting shares of Draw Company. During 20X3, Karlow produced 25.000 computer desks at a cost of \(\$ 82\) each and sold 10.000 desks to Draw Company for \(\$ 94\) each. Draw Company sold 7.000 of the desks to unaffiliated companies for \(\$ 130\) each prior

Holiday Bakery owns 60 percent of the stock of Farmco Products Company. During 20X8. Farmco Products produced 100.000 bags of flour, which it sold to Holiday Bakery for \(\$ 900.000\). On December 31. 20X8. Holiday Bakery had 20.000 bags of flour purchased from Farmco Products on hand. Farmco

Holiday Bakery owns 60 percent of the stock of Farmco Products. On January 1, 20X9. inventory reported by Holiday Bakery included 20.000 bags of flour purchased from Farmco Products at \(\$ 9\) per bag. By December 31. 20X9. all the beginning inventory purchased from Farmco Products had been baked

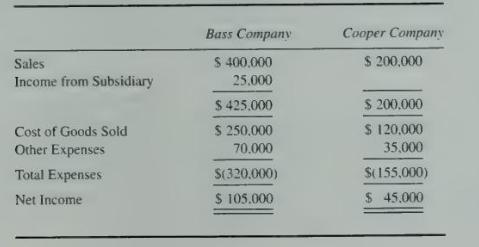

Bass Company purchased 60 percent of the voting shares of Cooper Company for \(\$ 260,000\) on January 1. 20X2. Cooper Company reported total stockholders' equity of \(\$ 400.000\) at the time of acquisition. The purchase differential is assigned to patents with an expected economic life of 10

The price of high-quality burnwhistles fluctuates substantially from month to month. As a result, it is not uncommon for a company that deals in burnwhistles to report a substantial gain in one period, followed by a substantial loss in the following period. The price of burnwhistles was relatively

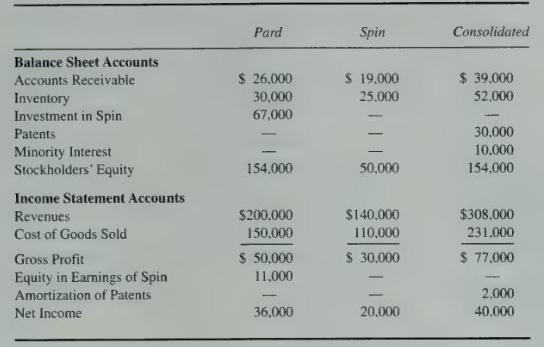

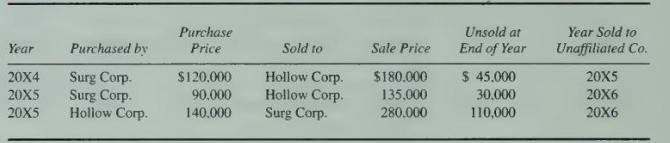

Hollow Corporation purchased 70 percent of the voting stock of Surg Corporation on May 18, 20X1, at underlying book value. The companies reported the following data with respect to intercompany sales in 20X4 and 20X5:Hollow Corporation reported operating income (excluding income from its investment

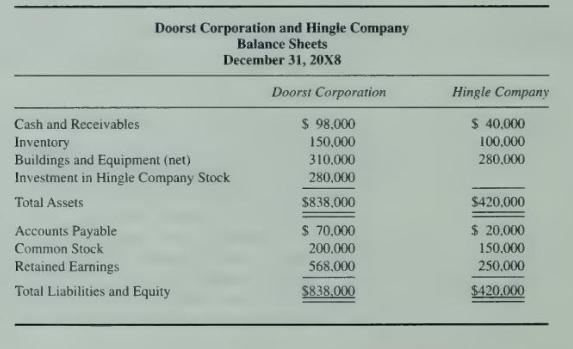

The December 31, 20X8, balance sheets for Doorst Corporation and its 70 percent owned subsidiary Hingle Company contained the following summarized amounts:Doorst purchased the shares of Hingle Company at underlying book value on January 1, 20X7. On December 31, 20X8, the balance sheet of Doorst

Klon Corporation owns 70 percent of the stock of Brant Company and 60 percent of the stock of Torkel Company. During 20X8, Klon sold inventory purchased in 20X7 for \(\$ 100,000\) to Brant Company for \(\$ 150,000\). Brant then sold the inventory at its cost of \(\$ 150,000\) to Torkel. Prior to

Herb Corporation holds 60 percent ownership of Spice Company. Each year, Spice Company purchases large quantities of a gnarl root used in producing health drinks. Spice purchased \(\$ 150,000\) of roots in \(20 \times 7\) and sold \(\$ 40,000\) of these purchases to Herb Corporation for \(\$

Home Products Corporation sells a broad line of home detergent products. Home Products owns 75 percent of the stock of Level Brothers Soap Company. During 20X8, Level Brothers sold soap products to Home Products for \(\$ 180,000\), which it had produced for \(\$ 120,000\). Home Products sold \(\$

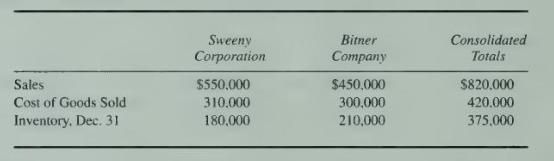

Sweeny Corporation owns 60 percent of the shares of Bitner Company. Partial 20X2 financial data for the companies and consolidated entity were as follows:On January 1, 20X2, the inventory of Sweeny Corporation contained items purchased from Bitner Company for \(\$ 75,000\). The cost of the units to

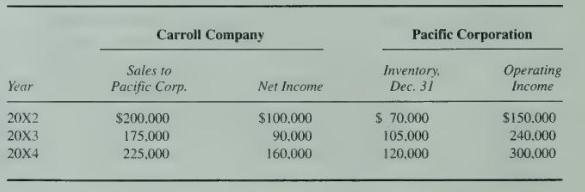

Carroll Company sells all its output at 25 percent above cost. Pacific Corporation purchases all its inventory from Carroll Company. Selected information on the operations of the companies over the past three years is as follows:Pacific Corporation purchased 60 percent of the ownership of Carroll

Stem Corporation purchased 70 percent of the voting stock of Crown Corporation on January 1, 20X2, for \(\$ 465,000\). At that date, Crown reported common stock outstanding of \(\$ 200,000\) and retained earnings of \(\$ 350,000\). The purchase differential is assigned to buildings with an expected

In preparing the consolidation workpaper for Bolger Corporation and its 60 percent owned subsidiary, Feldman Company, the following eliminating entries were proposed by the bookkeeper for Bolger Corporation:The bookkeeper for Bolger recently graduated from Oddball University, and while the dollar

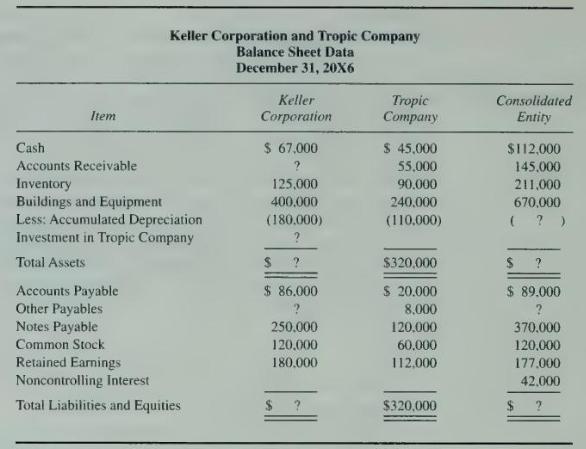

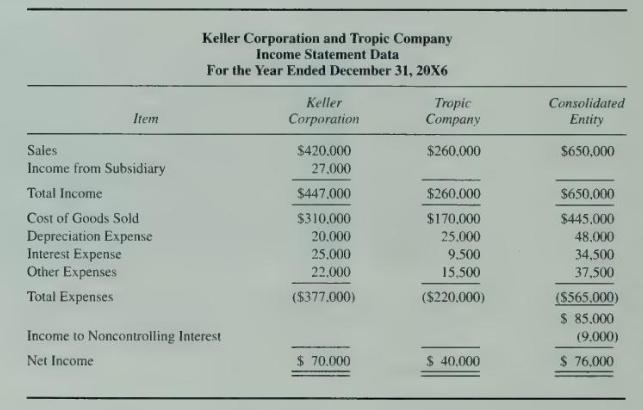

Keller Corporation acquired 75 percent of the ownership of Tropic Company on January 1, 20X1. The purchase differential paid by Keller is assigned to buildings and equipment and expensed over 10 years. Financial statement data for the two companies and the consolidated entity at December \(31,20

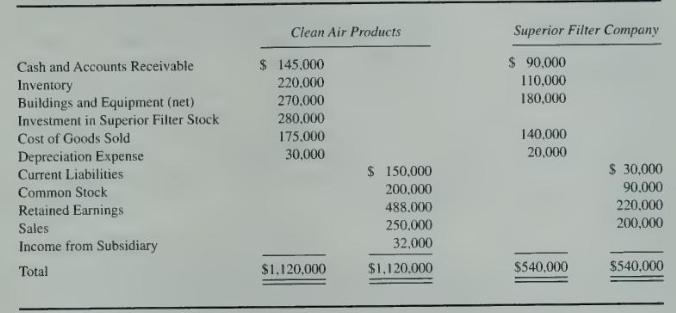

Clean Air Products owns 80 percent of the stock of Superior Filter Company, which it acquired at underlying book value on August 30,20X6. Summarized trial balance data for the two companies as of December \(31,20 \times 8\), are as follows:On January 1, 20X8, the inventory held by Clean Air

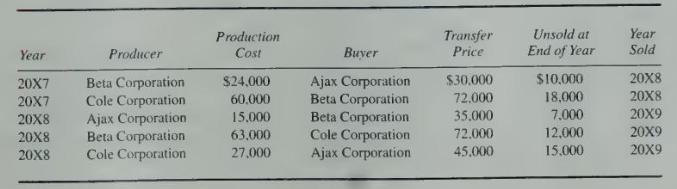

Ajax Corporation purchased at book value 70 percent of the ownership of Beta Corporation and 90 percent of the ownership of Cole Corporation in 20X5. There are frequent intercompany transfers among the companies. Activity relevant to \(20 \mathrm{X} 8\) is presented below.For the year ended

On January 1, 20X1, Priority Corporation purchased 90 percent of the common stock of Tall Corporation at underlying book value. Priority uses the equity method in accounting for its investment in Tall. The stockholders' equity section of Tall at January 1, 20X5, contained the following

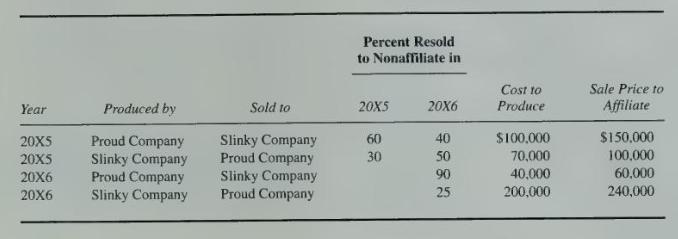

Proud Company and Slinky Company both produce and purchase equipment for resale each period and frequently sell to each other. Since Proud Company holds 60 percent ownership of Slinky Company, the controller of Proud compiled the following information with regard to intercompany transactions

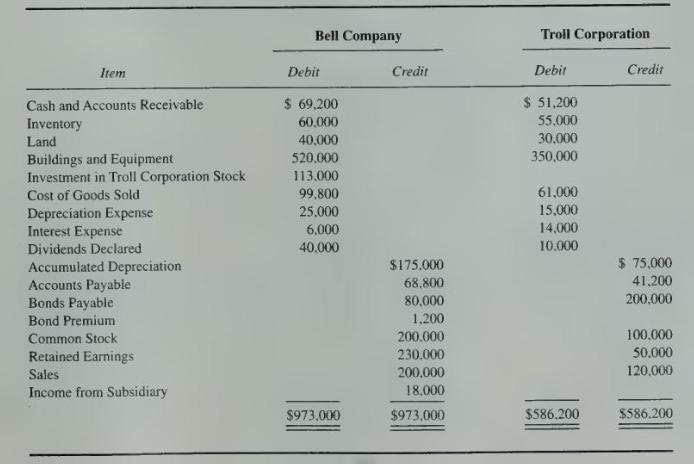

Bell Company purchased 60 percent ownership of Troll Corporation on January 1, 20X1, for \(\$ 83,000\). On that date, Troll reported common stock outstanding of \(\$ 100,000\) and retained earnings of \(\$ 20,000\). The purchase differential is assigned to land to be used as a future building site.

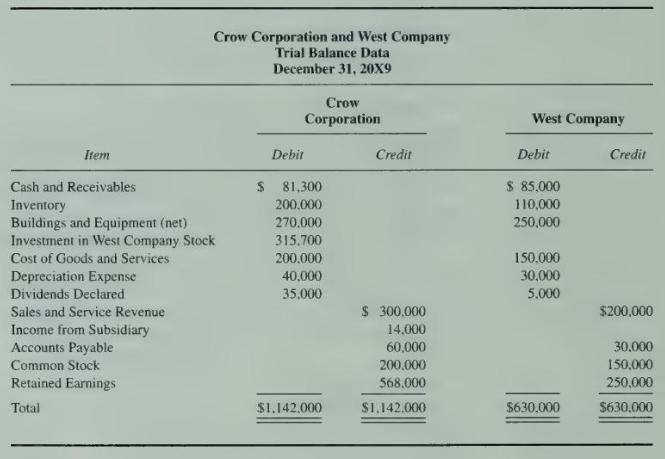

Crow Corporation purchased 70 percent of the voting common stock of West Company on January \(1,20 \times 7\), for \(\$ 291,200\). On that date, the book value of West Company's net assets was \(\$ 380,000\), and their book values were equal to fair values, except for land that had a fair value

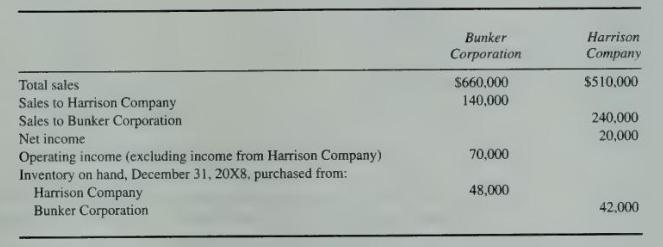

Bunker Corporation owns 80 percent of the stock of Harrison Company. At the end of 20X8, Bunker Corporation and Harrison Company reported the following partial operating results and inventory balances:Bunker Corporation regularly prices its products at cost plus a 40 percent markup for profit.

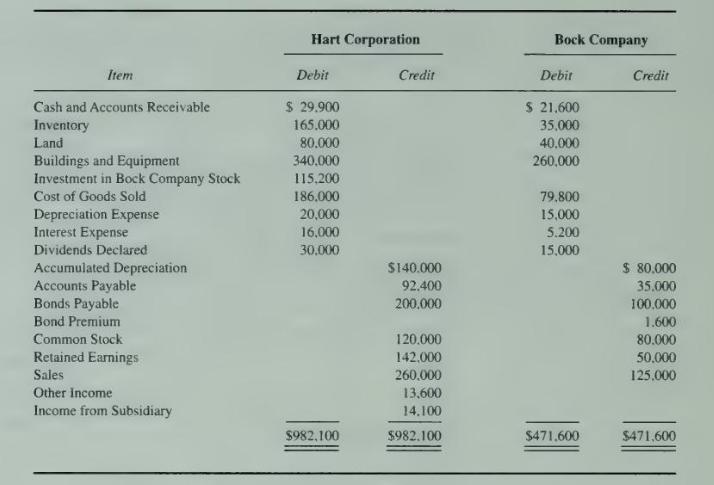

Hart Corporation purchased 70 percent of the voting common shares of Bock Company on January \(1,20 \times 2\), for \(\$ 94,000\). At that date, Bock Company had \(\$ 80,000\) of common stock outstanding and retained earnings of \(\$ 20,000\). The excess of the amount paid over underlying book

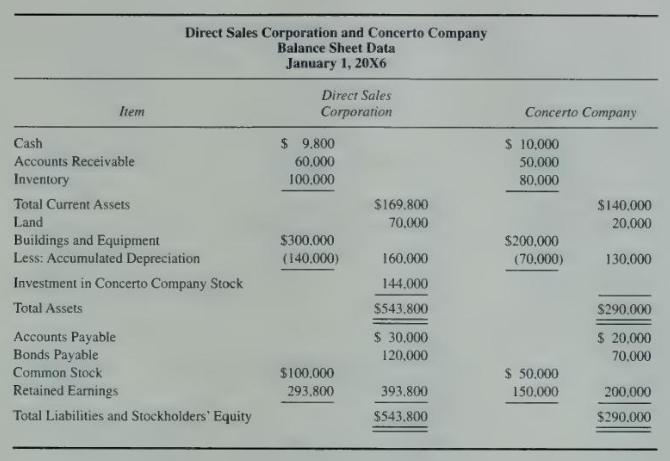

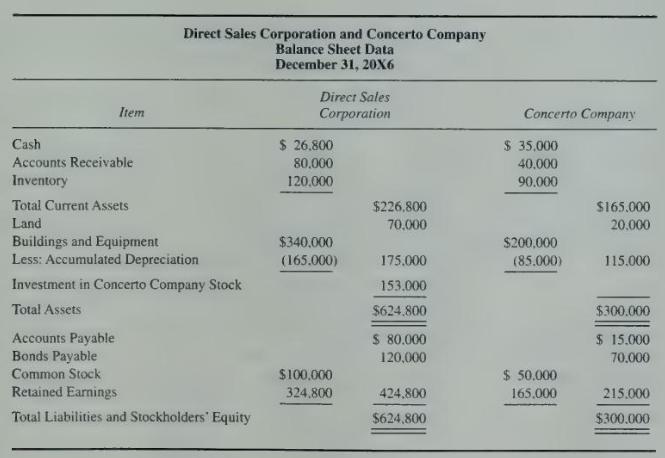

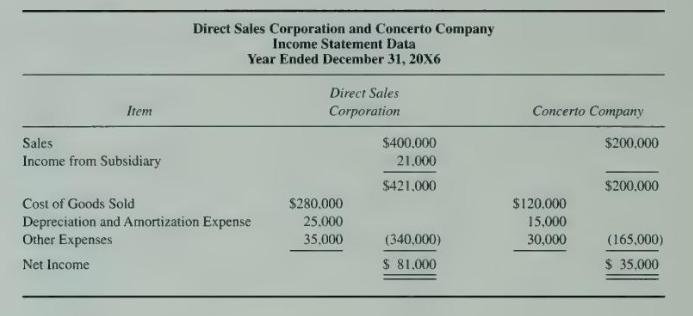

Direct Sales Corporation purchased 60 percent of the stock of Concerto Company on January 1, 20X3, for \(\$ 24.000\) in excess of the underlying book value. The difference relates to goodwill. At December 31, 20X6, the management of Direct Sales reviewed the amount attributed to goodwill and

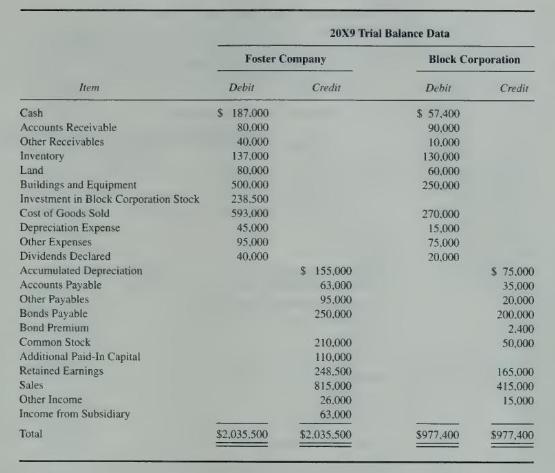

Block Corporation was created on January 1, 20X0, to develop computer software. On January 1, 20X5, Foster Company purchased 90 percent of the common stock of Block Corporation at underlying book value. Trial balances for Foster Company and Block Corporation on December 31, 20X9, are as follows:On

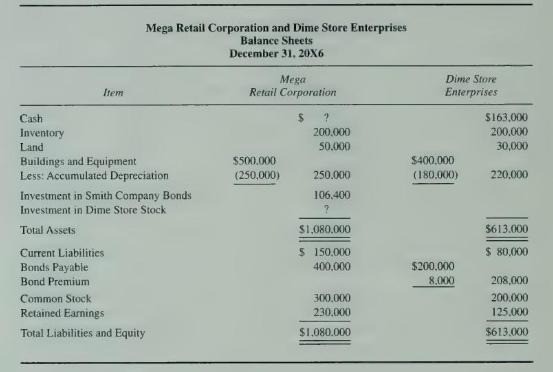

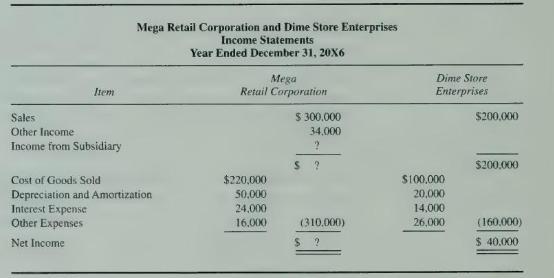

Mega Retail Corporation purchased 80 percent of the voting shares of Dime Store Enterprises on January 1, 20X4, for \(\$ 227,200\). On that date Dime Store Enterprises reported retained earnings of \(\$ 50,000\) and common stock outstanding of \(\$ 200,000\).Partial balance sheets and income

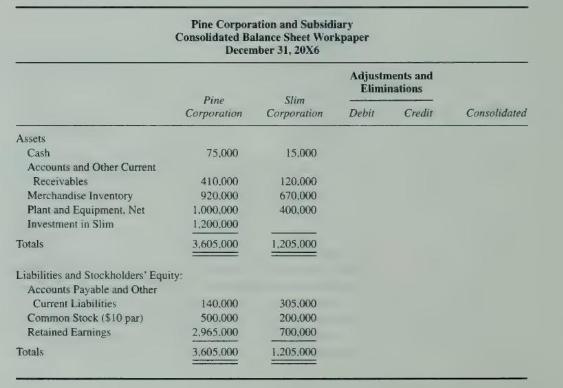

The December 31, 20X6, condensed balance sheets of Pine Corporation. and its 90 percent owned subsidiary, Slim Corporation, are presented in the accompanying worksheet.Additional information is as follows:- Pine's investment in Slim was purchased for \(\$ 1,200,000\) cash on January 1, 20X6, and is

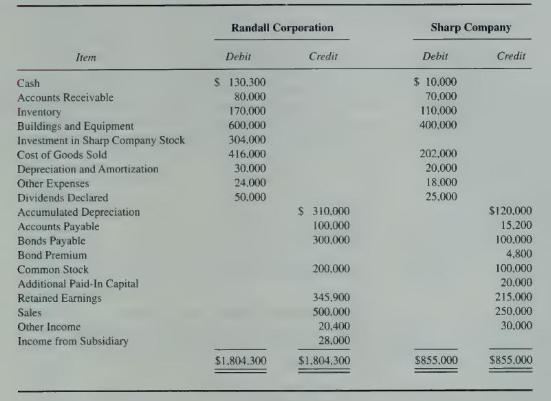

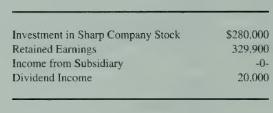

Randall Corporation acquired 80 percent of the voting shares of Sharp Company on January 1 . 20X4, for \(\$ 280,000\) in cash and marketable securities. At the time of acquisition, Sharp Company reported net assets of \(\$ 300,000\). Trial balances for the two companies on December \(31,20 \times

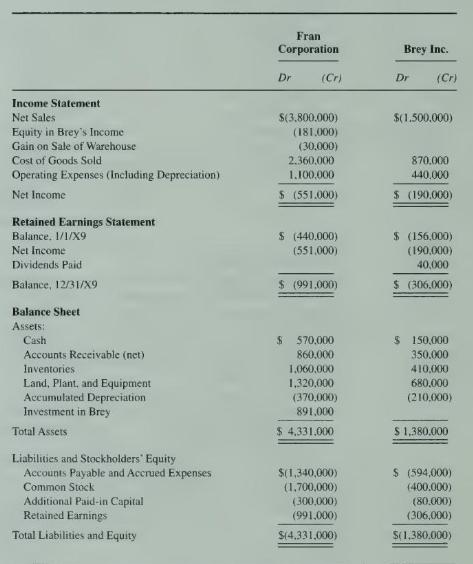

Fran Corporation acquired all the outstanding \(\$ 10\) par value voting common stock of Brey Inc. on January 1, 20X9. in exchange for 25,000 shares of its \(\$ 20\) par value voting common stock. On December \(31,20 X 8\). Fran's common stock had a closing market price of \(\$ 30\) per share on a

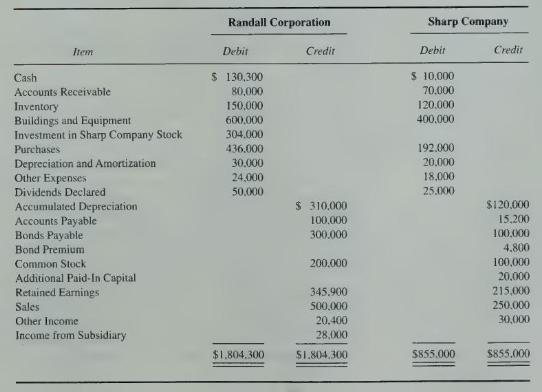

Randall Corporation acquired 80 percent of the voting shares of Sharp Company on January 1, 20X4, for \(\$ 280,000\) in cash and marketable securities. At the time of acquisition, Sharp Company reported net assets of \(\$ 300,000\). Trial balances for the two companies on December \(31,20 X 7\),

On December 31, 20X7, Randall Corporation recorded the following entry on its books to adjust from the basic equity method to the fully adjusted equity method for its investment in Sharp Company stock:\section*{Required}a. Adjust the data reported by Randall Corporation in the trial balance

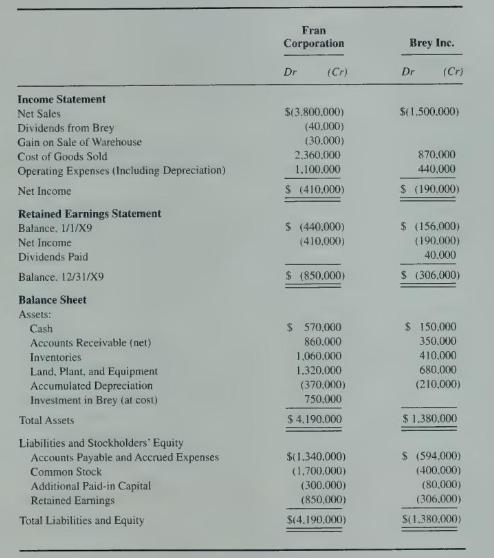

Fran Corporation acquired all the outstanding \(\$ 10\) par value voting common stock of Brey Inc. on January 1,20X9, in exchange for 25,000 shares of its \(\$ 20\) par value voting common stock. On December 31, 20X8. Fran's common stock had a closing market price of \(\$ 30\) per share on a

The trial balance data presented in Problem 7-35 can be converted to reflect use of the cost method by inserting the following amounts in place of those presented for Randall Corporation:\section*{Required}a. Prepare the journal entries that would have been recorded on the books of Randall

When a bond issue has been placed directly with an affiliate, what account balances will be stated incorrectly in the consolidated statements if the intercompany bond ownership is not eliminated in preparing the consolidation workpaper?

When bonds of an affiliate are purchased from a nonaffiliate during the period, what balances will be stated incorrectly in the consolidated financial statements if the intercompany bond ownership is not eliminated in preparing the consolidation workpaper?

When a parent company sells land to a subsidiary at more than book value, the consolidation eliminating entries at the end of the period include a debit to the gain on the sale of land. When a parent purchases the bonds of a subsidiary from a nonaffiliate at less than book value, the eliminating

What is the effect on consolidated net income of eliminating intercompany interest income and interest expense when there has been a direct sale of bonds to an affiliate? Why?

What is the effect on consolidated net income of eliminating intercompany interest income and interest expense when a loss on bond retirement has been reported in a prior year's consolidated financial statements as a result of a constructive retirement of an affiliate's bonds? Why?

If the bonds of an affiliate are purchased from a nonaffiliate at the beginning of the current year, how can the amount of the gain or loss on constructive retirement be computed by looking at the year-end trial balances of the two companies?

When the parent company purchases the bonds of a subsidiary from a nonaffiliate for more than book value, what income statement accounts will be affected in preparing consolidated financial statements? What will be the effect of the purchase upon consolidated net income? Explain.

When a subsidiary purchases the bonds of its parent from a nonaffiliate for less than book value, what will be the effect on consolidated net income?

How is the amount of income assigned to the noncontrolling interest affected when bonds of the subsidiary are purchased by the parent from an unaffiliated company for less than book value?

How would the relationship between interest income recorded by a subsidiary and interest expense recorded by the parent be expected to change when a direct placement of the parent's bonds with the subsidiary is compared with a constructive retirement in which the subsidiary purchases the bonds of

A subsidiary purchased bonds of the parent company from a nonaffiliate in the preceding period, and a gain on bond retirement was reported in the consolidated income statement as a result of the purchase. What effect will that event have on the amount of consolidated net income reported in the

A parent company purchased bonds of its subsidiary from a nonaffiliate in the preceding year, and a loss on bond retirement was reported in the consolidated income statement. How will income assigned to the noncontrolling interest be affected in the year following the constructive retirement?

A parent purchases bonds of a subsidiary directly from the subsidiary. The parent later sells the bonds to a nonaffiliate. From a consolidated viewpoint, what occurs when the parent sells the bonds? Is a gain or loss reported in the consolidated income statement when the parent sells the bonds? Why?

Shortly after a parent company purchased its subsidiary's bonds from a nonaffiliate, the subsidiary retired the entire issue. How is the gain or loss on bond retirement that is reported by the subsidiary treated for consolidation purposes?

Describe the consolidation procedures needed to deal with intercorporate leasing arrangements for the following types of leases: (a) operating, (b) direct financing, and (c) sales-type.

Bradley Corporation sold bonds to Flood Company in 20X2 at 90 . At the end of 20X4, Century Corporation purchased the bonds from Flood Company at 105. Bradley Corporation then retired the full bond issue on December 31, 20X7, at 101. Century Corporation holds 80 percent of the voting stock of

The controller of Snerd Corporation is experiencing difficulty in explaining the impact of several of the company's intercorporate bond transactions.\section*{Required}a. Snerd receives interest payments in excess of the amount of interest income it records on its investment in Snort bonds. Did

Intercompany debt, both long-term and short-term, arises frequently. In some cases intercorporate borrowings may arise because one affiliate can borrow at a cheaper rate than others, and lending to other affiliates may reduce the overall cost of borrowing. In other cases, intercompany

Lamar Corporation owns 60 percent of the voting shares of Humbolt Corporation. On January 1 . 20X2, Lamar Corporation sold \(\$ 150,000\) par value 6 percent first mortgage bonds to Humbolt for \(\$ 156,000\). The bonds mature in 10 years and pay interest seminannually on January 1 and July

Nettle Corporation sold \(\$ 100,000\) par value, 10 -year, first mortgage bonds to Timberline Corporation on January 1, 20X5. The bonds, which bear a nominal interest rate of 12 percent, pay interest semiannually on January 1 and July 1. The entry to record interest income by Timberline

Wood Corporation owns 70 percent of the voting shares of Carter Company. On January 1, 20X3, Carter Company sold bonds with a par value of \(\$ 600,000\) at 98 . Wood Corporation purchased \(\$ 400,000\) par value of the bonds and the remainder was sold to nonaffiliates. The bonds mature in five

Stellar Corporation purchased bonds of its subsidiary from a nonaffiliate during 20X6. Although Stellar purchased the bonds at par value, a loss on bond retirement is reported in the 20X6 consolidated income statement as a result of the purchase.\section*{Required}a. Were the bonds originally sold

Select the correct answer for each of the following questions.1. [AICPA Adapted] Wagner, a holder of a \(\$ 1,000,000\) Palmer Inc. bond, collected the interest due on March 31, 20X8, and then sold the bond to Seal Inc. for \(\$ 975.000\). On that date. Palmer, a 75 percent owner of Seal, had a

Parent Company paid a nonaffiliate \(\$ 95,000\) in \(20 \times 4\) to purchase bonds that are recorded as a liability of \(\$ 105,000\) on the books of Subsidiary Company. Parent Company owns 60 percent of the shares of Subsidiary Company stock. The bonds have five years remaining to maturity from

On January 1, 20X4, Passive Heating Corporation paid \(\$ 104,000\) for \(\$ 100,000\) par value, 9 percent bonds of Solar Energy Corporation. Solar Energy Corporation had issued \(\$ 300,000\) of the 10 -year bonds on January 1, 20X2, for \(\$ 360,000\). Passive previously had purchased 80 percent

Able Company issued \(\$ 600,000\) of 9 percent first mortgage bonds on January 1. 20X1, at 103. The bonds mature in 20 years and pay interest semiannually on January 1 and July 1. Prime Corporation purchased \(\$ 400,000\) of Able's bonds from the original purchaser on December 31, 20X5, for \(\$

Able Company issued \(\$ 600,000\) of 9 percent first mortgage bonds on January 1, 20X1, at 103. The bonds mature in 20 years and pay interest semiannually on January 1 and July 1. Prime Corporation purchased \(\$ 400,000\) of Able's bonds from the original purchaser on January 1, 20X5, for \(\$

Farley Corporation owns 70 percent of the stock of Snowball Enterprises. On January 1, 20X1, Farley Corporation sold \(\$ 1,000,000\) par value 7 percent, 20 -year, first mortgage bonds to Kling Corporation at 97 . On January 1, 20X8, Snowball Enterprises purchased \(\$ 300,000\) par value of the

Apple Corporation holds 60 percent of the voting shares of Shortway Publishing Company. Apple Corporation issued \(\$ 500,000\) of 10 percent bonds with a 10 -year maturity on January 1, 20X2, at 90. On January 1, 20X8, Shortway Publishing Company purchased \(\$ 100,000\) of the Apple Corporation

Showing 400 - 500

of 2939

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers