New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing assurance services

Auditing Assurance And Risk 3rd Edition W. Robert Knechel, Steve Salterio, Brian Ballou - Solutions

Consider the following two independent situations:a. Company Alpha supplies women's clothes from its seven regional warehouses to small retail stores in shopping malls and roadside mini-malls throughout the country. By employing a sophisticated bar-coding scheme, Company Alpha tracks each article

Many organizations are implementing production process innovations designed to move more to a just-in-time (JIT) systems emphasizing lean manufacturing. One of the goals of this process is to minimize inventory storage costs for production inputs and outputs. Describe the impact of the production

United States accounting rules (Accounting Research Bulletin No. 43) require that inventory be carried on the financial statements at the lower of its cost or market value with the market value of the inventory bounded on the upper end by net realizable value and on its lower end by net realizable

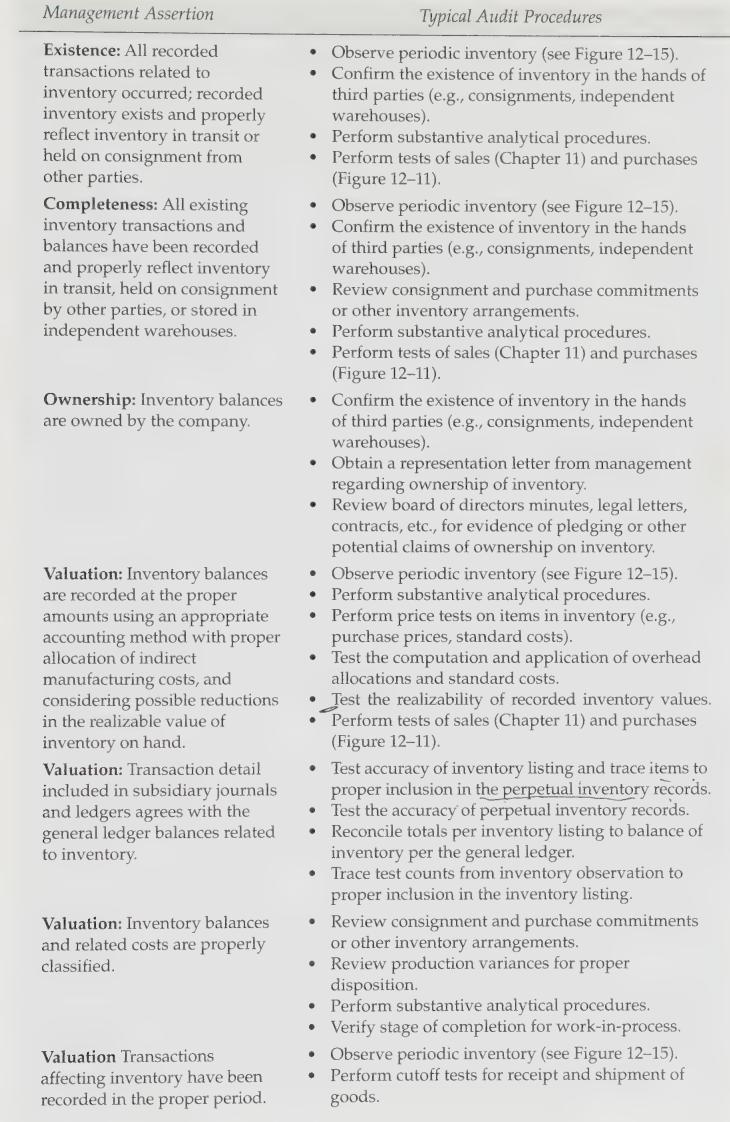

Consider Figure 12-13, where a substantive analysis of inventory turnover was performed during the audit of Jones Manufacturing Company to determine whether inventory should be written down due to obsolescence.a. Is the total proposed adjustment material? What factors go into your judgment?b. What

What key accounts and transactions are affected by the supply chain and production process? Discuss and illustrate with examples.

For each of the following internal controls in the payables department, state the management assertion that the control helps meet. Then describe a test of controls to obtain assurance that each procedure was effectively performed.a. The signature plate for the check-writing machine is kept in a

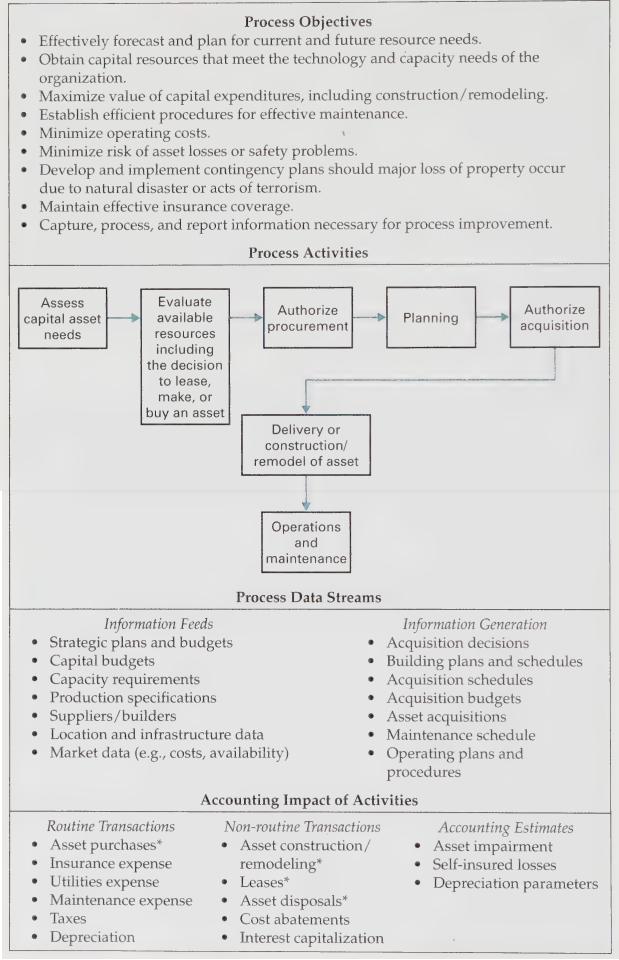

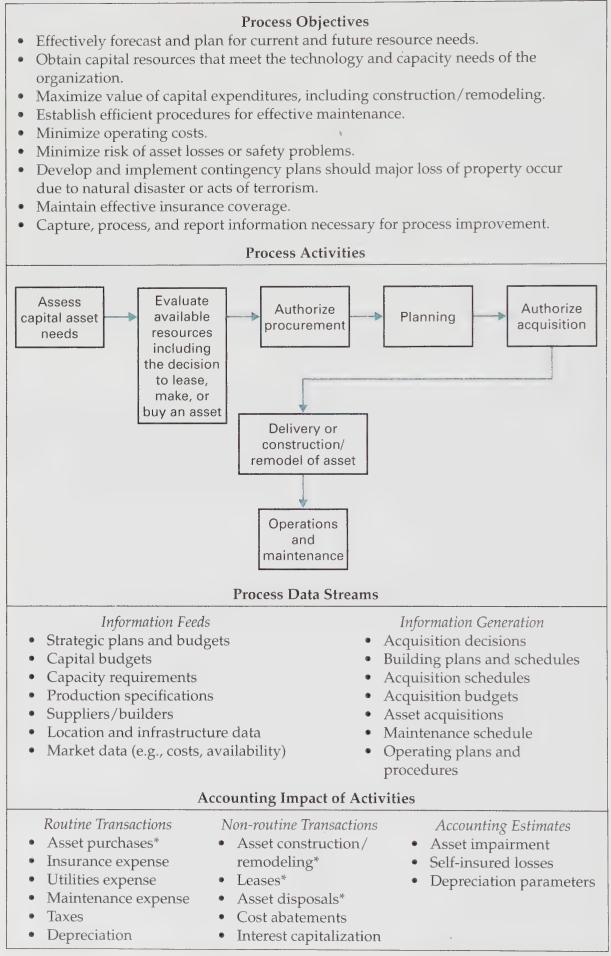

Explain how creating a process map and internal threat analysis helps in determining the extent to which substantive testing is to be performed on the accounts associated with each of the following processes:a. Human resource managementb. Property managementc. Financial resource management

