New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing assurance services

Auditing Assurance And Risk 3rd Edition W. Robert Knechel, Steve Salterio, Brian Ballou - Solutions

Consider the following situation. The board of directors of a major airline promotes one of its marketing vice presidents to the position of president and CEO. Included in the compensation package is a large salary increase and a bonus based on accounting ratios such as return on equity. Before

Answer each of the following independent questions, based on your understanding of the AICPA Code of Professional Conduct or IFAC Code of Ethics for Professional Accountants. Justify your answer.a. May an auditor refer business to a client in exchange for commissions?b. May an auditor allow clients

Compare and contrast the different levels of assurance provided by assurers who conduct reviews, compilation engagements, and agreed-upon procedures engagements. As part of your answer, describe why an organization would opt to hire assurers to provide each type of service.

Assertions are amenable to attestation when the measures used to make them are objective and the data to support the assertion are available. In that light, consider the following assertions:a. Nine out of ten dentists recommend Bleegum toothpaste.b. Cholesterol is the leading cause of heart

Why do you believe that the SEC requires that quarterly financial statements be issued and subject to a review? Describe the procedures that an auditor performs when conducting a review of interim financial statements. Describe the risks that investors take when relying on information contained in

In reviewing the interim financial statements of Lady Day Enterprises, a publicly traded electronic components wholesaler, your audit firm (which also conducts the annual audit) performs the following procedures:- Analytical procedures on the overall reasonableness of most of the account balances

Given that a compilation does not involve providing any assurance and the auditor does not need to be independent to conduct the engagement, why do you believe that auditing standards (for example, the AICPA) prohibits the performance of management functions, such as approving journal entries?

Your audit firm has been called in to examine the financial forecasts of Martin Corp., a multinational commercial building contractor. Toward that end, your firm conducted the following procedures:- Studied the reliability of the statistical models used to predict the economic environment in the

Assume that a hotel audit client owned by a consortium of investors is not satisfied with the hotel management company that performs most of its operations. The hotel hires a public accounting firm to go to the hotel management company to perform agreedupon procedures to make sure that the hotel

As part of your audit engagement of Walter's Bank N.A., you have been asked to provide a letter assuring the Office of the Comptroller of the Currency (OCC) that the bank has maintained adequate capital and loan loss provisions against a downturn in their area's economy. Having completed the task,

Describe why you believe that many auditors are reluctant to issue reports on prospective information and financial forecasts. How do the restrictions associated with these reports help address these risks?

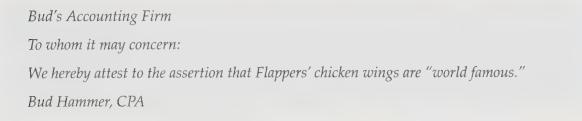

Flappers, a restaurant located in Birmingville, has hired their auditors, Bud's Accounting Firm, to attest to the following assertion: "Our chicken wings are world famous!" Bud's Accounting Firm accepted the engagement mostly because their partners believe that Flappers might use the attestation to

What are some risks and barriers associated with providing independent assurance for corporate sustainability reports? What are the possible ramifications of not providing assurance for these reports? How can auditors address the risks and barriers to avoid such ramifications?

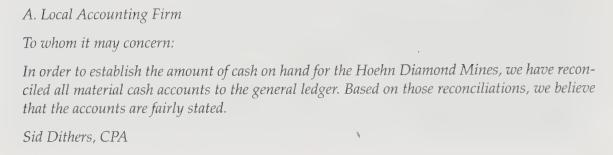

Barbara and Bill Hoehn have engaged A. Local Accounting Firm to conduct an audit of the cash accounts of their diamond mining business. The mines are not publicly owned, so a full-fledged audit is neither necessary nor desired, but the Hoehn's are concerned with the possibility that embezzlement

Compare and contrast an attestation engagement and an audit of financial statements. Provide examples of attestation engagements that are not audits of financial statements and describe how they are different.

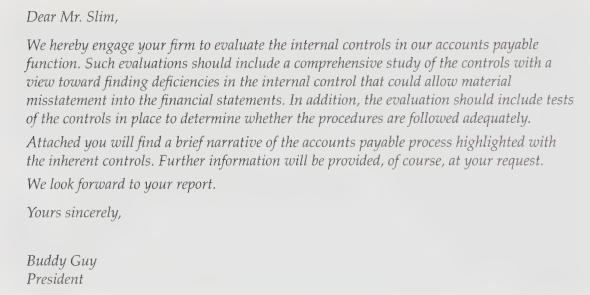

The Buddy Guy Co., a moving and storage firm with operations throughout the Midwest, has contracted with the Memphis Slim Accounting and Consulting Group to evaluate the adequacy of the controls associated with their accounts payable and to test the extent of compliance with them. Memphis Slim

Public accounting firms are sometimes called on to perform operational audits, where the operational effectiveness and efficiency of some process of an organization is studied. Consider the following independent situations where a public accounting firm might be asked to perform an operational

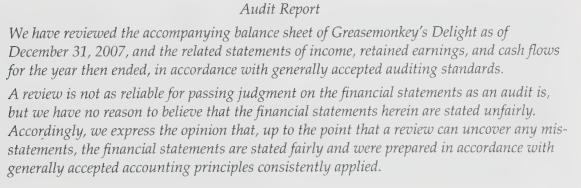

Assume the same facts as in the preceding problem except that your junior staff auditors performed a review, instead of a compilation. The rough draft of the engagement report looks like this:Discuss the deficiencies, omissions, and errors in this report. What other information would be necessary

The chapter describes five principles that are evaluated during a WebTrust \({ }^{5 M}\) engagement:- Availability- Security- Processing Integrity- Privacy- Confidentiality Suppose that you are performing a WebTrust \({ }^{S \mathrm{M}}\) engagement for the order processing system for an online

The risk model from the chapter can be restated as follows:\[ \mathrm{DR}=\frac{\mathrm{AR}}{(\mathrm{IR} \times \mathrm{CR})} \]where \(\quad \mathrm{DR}=\) detection risk\(\mathrm{IR}=\) inherent risk\(\mathrm{AR}=\) audit risk\(C R=\) control risk This representation illustrates that an

In 1999, the U.S. Securities and Exchange Commission issued SAB 99-3, which essentially established that no level of materiality is acceptable for intentional misstatements involving any registered public U.S. company (e.g., a company opts not to value its marketable securities at market (as

Explain the benefit of setting tolerable misstatement for individual accounts. Argue for or against using the same level of tolerable misstatement for each account.

Misstatements that are not corrected in a given year because they are not deemed material likely will affect the financial statements in the following year. This impact might be in the form of a reversal of the amount (i.e., an overstatement of inventory in year 0 results in an understatement in

Consider each of the qualitative considerations in setting materiality listed below. For each, describe why it could lead to users being more impacted by smaller levels of misstatements (i.e., why it could lead auditors to set materiality at lower levels).- Materially significant segments-

Three of the most important decisions that auditors make concern the nature, timing, and extent of evidence. Describe each of these decisions, carefully describing how each decision impacts the other decisions as part of your answer.

Describe how residual business process risks impact management assertions about transactions and accounts. As part of your answer, consider the risk that management fails to properly store and label perishable inventory for a grocery store.

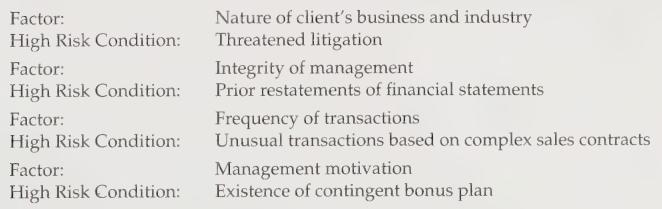

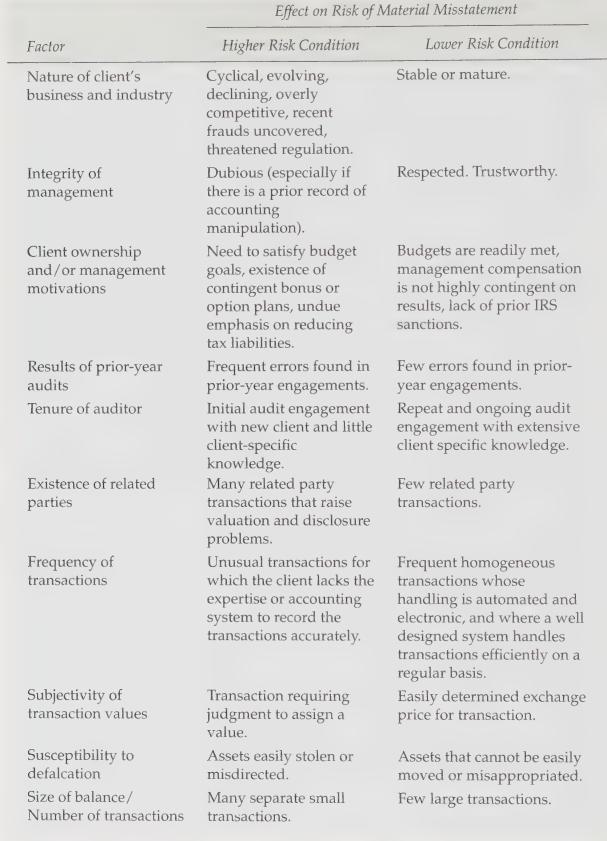

Consider the factors described in Figure 10-6 that affect the risk of assertions being materially misstated. For each of the following factors from that table, describe how the high-risk condition could impact a management assertion related to sales transactions.Figure 10-6 Factor: High Risk

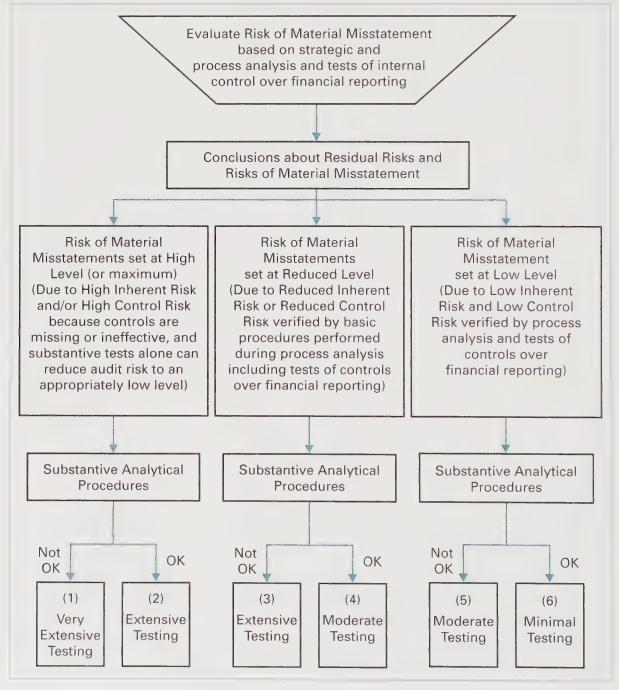

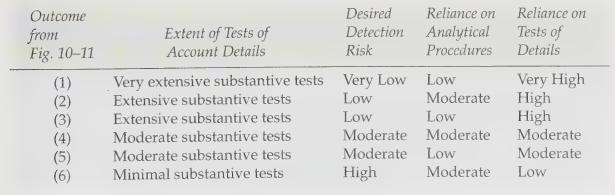

Consider the alternative audit planning strategies depicted in Figures 10-12 and 10-13 and answer each of the following questions.a. Why would a strategy of performing moderate substantive tests of details not be acceptable, regardless of the outcome of substantive analytical procedures when the

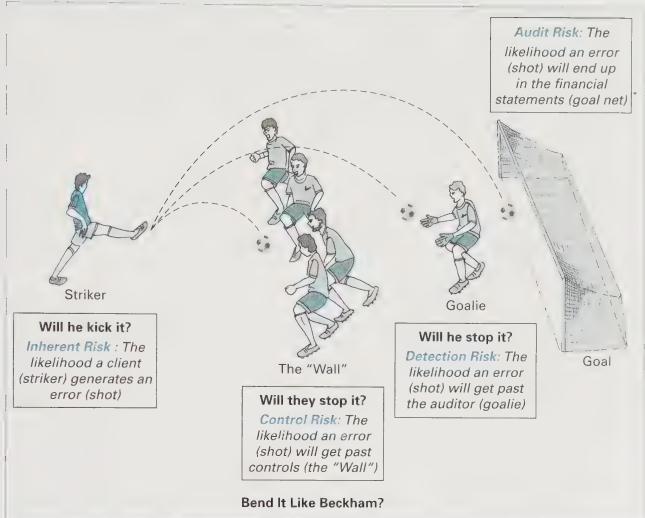

Describe how an auditor is able to achieve a given level of audit risk through different combinations of tests of controls and substantive tests. Consider the soccer/football analogy provided in Figure 10-7.Figure 10-7 Audit Risk: The likelihood an error (shot) will end up in the financial

Risk of material misstatement can be decomposed into two highly interrelated risks. Discuss these risks and indicate how they are related.

What factors should the auditor consider in setting the level of audit risk? How do these factors affect the level of audit risk?

What is materiality? Why is it an important concept for auditors to consider in the conduct of their audits?

How do auditors establish a materiality level? What factors affect the level of materiality set by the auditor?

What characteristics can be considered by the auditor to assess the appropriateness of audit evidence? Define these characteristics and illustrate each with an example.

What is an audit program? How does the auditor compose the audit program?

Using the audit risk model, compute the detection risk for the following values of audit risk, inherent risk, and control risk. Then answer the questions below.a. Which of the "points" yields the highest required detection risk? What does this imply for evidence gathering by the auditor?b. Which of

Assume that a client has materiality of \(\$ 10\) million for financial statements that has accounts receivable (net) of \(\$ 20\) million and inventory of \(\$ 80\) million.a. What amount of tolerable misstatement would you establish for accounts receivable? Justify your answer.b. What amount of

Armour Inc. has been in the defense contracting business for about 22 years. From its small factory in Wales, it manufactures boots, belts, ammo holders, and assorted accessories for foot soldiers in the British Army. Raw materials are obtained from sources around the world. Armour bids on a few

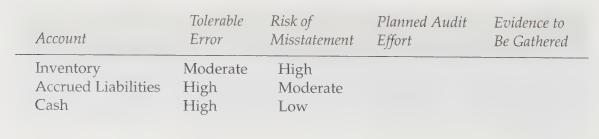

In practice, the auditor frequently sets tolerable error on individual accounts so that the sum of those errors is greater than the level of materiality for the engagement. For example, the audit manager on the Mary Sue Co. audit set tolerable error on its accounts as follows:The overall

For each of the following independent scenarios, state whether detection risk is higher or lower. If detection risk is higher, select the reason for the increase from the following four: inadequate planning, sampling omissions, non-sampling errors, or improper corrective actions.a. The auditor

For each of the following situations, discuss the competence of the evidence gathered to support the assertion being audited. Where possible, suggest a more competent procedure. Why might your suggested procedure not be performed?a. In her audit of the cash balances of a very large wholesaler, an

Consider the following three independent scenarios:a. Chieftain's, Inc.: A chain of finer men's clothing shops with locations in malls throughout the country.b. Sunnystuff Inc.: A bottler of juice-based beverages and teas.c. Sarah Co.: A manufacturer of high-tech hospital equipment (e.g., MRI

McGuffin Corp. is a manufacturer of aircraft parts for government-owned and commercial planes. The company's government contracts are usually performed on a "cost-plus" basis whereas its private contracts are competitively bid for a fixed amount. During your annual audit of the company's financial

In planning the audit of Tralfaz Co., a manufacturer of animal feeds and fertilizers, a staff member prepares the following audit program for the substantive test of the accounts receivable balance:a. For each step in the audit program identify - The audit objective(s) being addressed - The type of

Assume that materiality was set for Barclay's Bank at 5 percent of net income. Research Barclay's Bank and describe qualitative reasons for why an auditor of Barclay's might assess materiality lower than this amount.

Explain how creating a process map and internal threat analysis helps in determining the extent to which substantive testing is to be performed on the accounts associated with the marketing, sales, and distribution process.

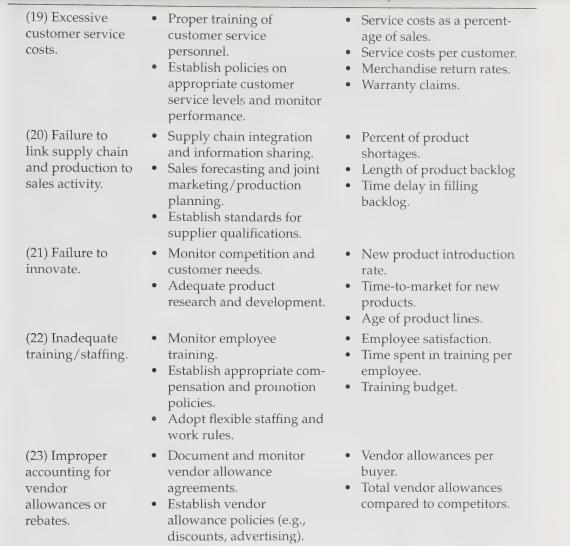

One of the most common forms of fraudulent financial reporting is recording sales that never occurred. Examine the examples of financial reporting controls for sales-related transactions in Figure 11-5. Identify relevant controls that can be used to help prevent or detect fraudulent sales from

Reconciliation is an important control for helping to test the management assertions of completeness, occurrence, and accuracy of cash receipts transactions. Describe how a reconciliation helps test all three assertions for cash receipts.

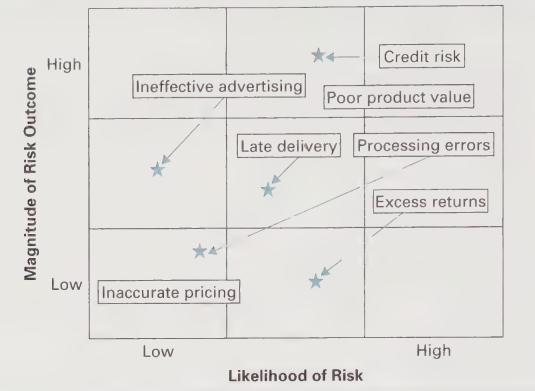

Examine the inherent risk, impact of controls, and residual risk plots in Figure 11-6 for the sales and customer service process. Based on this plot, what conclusions should an auditor reach for each of the risks regarding whether to test controls and the extent to which substantive testing should

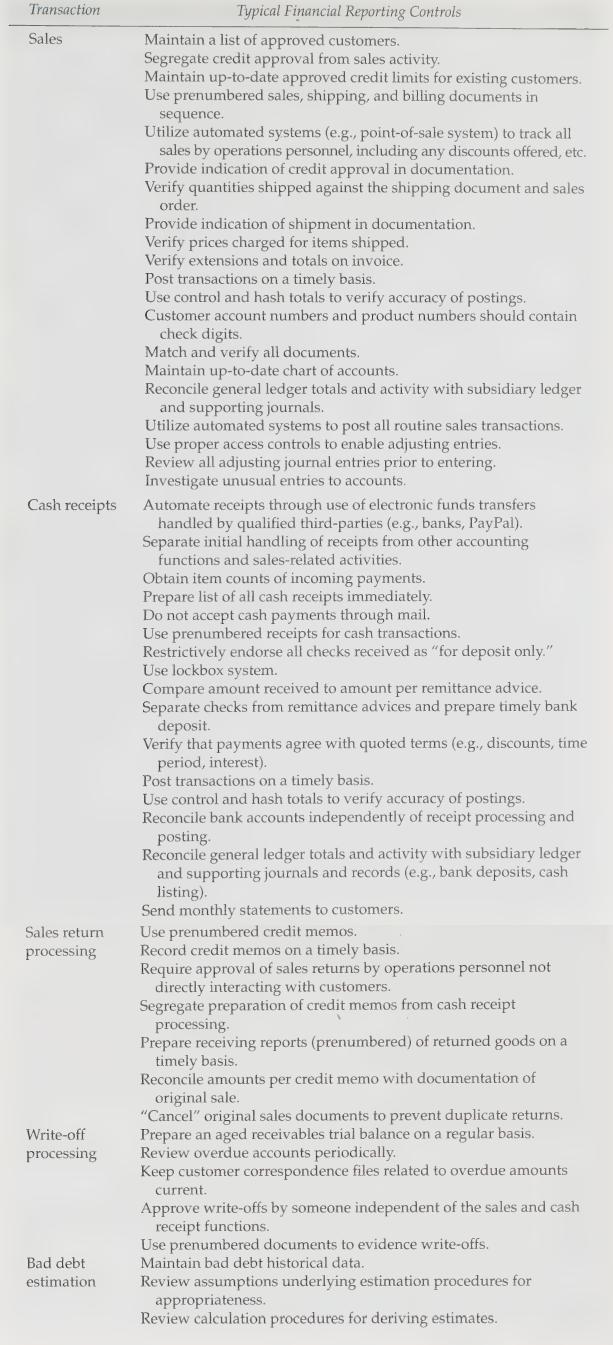

Figure 11-7 contains a listing of tests of operating effectiveness for internal controls related to the sales and customer service process. For each type of control activity (performance reviews and overall process management, information processing controls, physical controls, and segregation of

Among the tools the auditor may employ to determine the reasonableness of the sales amount for a company during a given accounting period is regression analysis, whereby the company's sales are predicted using various economic factors such as interest rates and unemployment.a. Discuss the

Discuss the utility of using confirmations to test the valuation of accounts receivable. Assuming that the auditor has decided to employ confirmations, discuss the possible ways the auditor may use them (i.e., positive vs. negative, to whom they should be sent, and so on). How should the auditor

Many organizations are moving to automated processes for performing the sales and customer service process, using such processes as electronic data interchange, in which order placing, product tracking, invoicing, and collecting activities occurring electronically through systems connecting the

Evidence gathering procedures for the cash account have been de-emphasized by many auditors in recent years. As described in Appendix 11A, there is a large volume of transactions that flow through the account. Describe whether you believe that this reduction in emphasis is appropriate and defend

Audit documentation, described in detail in Appendix 11B, has received attention during the past several years, with standards being issued emphasizing its importance by international standards setters (including the IAASB and PCAOB). Describe the role that audit documentation plays for the auditor

What process objectives and activities typically are associated with the sales and customer service process? Why is understanding them important for the auditor?

What key accounts and transactions are affected by the sales and customer service process? Discuss and illustrate with examples.

As part of his or her internal threat analysis of the sales and customer services process, the auditor will pay special attention to internal control over financial reporting. In the context of the sales and customer service process, what controls specifically relate to financial reporting and will

For each of the following process activities for sales and customer service, discuss management assertions related to transactions or accounts that are impacted by the specific activity:a. Marketing and brand awarenessb. Customer approvalc. Customer service order entryd. Sales order entrye.

For each of the following internal controls in the sales order processing function, state the management assertion related to sales and receipts transactions that the control helps meet. Then list a test that would give the auditor assurance that the control procedure was effectively performed.a.

Examine the following questions from an internal control questionnaire for the sales process of a large home improvement retailer that extends credit to small contractors. Assume that the answer to each of these is "no" (which means that the control is weak in that area). For each of the following

The following are routine procedures for the audit of revenue processes. For each procedure, state whether it is a test of controls or a substantive test of transactions, state which management assertion the procedure is designed to fulfill, and state the type of evidence used in the procedure.a.

High-tech manufacturers are notorious for practicing "channel stuffing," whereby they ship to their distributors a great deal of merchandise shortly before the end of the accounting period, knowing full well that most of it will be returned-but not until after the beginning of the new accounting

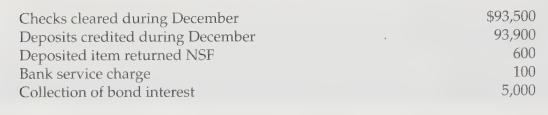

Your assignment as an auditor is to reconcile the general disburseinent account at the Green Dolphin Bank for Monk, Miles, and Trane Co. as of 12-31-06. Your analysis of its cash activity for the month of December 2006 is as follows:In addition, your study of the 12-31-06 bank statement yields the

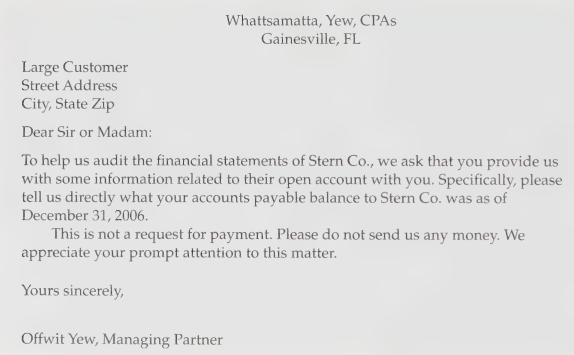

In preparation for your audit of the accounts receivable of Stern Co., you compose a confirmation letter to send to several of their largest customers. Your effort looks like the following:Discuss the deficiencies in this confirmation. Then discuss alternative ways it can be written. Large Customer

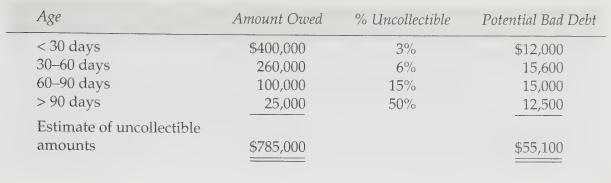

In your audit of the allowance for uncollectible accounts for Patrick Co., a wholesaler of hospital supplies, you prepare the following aging schedule:a. What type of audit evidence is this schedule?b. If the beginning balance in allowance for uncollectible accounts was \(\$ 51,000\), what amount

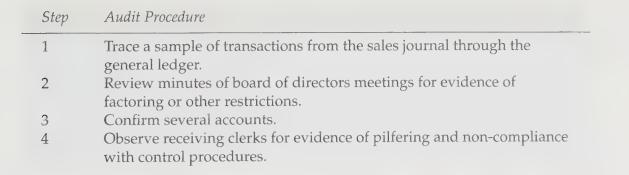

Discuss the deficiencies in the following audit program for the tests of controls over the sales order process of Skylark, a cable TV home shopping channel. Working Paper Step Reference 1 2 3 5 6 9. 7 00 Audit Procedure Observe telephone operators for compliance with control procedures related to

Distinguish between internal controls and internal controls over financial reporting, Under what circumstances does this distinction matter for auditors?

Distinguish between each of the following types of controls and given an example of each that makes the difference clear.a. Management controlsb. Business process controlsc. Monitoring controlsd. Financial reporting controls

Distinguish between the following management assertions about transactions and give an example of each that makes the difference clear.a. Classification vs. Accuracyb. Occurrence vs. Completenessc. Occurrence vs. Accuracyd. Occurrence vs. Cutoff

For each of the four components of a financial reporting process, provide an example for how a control weakness within that component could result in materially misstated financial statements.a. Source documents and transactionsb. Journalsc. General and subsidiary ledgersd. Trial balances

For each of the four components of a financial reporting process, discuss how information technology can be used to reduce the likelihood or impact of a material misstatement. Also, describe how using information technology could increase the likelihood or impact of a material misstatement without

Compare and contrast the merits and drawbacks associated with the requirement for U.S. registered companies and auditors to perform assessments of the effectiveness of internal control over financial reporting. Conclude by arguing either for this requirement to be discontinued for U.S. registered

Define a walkthrough. As part of the definition, describe how the procedure is used to develop an understanding of internal control over financial reporting. Also, describe the conditions, if any, under which a walkthrough can serve as a test of operating effectiveness of a control for purposes of

Why is the assessment of control risk a critical part of any financial statement audit? What is the impact on an auditor's financial statement audit strategy if control risk is set at a high level versus being set at a low level? What is the impact on the financial statement audit if an auditor

Compare and contrast a material weakness discovered during an assessment of internal control over financial reporting for a U.S. registered public company and a reportable condition identified during any other type of audit engagement. As part of the comparison, describe whether there can be

What are compensating controls? When would an auditor need to identify compensating controls, and how can the auditor determine whether they serve their intended purpose? For example, what would be possible compensating controls for not having separate personnel collect cash from customers and

The chapter emphasizes accounting informations systems in ensuring internal control over financial reporting. What is the role of financial reporting personnel in internal control over financial reporting?

What is a control deficiency in an integrated audit (i.e., an audit that includes opinions related to ICOFR)? What are the three categories of control deficiencies? How does the presence of these deficiencies affect auditor testing of financial statement assertions?

Suppose that as an audit staff associate of an accounting firm, you are asked to perform a complete walkthough of two financial reporting processes at a retailer that specializes in selling athletic equipment for winter sports (e.g., skis, hockey equipment, ice skating apparel). For each of the

In its first Assessment of Internal Control over Financial Reporting (for the fiscal year ended December 31, 2004), General Electric identified a material weakness in internal control and concluded that its internal control over financial reporting was not effective as of that date. General

As an audit manager, you have been given charge of assessing risk management for two business processes of The Solas Co., a privately owned wholesaler of textbooks (hence not subject to PCAOB AS 2).The first process, sales collection, processes high-volume payments from many small, independent

For each of the following, state the financial reporting process control activity that is being followed and which management assertion for associated transactions is strengthened if a company actually performs it.a. Only certain employees are allowed into the central computer room. Those employees

In preparing to conduct the audit of the O'Farrell Corp, a manufacturer of fine Irish apparel, you have prepared the following narrative description of the process internal controls over financial reporting related to the materials acquisition process. The narrative is based on conversations with

You are analyzing the control plans of a new client, McGriff Co., a publicly traded U.S. airline specializing in long-distance cargo shipping. Its receivables processing business subprocess is your special concern as its operations affect such a large part of their financial statements. In

USBB, an Australian property and casualty insurer, actively seeks to maintain a paperless office. Toward that end, it has invested in optical character recognition scanning technology so that incoming paperwork (e.g., an insurance application) can be immediately scanned into an electronic file.

Consider the following control weaknesses revealed by your tests of controls on a publicly held U.S. mail-order computer peripheral retailing company.a. Clerks do not compare daily sales orders to credit limits until after the day's business has been transacted and the orders shipped.b. Warehouse

Consider the following situations for each of the privately owned organizations independently. For each situation, identify the risk exposures and any possible controls.a. In your observation of the payables posting function of 'a construction firm, you notice that a payables clerk prepares a

Consider the following independent assessments of the level of control risk for a class of transactions the following publicly traded U.S. companies.a. The control plans for the accounts payable function of a real estate management firm are very poorly conceived.b. The deferred tax accounting

Explain the following internal control procedures classified under "Independent Verifications." Give an example where a newspaper subscription processing department might use each of them.a. Key verificationb. Check digitsc. Reconciliationsd. Batch controlse. Control totalsf. Customer

Why do you believe that auditors traditionally have been required to perform preliminary analytical procedures? What role does these procedures help achieve in the risk assessment process?

Inquiry has long been considered one of the most controversial forms of audit evidence. Describe the strengths for the audit if an auditor effectively utilizes inquiry as a key source of audit evidence. Also, describe the weaknesses associated with that strategy and discuss how an auditor can

Three considerations provided in the chapter when conducting inquiries include- Being clear to the interviewer and the interviewee as to what is to be discussed- Staying on topic unless follow-up is needed or important tangential issues arise in the conversation- Respecting the interviewee's

The chapter discusses the need to compare and contrast answers to inquires made across different aspects of the audit (e.g., this discussion can occur during engagement brainstorming sessions). For example, why might operations personnel provide different answers than accounting personnel to

Consider each of the basic judgmental methods for obtaining analytical evidence:- Comparative financial statement analysis- Common-size financial statement analysis- Ratio analysis Describe strengths of using these methods for gathering analytical methods and the limitations associated with using

Describe the strengths and weaknesses associated with using nonfinancial performance measures. How can auditors ensure that they are properly utilizing nonfinancial performance measures as analytical evidence? As part of you answer, illustrate your suggestion using an example nonfinancial measure

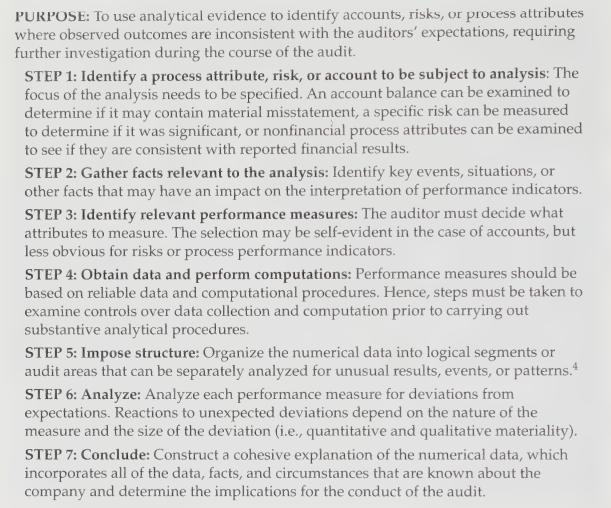

Use the systematic process for conducting analytical procedures provided in Figure \(9-8\) to design an approach for developing an expectation for the commissions expense account for an electronics retailer that pays its employees based in part on preestablished commission rates.Figure 9-8 PURPOSE:

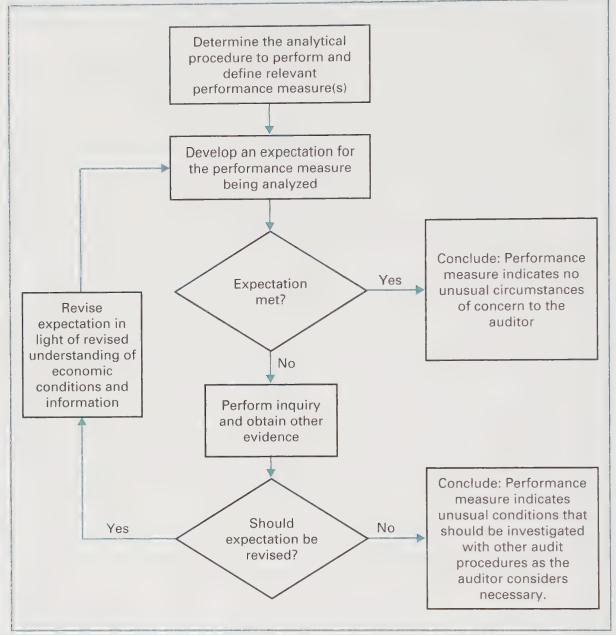

Developing expectations independent of the client is critical for effective use of analyti\(\mathrm{cal}\) evidence. Figure 9-9 presents a process for evaluating analytical evidence. Examine the figure and apply it to an example situation in which an auditor develops an expectation that the

Regression can help the auditor develop fairly precise expectations for financial reporting. However, auditors should use regression carefully. For example, consider the following scenario:The relationship depicted in the model is not valid; rather, the relationship in the model exists because a

When using regression, interpreting the output is very important for carefully using the results as analytical evidence. Discuss each of the following regression terms and describe how they can be used to evaluate regression results as analytical evidence for the auditor:- Correlation coefficient-

Showing 2000 - 2100

of 2689

First

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

Step by Step Answers