New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing assurance services

Modern Auditing 1st Edition Graham Cosserat - Solutions

Which of the following procedures would not be appropriate for an auditor in discharging his or her responsibilities concerning the existence of the entity’s stock?(a) Obtaining written representation from the entity as to the existence, quality and value of the stock.(b) Carrying out

If the client maintains perpetual stock records and performs cyclical counts of stock rather than one major stock-take at the end of the year, what should the auditor do?(a) Suggest to the client that it performs a full year-end stock count.(b) Observe several of the cyclical counts — and not

What should an auditor do to ensure that stock is stated at the lower of cost and net realisable value?(a) Select a sample of stock purchases made during the year and check the associated invoice to ensure they are not recorded at more than that value.(b) Compare a sample of stock items held at

In auditing fixed assets, why might the auditor decide to assess control risk at the maximum and perform predominantly substantive testing?(a) The number of additions to/disposals of fixed assets is usually not a material number — therefore, it is not of concern to the auditor.(b) Fixed assets in

What audit procedure is most likely to detect the incorrect capitalisation of an expense to fixed assets?(a) Checking a sample of repairs and maintenance expenses to supporting documentation.(b) Selecting a sample of additions to fixed assets, and ensuring that they have adequate supporting

You are currently reviewing the audit files of Eighties Fashions Ltd, a manufacturer and retailer of retro clothing. In your review of your audit assistant’s work on stock, you note the following:1. In performing substantive analytical procedures, the audit assistant has used several detailed

Your firm is the auditor of Daybrook Insurance Brokers Ltd, which operates from a number of branches and provides insurance for the general public and businesses. The company obtains insurance from large insurance companies, and takes a commission for its services. You have been asked to audit

You are currently planning the audit of Munchees Ltd, a manufacturing company which sells biscuits and snack foods to a large number of retailers nationally. You have turned your attention specifically to the audit of inventory, and have obtained the following information from client staff:•

Your firm is auditing the financial statements of Newthorpe Manufacturing Limited for the year ended 30 June 20X0. You have been assigned to the audit of the company’s fixed assets, which comprise freehold land and buildings, plant and machinery, fixtures and fittings and motor vehicles.The

What are the three main audit objectives for cash, and why?

How might an auditor test to ensure that cut-off for cash has been correctly performed?

What information is requested in confirming bank deposit balances?

What effects may the acceptable level of detection risk have on substantive tests for reconciling bank accounts?

What are the three main audit objectives for investments, and why?

State and describe the functions that relate to investing transactions.

Discuss some of the special considerations involved in the audit of investments in group entities.

Joplin Ltd’s financial year ends on 30 June 20X1 and the company’s auditor, Hagan and Partners, conducts the annual audit during July and August. Hagan and Partners has prepared auditing procedures for the different phases of the audit engagement with Joplin Ltd. Included among the steps in the

Dealtime Ltd is a company that has substantial investments in south-east Asia and carries out a significant volume of trading with the region. The company has substantial shareholdings in a number of south-east Asian companies and has a controlling interest in Pakti Ltd, listed in Malaysia.

You have been asked by the chairperson of Beeston Trading Limited, Mrs Burton, to carry out an investigation of a suspected fraud by the company’s cashier. The cashier, Ralph Biggs, has left the firm without notice.Beeston Trading Limited is a small company and there have been few controls and

You are performing the audit of Galway Ltd for the financial year ended 30 June 20X0.Under the terms of a major loan contract, Galway Ltd is required to maintain certain financial ratios. If the ratios are breached, the loan is immediately due for repayment. This would create significant cash flow

Identify the distinctive characteristics of the audit work associated with completing the audit.

Define the two types of after-balance-date events and indicate the potential accounting effects of each type. 3

What is the auditor’s responsibility for after-balance-date events? How does the auditor discharge this responsibility?

What is a solicitor’s representation letter? What effect might the failure of a solicitor to respond to a request for representation have on the auditors’ report?

What objectives are met in obtaining a management letter of representation? What is the relationship between a management letter of representation and other auditing procedures?

Discuss the various steps required in evaluating the findings of the audit.

What purpose does a management letter serve?

In the auditors’ completion of the audit, which of the following is not a subsequent event procedure?(a) Read available minutes of meetings of directors.(b) Make enquiries with respect to the previously audited financial statements to establish whether new information has become available that

Which of the following would an auditor ordinarily perform during his or her review of after-balance-date events?(a) Analyse related party transactions to discover possible irregularities.(b) Investigate control weaknesses previously reported to management.(c) Inquire of the entity’s solicitor

The auditors are concerned with completing various phases of the examination after the balance sheet date. This period extends to:(a) the date of the final review of the audit working papers.(b) the date of the auditors’ report.(c) the issue of the financial statements.(d) five months after the

The following matters came to the attention of the auditors before the audit fieldwork was completed. Which one would require an adjustment to be made to the financial statements?(a) A discussion by management to change the main operations of the company.(b) A major lawsuit against the company,

Auditors should send a letter of inquiry to those solicitors who have been consulted concerning litigation or claims. The primary reason for this request is to provide:(a) corroborative evidential matter.(b) information concerning the progress of cases to date.(c) anestimate of the amount of the

Which of the following is ordinarily included among the written management representations obtained by the auditors?(a) Sufficient audit evidence has been made available to permit the issue of an unqualified opinion.(b) All books of account and supporting documentation have been made available.(c)

Six months after issuing an unqualified opinion on a set of financial statements, the audit partner discovered that the engagement personnel on the audit failed to confirm several of the client’s material debtors’ balances. The audit partner should first:(a) inquire whether there are persons

Subsequent to the issuance of the auditors’ report, the auditors became aware of facts existing at the report date that would have affected the report had the auditors then been aware of them. After determining that the information is reliable, the auditors should next:(a) notify the board of

Cosmos Ltd is a listed company that manufactures satellites and other communication equipment. It is now August 20X0, and the audit of Cosmos for the year ended 30 June 20X0 is nearing completion. You are the engagement manager. While reviewing the audit working papers, you identify several issues

During the audit of the financial statements of Blackheath Manufacturing Ltd (BM), the managing director, Mr S. Hill, and the auditor, Mr P. Wales, reviewed matters that were supposed to be included in a written management representation letter. Mr Hill prepared the following management

The financial year of Terry’s Tiles Ltd ended on 31 December 20XO. Your auditors’ report was signed on 26 February and the financial statements were issued on 9 March. Listed below are events that occur or are discovered from the date of the balance sheet to 30 June of the following year.

Brown and Collins, a firm of chartered accountants, is auditing the financial statements of Globe Ltd for the year ended 31 December 20X1. Tom Brown, the engagement audit partner, anticipates expressing an unqualified opinion on 20 May 20X2.Jane Grieves, an audit assistant on the engagement,

State the main audit objectives for (1) sales transactions and (2) debtors’ balances.

What is the sequence of steps normally associated with processing of credit sales? For each step, identify one control.

What are the major files and printed outputs of computerised processing for sales transactions?

For each of the three functions pertaining to cash receipts transactions, formulate two questions that may be used in preparing an internal control questionnaire for this transaction class.

For the sales adjustment transaction class, indicate the three main types of transaction that might occur. For each transaction type, indicate one question that might be used in an internal control questionnaire.

What are some of the inherent risk factors that may affect (1) sales transactions and (2) debtors’ balances?

Discuss why the principal risk associated with the audit of sales and debtors is overstatement.

Indicate the transaction classes that should be considered in assessing control risk for debtors assertions. Should the acceptable level of detection risk be based on the planned or actual level of control risk?

What do you think are the three main assertions for debtors? Indicate the primary substantive procedures for those assertions.

Which of the following controls would most likely help to ensure that all credit sales transactions of the entity are recorded?(a) The invoicing department supervisor matches pre-numbered shipping documents with entries in the sales journal.(b) The accounting department supervisor controls the

Which of the following internal control procedures would most likely ensure that all billed sales are correctly posted to the sales ledger?(a) Each shipment on credit is supported by a pre-numbered sales invoice.(b) The sales ledger is reconciled daily to the control account in the general

Sales revenue is usually a very material balance within the financial statements of a company. Why would an auditor mainly focus his or her work on sales transactions occurring at the end of the year rather than throughout the year?(a) There are usually larger sales transactions occurring at the

Which of the following tests of control would provide audit evidence for the management assertion of completeness of revenue?(a) Observe separation of duties between filling and dispatching orders.(b) Check to ensure that all dispatch orders have been properly matched to a sales invoice.(c) Ensure

After completing the testing of controls over cash receipts and sales adjustments, the auditor assesses the level of control risk to be higher than expected. How would this affect the auditor’s substantive audit work on debtors?(a) More work would need to be performed to ensure that the provision

Which of the following would most likely be detected by an auditor’s review of an entity’s sales cut-off?(a) Unauthorised goods returned for credit.(b) Excessive sales discounts.(c) Overlapping of year-end debtors.(d) Unrecorded sales for the year.Choose the best answer.

Which of the following would give the most assurance concerning the valuation assertion of debtors?(a) Tracing amounts in the subsidiary ledger to details on shipping documents.(b) Comparing debtors’ turnover ratios with industry statistics for reasonableness.(c) Sending a debtor’s confirmation

You are conducting the interim audit of the Lancastrian branch of CB Wholesalers Ltd, fashionwear wholesalers. The branch is the largest single outlet of the company and has substantial annual sales which are invoiced by the branch. Three methods are used to collect cash at the branch:• sales

Ally McNeil is conducting the audit of a wholesale electrical goods distributor, Electra Ltd.Electra supplies appliances to hundreds of individual customers in the metropolitan area of Bigtown. It maintains detailed accounts receivable records on a computer system. At the end of each business day,

Easy Europe Ltd (EE) is a large private company which operates a network of travel agencies throughout Middletown. EE uses a centralised on-line system to maintain its accounting records. Each branch accesses this system through PCs linked to the central computer network.Information technology

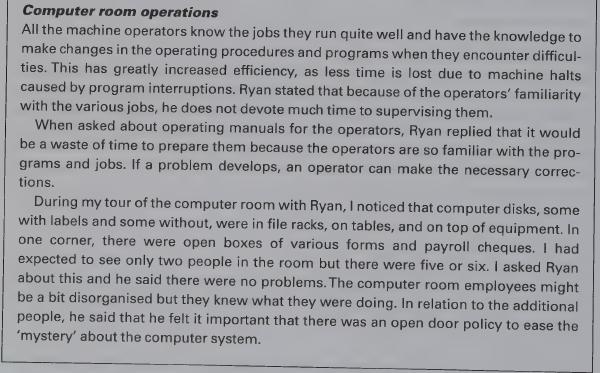

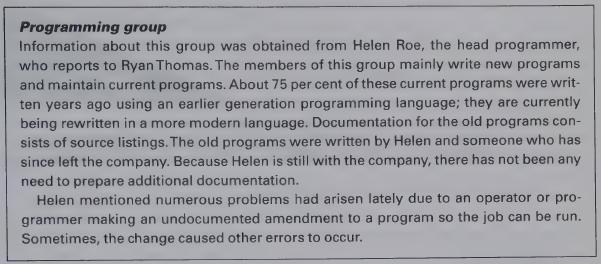

You have been assigned to the annual audit of Kaboom Ltd. You contacted the audit senior, Patrick Corr, and arranged a date to discuss the client and the current year’s audit.During your meeting with Patrick, he emphasised that he wanted to take a good look at the computer department. On the

You are an audit senior and you have just finished the audit of Speedy Spares Ltd — a used car parts company. One month later...Your audit partner calls you into his office — he is not happy! Speedy Spares has just gone into liquidation. It seems the financial controller was diverting company

Western Ltd purchased the assets of Green Ltd. The financial report of Green Ltd was audited by Donaghue Partners, registered company auditors. While performing the audit, Donaghue Partners discovered that Green’s accounts clerk had embezzled £500.Donaghue Partners also had some evidence of

Excregrow Ltd was a very successful fertiliser company operating in Sussex. The company had large stocks of fertiliser held in different locations throughout the county. The annual audit for 30 June 20X0 was completed by Detmold Forster, a firm of chartered accountants.It signed the audit report on

You are the external auditor of Kiwi Tours, a company which promotes New Zealand tours to the UK and owns a chain of duty-free shops. You have been auditing the company since it was listed on the London Stock Exchange in 1990. Although the accounts have never been qualified, you are aware that the

Identify the categories of management’s financial statement assertions and briefly explain each one.

Discuss the interrelationship between management assertions and the specific audit objectives developed for an entity.

What factors should the auditor consider when developing specific audit objectives?Can there be more than one specific audit objective for a particular account for each category of assertion? Explain.

Identify the types of auditing procedure that may be used to obtain evidence. For each procedure indicate one type of audit evidence that is obtained.

What information would you expect to see on a ‘standard’ audit working paper?

The objective of an audit of financial statements is:(a) to ensure that the company is free from all fraud.(b) to ensure that the financial statements are prepared in accordance with relevant accounting or other requirements.(c) to report that the controls within a company are operating

What audit procedure is most associated with completeness?(a) Checking that the sales ledger aged trial balance adds up.(b) Searching for all unmatched goods received notes.(c) Confirming a debtors balance with a customer.(d) Reviewing the outstanding cheque listing.Choose the best answer.

Inquiries of warehouse personnel concerning possible obsolete or slow-moving stocks provide assurance about management’s assertion of:(a) completeness.(b) existence.(c) presentation.(d) valuation.Choose the best answer.

To verify management’s assertion of existence, an auditor would most likely:(a) compare a sample of shipping documents to related sales invoices.(b) recalculate the total depreciation expense.(c) confirm a sample of recorded debtors by direct communication with the customer.(d) compare a sample

Which of the following audit objectives was derived from the management assertion of rights and obligations?(a) Stock quantities include all products, materials and supplies on hand.(b) Liens on the stocks are properly disclosed in the notes to the financial statements.(c) The entity has legal

What does ‘sufficient appropriate’ audit evidence mean?(a) The amount of audit evidence that can be obtained given the time budget on the task.(b) Adequate evidence has been obtained in the auditor’s professional judgement.(c) All material errors have been detected.(d) A qualified auditors’

What would not be described as corroborating information?(a) Analytical evidence.(b) Confirmation from the bank.(c) Bank reconciliation prepared by the accounts clerk.(d) Attendance by the auditor at the stocktake.Choose the best answer.

What is not required as part of the audit process?(a) Substantive procedures.(b) Tests of control.(c) Assessment of materiality.(d) Procedures to obtain an understanding of the accounting and internal control systems.Choose the best answer.

The auditor’s permanent working paper file should not normally include:(a) copies of the memorandum of association.(b) extracts from the entity’s bank statements.(c) details of mortgages.(d) past years’ financial statements.Choose the best answer.

Under what circumstances can an auditor disclose information in the audit working papers?(a) When the working papers are subpoenaed by a court.(b) Ifthe Inland Revenue requests some information.(c) If the stock exchange requires details about the company’s share trading activities.(d) If another

During the course of an audit some of the following evidence is obtained by the auditor:1. creditor’s monthly statement from the entity’s files;2. management working papers in making accounting estimates;3. letter from a customer stating that she will pay a balance owing;4. bank statement

A variety of specific auditing procedures for obtaining audit evidence is listed below.1. Send debtor’s confirmation letters to a number of the entity’s customers.2. Recompute depreciation charges.3. Compute gross profit rates for the current year and preceding year.4. Discuss the potential

The audit partner of Smythe and Associates, Sally Smythe, receives a phone call from another auditing firm asking whether it can review the audit working papers of Identical Ltd, a client her firm has recently lost. Sally is a bit nervous about this request because she made some adjustments last

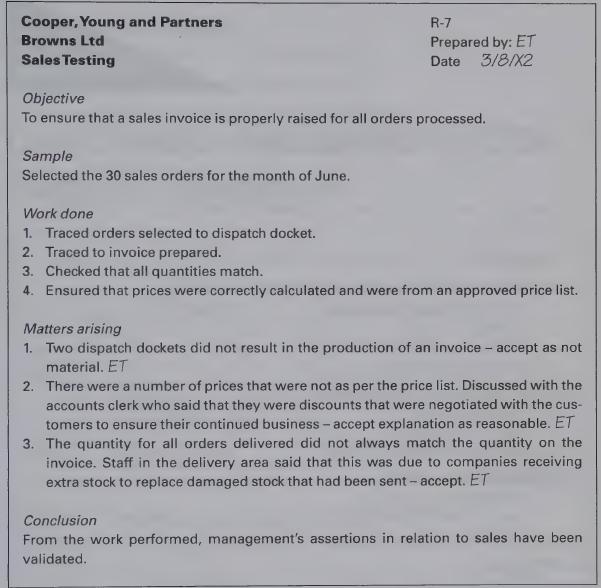

You are the audit partner of the accounting firm Cooper, Young and Partners. You are reviewing the work of an audit senior, Emily Tan, on your client Browns Ltd. You find the following working paper in relation to testing of sales invoices.RequiredReview the above working paper (note that it is the

Identify the four phases of a financial statement audit and discuss the time frame in which each of these occurs.

State the steps involved in accepting an audit engagement.

Why is it considered necessary for a successor auditor to communicate with a previous auditor? Identify three matters about which the proposed auditor should direct inquiries to the previous auditor.

Discuss the factors that an auditor must consider when deciding to accept an audit engagement.

Why is it important for an auditor to evaluate independence in deciding whether to accept a new client?

What are the purposes of an engagement letter?

Discuss the steps involved in the audit planning process.

Describe three types of information that an auditor might obtain to gain an understanding of the entity’s business and industry. How might these three types of information affect the audit plan?

Why is an auditor going to be interested in obtaining information about related parties in auditing an entity?

How can analytical procedures assist the auditor in audit planning?

The previous audit firm should tell the proposed audit firm:(a) the total cost it incurred in performing the audit of a company in the prior year.(b) its evaluation of the strength of the company’s internal control systems.(c) its understanding of the reason for the change in auditors.(d) all of

An auditor has been offered a new audit. What should the auditor do next?(a) The auditor should contact the client and discuss the risks associated with the audit for the purposes of planning.(b) The auditor should assess the integrity of management and unusual risks associated with the business

The exercise of ‘due professional care’ requires that an auditor:(a) examines all available corroborating evidence.(b) critically reviews the judgement exercised at every level on the engagement.(c) reduces control risk below the maximum.(d) attains the proper balance of professional experience

Engagement letters are widely used in practice for professional engagements of all types. The primary purpose of the engagement letter is to:(a) remind management that the primary responsibility for the financial statements rests with management.(b) satisfy the requirements of the auditor’s

The element of the audit planning process most likely to be agreed with the client before implementation of the audit strategy is the determination of:(a) methods of statistical sampling to be used in confirming debtors.(b) schedules and analyses to be prepared by the client’s staff.(c) pending

In the tour of the client’s operations, the auditor noted two machines were not operating in the client’s factory. This meant that production was 25 per cent lower than normal. The factory manager informed the auditor that this was because the machines were being serviced; however, the auditor

Analytical procedures used in planning an audit should focus on identifying:(a) material weaknesses in the accounting and internal control systems.(b) the predictability of financial data from individual transactions.(c) the various assertions that are embodied in the financial statements.(d) areas

In performing your analytical review of sales, you find the following for a company with a 30 June year-end:Monthly gross profit April — 25 per cent May - 27 per cent June - 37 per cent July - 21 per cent How would this affect the audit plan?(a) It would be necessary to discuss with management

Showing 1600 - 1700

of 2689

First

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

Last

Step by Step Answers