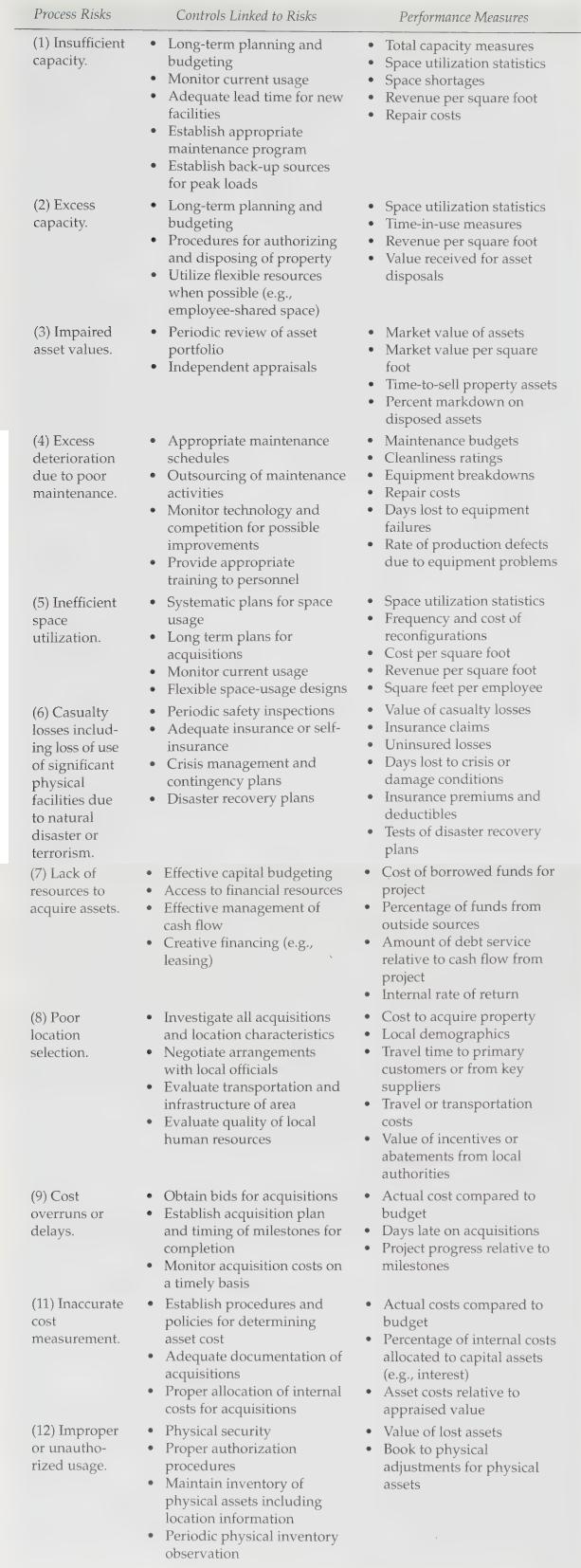

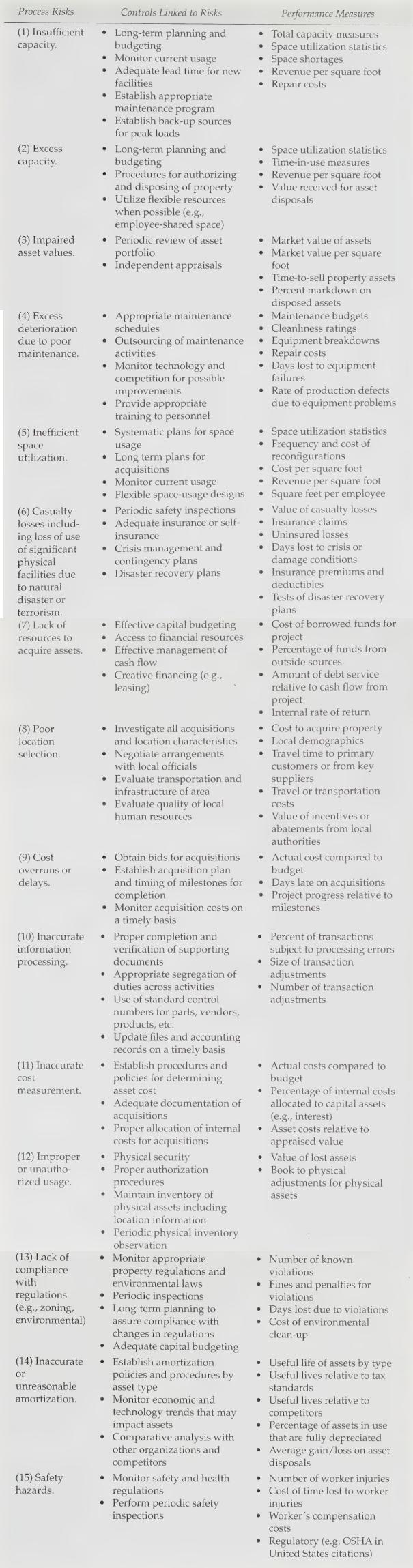

The property management process is important for gasoline retailers like Chevron. Access Chevron's web site and research the descriptions of its service stations through its learning center link. Use this information and Figures 13-2 and 13-3 to create an internal threat analysis for Chevron's

Examine the process activities and transactions for the property management process shown in Figure 13-2.a. Using the example transactions listed in the same figure, describe which transactions or estimates are impacted by the different activities listed in the process.b. Describe which accounts

Site selection and property development is an important property management subprocess for many organizations. Consider The Home Depot, which opened at least 100 stores per year for more than 15 years consecutively, making it the fastest growing retailer in U.S. history. Its growth rate is

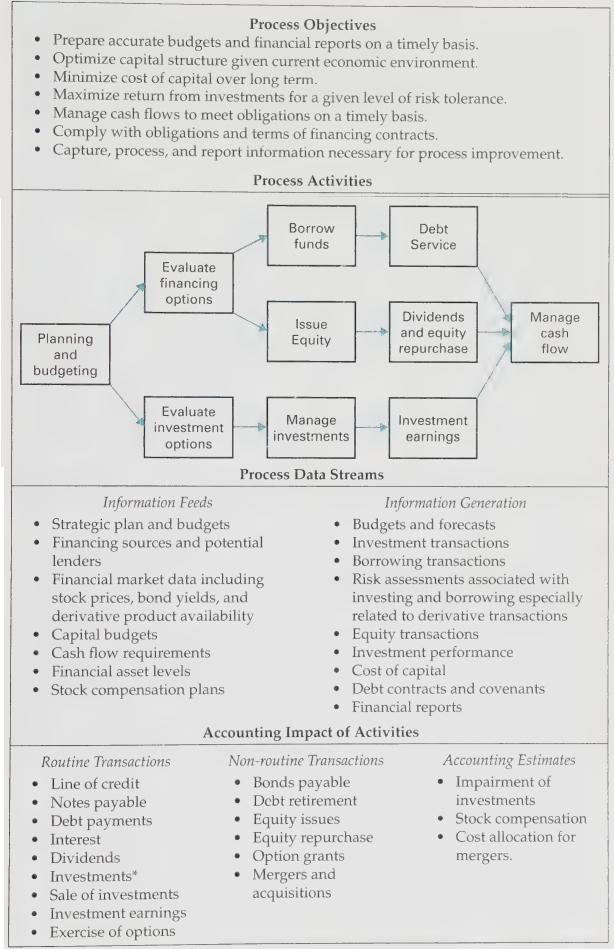

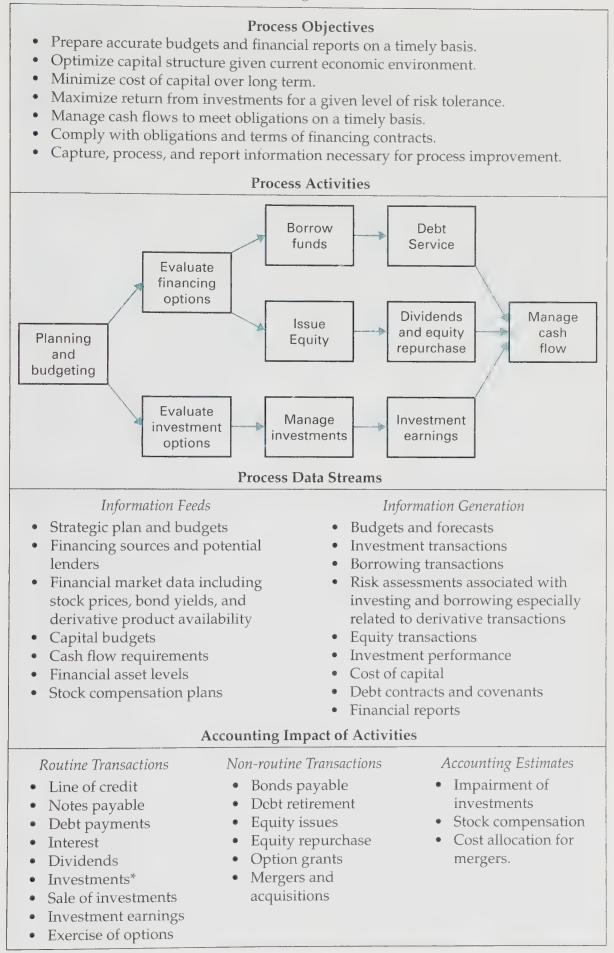

Examine the process activities and transactions for the financial management process shown in Figure 13-6.a. Using the example transactions listed in the same figure, describe which transactions or estimates are impacted by the different activities listed in the process.b. Describe which accounts

Consider an internal threat analysis for the property management of a food chain specializing in donuts and coffee (e.g., Dunkin' Donuts, Tim Horton's, etc.). Using Figure \(13-3\) as a guide:a. Describe the people risks, direct process risks, and indirect process risks associated with a move to

The internal threat analysis shown in Figure 13-3 contains a listing of controls linked to risks related to the property management process. For each process risk, describe the impact on the audit for each of the following results of controls testing.a. Controls are found to be operating

Organizations often will utilize third parties to perform their resource management processes. For example, organizations can utilize investment banks to perform financial asset management to conduct many of the activities shown in Figure 13-6. Access Credit Suisse's web site and research the

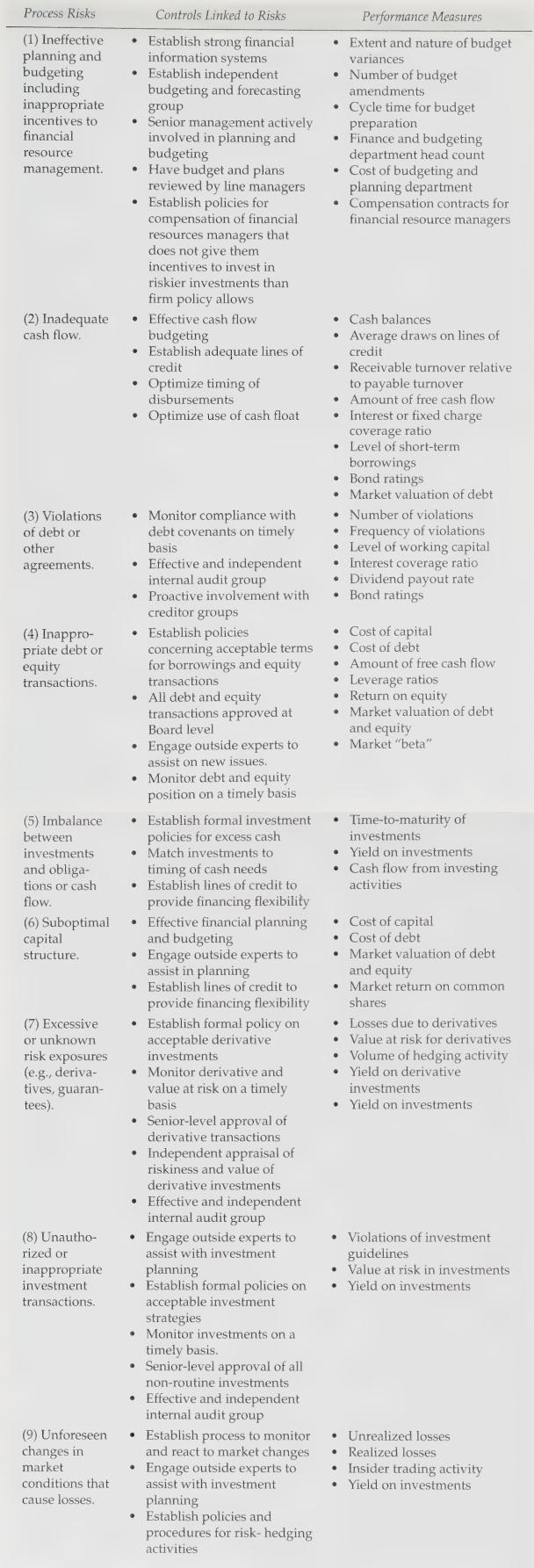

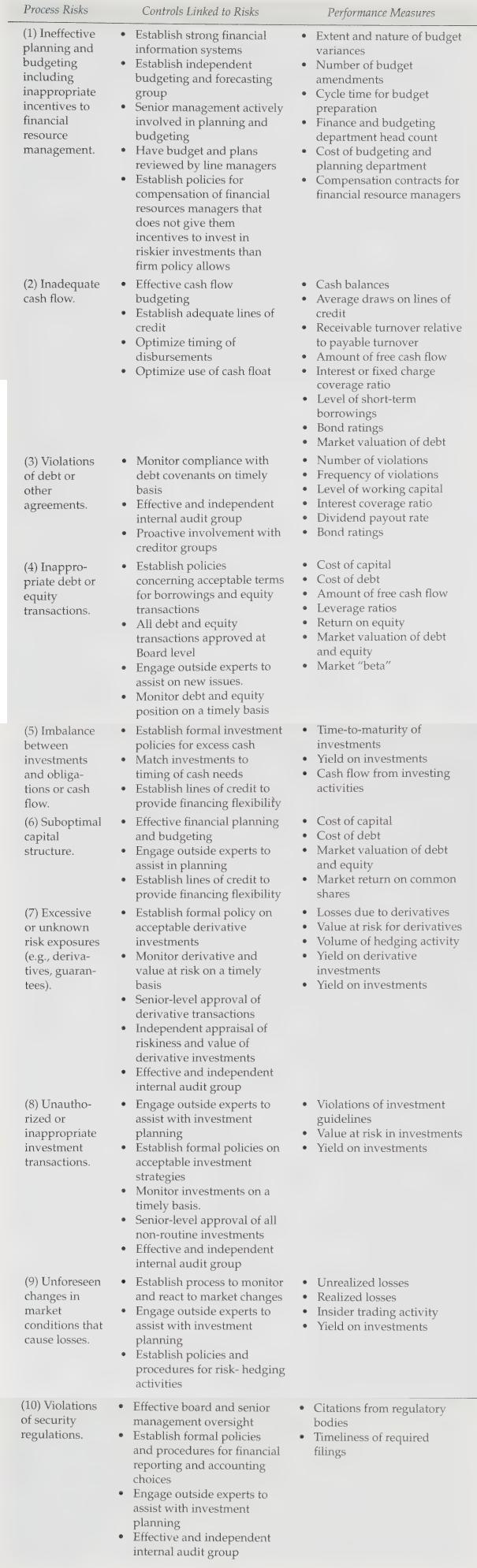

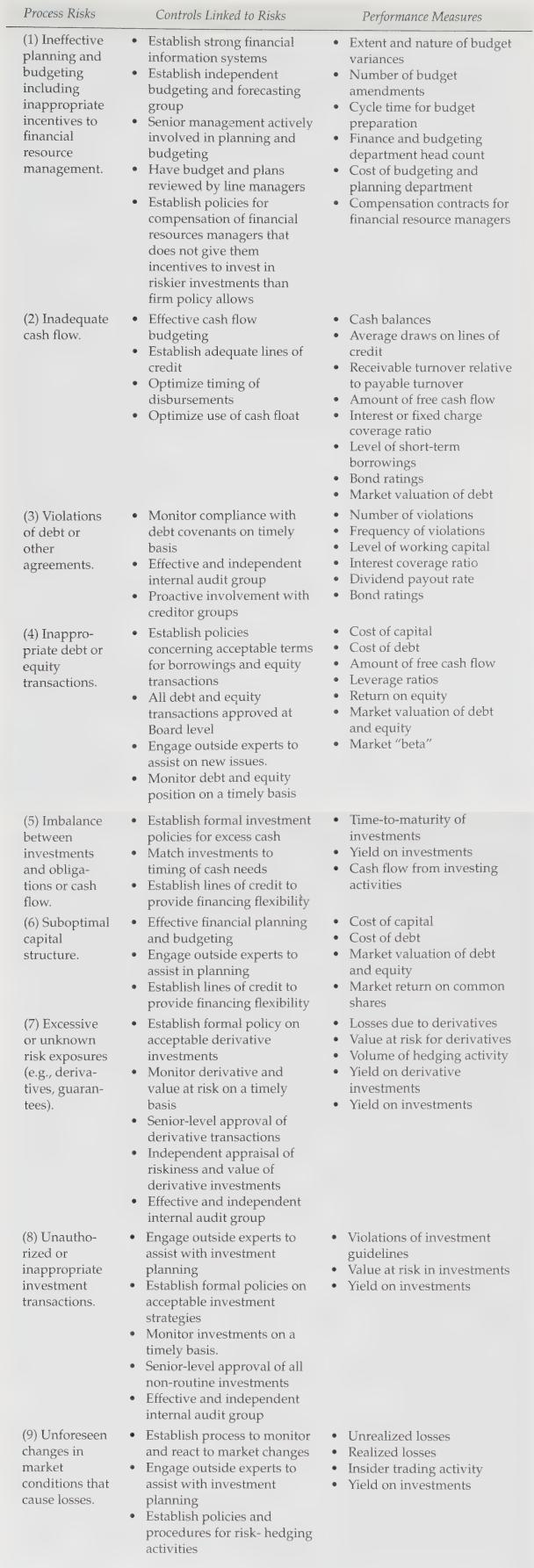

The internal threat analysis shown in Figure 13-7 contains a listing of controls linked to risks related to the financial resource management process. For each process risk, describe the impact on the audit for each of the following results of controls testing.a. Controls are found to be operating

Consider an internal threat analysis for the loan management process for the commercial bank segment of a large financial banking institution (e.g., Bank of America, Deutsche Bank, etc.). Using Figure 13-7 as a guide:a. Describe the people risks, direct process risks, and indirect process risks

The financial management process is important for auditors because of its role in helping to form expectations about financial statement results. To illustrate this concept, explain how an understanding of the controls and performance measures in place to manage the following risks impacts

Following are some routine procedures for the audit of payroll (discussed in the Appendix). For each procedure, (1) state whether it is a test of controls or a substantive test, (2) state which management assertion the procedure is designed to fulfill, and (3) state the type of evidence used in the

After an analysis of the borrowed funds portion of the financial management process, an auditor might choose not to perform many tests of controls but will instead concentrate on substantive tests of account balance details.a. What unique characteristics of borrowed funds motivate an auditor to

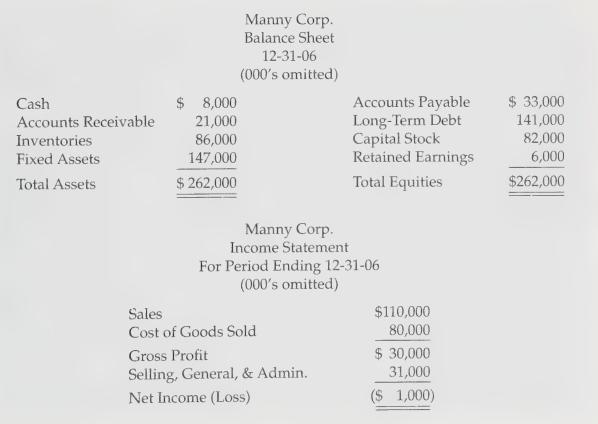

Consider Manny Corp., our military outfitting operation from Chapter 10.Its financial data is reprinted here for convenience.a. If you were the auditor assigned to perform substantive analytical procedures on expenses, describe the management assertions you would be hoping to support and for which

Based on this chapter and the result of answering the previous questions, offer an explanation for why performing a detailed analysis of resource management is an important part of the auditing engagement. As part of your answer, provide several specific examples for when failing to properly

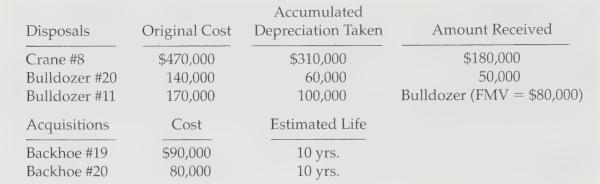

The controller of Mingus \& Mingus Inc., a construction company, provides you with the following schedule of additions and disposals to fixed assets for the past year:The following account balances were obtained from the financial statements from last year and the trial balance (unaudited) from

The disclosure objective for the equity portion of the audit is said to be critical. Examine the partial balance sheet of Barron Co., a large, diversified financial services firm with 22,000 employees worldwide:a. What are the deficiencies in this disclosure?b. What further disclosures should be

Consider the following information gathered by several auditors on the same engagement team performing an audit of the financial statements of a home improvement center.Suppose the audit team gathered the following subtantive evidence when testing existence and valuation account:- Of the 100 new

Aggregating audit evidence across business processes is an important auditing issue that has received relatively little emphasis by auditing standard setters and auditing researchers (other than to consider total misstatements identified). Describe what you believe are the most imporant benefits

Consider the following financial statement line items reported from three subsidiary locations of a manufacturer:Assume the following exchange rates:1 U.S. dollar \(=0.57\) British pounds 1 U.S. dollar \(=1.15\) Canadian dollars 1 British pound \(=2.016\) Canadian dollars Explain the audit issues

Consider the following analytical procedures performed as of the end of the audit:Suppose the working papers include a summary document indicating that - Sales have increased because of an increase in sales price.- Ten new employees were added to the production line.- A new storage facility was

Why should auditors be diligent in ensuring that different business segments' financial statements properly reconcile to the consolidated financial statements? As part of your answer, describe reasons why errors might occur in this activity and why management would choose this aspect of financial

Final analytical review is required by auditing standards for all auditing engagements and, in practice, generally is performed by the partner on the engagement. What is the purpose of conducting a general analytical review of this nature? What are the limitations associated with this type of

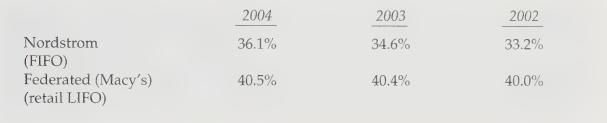

Consider the department store example provided in the chapter regarding gross margin percentages under different inventory methods:How might an auditor approach developing a pro forma version of this data to enable a comparison between both retailers? 2004 2003 2002 Nordstrom 36.1% 34.6% 33.2%

What is meant by business measurement analysis as described in this chapter? How should the auditor perform such an analysis? If performed properly, why should it help address the limitations associated with general analytical review performed by a partner at the end of an engagement?

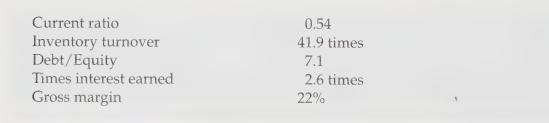

Financial performance measures have traditionally been used to assess the reasonableness of the overall financial statements. Financial ratios and comparisons with other organizations in the same industry have been heavily used for this purpose. List financial ratios and financial metrics that can

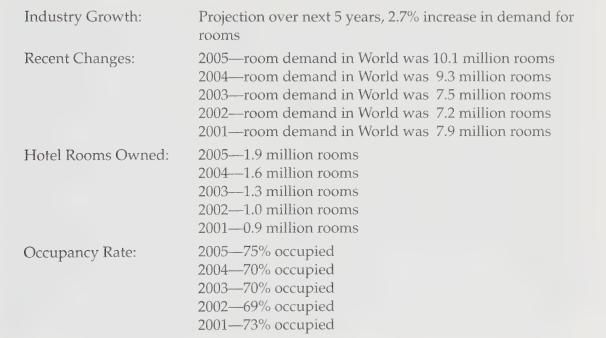

Consider the following information about an international luxury hotel chain:Based on this information, what are some general, relative expectations that can be inferred from this information for 2003, 2004, and 2005 for revenues, operating costs, and depreciation? Furthermore, given that there has

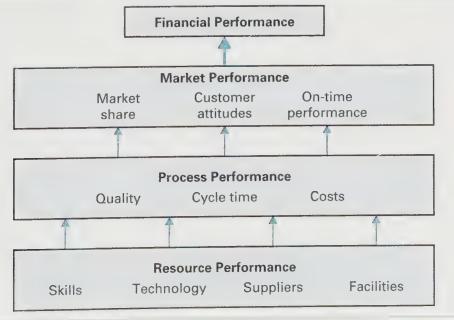

The Balanced Scorecard is a business measurement tool that enables an auditor to better understand whether financial measures reported by an organization are consistent with measures about the organization's market, core processes, and resource management processes. Assume that you are auditing

This chapter argues that nonfinancial measures are useful in assessing whether reported financial results are reasonable. Offer an explanation for why this argument should be valid for most auditing engagements and provide conditions under which it might not be valid.

Describe what is meant by a balanced scorecard approach for business measurement analysis. As part of your explanation, describe each of the four perspectives utilized in this chapter (see Figure 14-2). How can an auditor use this approach to help assess the overall reasonableness of the financial

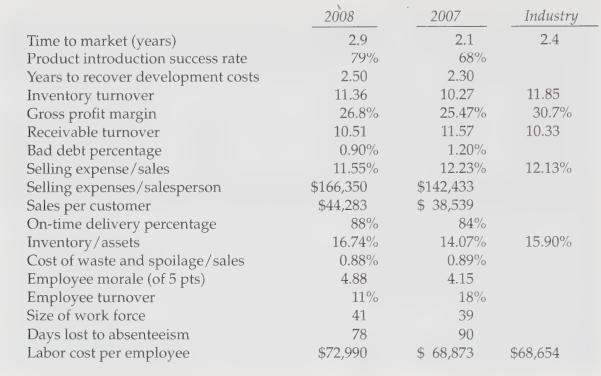

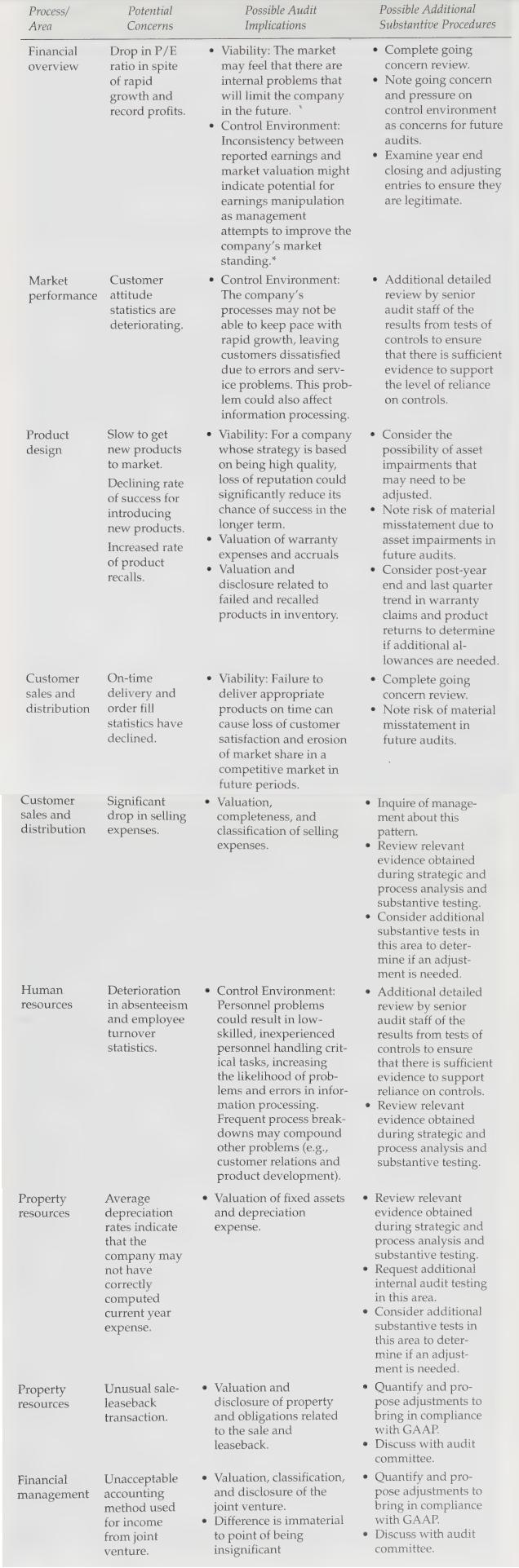

Consider the following measures taken from product design and development, customer sales and service, production management, and human resource management business processes for the manufacturer of parts for the appliance industry:Based on this information, what concerns do you have for each of

As part of the audit evidence aggregation process, auditors should consider the relationship across business processes performance. Describe how an auditor could assess the overall reasonableness of reported financial performance by considering business process performance for the following

The Altman Z-score predicts bankruptcy using commonly available financial accounting information (e.g., EBIT and total assets). Suppose you are studying a company (whose primary business is produce wholesaling) for purposes of making the going concern determination and its Altman Z-score comes to

Why do you believe that auditors must assess the risk of an organization being able to continue as a going concern, given that auditors perform no other procedures regarding future performance of an organization? Do you believe that auditors should have to perform this assessment and inform users

This chapter uses the Balanced Scorecard as an mechansim for conducting business measurement analysis. An increasingly used approach for tracking performance measurement is the use of dashboard software. Conduct research on the use of dashboards for tracking and reporting on performance measurement

Describe signals of financial distress offered in the chapter for assessing asset composition, debt levels, cost structure, and equity levels. What are the strengths and weaknesses associated with these signals?

Contingent liabilities often are one of the most serious issues for an auditor to audit because a single contingent liability can be highly material. Further, clients are hesitant to establish accruals or make related disclosures about contingent liabilities. Thus, assessing attorney confirmations

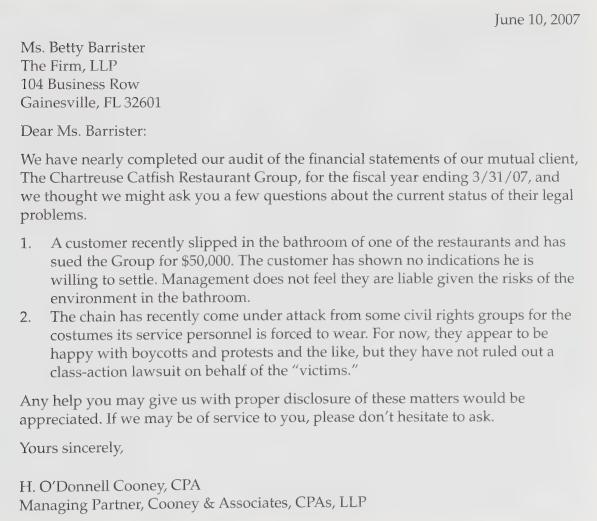

Consider the following letter from the managing partner of Cooney \& Associates, CPAs, to the legal counsel for their client, The Chartreuse Catfish Restaurant Group, requesting information on potential contingent liabilities:Describe all the elements of this letter that make it unsatisfactory

Determining whether a subsequent event requires an adjustment to the financial statements is difficult in many circumstances. Discuss the primary difference between subsequent events that require adjustment and those that only require disclsoure. As part of your explanation, include examples of

For each of the following events concerning disclosure of events that took place after year end, discuss the manner in which it should be disclosed in the financial statements or the audit report. Assume that all items are material.a. Shortly after the audit report has been issued, your client

Argue whether you agree or not that a representation letter is a critical part of an audit engagement. Consider in your argument that the letter itself can only serve as minimal evidence because it is an inquiry, but also that auditors have been known to resign when a letter has not been properly

Each of the following techniques for managing earnings was described in the chapter:- "Big Bath" charges- Write-off of acquired assets- "Cookie Jar" reserves- Abuse of materiality- Questionable revenue recognition For each of the following examples of earnings management, state which technique is

Many auditors rely on a disclosure checklist when evaluating presentation and disclosure assertions. Describe the benefits of using a checklist to help in performing this evaluation. In addition, describe the drawbacks to using a checklist and your suggestions for overcoming such drawbacks.

For each of the following scenarios, indicate whether earnings quality is likely to be high, moderate, or low. Based on your assessment, how might an auditor adjust the nature or extent of audit testing, including investigations into possible earnings manipulation?a. A drug manufacturer has

Describe the difference between a known and a likely misstatement. As part of your explanation, describe the roles of each of the following:- Materiality- Degree of objectivity- Impact on financial statements- Implications for overall audit risk Also, under what conditions would the auditor

For each of the following situations that require an audit report: (1) determine what type of audit report is called for and (2) for reports other than standard unqualified, state where in the audit report changes would have to be made and make the changes. Be specific.a. The accountant merely

Describe how a client with high quality of earnings likely should appear under each of the following circumstances:- Correlation with underlying economic activity- Permanence and sustainability- Relationship with market valuation- Extent and impact of discretionary accruals- Transparency and

Public accounting firms and regulators have long been concerned with the notion of the "expectations gap," which describes an accounting firm's understanding of the assertions provided in an auditor's report compared to the users' understanding of those assertions. Consider the form and content of

A study of the Los Angeles police department by management consultants (as reported in The Wall Street Journal, June 11, 1996) uncovered numerous practices that tended to decrease the efficiency and effectiveness of the force. Among the practices the report criticized and the costs it estimated

In your audit of the Strangelove Group, a privately-held company based in Great Britain, you encountered the following situations:a. The internal control plans in the payables processing area are poorly designed or are not well executed. However, your audit of the area failed to turn up any

Auditors typically are not responsible for evaluating the performance of an organization or its prospects for future performance; however, they are required to include an explanatory paragraph when they believe that there is substantial doubt regarding the ability of an organization to continue as

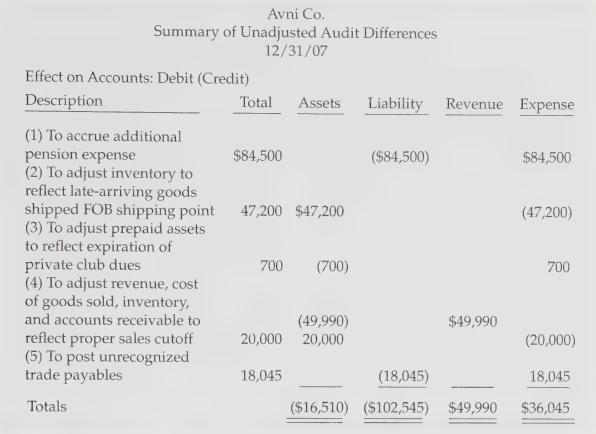

Consider the following summary of unadjusted audit differences for Avni Co., a privately-held importer of fine wines with total assets of \(\$ 1.5\) million.a. Which items do you think management will accept without much argument? Why?b. Which items do you think management will be less willing to

In practice, auditors who are unable to convince clients to adjust for known or likely misstatements often resign from an engagement instead of issuing a qualified or adverse opinion. Argue for or against this practice as being acceptable given the duty of the auditor to serve the public's best

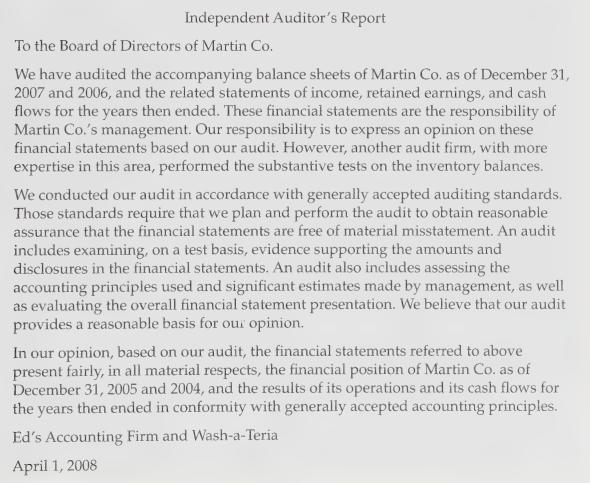

Consider the following auditor's report that refers to a shared engagement of a privatelyheld organization:Discuss the deficiencies with this audit report. Independent Auditor's Report To the Board of Directors of Martin Co. We have audited the accompanying balance sheets of Martin Co. as of

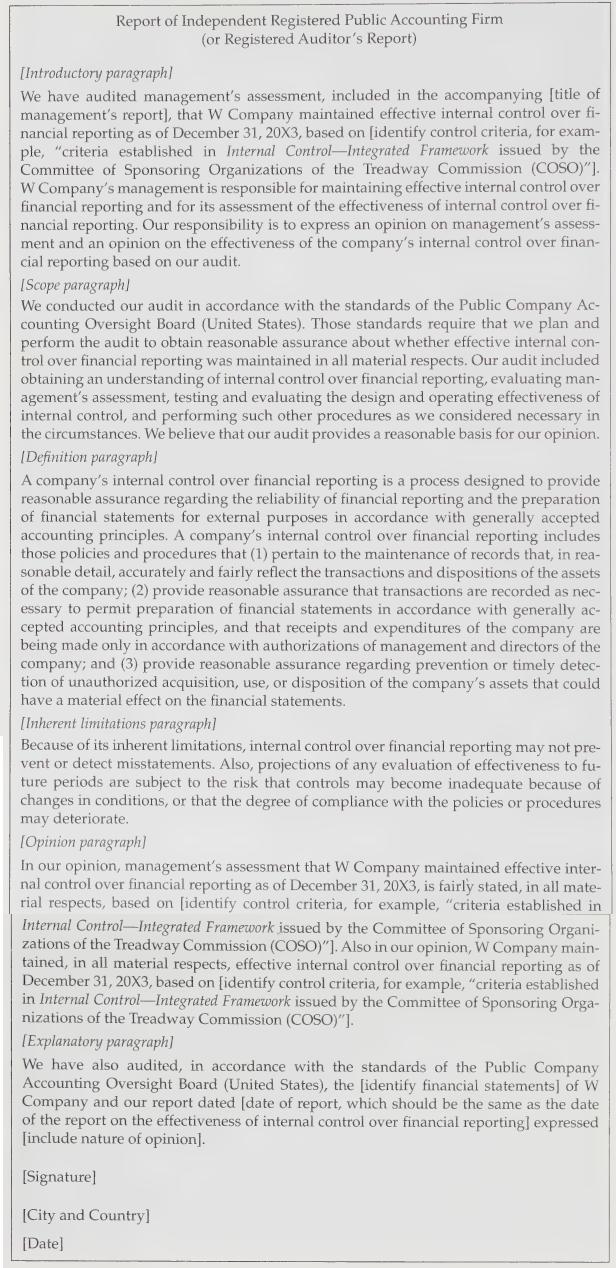

Compare and contrast the reporting requirements for the presence of a significant deficiency and material weakness under an integrated audit under AS 2.Why, in your opinion, do these reporting differences exist?

For each of the following situations, indicate which type of audit report you would issue if you were the partner in charge of the engagement and explain why.a. Although the audit of Coltrane Enterprises occurred without incident and you are prepared to issue an unqualified opinion, you discover

Sampling risk is the probability that a misstatement exists in the population but is not selected in an auditor's sample. Non-sampling risk is the probability that a misstatement exists in an auditor's sample, but the auditor fails to identify it. Do you believe that either of these scenarios can

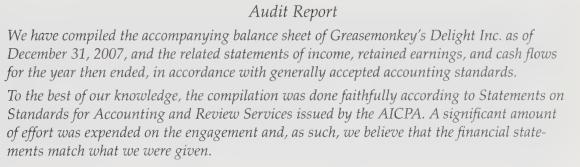

You are the senior partner of a large, local audit firm. In reviewing the work of a junior staff member on a compilation engagement for Greasemonkey's Delight Inc., a local autoparts store (in which your brother-in-law is the CFO), you notice that she has written the following rough draft for an

You have been assigned to audit the accounts payable of Slamtastic, a small recording company specializing in alternative music. Following is a portion of their accounts payable journal for the month of December:Generate a sample of eight transactions under the following sampling methods using the

Compare and contrast statistical and non-statistical (judgmental) sampling. Include in your discussion conditions that might make one approach to sampling more desirable than the other.

Consider the data from the previous problem. For each of the sampling methods named:a. Compute the total amount of the transactions sampled and the proportion of the cumulative total the sample represents.b. Discuss the advantages and risks of each sampling method assuming that it would be applied

The chapter discussed three issues to consider when obtaining evidence using a sample-based audit procedure:a. The number of transactions or items to examineb. The actual transactions or items to examinec. Interpreting the results of the sample Discuss the how the presence of a misstatement couuld

For each of the five sampling techniques commonly used by auditors, discuss an audit test using the sampling technique that should enable to auditor to conduct an effective and efficient audit test.- Random sampling- Systematic sampling- Block sampling- Haphazard sampling- Judgmental sampling

Suppose you are the audit manager on the audit of a large computer peripherals Internet business and you are attempting to test the controls of its processes. Members of the audit staff have brought you samples of the following items:a. Credit approvals from a file cabinet drawer in the credit

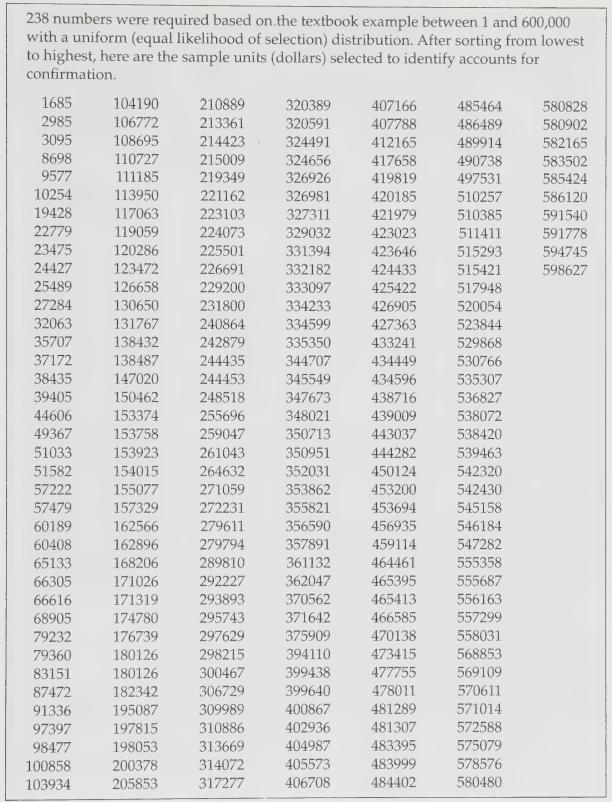

Suppose that an auditor chooses to use a random sampling technique to test additions to fixed assets for the fiscal year for manufacturing company. Walk through the key steps the auditor should consider to make sure that the random sample audited is representative of the population of fixed asset

In your audit of the accounts payable function of Gorgon Inc., you notice the following:a. Several checks do not bear the appropriate signature for the nature or amount of the payment.b. The prices paid on the invoice do not match those on the purchase order on several transactions.c. Due to delays

Suppose that an auditor is interested in stratifying a sample of accounts receivable customers and then using a judgmental sampling approach. Suggest a strategy for stratifying the sample of accounts receivable so that the judgmental sampling approach will result in an effective means for testing

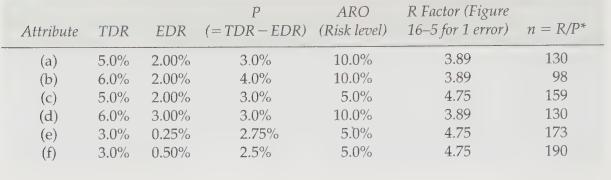

For the sample size calculation described in Figure 16-4, explain the following statements:a. The required sample sizes are larger (all else held equal) the lower the tolerable deviation rate (TDR).b. The required sample sizes are larger the lower the acceptable risk of overreliance (ARO).c. The

Consider the formula for selecting a sample size when performing attribute sampling:\[ n=R / P \]where: \(n=\) sample size\(R=\) Risk factor based on ARO and the expected number of errors\(P=T D R-E D R\)Explain why this formula should be effective for determing a sufficient sample size to enable

You are auditing the sales order processing department at Joe Henderson \& Co., a highend book publisher. You are attempting to determine whether you can rely on the control procedure that stipulates that all sales invoices will bear the prices from a master price list.a. Find the sample size

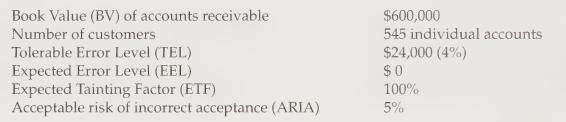

Consider the example provided in the chapter for selecting a sample for dollar unit sampling application, where sample size is computed as\(n=\frac{\mathrm{BV}^{*} \mathrm{R} * \mathrm{ETF}}{(\mathrm{TEL}-\mathrm{EEL})}\)Where:and:\[ n=\left(B V^{*} \mathrm{R}^{*} \mathrm{ETF}\right)

You are conducting dollar unit sampling (DUS) of the accounts receivable balances of an agricultural co-op. You are willing to accept a 5 percent risk of incorrect acceptance, the book value of the account is \(\$ 2,500,000\) and your sample size (based on a tolerable error limit of \(\$ 125,000\),

Compare and contrast the implications of deviations found when testing process controls and misstatements found when performing substantive tests. Include in your discussion the rationale behind the implications of finding sample deviation rates and sample misstatements.

Regarding the facts in problem 8 :a. If your tolerable error limit (TEL) is \(\$ 250,000\) (10 percent of the account balance), are you satisfied that accounts receivable are fairly stated? Why or why not?b. If your tolerable error limit (TEL) is \(\$ 175,000\) (7 percent of the account balance),

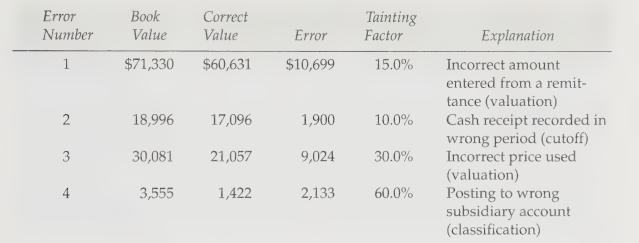

Consider the following findings from the test of accounts receivable using DUS:An auditor determines that the most likely error based on a sample is 4 percent of the total accounts receivable balance. By projecting the 4 percent error rate on the entire population, the UEL is \(\$ 3\) million.

Typically, sampling for tests of transactions occur when the client stores transaction files from which the auditor selects a sample. For some automated systems (e.g., electronic data interchange, point-of-sales systems), clients do not save transaction data beyond a month or so (or the transaction

For each of the common errors in sampling provided below, describe steps that the auditor can take to avoid the errors whenever possible.- Sample size is too small given reliance placed on the sample results- Misuse of decision aids- Influence of irrelevant transaction attributes- Failure to

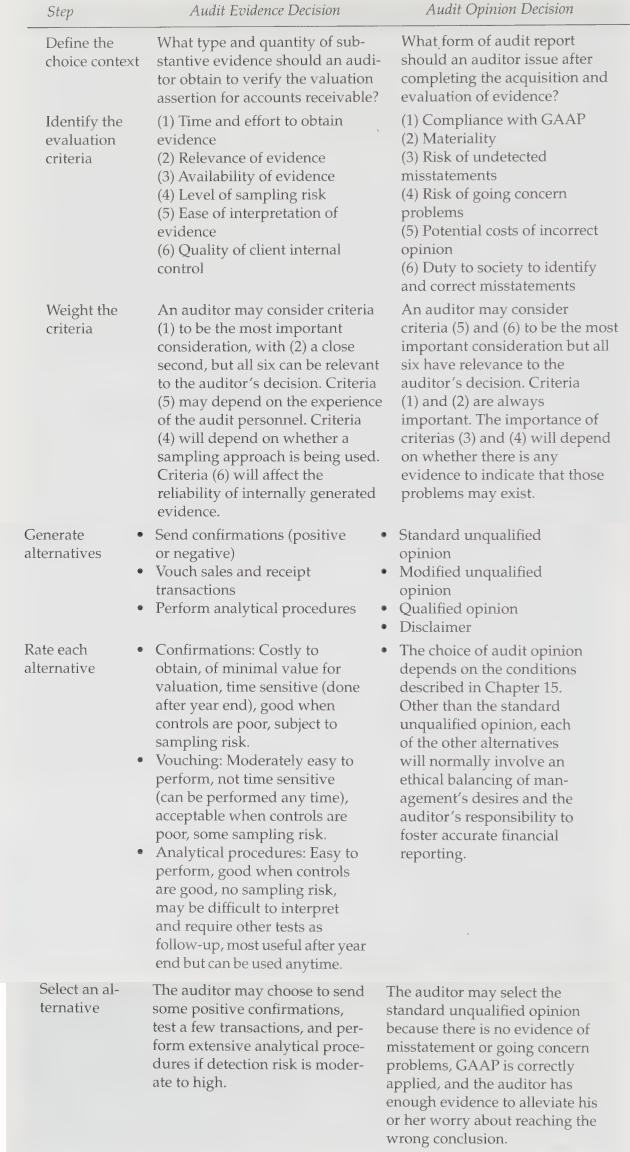

For each of the following routine audit decisions, use Figure \(17-2\) as a guide and apply each step of the decision process to the audit decision.a. The business process that will require the most attention/resources for a retail clothing chainb. The type of specialists to employ on an audit of a

For each of the following audit judgments, provide one example of a behavior that you believe would be unethical.- Client acceptance- Establishing materiality- Evaluating the effectiveness of controls- Evaluating client explanations- Selecting audit procedures

Consider the following example of ethical misconduct:An audit staff member is asked to work extra hours on an engagement and not report the hours worked so that the engagement will report being completed within the budgeted amount of time. The manager who asked the staff to work the hours is trying

Although the use of heuristics may lead to biased audit decisions in some cases, all humans make use of them. However, it is important to recognize when an auditor is employing a heuristic so that he or she can be cognizant of the biases and can minimize their effect on decision making.For each of

Consider each of the five examples provided in the chapter for why auditors might demonstrate mistakes in professional judgment:- Auditors may not be able to define their decision problem clearly- Auditors may not be able to consider all relevant evidence and alternatives- Auditors may act in a

Auditors employ numerous methods to alleviate the potential biases that may result from the use of judgment heuristics. These include- Improving expertise- Debiasing techniques- Framing and perspective- Group decision making and review- Justification- Decision aids Examine each of the following

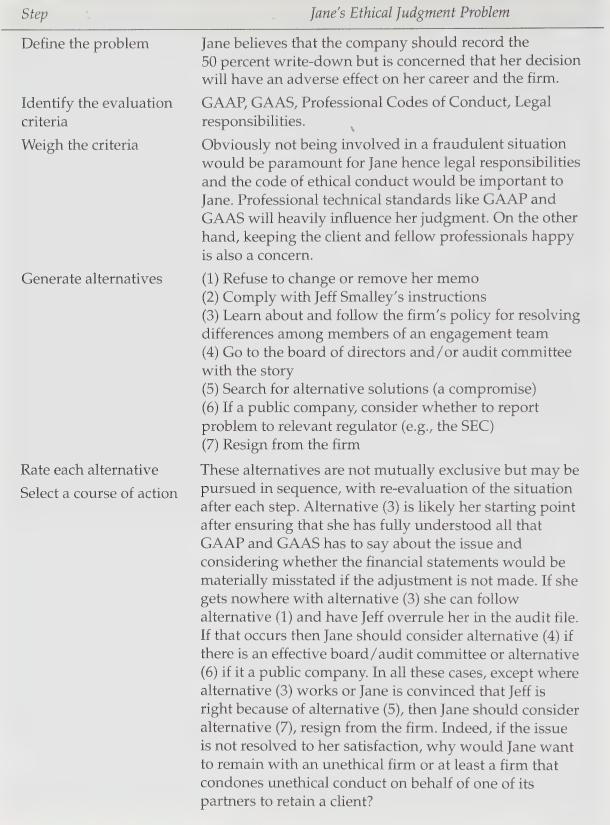

Audit decisions sometimes come down to a trade-off between satisfying one set of stakeholders at the expense of others. In the example in Figure 17-4 and 17-5, an auditor is forced to choose between making her superiors and the client happy or doing what she feels is appropriate to the goal of an

Evidence from audit research shows that the anchoring and adjustment heuristic occurs when auditors begin their audit of a financial statement account assertions by first obtaining the unaudited ending balances from the client's management. Consider the following example of this situation.The

Below are common techniques generally used by an audit firm to reduce the chance that ethical dilemmas will result in auditors making poor decisions. For each technique, describe how you think that it might help you avoid making an unethical decision at your employer.- Expertise in a subject area-

Answer each of the following independent questions, based on your understanding of the AICPA Code of Professional Conduct or IFAC Code of Ethics for Professional ACcountants. Cite support for your answer.a. May an auditor refer business to a client in exchange for commissions?b. Under what

Compare and contrast the concepts of independence in fact and independence in appearance. Explain why you agree or disagree with the notion that independence in appearance is equally as important as independence in fact, keeping in mind that this argument has been the subject of many heated debates

Auditors typically rely on the following legal defenses when parties bring suit against them:- No responsibility to plaintiff- Lack of reliance by the plaintiff- Auditor exercise of due diligence- Lack of auditor intent to defraud- Contributory negligence by management Consider each of the

For each of the following threats to independence discussed in the chapter, provide an example of a breakdown of independence in fact or appearance to illustrate why auditors should take the threat seriously.- Self-interest threat- Self-review threat- Advocacy threat- Familiarity threat-

Five common auditor defenses when charges of negilence are brought against auditors include- No responsibility to plaintiff- Lack of reliance by the plaintiff- Auditor exercise of due diligence- Lack of auditor intent to defraud- Contributory negligence by management In actuality, most lawsuits

The U.S. SEC Acts of 1933 and 1934 established the SEC, in part, to help prevent the business practices, including financial reporting, that worsened the impact of the 1929 depression in the United States. There was not another major piece of congressional legislation to affect public accountants

Auditors must maintain both the fact and appearance of independence if they are to maintain their respected role in the business community. Consider each of the following independent situations. Using the material in the text, comment on whether the subject is within professional guidelines for

Consider the following situation. A group of investors who specialize in investing in high-technology IPOs files suit against the auditors of one of those firms when the stock loses 50 percent of its value shortly after issue. Analysts attribute the steep decline to the firm losing a major

Showing 1900 - 2000

of 2689

First

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

Step by Step Answers