New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

advanced financial accounting

Advanced Financial Accounting 5th Edition Richard E. Baker, Valdean C. Lembke, Thomas E. King - Solutions

Current reporting standards require the consolidated entity to include all the revenue, expenses, assets, and liabilities of the parent and its subsidiaries in the consolidated financial statements. In those cases where the parent does not own all of a subsidiary's shares, various rules and

Companies have many different practices for pricing transfers of goods and services from one affiliate to another. Regardless of the approaches used for internal decision making and performance evaluation, or for tax purposes, all intercompany profits, unless immaterial, are supposed to be

Select the correct answer for each of the following questions.1. A 70 percent owned subsidiary company declares and pays a cash dividend. What effect does the dividend have on the retained earnings and minority interest balances in the parent company's consolidated balance sheet?a. No effect on

Select the correct answer for each of the following questions.1. On January 1, 20X5, Post Company purchased an 80 percent investment in Stake Company. The acquisition cost was equal to Post's equity in Stake's net assets at that date. On January 1, 20X5, Post and Stake had retained earnings of \(\$

Trim Corporation purchased 100 percent of the voting common stock of Round Corporation on January 1, 20X2, for \(\$ 400,000\). At that date, Round reported the following summarized balance sheet data:Round Corporation reported net income of \(\$ 80,000\) for \(20 \mathrm{X} 2\) and paid dividends

Trim Corporation purchased 75 percent of the voting common stock of Round Corporation on January 1, 20X2, for \(\$ 300,000\). At that date, Round reported the following summarized balance sheet data:Round Corporation reported net income of \(\$ 80,000\) for \(20 \mathrm{X} 2\) and paid dividends of

Amber Corporation reported the following summarized balance sheet data on December 31, 20X6:On January 1, 20X7, Purple Company purchased 100 percent of the stock of Amber Corporation for \(\$ 500,000\). Amber Corporation reported net income of \(\$ 50,000\) for \(20 \mathrm{X} 7\) and paid

Farmstead Company reported the following summarized balance sheet data on December 31, 20X8:On January I, 20X9, Horrigan Corporation purchased 70 percent of the stock of Farmstead Company for \(\$ 210,000\). Farmstead Company reported net income of \(\$ 20,000\) for \(20 \mathrm{X} 9\) and paid

Canton Corporation is a wholly owned subsidiary of Winston Corporation. Winston acquired ownership of Canton on January 1, 20X3, for \(\$ 28,000\) above the reported net assets of Canton. At that date, Canton reported common stock outstanding of \(\$ 60,000\) and retained earnings of \(\$ 90,000\).

Canton Corporation is a majority-owned subsidiary of Winston Corporation. Winston acquired 75 percent ownership of Canton on January 1,20X3, for \(\$ 133,500\). At that date, Canton reported common stock outstanding of \(\$ 60,000\) and retained earnings of \(\$ 90,000\). The purchase differential

Short Company acquired 75 percent of the common stock of Justice Enterprises on January 1. 20X6, and paid \(\$ 30,000\) more than book value. The entire amount is assigned to equipment with an economic life of 10 years on the date of acquisition. Short accounts for its investment in Justice using

Franklin Corporation acquired 90 percent of the voting common stock of Lancaster Company on January 1, 20X1, for \(\$ 486,000\). At the time of the combination, Lancaster reported common stock outstanding of \(\$ 120,000\) and retained earnings of \(\$ 380,000\). The book value of Lancaster's net

Franklin Corporation acquired 90 percent of the voting common stock of Lancaster Company on January 1, 20X1, for \(\$ 486,000\). At the time of the combination. Lancaster reported common stock outstanding of \(\$ 120,000\) and retained earnings of \(\$ 380.000\). The book value of Lancaster's net

Franklin Corporation acquired 90 percent of the voting common stock of Lancaster Company on January 1, 20X1, for \(\$ 486,000\). At the time of the combination. Lancaster reported common stock outstanding of \(\$ 120,000\) and retained earnings of \(\$ 380.000\). The book value of Lancaster's net

Blithe Company purchased 60 percent of the stock of Spirit Company for \(\$ 100,000\) on January 1, 20X6, when Spirit reported \(\$ 120,000\) of common stock outstanding and retained earnings of \(\$ 25,000\). On December 31, 20X8. Blithe reported its investment in Spirit at \(\$ 126,100\) using

Jersey Company purchased 80 percent of the common stock of Briar Company at the beginning of the current year. On the date of acquisition, Briar Company reported common stock outstanding of \(\$ 80,000\) and retained earnings of \(\$ 140.000\), and Jersey reported common stock outstanding of \(\$

Boxwell Corporation purchased 60 percent of the ownership of Conway Company on January 1, \(20 X 7\), for \(\$ 277,500\). Conway reported the following net income and dividend payments:On January 1. 20X7. Conway had \(\$ 250,000\) of \(\$ 5\) par value common stock outstanding and retained earnings

Asp Corporation holds 60 percent ownership of Parry Company, which it acquired on January 1, 20X1. Asp Corporation paid \(\$ 226,000\) for its ownership of Parry. At acquisition, Parry had retained earnings of \(\$ 50,000\) and \(\$ 200,000\) of stock outstanding. Book values approximated market

Farrow Corporation acquired 70 percent of the stock of Rand Company on January 1, 20X7, for \(\$ 300,000\). Other relevant data are as follows:The excess of purchase price over book value was assigned to depreciable assets with a remaining economic life of five years.\section*{Required}Select the

Blake Corporation acquired 100 percent of the voting shares of Shaw Corporation on January 1, 20X3, at underlying book value. Blake uses the equity method in accounting for its investment in Shaw Corporation. Adjusted trial balances for Blake Corporation and Shaw Corporation on December \(31,20

Blake Corporation acquired 100 percent of the voting shares of Shaw Corporation on January 1, \(20 \mathrm{X} 3\), at underlying book value. Blake uses the equity method in accounting for its investment in Shaw Corporation. Adjusted trial balances for Blake Corporation and Shaw Corporation on

Kennelly Corporation purchased all the common shares of Short Company on January 1, 20X5, for \(\$ 180,000\). On that date, the book value of the net assets reported by Short Company was \(\$ 150,000\). The entire purchase differential was assigned to depreciable assets with a six-year remaining

Proud Corporation purchased 80 percent of the voting stock of Stergis Company on January 1, 20X3, at underlying book value. Proud Corporation uses the equity method in accounting for its ownership of Stergis during 20X3. On December 31, 20X3, the trial balances of the two companies are as

Proud Corporation purchased 80 percent of the voting stock of Stergis Company on January 1, 20X3, at underlying book value. Proud Corporation uses the equity method in accounting for its ownership of Stergis. On December 31, 20X4, the trial balances of the two companies are as

Tollway Corporation purchased 75 percent of the common stock of Stem Corporation on January 1, 20X8, for \(\$ 435,000\). At that date, Stem reported common stock outstanding of \(\$ 300,000\) and retained earnings of \(\$ 200,000\). The purchase differential is assigned to other intangible assets

Palmer Corporation purchased 70 percent of the ownership of Krown Corporation on January 1, 20X8, for \(\$ 140,000\). At that date Krown reported capital stock outstanding of \(\$ 120,000\) and retained earnings of \(\$ 80,000\). During 20X8, Krown reported net income of \(\$ 30,000\),

On December 31, 20X4, Holly Corporation purchased 90 percent of the common stock of Brinker Inc. for \(\$ 888.000\), a price that was \(\$ 240.000\) in excess of the book value of the shares acquired. Of the \(\$ 240,000\) differential, \(\$ 5,000\) related to the increased value of Brinker's

City Touring Company holds 70 percent ownership of Country Playgrounds Inc. and uses the cost method in accounting for its investment. During 20X5, Country Playgrounds reported net income of \(\$ 70,000\) and paid dividends of \(\$ 40,000\). City Touring reported net income (including dividend

Cable Corporation purchased 70 percent of the ownership of Brush Company on January 1, 20X5, and paid \(\$ 220,000\). At that date. Brush Company reported the book value of its net assets as\(\$ 280,000\) and a remaining useful life of 10 years for those assets to which the purchase differential is

Blake Corporation purchased 100 percent of the voting shares of Shaw Corporation on January 1, 20X3, at underlying book value. Blake uses the cost method in accounting for its investment in Shaw Corporation. Shaw Corporation retained earnings, as shown in the 20X3 trial balance, was \(\$ 50,000\)

The trial balances for Blake Corporation and Shaw Corporation as of December 31, 20X4, are as follows:Blake purchased 100 percent ownership of Shaw Corporation on January 1, 20X3, at a cost of \(\$ 150,000\). Shaw reported \(\$ 50,000\) of retained eamings at acquisition. Blake uses the cost method

Lintner Corporation purchased 80 percent of the voting stock of Knight Company on January 1, 20X6, at underlying book value. Lintner uses the cost method in accounting for its investment in Knight Company. Knight reported \(\$ 50,000\) of retained earnings at the time of acquisition. Trial balance

The separate condensed balance sheets and income statements of Purl Corporation and its wholly owned subsidiary, Scott Corporation, are as follows:- On January 1, 20X0, Purl purchased for \(\$ 360,000\) all of Scott's \(\$ 10\) par, voting common stock. On January 1, 20X0, the fair value of Scott's

Penn Corporation acquired 75 percent of the voting common stock of Eastland Company on January \(1,20 \mathrm{X} 2\), for \(\$ 648,000\). The purchase differential was assigned to equipment with a remaining economic life of eight years at the date of acquisition. On that date, Eastland reported the

Bolt Corporation is 80 percent owned by Allied Foundries Inc. The shares of Bolt were acquired by Allied on January \(1,20 \mathrm{X} 2\), for \(\$ 160,000\). Selected stockholders' equity balances for the companies are as follows:Allied operates the subsidiary as an independent company and uses

Quill Corporation purchased 70 percent of the stock of North Company on January 1, 20X9, for \(\$ 105,000\). The following stockholders' equity balances were reported by the companies immediately after the acquisition:Quill and North reported 20X9 operating incomes of \(\$ 90,000\) and \(\$

Rise Corporation purchased 60 percent of the voting common stock of Doughboy Company on January 1, 20X7, for \(\$ 400,000\). At the date of acquisition, Doughboy reported common stock outstanding of \(\$ 240,000\) and retained earnings of \(\$ 310,000\). The purchase price included a differential

Power Corporation acquired 75 percent of the ownership of Best Company on January 1, 20X8, for \(\$ 96,000\). At that date, the fair value of Best's buildings and equipment was \(\$ 20,000\) greater than book value. Buildings and equipment are depreciated on a 10 -year basis. Although goodwill is

Power Corporation acquired 75 percent of the ownership of Best Company of January 1, 20X8, for \(\$ 96,000\). At that date, the fair value of Best's buildings and equipment was \(\$ 20,000\) greater than book value. Buildings and equipment are depreciated on a 10 -year basis. Although goodwill is

Terrier Corporation was created on January 1, 20X2, and quickly became successful. On January 1, 20X5, the owner sold 75 percent of the stock to Richards Company for \(\$ 12,000\) over book value. The differential was attributed to equipment that had a remaining economic life of eight years at the

Case Inc. acquired all the outstanding \(\$ 25\) par common stock of Frey Inc. on December 31, \(20 \times 3\), in exchange for 40,000 shares of its \(\$ 25\) par common stock. The business combination was considered to be a purchase transaction. Case's common stock closed at \(\$ 56.50\) per share

Thompson Company spent \(\$ 240.000\) to buy all the stock of Lake Corporation on January 1, \(20 \times 2\). The balance sheets of the two companies on December \(31,20 \times 3\), showed the following amounts:Lake Corporation reported retained earnings of \(\$ 100,000\) at the date of

Thompson Company spent \(\$ 240,000\) to buy all the stock of Lake Corporation on January 1, 20X2. On December 31,20X4, the trial balances of the two companies are as follows:Lake Corporation reported retained earnings of \(\$ 100,000\) at the date of acquisition. The difference between the

Pillar Corporation acquired 80 percent ownership of Stanley Wood Products Company on January 1. 20X1, for \(\$ 160,000\). On that date Stanley Wood Products reported retained eamings of \(\$ 50,000\) and had \(\$ 100,000\) of common stock outstanding. Pillar has used the equity method in accounting

Bigelow Corporation purchased 80 percent of Granite Company on January 1, 20X7, for \(\$ 173,000\). The trial balances for the two companies on December \(31,20 \times 7\), included the following amounts:1. On January \(1,20 \times 7\), Granite Company reported net assets with a book value of \(\$

Bigelow Corporation purchased 80 percent of Granite Corporation on January 1, 20X7, for \(\$ 173,000\). The trial balances for the two companies on December \(31,20 \mathrm{X} 8\), included the following amounts:1. On January 1, 20X7, Granite Company reported net assets with a book value of \(\$

Buckman Corporation and Eckel Mining Company reported the following balance sheet data as of December 31, 20X3:Buckman Corporation purchased controlling ownership of Eckel Mining Company on January 1, 20X3. Buckman Corporation uses the equity method in accounting for its ownership in Eckel Mining.

Amber Corporation acquired 60 percent ownership of Sparta Company on January 1, 20X8, at underlying book value. Trial balance data at December 31, 20X8, for Amber and Sparta are as follows:Sparta Company purchased stock of Row Company on January 1, 20X8, for \(\$ 30,000\) and classified the

Amber Corporation acquired 60 percent ownership of Sparta Company on January 1, 20X8, at underlying book value. Trial balance data at December 31, 20X9, for Amber and Sparta are as follows:Sparta Company purchased stock of Row Company on January 1, 20X8, for \(\$ 30.000\) and classified the

Trial balance data for Light Corporation and Star Company on December 31, 20X6, are as follows:Light Corporation purchased all the shares of Star Company on January 1, 20X5, for \(\$ 220,000\). The retained earnings balance of Star Company at the date of acquisition was \(\$ 50,000\). The full

Rapid Delivery Corporation was created on January 1, 20X2, and quickly became successful. On January 1, 20X6, the owner sold 80 percent of the stock to Samuelson Company at underlying book value. Samuelson has continued to operate the subsidiary as a separate legal entity and uses the cost method

Pillar Corporation acquired 80 percent ownership of Stanley Wood Products Company on January 1, 20X1, for \(\$ 160,000\). On that date Stanley Wood Products reported retained earnings of \(\$ 50,000\) and had \(\$ 100,000\) of common stock outstanding. Pillar has used the cost method in recording

On December 31, 20X6. Greenly Corporation and Lindy Company entered into a business combination in which Greenly acquired all the common stock of Lindy for \(\$ 935.000\). At the date of combination, Lindy had common stock outstanding with a par value of \(\$ 100.000\), additional paid-in capital

Select the most appropriate answer for each of the following questions.1. If A Company purchases 80 percent of the stock of B Company on January 1, 20X2, immediately after the acquisition:a. Consolidated retained earnings will be equal to the combined retained earnings of the two companies.b.

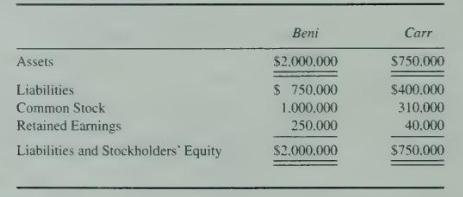

Select the correct answer for each of the following questions.1. Beni Corporation purchased 100 percent of Carr Corporation's outstanding capital stock for \(\$ 430,000\) cash. Immediately before the purchase, the balance sheets of both corporations reported the following:At the date of purchase,

On December 31, 20X3, Broadway Corporation reported common stock outstanding of \(\$ 200.000\). additional paid-in capital of \(\$ 300,000\), and retained earnings of \(\$ 100,000\). On January 1, 20X4, Johe Company acquired control of Broadway in a purchase-type business combination.a. Give the

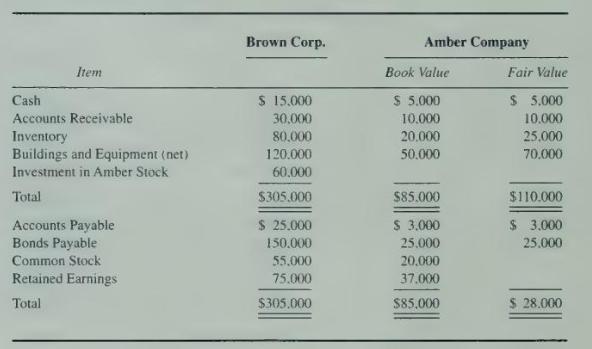

On June 10, 20X8, Brown Corporation purchased 60 percent of the common stock of Amber Company. Summarized balance sheet data for the two companies immediately after the stock purchase are as follows:\section*{Required}a. Give the eliminating entries required to prepare a consolidated balance sheet

Elder Corporation purchased 75 percent of the voting common stock of Dynamic Corporation on December 31, 20X4, for \(\$ 388,000\). At the date of combination, Dynamic reported the following:At December 31, 20X4, the book values of Dynamic's net assets and liabilities approximated their fair values,

Snow Corporation purchased all of the voting shares of Conger Corporation on January 1, 20X2. for \(\$ 365,000\). At that time Conger reported common stock outstanding of \(\$ 80,000\) and retained earnings of \(\$ 130,000\). The book values of Conger's assets and liabilities approximated their

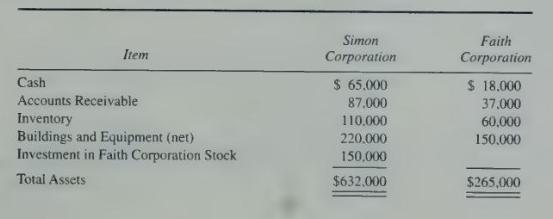

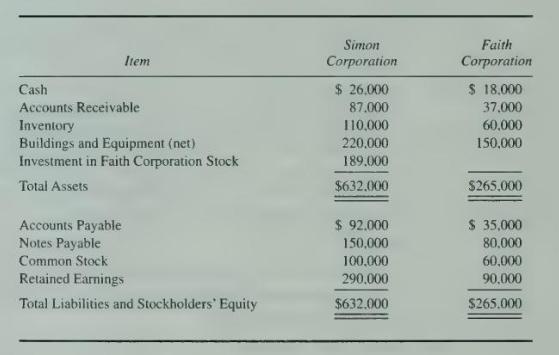

Simon Corporation purchased 100 percent of the common stock of Faith Corporation on December \(31,20 \mathrm{X} 2\), for \(\$ 150,000\). Data from the balance sheets of the two companies included the following amounts as of the date of acquisition:At the date of the business combination, the book

Simon Corporation purchased 100 percent of the common stock of Faith Corporation on December \(31,20 \times 2\), for \(\$ 189,000\). Data from the balance sheets of the two companies included the following amounts as of the date of acquisition:At the date of the business combination, Faith's net

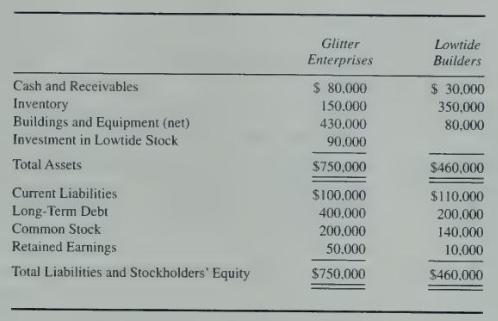

Glitter Enterprises purchased 60 percent of the stock of Lowtide Builders Inc. on December 31, 20X4. Balance sheet data for Glitter and Lowtide on January 1, 20X5, are as follows:\section*{Required}a. Give all eliminating entries needed to prepare a consolidated balance sheet on January 1, 20X5.b.

The balance sheet of Sparkle Corporation at January 1, 20X7, reflected the following balances:Harrison Corporation, which had just entered into an active acquisition program, purchased 80 percent of the common stock of Sparkle on January 2, 20X7, for \(\$ 470,000\). A careful review of the fair

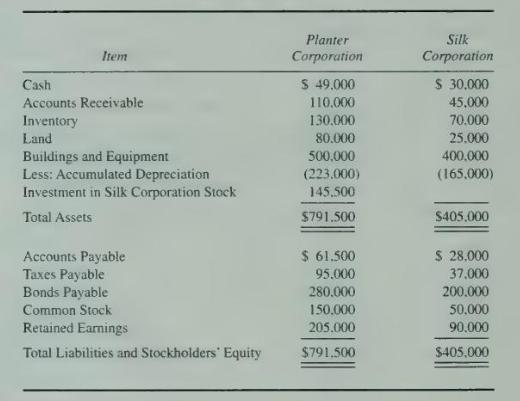

Planter Corporation purchased 70 percent of the common stock of Silk Corporation on December 31. 20X2. Balance sheet data for the two companies immediately following the acquisition are given below:At the date of the business combination, the book values of Silk's net assets and liabilities

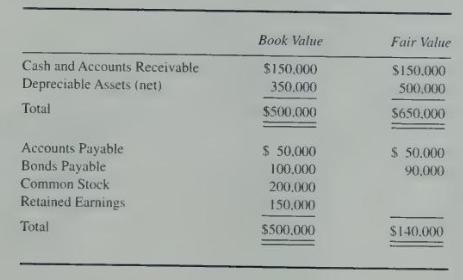

Jefferson Company purchased all of the common shares of Louis Corporation on January 2. 20X3. for \(\$ 789.000\). At the date of combination, the balance sheet of Louis Corporation appeared as follows:The fair values of all of Louis's assets and liabilities were equal to their book values except

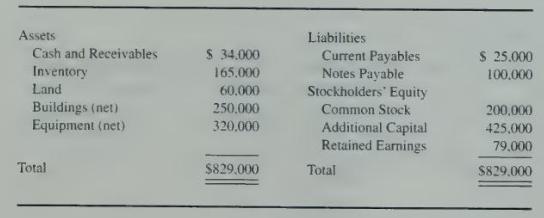

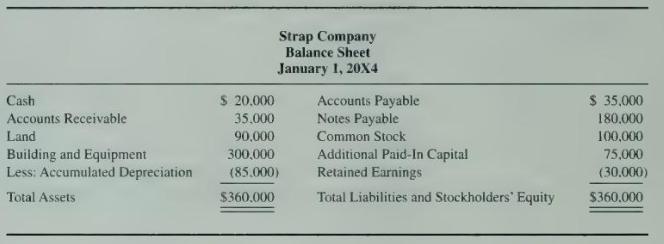

General Corporation purchased 80 percent of the voting common stock of Strap Company on January 1, \(20 \mathrm{X} 4\), for \(\$ 138,000\). The balance sheet of Strap at the date of acquisition contained the following balances:At the date of acquisition, the reported book values of Strap Company's

Select the correct answer for each of the following questions.1. Parent Company holds 80 percent of the stock of Subsidiary Company. Parent net assets are \(\$ 400,000\), and Subsidiary net assets are \(\$ 150,000\). Noncontrolling interest in the consolidated balance sheet is reported at:a. \(\$

On January 1, 20X9. Long Corporation purchased 60 percent of the common stock of Shortway Company and recorded the following entry:The book values and fair values of the balance sheet items reported by Shortway at January 1 ,\section*{Required:}a. Compute the amount of the purchase differential

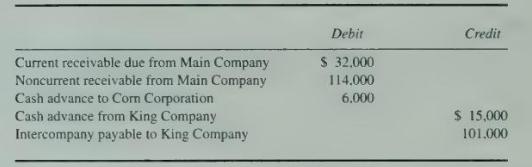

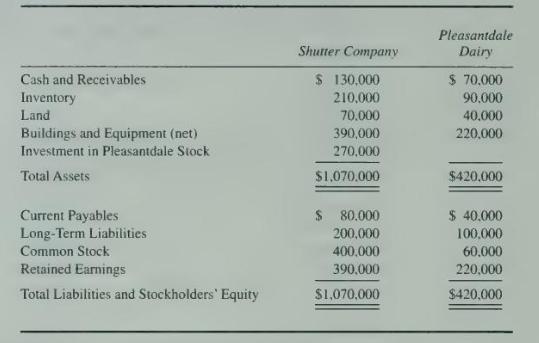

Shutter Company owns 90 percent of the stock of Pleasantdale Dairy. The balance sheets of the two companies immediately after the acquisition of Pleasantdale showed the following amounts:At the date of acquisition, Pleasantdale owed Shutter \(\$ 8,000\) plus \(\$ 900\) accrued interest. The accrued

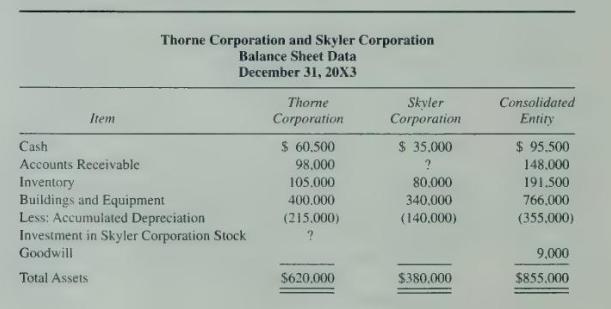

Thorne Corporation purchased controlling ownership of Skyler Corporation on December 31, 20X3, and a consolidated balance sheet was prepared immediately. Partial balance sheet data for the two companies and the consolidated entity at the date were:During 20X3, Thorne provided engineering services

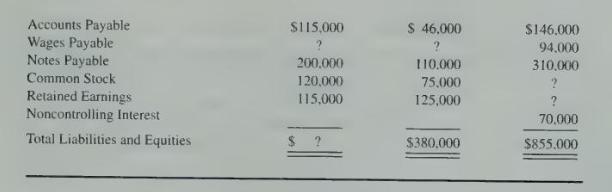

Kasper Corporation acquired controlling interest over Timmin Company on January 1, 20X7, and a consolidated balance was prepared. Partial balance sheet data for Kasper Corporation and Timmin Company and the consolidated entity is presented below:The fair value of Timmin's land was \(\$ 80,000\) and

Teresa Corporation purchased all the voting shares of Sally Enterprises on January 1, 20X4. Balance sheet amounts for the companies on the date of acquisition were as follows:The buildings and equipment reported by Sally Enterprises on January 1, 20X4, were estimated to have a market value of \(\$

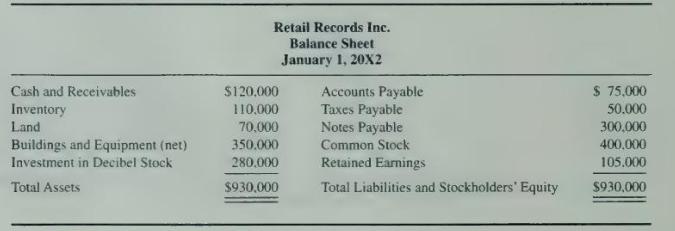

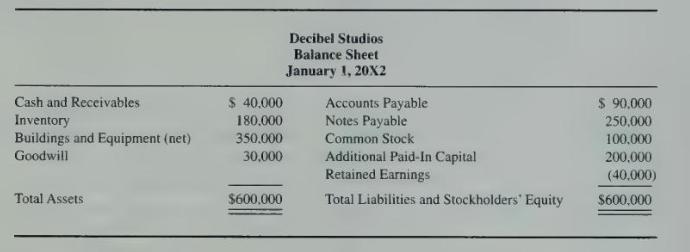

Retail Records Inc. purchased all the voting shares of Decibel Studios on January 1, 20X2, for \(\$ 280,000\). The balance sheet of Retail Records immediately after the combination contained the following balances:The balance sheet of Decibel at acquisition contained the following balances:On the

Cameron Corporation purchased 70 percent of the common stock of Darla Corporation on December \(31,20 \times 4\), for \(\$ 87,500\). Data from the balance sheets of the two companies included the following amounts as of the date of acquisition:At the date of the business combination, the book

Cameron Corporation purchased 70 percent of the common stock of Darla Corporation on December 31,20X4, for \(\$ 102,200\). Data from the balance sheets of the two companies included the following amounts as of the date of acquisition:At the date of the business combination, the book values of Darla

Forward Company was 75 percent acquired by Quinn Company on January 1, 20X9. The following balance sheet information was provided by the companies at the time:\section*{Required}a. Give all eliminating entries to prepare a consolidated balance sheet as of the date of acquisition.b. Prepare a

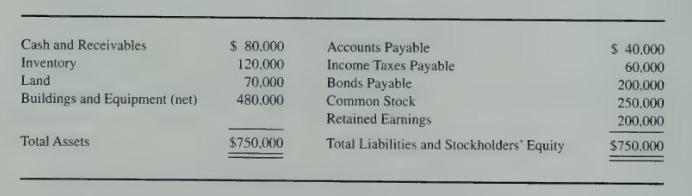

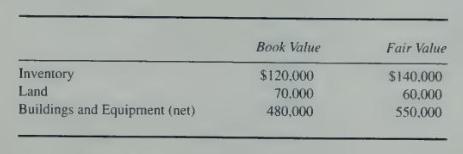

Skyhigh Airlines acquired 80 percent of the stock of Klunker Car Rentals for \(\$ 285,000\) on January 1, 20X2. Summarized balance sheets for the two companies on January 1, 20X2, are presented below:At the time of acquisition, Klunker's land had an estimated value of \(\$ 40,000\), its buildings

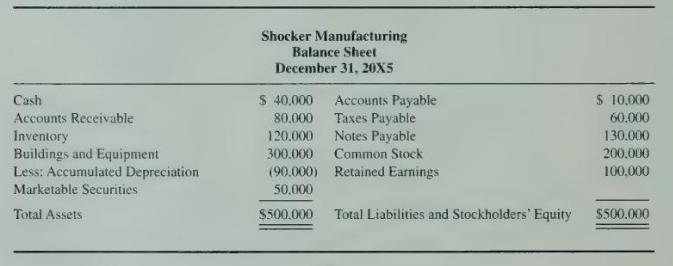

Whitehurst Electronics published the following balance sheet for December 31, 20X5:The balance sheet for Shocker Manufacturing for December 31, 20X5, appeared as follows:Whitehurst acquired 80 percent of Shocker's common stock on December 31, 20X5. The fair values of Shocker's identifiable assets

Astor Corporation acquired 60 percent of the outstanding shares of Shield Company on January 1, 20X7. Balance sheet data for the two companies immediately following the purchase were as follows:As indicated in the parent company balance sheet, Astor purchased \(\$ 50,000\) of Shield Company bonds

On January 2. 20X8, B.N. Counter Corporation purchased 75 percent of the outstanding common stock of Ticken Tie Company. In exchange for Ticken Tie's stock. B.N. Counter issued bonds payable with a par and fair value of \(\$ 500,000\) directly to the selling stockholders of Ticken Tie. The two

Compared with at the date of combination, how does the elimination process change when consolidated statements are prepared after the date of acquisition?

What are the three parts of the consolidation workpaper, and what sequence is used in completing the workpaper parts?

How is the amount of income assigned to a noncontrolling interest determined?

How are dividend declarations of a subsidiary reported in the consolidated retained earnings statement?

Why is the income assigned to the noncontrolling interest treated as a deduction in computing consolidated net income?

What portion of other comprehensive income reported by a subsidiary is included in the consolidated statement of other comprehensive income as accruing to the parent company shareholders?

How is consolidated net income computed in a consolidation workpaper?

Why is the beginning retained earnings balance for each company entered in the three-part consolidation workpaper rather than the ending balance?

When Ajax was preparing its consolidation workpaper, the differential was properly assigned to buildings and equipment. What additional entry generally must be made in the workpaper?

How will other comprehensive income elements reported by a subsidiary affect the consolidated financial statements?

What type of adjustment must be made in preparing the consolidation workpaper if a differential is assigned to land and the subsidiary disposes of the land in the current period?

Why are the eliminating entries that are used in preparing the consolidation workpaper different when the parent uses the cost method in accounting for its investment rather than the equity method? What is the major difference in the eliminating entries?

The newest clerk in the accounting office recently entered trial balance data for the parent company and its subsidiaries on the new company microcomputer. After a few minutes of additional work needed to eliminate the intercompany investment account balances, he expressed his satisfaction at

A new employee has been given responsibility for preparing the consolidated financial statements of Sample Company. After attempting to work alone for some time, the employee seeks assistance in gaining a better overall understanding of the way in which the consolidation process

Following a purchase-type business combination, any differential (excess of cost over the book value of the net assets acquired) must be allocated to specific assets and liabilities each time consolidated financial statements are prepared. Different companies approach the task of allocating the

Select the correct answer for each of the following questions.1. When a parent-subsidiary relationship exists, consolidated financial statements are prepared in recognition of the accounting concept of:a. Reliability.b. Materiality.c. Legal entity.d. Economic entity.2. Consolidated financial

Select the correct answer for each of the following questions.1. Par Corporation owns 60 percent of Sub Corporation's outstanding capital stock. On May 1, 20X8, Par advanced Sub \(\$ 70,000\) in cash, which was still outstanding at December 31, 20X8. What portion of this advance should be

Select the correct answer for each of the following questions.1. How would the retained earnings of a subsidiary acquired in a business combination usually be treated in a consolidated balance sheet prepared immediately after the acquisition?a. Excluded for both a purchase and a pooling of

On January 1, 20X3, Guild Corporation reported total assets of \(\$ 470,000\), liabilities of \(\$ 270,000\), and stockholders' equity of \(\$ 200,000\). At that date, Bristol Corporation reported total assets of \(\$ 190,000\), liabilities of \(\$ 135,000\), and stockholders' equity of \(\$

Potter Company purchased 100 percent of the voting common shares of Stately Corporation by issuing bonds with a par value and fair value of \(\$ 135,000\) to the existing shareholders of Stately. Immediately prior to the acquisition, Potter Company reported total assets of \(\$ 510,000\),

Showing 600 - 700

of 2939

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers