New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing 12th

Modern Auditing 5th Edition Walter Gerry Kell, William C. Boynton, Richard E. Ziegler - Solutions

Data relative to three sampling plans are presented below:Required:Calculate sample size in each of the plans. Show computations. Materiality Size of population Desired reliability Estimated population standard deviation Internal control effectiveness Supplemental audit procedures effectiveness.

An audit client has an inventory of 10,000 head of beef cattle (steers). The steers were purchased at various dates and varying prices. In view of the dollar amounts involved, \(\$ 150,000\) is considered to be a material amount, and a 95 percent confidence level is deemed to be necessary. Internal

This question is designed to test your knowledge of alpha and beta risks in estimation sampling for variables.Required:a. Compute the maximum planned beta risk to specify in a statistical test for each of the following situations if your desired combined reliability is 95 percent, supplemental

A contractor has 1,515 homes in various stages of construction. From a random presample of 50 homes, you determine that the estimated population standard deviation is \(\$ 2,000\). On the basis of audit risk and other factors, you set desired precision \(\$ 250 .(0) 0\) and desired reliability at

You are engaged in the annual examination of The Mountainview Corporation, a wholesale office supply business, for the year ended September 30. A review of internal control has revealed substantial weaknesses. You have been assigned to examine the accounts receivable.The following information is

In planning the audit of accounts receivable, you decide to select accounts for confirmation using a variables estimation sampling plan. A major reason for your decision is the advantage of being able to measure and control the risks involved. You recall that auditing literature describes ultimate

The following facts relative to a variables sampling plan are presented in random order:1. Combined reliability is 95 percent.2. Materiality is \(\$ 80,000\).3. Audited value of sample items is \(\$ 371,250\).4. The preliminary estimated population standard deviation is \(\$ 200\).5. Effectiveness

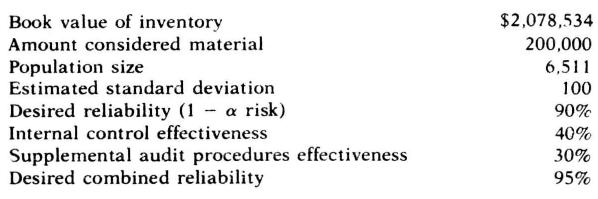

You desire to evaluate the reasonableness of the book value of the inventory of your client, Draper, Inc. You satisfied yourself earlier as to inventory quantities. During the examination of the pricing and extension of the inventory, the following data were gathered using appropriate unrestricted

During the course of an audit engagement, a CPA attempts to obtain satisfaction that there are no material misstatements in the accounts receivable of a client. Statistical sampling is a tool that the auditor often uses to obtain representative evidence to achieve the desired satisfaction. On a

The Easy Finance Company has 3,000 loans outstanding at a recorded total book value of \(\$ 960,000\). As the auditor on this engagement, Mary Jones selects a sample of 300 loans for vouching. These loans have a reported book value of \(\$ 93,000\) and a verified book value of \(\$

Fairview Publishing Company, incorporated in 1974, is a small, closely held publisher of high school textbooks. A local accounting firm has reviewed the preparation of the financial statements, performed certain audit procedures, and prepared the tax returns for many years. The accountants' report

Describe the nature and scope of tests of balances.

Identify and briefly explain the primary purpose of the audit objectives that are applicable to tests of balances.

What audit procedures are required to verify the (a) existence or occurrence and (b) completeness of cash balances?

What precautions should be taken by the auditor in (a) counting cash on hand and (b) confirming bank balances?

Identify the five types of information included in a standard bank confirmation.

How reliable is a bank reconciliation in terms of audit evidence? Briefly defend your answer.

What safeguards must be taken by the auditor in obtaining and using a bank cutoff statement?

What steps should be taken by the auditor after he has received a cutoff statement?

What steps are involved in performing a cash cutoff test?

a. Define and illustrate kiting.b. How can kiting be prevented and detected?

List four cash items that require special classification and disclosure. For each item indicate the required statement presentation.

Identify the audit procedures in tests of receivable balances that satisfy the audit objectives of (a) existence and occurrence and (b) completeness.

In confirming receivables, what conditions (a) may make it impracticable or unreasonable for the auditor to perform this test, (b) should be considered by the auditor in determining the form of the confirmation request, and (c) are relevant to the auditor in determining the timing and extent of the

What precautions should the auditor take in confirming accounts receivables?

When the auditor is unable to confirm accounts receivable, indicate (a) the alternative procedures he may perform and (b) the effects on his audit report.

For an aged trial balance prepared by the client, explain (a) the auditor's responsibilities and (b) the specific types of data he may obtain therefrom.

How does the auditor perform a sales cutoff test?

What is the best evidence of the collectibility of an account?

How does the auditor establish the reasonableness of the allowance for uncollectible accounts?

What specific assistance can a computer provide in verifying accounts receivable balances?

As the senior auditor on the audit of the Elles Company for the year ending December 31, you discover the following errors in cash working papers prepared by your assistants:1. Compensating bank balances were overlooked.2. Kiting was missed.3. Several December 31 checks were not recorded as

Lingham Company's fiscal year ends on April 30, and the company's certified public accountant, Sanders \& Stein, conducts the annual audit during May and June. Sanders \& Stein has prepared audit procedures for the different phases of the audit engagement with Lingham Company. Included among the

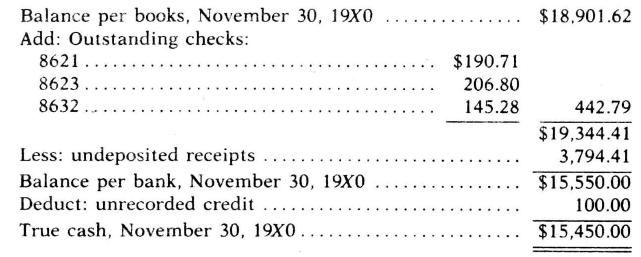

The Patricia Company had poor internal control over its cash transactions. Facts about its cash position at November 30, 19X0 were as follows:The cashbooks showed a balance of \(\$ 18,901.62\), which included undeposited receipts. A credit of \(\$ 100\) on the bank's records did not appear on the

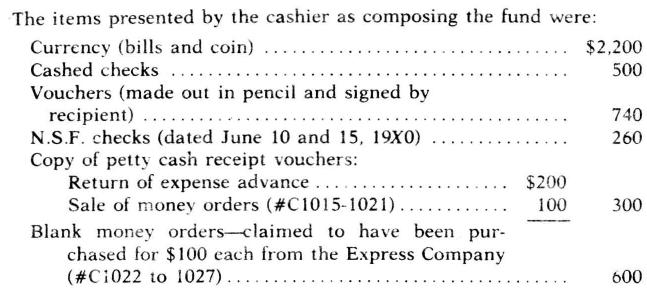

A surprise count of the \(Y\) Company's imprest petty cash fund, carried on the books at \(\$ 5,000\) was made on November \(10,19 X 0\).The company acts as agent for an Express Company in the issuance and sale of money orders. Blank money orders are held by the cashier for issuance upon payments

You are the in-charge accountant examinıng the financial statements of the Gutzier Company for the year ended December 31, 19X0. During. late October, 19X0, you, with the help of Gutzler's controller, completed an internal control questionnaire and prepared the appropriate memorandums describing

Dodge, CPA, is examining the financial statements of a manufacturing company with a significant amount of trade accounts receivable. Dodge is satisfied that the accounts are properly summarized and classified and that allocations, reclassifications, and valuations are made in accordance with GAAP.

The following situations were not discovered in the audit of Pars Company by an inexperienced staff assistant:1. Several accounts were incorrectly aged on the client's aging schedule.2. Interest earned on notes receivable was incorrectly accrued.3. A note reported to be held by a bank for

Jerome and Gerard, Certified Public Accountanis, are preparing for the annual audit of the Fordham Office Machine Company. Several procedures which are included in the audit program pertaining to accounts receivable and sales are summarized below:1. Evaluate internal controls relating to accounts

You have been assigned to the first examination of the accounts of The Chicago Company for the year ending March 31, 19X1. The accounts receivable were circularized at December \(31,19 X 0\) and at that date the receivables consisted of approximately 200 accounts with balances totaling \(\$

The Fox Company has been using 0.05 percent of net sales in providing for uncollectible accounts. The provision, however, has been inadequate since the allowance account shows a debit balance of \(\$ 1,272\) on December 31, \(19 X 0\) before making the annual provision for bad debts.On December 31,

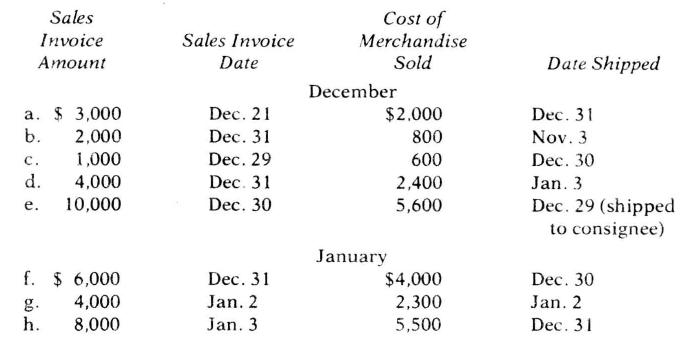

You are engaged to perform an audit of the Wilcox Corp. for the year ended December \(31,19 X 0\).Only merchandise shipped by the Wilcox Corporation to customers up to and including December 30, 19X0 has been eliminated from inventory. The inventory as determined by physical inventory count has

You have been engaged to examine the financial statements of the Elliott Company for the year ended December 31, 19X1. You performed a similar examination as of December 31, 19X7. The trial balance of the company as of December 31, 19X1 shows: interest receivable- \(\$ 47,450,6.5\) percent secured

As the in-charge auditor, you begin your field work to examine the December 31 financial statements of a client on January 5, knowing that you must leave temporarily for another engagement on January 7 after outlining the audit program for your assistant. Before leaving, you inquire about the

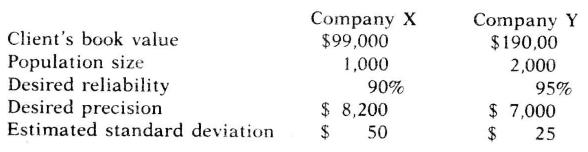

Data relevant to the audit of accounts receivable in two companies are tabulated below:The auditor decides to consider alpha risk only.Required:a. Compute the required sample size for each company with replacement.b. Compute the required sample size for each company without replacementc. Ignoring

An auditor is conducting an examination of the financial statements of a wholesale appliance distributor. The distributor supplies appliances to hundreds of individual customirs in th: metropolitan area. The distributor maintains detail accounts receivable records on a computer disk. At the end of

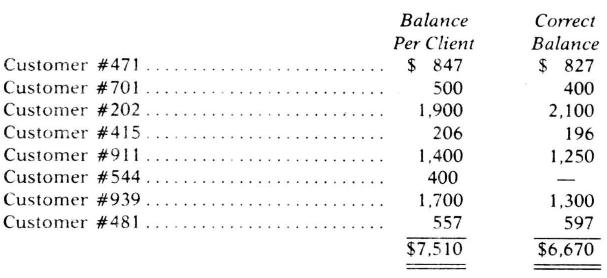

You are auditing the financial statements of Colonial, Inc., a wholesale office supply company, for the year ended September 30, 19X0. Your internal control review points out many weaknesses. In examining the accounts receivable, the following information is available as of September \(30,19 X

Identify the audit procedures that enable an auditor to verify the (a) existence or occurrence and (b) valuation or allocation objectives for inventory balances.

For the observation of inventories, indicate (a) when this test is required, (b) the meaning of inventory taking, and (c) the timing and extent of the test.

Identify the items that should be (a) included in the inventory-taking plan and (b) done in observing inventories.

When statistical sampling methods are used in determining inventories, what additional requirements must be met by the auditor?

What alternative procedures are available to the auditor when he is unable to observe (a) the ending inventory and (b) the beginning inventory?

Why is it necessary for the auditor to make tests of the client's inventory counts?

What procedures are required when inventories stored in a public warehouse are material?

a. Explain the auditor's responsibility for the quality and condition of the inventory.b. Indicate how the auditor can discover obsolete and slow moving items.

What steps are involved in verifying inventory pricing?

a. What information is required to determine sample size in a basic variables sampling plan of inventory balances?b. Assuming the auditor has calculated the estimated population value, what additional information is required to determine the achieved precision interval?

What data and program(s) are needed to use the computer in an inventory pricing test?

What are the principal differences between the audit of plant assets and current assets?

What audit procedures are performed to determine (a) rights and obligations and (b) valuation or allocation of plant assets?

Identify the relationships that may be used in making an analytical review of property, plant, and equipment. For each relationship indicate the type of fluctuation that might occur and the cause thereof.

What procedures may be helpful in determining whether all plant asset retirements have been recorded?

What factors are involved in determining whether a company has been consistent in recording repair and maintenance expenditures?

Identify the principal differences between tests of asset balances and tests of current liability balances.

a. What audit procedures are used to verify the existence or occurrence and completeness of accounts payable?b. How may the auditor obtain evidence as to the valuation and completeness of accrued wages payable?

What purposes are served by examining payments to creditors subsequent to the statement date?

What procedures are useful to the auditor in searching for unrecorded accounts payable?

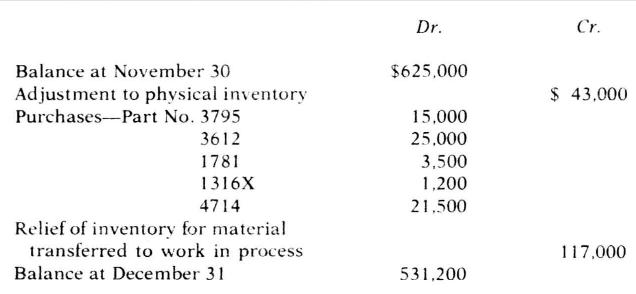

In performing tests of balances on inventory balances, the auditor should recognize that the following potential errors may occur or exist:1. All inventory items are not counted or tagged.2. Extension errors are made on the client's inventory summaries.3. Purchases received near the balance sheet

Often an important aspect of a CPA's examination of financial statements is his observation of the taking of the physical inventory.Required:a. What are the general objectives or purposes of the CPA's observation of the taking of the physical inventory? (Do not discuss the procedures or techniques

Ace Corporation does not conciuct a complete annual physical count of purchased parts and supplies in its principal warehouse but uses statistical sampling instead to estimate the year-end inventory. Ace maintains a perpetual inventory record of parts and supplies and believes that statistical

Your audit client, Household Appliances, Inc. operates a retail store in the center of town. Because of lack of storage space Household keeps inventory that is not on display in a public warehouse outside of town. The warehouseman receives inventory from suppliers and, on request from your client

As auditor for the Court Company, you decide to use variables sampling to estimate the total cost of an inventory of 1,150 items which has a net book value of \(\$ 260,400\). The auditor decides to use a sampling plan that will provide assurance that a fairly stated book value is not rejected as

In auditing the annual physical inventory being taken by employees in the Sutter Company, you decide to use estimation sampling for variables to estimate the cost of the inventory. You choose to use a plan that will consider the risk of accepting a materially misstated book value as being fairly

Rivers, CPA, is the auditor for a manufacturing company with a balance sheet that includes the caption "Property, Plant and Equipment." Rivers has been asked by the company's management if audit adjustments or reclassifications are required for the following material items that have been included

In connection with the annual examination of Johnson Corporation, you have been assigned to audit the fixed assets. The company maintains a detailed property ledger for all fixed assets. You prepared an audit program for the balances of property, plant, and equipment but have yet to prepare one for

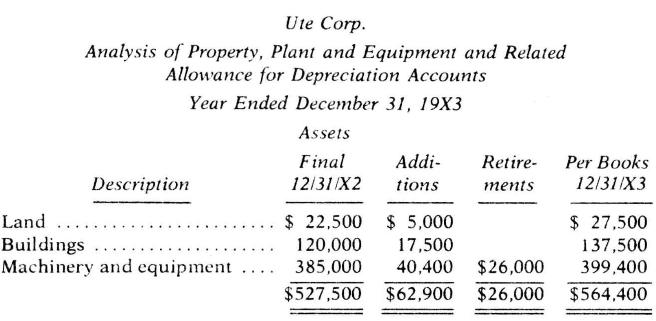

You are engaged in the examination of the financial statements of the Ute Corporation for the year ended December 31, 19X3. The following schedules for the property, plant, and equipment and related allowance for depreciation accounts have been prepared by the client. You have checked your prior

You were in the final stages of your examination of the financial statements of Ozine Corporation for the year ended December 31, 19X0 when you were consulted by the Corporation's president who believes there is nopoint to your examining the \(19 \times 1\) voucher register and testing data in

Your client, Special Cases, Inc., took its physical inventory at November 30, one month before its December 31, year-end.The client compiled the inventory as of November 30 and "carriedforward" the inventory amounts to December 31.You were present at the taking of the physical inventory and you

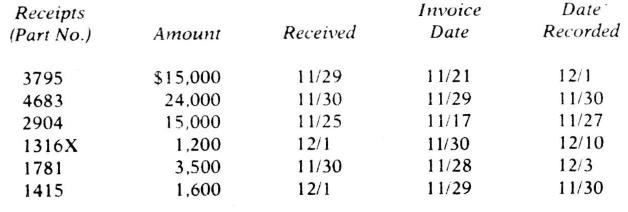

Your firm has been engaged to examine the financial statements of Brown Appliances, Inc. for the year ended December 31. The company manufactures major appliances sold to the general public through dealers and distributors.You are to audit the trade accounts payable of a division of Brown

Indicate the functions associated with the investing cycle.

Evaluate the materiality and audit risk for investing cycle balances.

Explain the specific internal accounting control objectives for the functions identified in (1) above.

What internal accounting control principles are applicable to (a) executing and (b) recording securities transactions?

Identify the internal control principles that reiate directly to the custody of securities.

What data should be shown in the working papers concerning securities?

Indicate the form and timing of confirming securities held by outside custodians.

What audit procedures are useful in verifying the (a) rights and obligations and (b) valuation or allocation of investment balances?

What evidence is available to the auditor in determining (a) "market" when securities are accounted for on the cost basis and (b) the value of underlying net assets when securities are accounted for under the equity method?

What supplemental disclosures in notes to financial statements are required for investments in securities?

Identify (a) the functions and (b) the specific internal accounting control objectives for financing cycle transactions.

Briefly explain the application of (a) authorization procedures and (b) segregation of functions to the proper execution of transactions in the financing cycle.

What audit procedures are useful in verifying (a) existence or occurrence, (b) completeness, and (c) valuation or allocation of long-term debt balances?

What purposes are served in confirming debt with holders?

What specific relationships may be determined in making an analytical review of long-term debt balances?

What audit procedures may be employed to establish the (a) existence or occurrence and (b) right and obligations of stockholders' equity balances?

What procedures are required in vouching dividend payments?

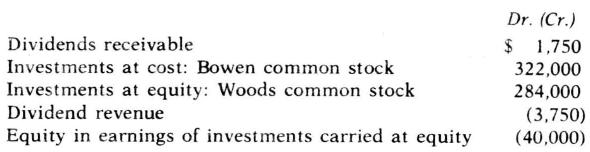

You have been assigned to the examination of the "investments" account of one of your firm's older clients, the \(D\) Co. During the prior year, your client received more than \(\$ 1\) million from the sale of all of its stock in a subsidiary. The proceeds from this sale were promptly invested in

You have been assigned to examine the "Long-term Investments" account of the Richard Company, a new audit client of your firm, for the current year. The client's records show an investment of \(\$ 75,000\) for 750 shares of the common stock of one of its major suppliers of raw materials. This

In verifying investing cycle balances, the auditor should recognize that the following errors may occur or exist:1. A mathematical error is made in accruing interest earned.2. A 25 percent common stock investment in an affiliated company is accounted for on the cost basis.3. Securities held by an

You have been engaged to examine the financial statements of the Elliott Company for the year ended December \(31,19 X 1\). You performed a similar examination as of December 31, 19X0.A partial trial balance for the company as of December \(31,19 \times 1\) shows:You have obtained the following

Showing 400 - 500

of 1793

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers