New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

advanced financial accounting

Advanced Financial Accounting 5th Edition Richard E. Baker, Valdean C. Lembke, Thomas E. King - Solutions

Downlink Corporation is 95 percent owned by Online Enterprises. On January 1, 20X1, Downlink Corporation issued \(\$ 200,000\) of five-year bonds at 115 . Annual interest of 12 percent is paid semiannually on January 1 and July 1. Online Enterprises purchased \(\$ 100,000\) of the bonds on August

Bundle Company issued \(\$ 500,000\) par value 10 -year bonds at 104 on January 1, 20X3, which were purchased by Mega Corporation. The coupon rate on the bonds is 11 percent. Interest payments are made semiannually on July 1 and January 1. On July 1, 20X6, Parent Company purchased \(\$ 200,000\)

Stang Corporation issued to Bradley Company \(\$ 400,000\) par value, 10 -year bonds with a coupon rate of 12 percent on January \(1,20 \mathrm{X} 5\), at 105 . The bonds pay interest semiannually on July 1 and January 1. On January 1, 20X8, Purple Corporation purchased \(\$ 100,000\) of the bonds

Thomas Company owns 95 percent of the common stock of Bradley Financial Corporation, from which Thomas leases some of the assets it uses in its operations. On November 7, 20X8, Thomas entered into an operating lease with Bradley under which Thomas leases several delivery trucks for \(\$ 38.000\)

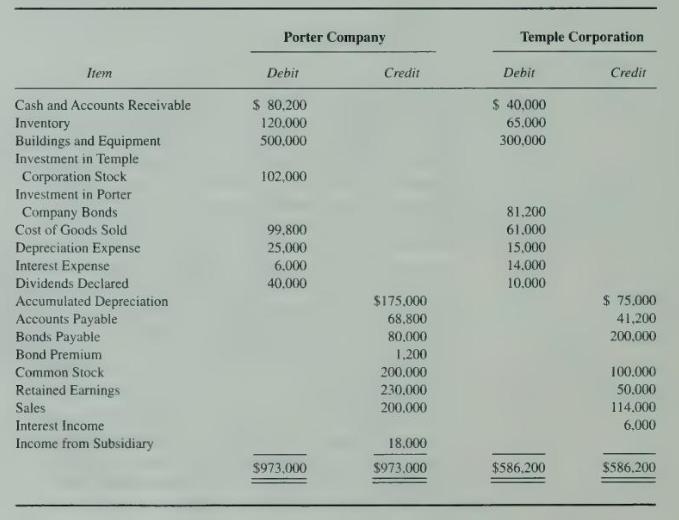

Porter Company purchased 60 percent ownership of Temple Corporation on January 1, 20X1, at underlying book value. On that date, Porter sold $80,000 par value 8 percent five-year bonds directly to Temple for $82,000. The bonds pay interest annually on December 31. Porter uses the basic equity method

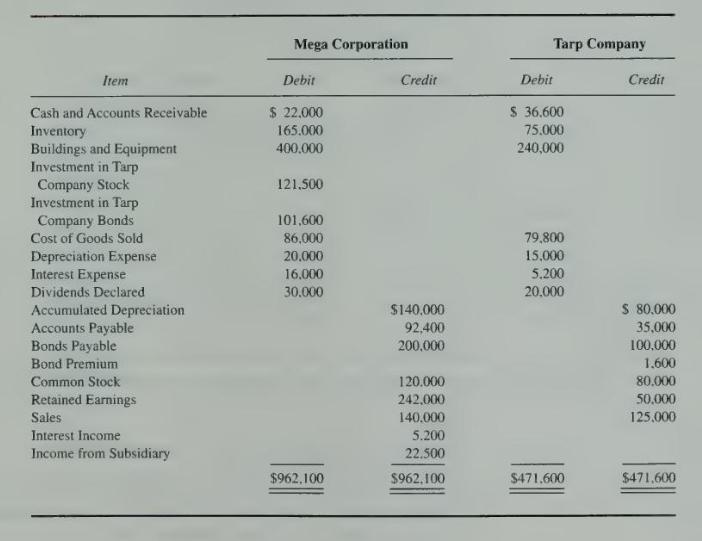

Mega Corporation purchased 90 percent of the voting common shares of Tarp Company on January 1, 20X2 at underlying book value. Mega also purchased \(\$ 100,000\) of 6 percent five-year bonds directly from Tarp on January 1, 20X2, for \(\$ 104,000\). The bonds pay interest semiannually on July 1 and

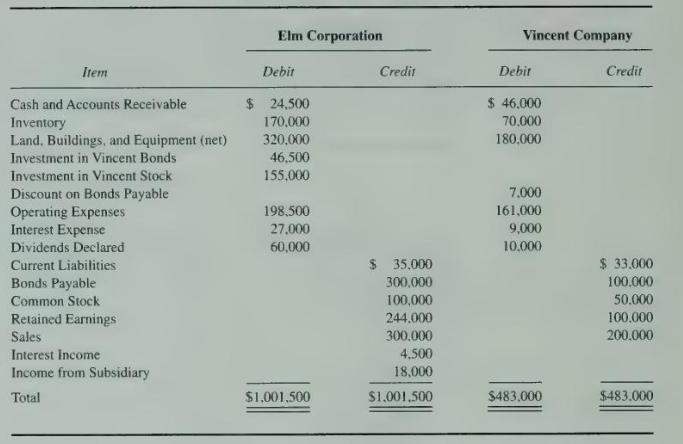

On January 1, 20X1, Elm Corporation paid Morton Advertising \(\$ 122,000\) to acquire 70 percent of the stock of Vincent Company. Elm Corporation also paid \(\$ 45,000\) to acquire \(\$ 50,000\) par value 8 percent 10 -year bonds directly from Vincent Company on that date. Interest payments are

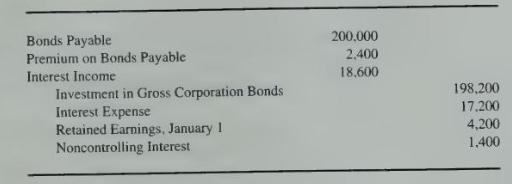

Gross Corporation issued \(\$ 500,000\) par value, 10 -year, bonds at 104 on January 1, 20X1, which were purchased by Independent Corporation. On July 1, 20X5, Rupp Corporation purchased \(\$ 200,000\) par value bonds of Gross Corporation from Independent Corporation. The bonds pay interest of 9

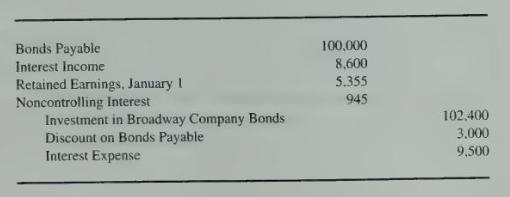

Amazing Corporation purchased \(\$ 100,000\) par value bonds of its subsidiary, Broadway Company, on December 31, 20X5, from Lemon Corporation. The 10 -year bonds bear a 9 percent coupon rate and were originally sold by Broadway on January \(1,20 \times 3\), to Lemon Corporation. Interest is paid

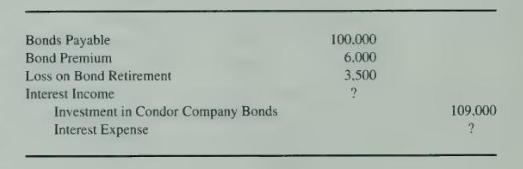

Ballard Corporation purchased 70 percent of the voting shares of Condor Company on January 1, 20X4, at underlying book value. It also purchased \(\$ 100,000\) par value, 12 percent Condor Company bonds on that date. The bonds had been issued on January 1, 20X1, with a 10 -year maturity.During

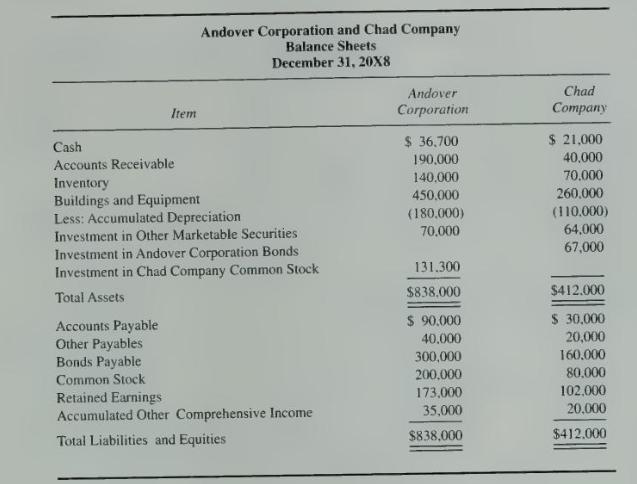

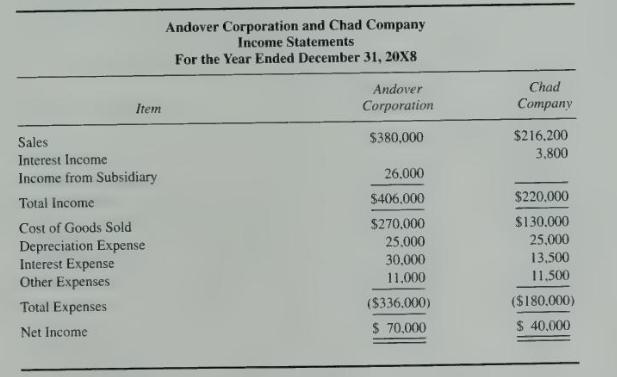

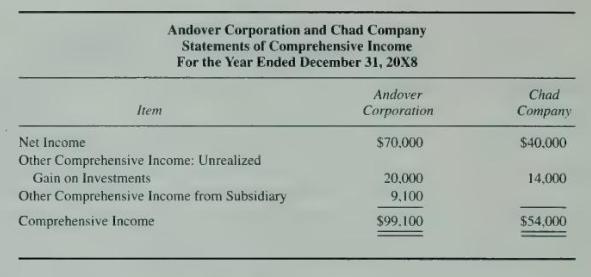

Andover Corporation acquired 65 percent of the ownership of Chad Company on January 1, 20X6, at underlying book value. Financial statements for the two companies at December 31, 20X8, are as follows:Andover and Chad paid dividends of \(\$ 45,000\) and \(\$ 28,000\), respectively, in \(20 \times

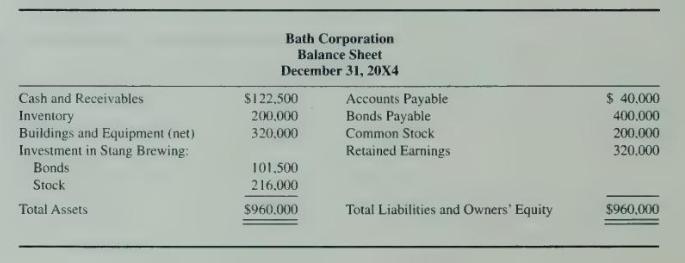

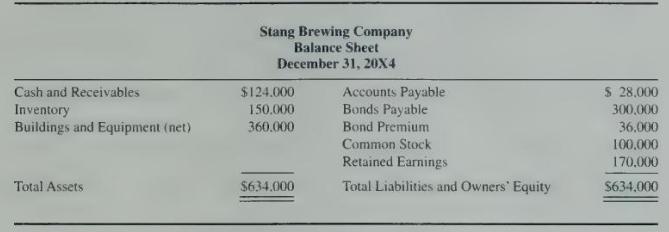

Bath Corporation purchased 80 percent of the stock of Stang Brewing Company on January 1, 20X1, at underlying book value. On that date, Stang Brewing Company issued \(\$ 300,000\) par value, 8 percent. 10 -year bonds to Sidney Malt Company. Bath Corporation subsequently purchased \(\$ 100,000\) of

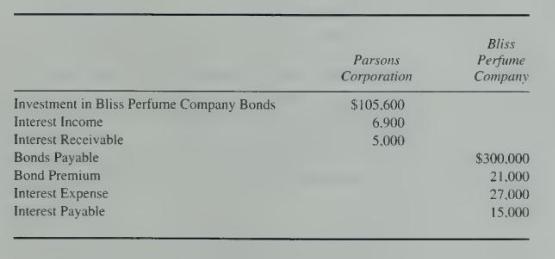

Bliss Perfume Company issued \(\$ 300,000\) of 10 percent bonds on January 1, 20X2, at 110. The bonds mature 10 years from issue and have semiannual interest payments on January 1 and July 1. Parsons Corporation owns 80 percent of the stock of Bliss Perfume Company. On April 1, 20X4, Parsons

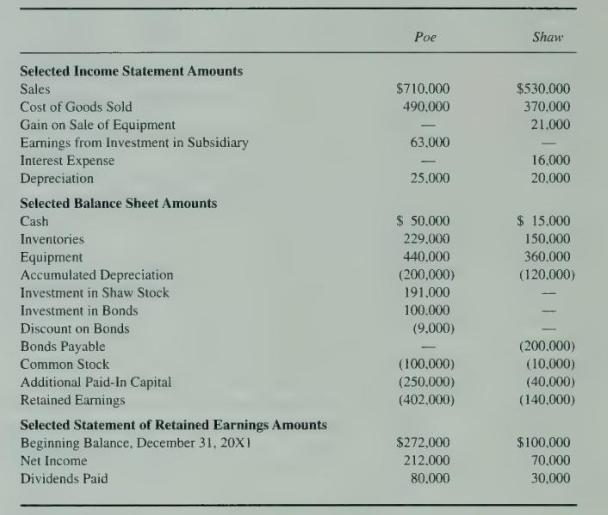

Presented below are selected amounts from the separate unconsolidated financial statements of Poe Corporation and its 90 percent owned subsidiary, Shaw Company, at December 31, 20X2.Additional information follows:1. On January 2, 20X2, Poe Corporation purchased 90 percent of Shaw Company's

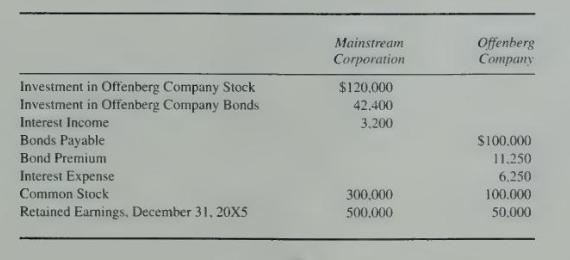

Mainstream Corporation holds 80 percent of the voting shares of Offenberg Company, acquired on January 1, 20X1, at underlying book value. On January 1, 20X4, Mainstream purchased Offenberg Company bonds with a par value of \(\$ 40,000\). The bonds pay 10 percent interest annually on December 31 and

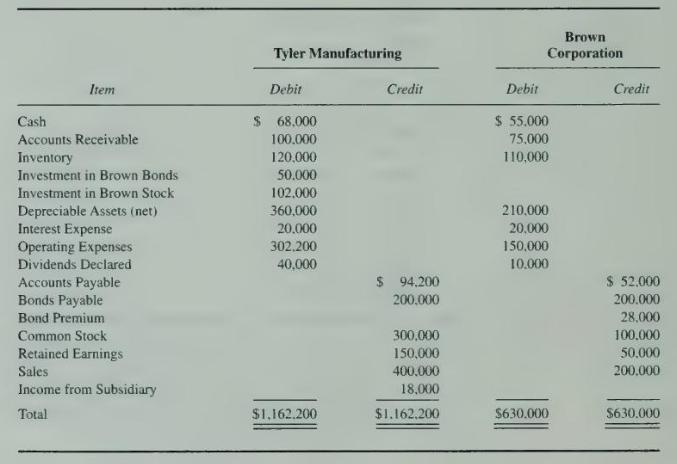

Tyler Manufacturing purchased 60 percent of the ownership of Brown Corporation stock on January 1, 20X1, at underlying book value. Tyler also purchased \(\$ 50,000\) of Brown Corporation bonds at par value on December 31, 20X3. The bonds were sold by Brown Corporation on January 1,20X1, at 120 and

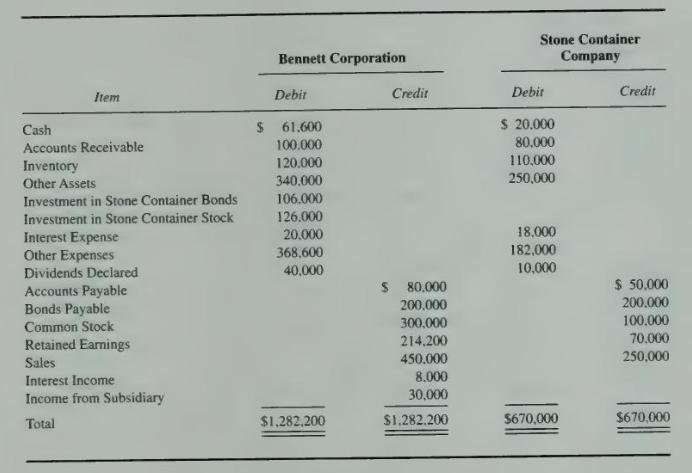

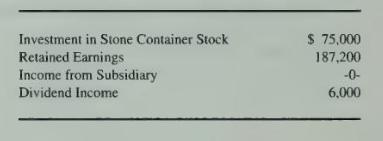

Bennett Corporation owns 60 percent of the stock of Stone Container Company, which it acquired at book value in 20X1. On December 31, 20X3, Bennett Corporation purchased \(\$ 100,000\) par value bonds of Stone Container. The bonds originally were issued by Stone Container Company at par value. The

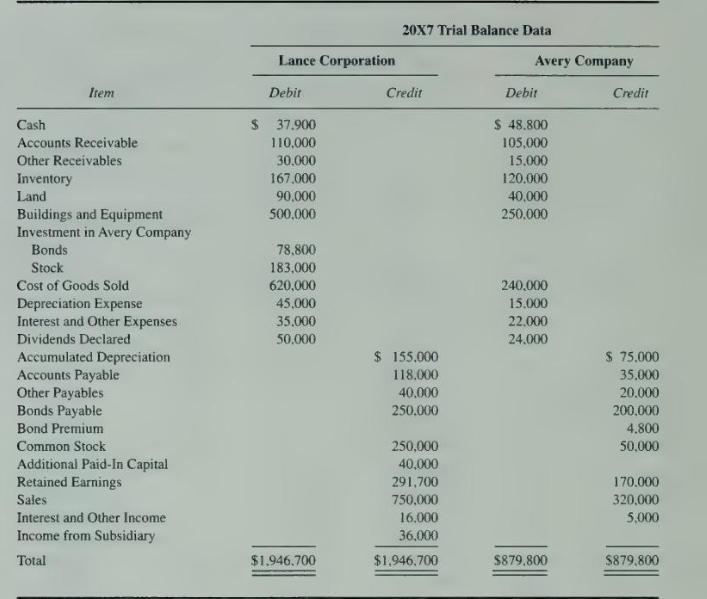

Lance Corporation purchased 75 percent of the common stock of Avery Company at underlying book value on January 1, 20X3. Trial balances for Lance Corporation and Avery Company on December \(31,20 \times 7\), are as follows:During 20X7, Lance Corporation resold inventory purchased from Avery in

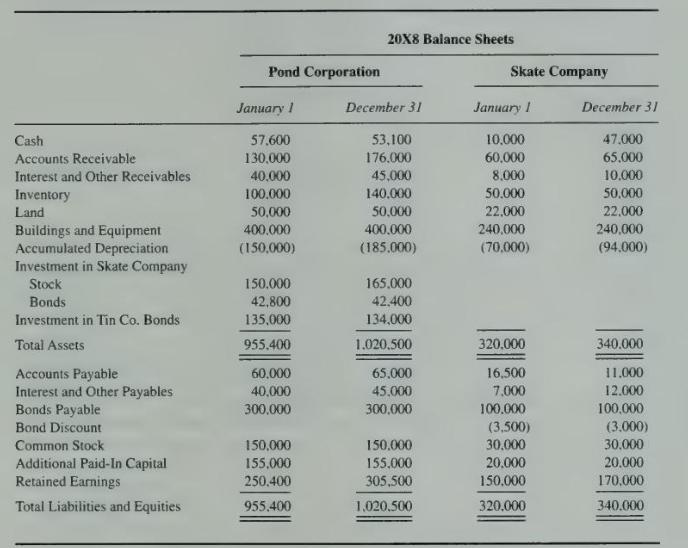

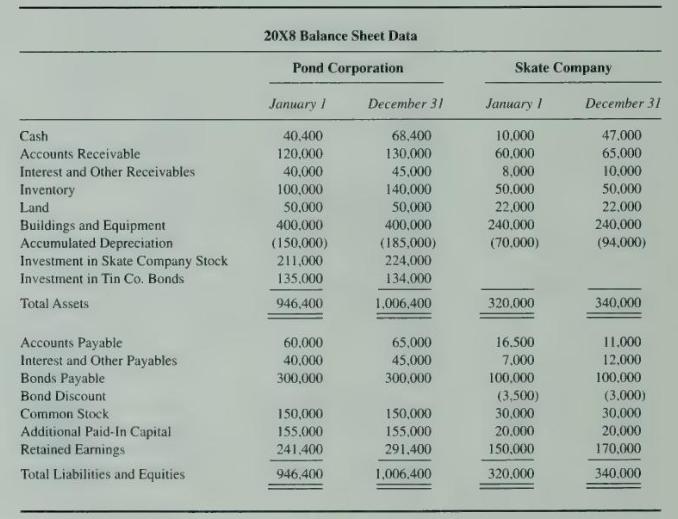

On January 1, 20X5, Pond Corporation purchased 75 percent of the stock of Skate Company at underlying book value. The balance sheets for Pond and Skate at January 1, 20X8, and December 31, 20X8, and income statements for \(20 \mathrm{X} 8\) were reported as follows:1. Pond Corporation sold a

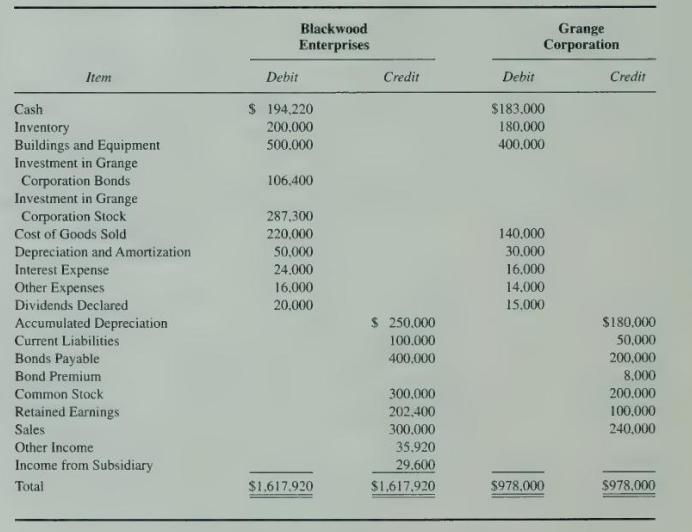

Blackwood Enterprises owns 80 percent of the voting stock of Grange Corporation. Blackwood purchased the shares on January \(1,20 \mathrm{X} 4\), for \(\$ 234,500\), at which time Grange reported common stock outstanding of \(\$ 200,000\) and retained earnings of \(\$ 50,000\). The book values of

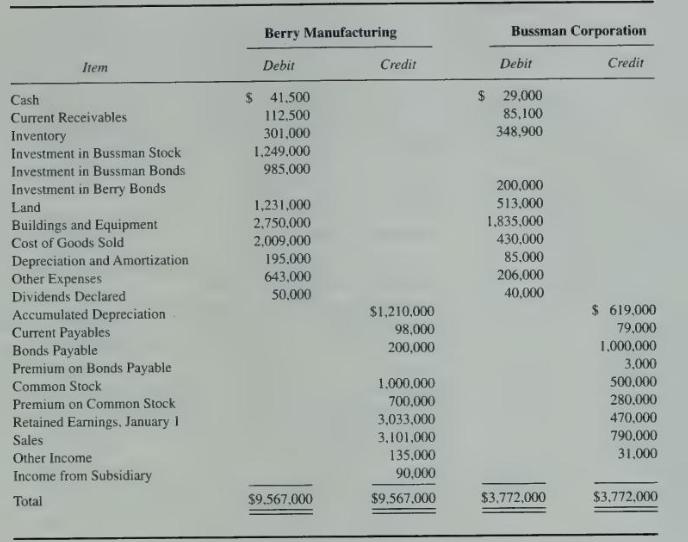

Berry Manufacturing Company purchased 90 percent of the outstanding common stock of Bussman Corporation on December 31, 20X5, for \(\$ 1,150,000\). On that date, Bussman reported common stock of \(\$ 500,000\), premium on common stock of \(\$ 280,000\), and retained earnings of \(\$ 420,000\). The

Johnson Company owns 75 percent of the voting shares of Hall Leasing Corporation. On January 1. 20X3, Hall Leasing Corporation purchased a fleet of small delivery trucks with an expected economic life of six years and no anticipated residual value. Hall Leasing Corporation leased the trucks to

On December 31, 20X4, Bennett Corporation recorded the following entry on its books to adjust its investment in Stone Container Company stock from the basic equity method to the fully adjusted equity method:\section*{Required}a. Adjust the data reported by Bennett Corporation in the trial balance

The trial balance data presented in Problem 8-28 can be converted to reflect use of the cost method by inserting the following amounts in place of those presented for Bennett Corporation:Stone Container Company reported retained earnings of \(\$ 25,000\) on the date Bennett Corporation purchased 60

A parent company sells common shares of one of its subsidiaries to a nonaffiliate for more than their carrying value on the parent's books. How should the sale be reported by the parent company? How should the sale be reported in the consolidated tinancial statements?

A subsidiary sells additional shares of its common stock to a nonaffiliate at a price that is greater than the previous book value per share. How does the sale benefit the existing shareholders?

A parent company purchases additional common shares of one of its subsidiaries from a nonaffiliate at \(\$ 10\) per share above underlying book value. Explain how this purchase is reflected in the consolidated financial statements for the year.

How does the entity method differ from the treasury stock method in computing consolidated net income when there is reciprocal ownership between the parent and the subsidiary?

Parent Company holds 80 percent ownership of Subsidiary Company, and Subsidiary Company owns 90 percent of the stock of Tiny Corporation. What effect will \(\$ 100,000\) of unrealized intercompany profits on the books of Tiny Corporation on December 31, 20X5, have on the amount of consolidated net

Snapper Corporation holds 70 percent ownership of Bit Company, and Bit Company holds 60 percent ownership of Slide Company. Should Slide Company be consolidated with Snapper Corporation? Why?

When there are multilevel affiliations, explain why it generally is best to prepare consolidated financial statements by completing the eliminating entries for companies furthest from parent company ownership first and completing the eliminating entries for those owned directly by the parent

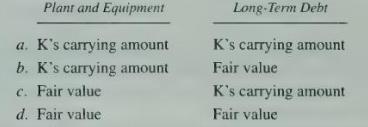

Snow Corporation issued common stock with a par value of \(\$ 100,000\) and preferred stock with a par value of \(\$ 80,000\) on January 1, 20X5, when the company was created. Klammer Corporation acquired a controlling interest in Snow Corporation on January 1, 20X6.\section*{Required}What does the

Hardcore Mining Company acquired 88 percent of the common stock of Mountain Trucking Company on January 1. 20X2, at a cost of \(\$ 30\) per share. On December 31, 20X7, when the book value of Mountain Trucking stock was \(\$ 70\) per share. Hardcore sold one-quarter of its investment in Mountain

Strong Manufacturing Company holds 94 percent ownership of Thorson Farm Products and 68 percent ownership of Kenwood Distributors. Thorson Farm Products has excess cash at the end of 20X4 and is considering buying shares of its own stock, shares of Strong Manufacturing, or shares of Kenwood

How do unrealized intercompany profits on a downstream sale of inventory made during the current period affect the computation of consolidated net income?

How do unrealized intercompany profits on an upstream sale of inventory made during the current period affect the computation of consolidated net income?

What is the basic eliminating entry needed when inventory is sold to an affiliate at a profit and is resold to an unaffiliated party before the end of the period, if perpetual inventory systems are used by both affiliates?

What is the basic eliminating entry needed when inventory is sold to an affiliate at a profit and is not resold before the end of the period, if perpetual inventory systems are used by both affiliates?

How do unrealized intercompany inventory profits from a prior period affect the computation of consolidated net income when the inventory is resold in the current period? Is it important to know if the sale was upstream or downstream? Why, or why not?

\(5^{\circ}\) Is an inventory sale from one subsidiary to another treated in the same manner as an upstream sale or a downstream sale? Why?

* Par Company regularly purchased inventory from Eagle Company. Recently, Par Company purchased a majority of the voting shares of Eagle Company. How should it treat inventory profits recorded by Eagle Company before the day of acquisition? Following the day of acquisition?

A What are the basic eliminating entries needed when inventory is sold to an affiliate at a profit and is not resold before the end of the period if periodic inventory systems are used by both affiliates?

A What is the basic eliminating entry needed when inventory is sold to an affiliate at a profit and is resold to an unaffiliated party before the end of the period if periodic inventory systems are used by both affiliates?

A What is the basic eliminating entry needed under a periodic inventory system when intercompany inventory profits that are unrealized at the beginning of the period are realized during the year?

Shortcut Charlie usually manages to develop some simple rule to handle even the most complex situations. In providing for the elimination of the effects of inventory transfers between the parent company and a subsidiary or between subsidiaries, Shortcut started with the following rules:1. When the

Morrison Company owns 80 percent of the stock of Bloom Corporation. The companies frequently engage in intercompany inventory transactions.\section*{Required}Name the conditions that would make it possible for each of the following statements to be true. Treat each statement independently.a. Income

Rockness Corporation purchases much of its inventory from its 90 percent owned subsidiary, Mauch Company. Mauch prices its sales to Rockness to earn a 40 percent gross profit on the sales. During 20X4, Rockness purchases \(\$ 400,000\) of inventory from Mauch and resells all of the inventory to

Ready Building Products has six subsidiaries that sell building materials and supplies to the public and to the parent and other subsidiaries. Because of the invoicing system used by Ready Building Products, it is not possible to keep track of which items have been purchased from related companies

Water Company owns 80 percent of the outstanding common stock of Fire Company. On December 31, 20X9, Fire sold equipment to Water at a price in excess of Fire's carrying amount, but less than its original cost. On a consolidated balance sheet at December 31, 20X9, the carrying amount of the

Select the correct answer for each of the following questions.1. Upper Company holds 60 percent of the voting shares of Lower Company. During the preparation of consolidated financial statements for \(20 \mathrm{X} 5\), the following eliminating entry was made:Which of the following statements is

Huckster Corporation purchased land on January 1, 20X1, for \(\$ 20,000\). On June 10, 20X4, Huckster sold the land to its subsidiary, Lowly Corporation, for \(\$ 30,000\). Huckster Corporation owns 60 percent of the voting shares of Lowly Corporation.\section*{Required}a. Give the workpaper

Sparkle Corporation holds 70 percent ownership of Playtime Enterprises. On December 31, 20X6, Playtime paid Sparkle \(\$ 40,000\) for a truck that had been purchased by Sparkle for \(\$ 45,000\) on January 1, 20X2. The truck was considered to have a 15-year life from January 1, 20X2, and no

Sparkle Corporation holds 70 percent ownership of Playtime Enterprises. On December 31, 20X6, Playtime paid Sparkle \(\$ 40,000\) for a truck that had been purchased by Sparkle for \(\$ 45,000\) on January 1, 20X2. The truck was considered to have a 15-year life from January 1, 20X2, and no

Frazer Corporation purchased 60 percent of the voting common stock of Minnow Corporation on January 1, 20X1, at underlying book value. On December 31, 20X5, Frazer received \(\$ 210,000\) from Minnow for a truck Frazer purchased on January 1, 20X2, for \(\$ 300,000\). The truck is expected to have

Frazer Corporation purchased 60 percent of the voting common stock of Minnow Corporation on January 1, 20X1, at underlying book value. On January 1, 20X5, Frazer received \(\$ 245,000\) from Minnow for a truck Frazer purchased on January 1, 20X2, for \(\$ 300,000\). The truck is expected to have a

On January 1, 20X7, Wainwrite Corporation sold to Lance Corporation equipment it had purchased for \(\$ 150,000\) and used for eight years. Wainwrite recorded a gain of \(\$ 14,000\) on the sale. The equipment has a total useful life of 15 years and is depreciated on a straight-line basis.

Baywatch Industries purchased 80 percent ownership of Tubberware Corporation on January 1, 20X0, at underlying book value. On January 1, 20X6, Baywatch paid \(\$ 270,000\) to Tubberware to acquire equipment that Tubberware had purchased on January 1, 20X3, for \(\$ 300,000\). The equipment is

Albion Corporation holds 90 percent ownership of Andrews Company. On July 1, 20X3, Albion Corporation sold equipment that it had purchased for \(\$ 30,000\) on January 1, 20 X1, to Andrews Company for \(\$ 28.000\). The original six-year estimated total economic life of the equipment remains

Verry Corporation owns 75 percent of the voting common stock of Spawn Corporation. Verry Corporation reported income from its separate operations of \(\$ 90,000\) and \(\$ 110,000\) in \(20 \mathrm{X} 4\) and 20X5, respectively. Spawn Corporation reported net income of \(\$ 60,000\) and \(\$

Speedy Delivery Service purchased at book value 80 percent of the voting shares of Acme Real Estate Company. On January 1, 20X3, the date of purchase, Acme Real Estate reported common stock of \(\$ 300,000\) and retained earnings of \(\$ 100,000\). During 20X3 Speedy Delivery provided courier

Turner Company purchased 70 percent of the stock of Split Company approximately 20 years ago. On December 31, 20X8, Turner purchased a building from Split for \(\$ 300,000\). Split purchased the building on January 1, 20X1, at a cost of \(\$ 400,000\) and used straight-line depreciation on an

Parent Company holds 90 percent of the voting common shares of Sunway Company. On December 31, 20X8. Parent Company recorded a loss of \(\$ 16,000\) on the sale of equipment to Sunway Company. At the time of the sale, the estimated remaining economic life of the equipment was eight

Brown Corporation holds 70 percent of the voting common stock of Transom Company. On January 1, 20X2. Transom paid \(\$ 300,000\) to acquire a building with an expected economic life of 15 years. Transom uses straight-line depreciation for all depreciable assets. On December 31, 20X7, Brown

Swanson Corporation purchased land from Clayton Corporation for \(\$ 240.000\) on December 20 . 20X3. This purchase followed a series of transactions between subsidiaries controlled by Swanson. On February 7, 20X3, Sullivan Company purchased the land from a nonaffiliate for \(\$ 145,000\). Sullivan

Blank Corporation owns 60 percent of the voting common stock of Grand Corporation. On December 31, 20X4, Blank paid Grand \(\$ 276,000\) for dump trucks purchased by Grand on January \(1,20 \times 2\). Both companies use straight-line depreciation. The eliminating entry included in preparing

Stern Manufacturing purchased an ultrasound drilling machine with a remaining economic life of 10 years from a 70 percent owned subsidiary for \(\$ 360,000\) on January 1, 20X6. Both companies use straight-line depreciation. The subsidiary recorded the following entry when it sold the machine to

Pastel Corporation acquired controlling interest of Somber Corporation in 20X5 at underlying book value. In preparing a consolidated balance sheet workpaper at January 1, 20X9, the controller of Pastel Corporation included the following eliminating entry:In a note at the bottom of the consolidation

Norgaard Corporation is provided with management consulting services by its 75 percent owned subsidiary. Bline Inc. During 20X3, Bline billed Norgaard \(\$ 123,200\) for the services provided. For the year 20X4. Bline billed Norgaard \(\$ 138,700\) for such services and collected all but \(\$

Newtime Products purchased 65 percent of TV Sales Company's stock at underlying book value on January 1, 20X3. At that time, TV Sales reported shares outstanding of \(\$ 300,000\) and retained earnings of \(\$ 100,000\). During 20X3, TV Sales reported net income of \(\$ 50,000\) and paid dividends

United Grain Company is 90 percent owned by Petime Corporation. Petime Corporation paid \(\$ 9.000\) in excess of underlying book value to purchase the shares of United Grain Company and is amortizing the balance over a 10 -year period. During 20X4. United Grain Company sold land to 1 Petime

Lander Corporation purchased 75 percent of the voting common shares of Toll Corporation for \(\$ 350,000\) on January 1,20X4, when Toll reported common stock outstanding of \(\$ 150,000\) and retained earnings of \(\$ 270,000\). The purchase differential is amortized over 10 years. On December

Forest Corporation purchased 70 percent of the voting common stock of Part Company on January \(1,20 \mathrm{X} 2\), for \(\$ 294,000\). At the time, Part Company reported common stock outstanding of \(\$ 150,000\) and retained earnings of \(\$ 220,000\). The excess paid over underlying book value

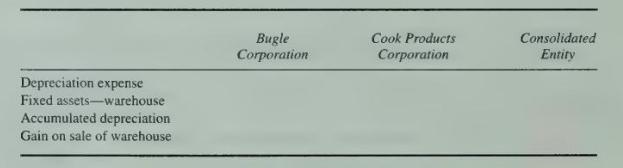

A total of 70 percent of Bugle Corporation and 80 percent of Cook Products Corporation stock is held by Smelts Company. Bugle Corporation purchased a warehouse with an expected life of 20 years on January 1, 20X1, for \(\$ 40,000\). On January 1, 20X6, Bugle Corporation sold the warehouse to Cook

In preparing its consolidated financial statements at December \(31,20 \times 7\), the following eliminating entry was included in the consolidation workpaper of Master Corporation:Master Corporation owns 60 percent of the voting common stock of Rakel Corporation. On January 1, 20X7, Rakel sold a

Select the correct answer for each of the following questions.1. In the preparation of a consolidated income statement:a. Income assigned to noncontrolling shareholders always is computed as a pro rata portion of the reported net income of the consolidated entity.\(b\). Income assigned to

In its 20X7 consolidated income statement, Skekel Development Company reported consolidated net income of \(\$ 921,000\) and \(\$ 45,000\) of income assigned to the 30 percent noncontrolling interest in its only subsidiary, Subsidence Mining, Inc. During the year, Subsidence had sold a previously

Great Company purchased 80 percent of the common stock of Meager Corporation on January 1, \(20 \mathrm{X} 4\), for \(\$ 280,000\). The corporate controller of Great Company has lost the consolidation files for the past three years and has asked you to compute the proper retained earnings balances

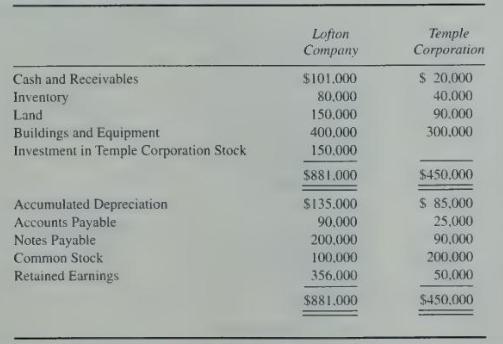

Lofton Company owns 60 percent of the voting shares of Temple Corporation, purchased on May 17. 20X1, at underlying book value. The permanent accounts of the companies on December 31, 20X6, contained the following balances:On January 1, 20X2, Lofton Company paid \(\$ 100,000\) for equipment with an

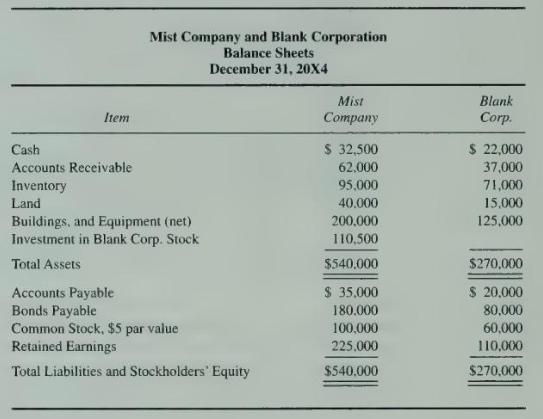

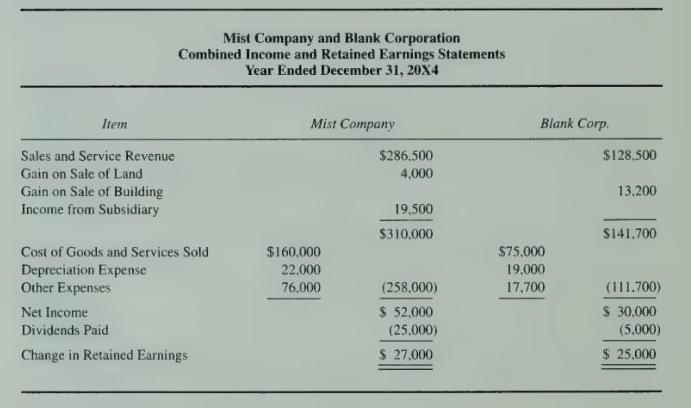

Mist Company purchased 65 percent of the voting common stock of Blank Corporation on June 20, 20X2, at underlying book value. The balance sheets and income statements for the companies at December \(31,20 \times 4\), are as follows:1. Mist Company uses the basic equity method in accounting for its

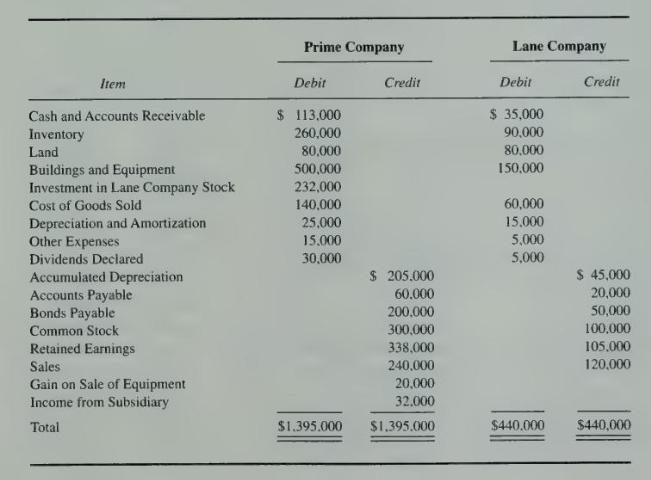

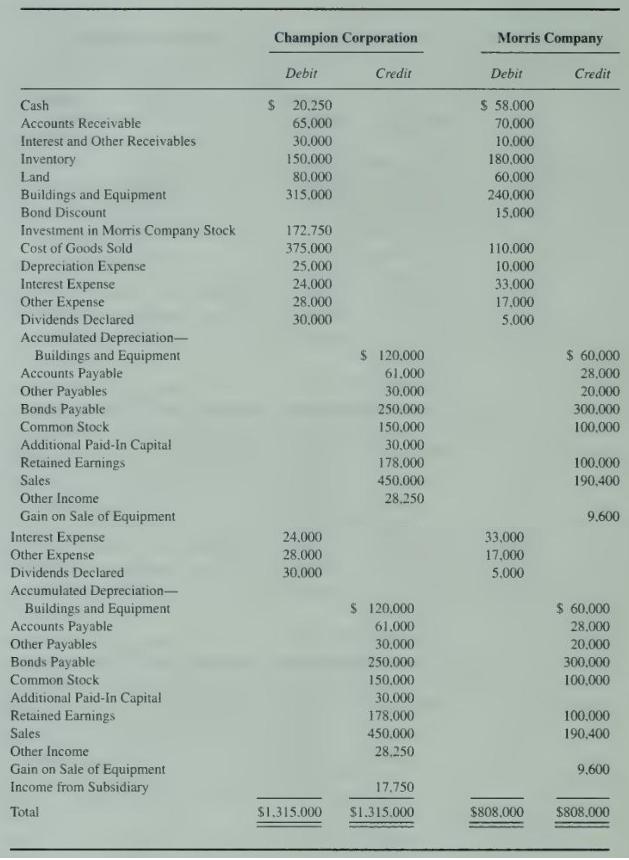

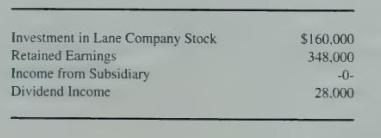

Prime Company holds 80 percent of the stock of Lane Company, acquired on January 1, 20X2, for \(\$ 160,000\). On the date of acquisition, Lane reported retained earnings of \(\$ 50,000\) and had \(\$ 100,000\) of common stock outstanding. Prime uses the basic equity method in accounting for its

On January 1, 20X5, Pond Corporation purchased 80 percent of the stock of Skate Company by issuing common stock with a fair value of \(\$ 180,000\). At that date, Skate reported retained earnings of \(\$ 100,000\). The balance sheets for Pond and Skate at January 1, 20X8, and December 31, 20X8, and

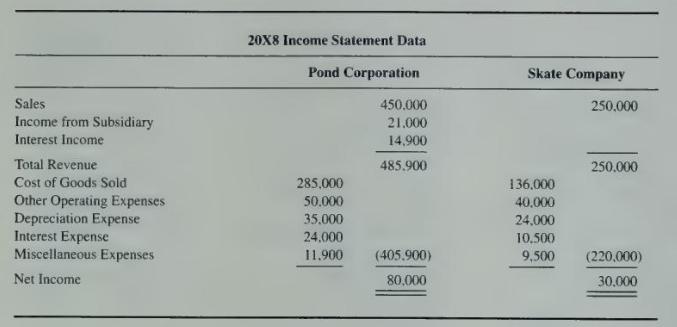

Champion Corporation purchased 70 percent of the voting common stock of Morris Company for \(\$ 154,500\) on January 1, 20X3, when Morris reported common stock outstanding of \(\$ 100,000\) and retained earnings of \(\$ 85,000\). At that date Morris held buildings and equipment with a fair value

Prime Company holds 80 percent of the stock of Lane Company, acquired on January 1, 20X2, for \(\$ 160,000\). On the date of acquisition, Lane reported retained earnings of \(\$ 50,000\) and \(\$ 100,000\) of common stock outstanding. Prime uses the basic equity method in accounting for its

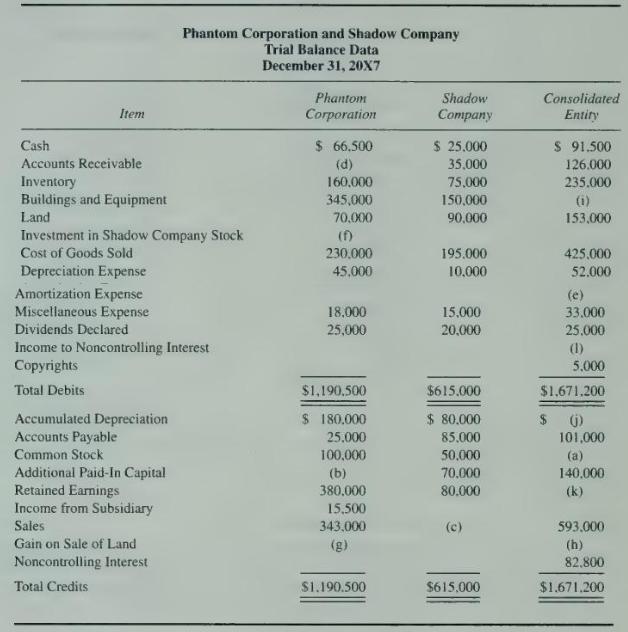

Partial trial balance data for Phantom Corporation and Shadow Company at December 31, 20X7. are as follows:1. Phantom Corporation purchased 60 percent ownership of Shadow Company on January \(1,20 \times 4\), for \(\$ 105.000\). Shadow reported retained earnings of \(\$ 30,000\) on January 1, 20X4.

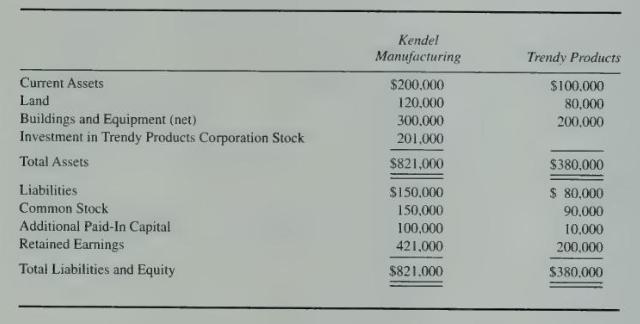

Kendel Manufacturing Corporation purchased 60 percent of the outstanding stock of Trendy Products Corporation on January 1, 20X2. Trendy reported retained earnings of \(\$ 120,000\) at the date of acquisition. The price paid for Trendy's stock included \(\$ 30,000\) that was attributable to

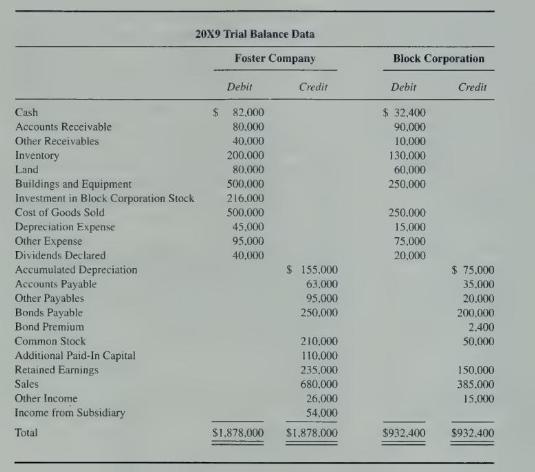

Block Corporation was created on January 1, 20X0, to develop computer software. On January 1, 20X5, Foster Company purchased 90 percent of the common stock of Block Corporation at underlying book value. Trial balances for Foster Company and Block Corporation on December 31, 20X9, are as follows:On

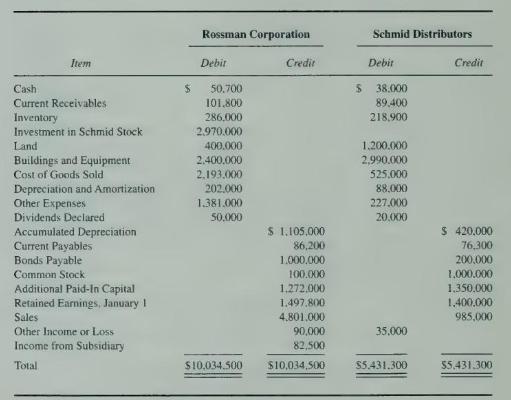

Rossman Corporation holds 75 percent of the common stock of Schmid Distributors Inc. The stock originally was purchased on December \(31,20 \mathrm{X} 1\), for \(\$ 2,340,000\). At the date of acquisition, Schmid reported common stock with a par value of \(\$ 1,000,000\), additional paid-in capital

On December 31, 20X7, Prime Company recorded the following entry on its books to adjust its investment in Lane Company from the basic equity method to the fully adjusted equity method:\section*{Required}a. Adjust the data reported by Prime Company in the trial balance contained in Problem 6-35 for

The trial balance data presented in Problem 6-35 can be converted to reflect use of the cost method by inserting the following amounts in place of those presented for Prime Company:\section*{Required}a. Prepare the journal entries that would have been recorded on the books of Prime Company during

When are profits on intercorporate sales considered to be realized?

How are unrealized profits on current-period intercorporate sales treated in preparing the income statement for \((a)\) the selling company and \((b)\) the consolidated entity?

How are unrealized profits treated in the consolidated income statement if the intercorporate sale occurred in a prior period and the transferred item is sold to a nonaffiliate in the current period?

How are unrealized intercorporate profits treated in the consolidated statements if the intercorporate sale occurred in a prior period and the profits have not been realized by the end of the current period?

What portion of the unrealized intercorporate profit is eliminated in a downstream sale? In an upstream sale?

How is the effect of unrealized intercorporate profits on consolidated net income different between an upstream and a downstream sale?

A subsidiary sold a depreciable asset to the parent company at a profit in the current period. Will the income assigned to the noncontrolling interest in the consolidated income statement for the current period be greater than, less than, or equal to a proportionate share of the reported net income

A subsidiary sold a depreciable asset to the parent company at a profit of \(\$ 1,000\) in the current period. Will the income assigned to the noncontrolling interest in the consolidated income statement for the current period be larger if the intercorporate sale occurs on January 1 or on December

A A parent company may use on its books one of several different methods of accounting for its ownership of a subsidiary: (a) cost method, (b) basic equity method, or (c) fully adjusted equity method. How will the choice of method affect the reported balance in the investment account when there are

The consolidation process is intended to adjust the reported amounts of items transferred between related companies back to their original acquisition costs. Such procedures are appropriate so long as original acquisition cost is the primary basis of asset valuation.\section*{Required}How might the

The elimination process used in consolidation is intended to remove all unrealized intercorporate profits from the various asset categories.\section*{Required}a. How might companies determine if there are unrealized intercorporate profits at year-end?\(b\). What problems occur if unrealized

Showing 500 - 600

of 2939

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers