New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

corporate accounting

Corporate Accounting 1st Edition Anita Raman, P. Radhika - Solutions

Payment of purchase consideration can be in the form of: (a). Shares (b). Debentures (c). Cash (d). All of the above

True and False. The difference has to be credited to goodwill A/c, when the value of net assets is less than the purchase price.

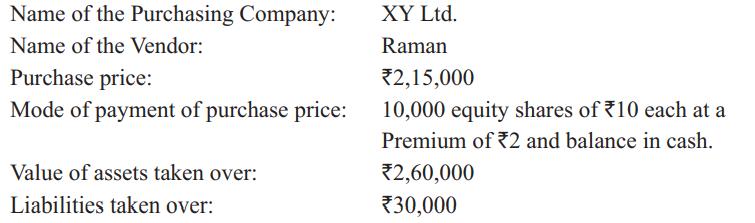

Pass journal entries to record the following transactions in the books of XY Ltd. Name of the Purchasing Company: Name of the Vendor: Purchase price: Mode of payment of purchase price: Value of assets taken over: Liabilities taken over: XY Ltd. Raman *2,15,000 10,000 equity shares of 10 each at

All ____________ liabilities are taken over by the purchasing company.

What is vendor’s suspense A/c?

True and False. Profit on acquisition has to be credited to capital reserve A/c.

The selling company is called as ____________ company in the acquisition of a business.

C Ltd. does not want to take over debtors and creditors of vendor. However, it agreed to collect from debtors and pay to creditors for a commission of 4% on amount collected and 2% on amount paid. The debtors realized ₹1,90,000 only, out of which ₹60,000 was paid to creditors. Calculate the

The excess of net assets over the purchase consideration is called as:(a). Goodwill (b). Net Loss (c). Capital Reserve (d). Balance in Suspense A/c

True and False. Interest account is debited when the interest is paid on purchase price.

When the value of net assets is less than the purchase price, the difference is debited to ____________ A/c.

A Ltd. agreed to collect the debts and pay the creditors on behalf of Senthil from whom the company had acquired a running business. The firm’s debtors and creditors totaled ₹1,50,000 and ₹50,000 respectively. The debtors realized ₹1,48,300 only and the creditors were paid ₹42,000 in full

When the debtors and creditors are taken over by the purchasing company on behalf of: vendors, then the purchasing company opens an A/c called as:(a). Debtor’s Suspense A/c (b). Creditor’s Suspense A/c (c). (a) and (b) (d). Vendor’s suspense A/c

True and False. The vendor company pay commission to the purchasing company for realising book debts and making payment to the creditors.

When the value of net assets is more than the purchase price, the difference is credited to ____________ A/c.

AK Ltd. purchased the business of Anish Kanth & Brothers and decided to continue the same set of books. The company decided to make the following revaluations:(a). Buildings to be appreciated by ₹1,20,000. (b). Plant & Machinery to be depreciated by ₹14,000. (c). Stocks to be

Any profit or loss arising on account of realising book debts and discharging creditors will be borne by: (a). The purchasing company (b). The vendor (c). (a) and (b) (d). None of these

True and False. The purchasing company has to bear any profit or loss that arises in collecting debts and paying creditors.

When the purchasing company takes over debtors and creditors on behalf of the vendor’s then, ____________ A/c has to be opened.

Shalini Ltd. purchased the business of Mr. Venkat. Shalini Ltd. did not take over the debtors and creditors of Mr. Venkat amounted to ₹65,000 and ₹40,000 respectively, but it promised to collect from debtors and pay to creditors. Shalini Ltd. collected ₹61,500 from debtors and paid all

Capital Reserve A/c is credited with the difference amount: (a). When the value of net assets is less than the purchase price (b). When the value of net assets is greater than the purchase price (c). (a) and (b) (d). None of the above

True and False. Realisation account has to be opened when the same set of books is continued by the purchasing company.

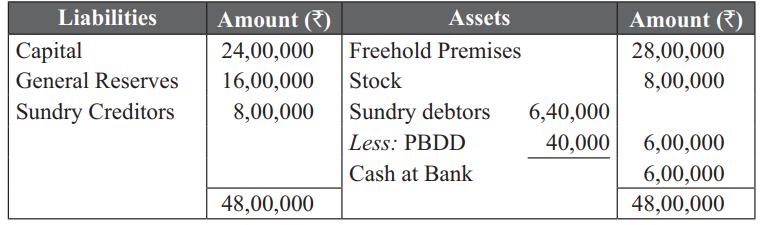

Ashish Ltd. was formed with an authorised capital of ₹48,00,000, divided into equity shares of ₹10 each, to acquire the business of Mr. Gupta, whose balance sheet on the date of acquisition was as follows:The purchase consideration was agreed upon at ₹56,00,000 to be paid in

When the same set of books is continued, a separate account for debtors should be opened under the ____________ A/c.

When the purchasing company maintains the same set of books, then the amount realised from the proceeds of assets taken over by the partners will be distributed in the ratio of:(a). Profit-sharing (b). Capitals (c). 1:1 (d). Final claim

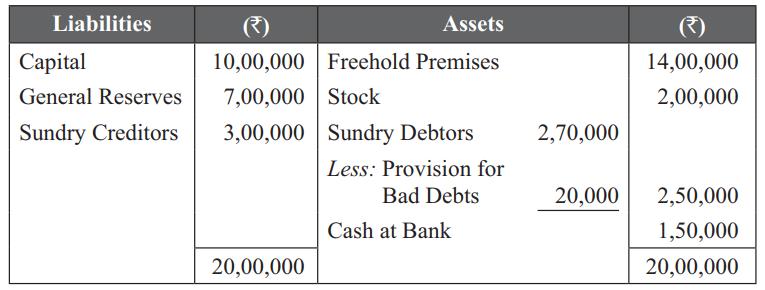

Swami Ltd. was formed with an authorised capital of ₹20,00,000, divided into equity shares of ₹10 each, to acquired the business of P&M, whose balance sheet on the date of acquisition was as follows:The purchase price was agreed upon at ₹23,00,000, to be paid in ₹20,00,000 fully-paid

True and False. When discount is received from vendor’s creditors, then it will be credited to Vendor’s suspense account.

When shares of debentures are issued at a premium, ____________ A/c has to be credited with premium amount.

Karan Limited purchases the business of Mr. Karthick. Karan Limited did not take over the debtors and creditors of Mr. Karthick, amounting to ₹25,000 and ₹15,000 respectively, but it promised to collect from debtors and pay to creditors. Karan Limited collected all debtors at a discount of

True or False. Those debentures, which are repaid before other debentures are paid out, are known as first debentures.

Zebra Ltd., redeemed ₹10,000 12% Debentures, out of capital by drawing a lot and it has also redeemed ₹20,000. 10% Debentures out of profit by drawing a lot. Journalise the transactions.

TTK Ltd. redeemed 4,000 15% Debentures of ₹100 each which were issued at a discount of 5% by converting them into equity shares of ₹10 each issued at a premium of 25%. Journalise the transactions.

Explain the accounting treatment of Premium on Redemption of Debenture.

The balance of sinking fund investment account, after the realisation of investment, is transferred to:(a). Profit & Loss A/c (b). Debentures A/c (c). Sinking Fund A/c (d). None of the above

Profit on sale of sinking fund investment is to be credited to ______________ account.

True or False. When debenture are repaid out of capital, entry for the transfer of profits to debentures redemption reserve account is passed in the books.

Babu Ltd., redeemed ₹2,88,000 15% Debentures of ₹100 each at 102% by converting them into 16% Debentures at 96%. Journalise the transactions.

After redemption of debentures, the balance in the sinking fund account is transferred to:(a). Debenture development reserve.(b). General reserve (c). Profit & Loss A/c.(d). Shares forfeited A/c.

A company issued at par 1,000 6% debentures of ₹1,000 each. Interest is payable half yearly on 30th September and 31st March.On 01.02.1983, the company purchased 20 of its own debentures as investment at ₹970. Give the necessary journal entries, assuming the books are closed on 31st March.

KK Ltd. has ₹2,00,000 6% debentures outstanding on 31st March 2007. The company redeemed the debentures on that date out of capital. Pass the necessary journal entry.

Write short notes on Redemption of Debentures out of Capital.

Amount needed after 5 years for debenture redemption: ₹60,00,000. Rate of Interest on investments expected: 5% Annual investment needed to get 15 after 5 years, *2.71462. Ascertain the annual transfer to Sinking Fund.

SS Ltd. purchased its 200 10% own debentures in the open market at ₹99 exinterest on 1.7.99. Later, these debentures were resold on 1.1.2000 at ₹98 exinterest. Interest is payable on 31st March and 30th September each year. Show journal entries for purchase and resale of own debentures.

AB Ltd. has ₹5,00,000, 9% debentures outstanding on 1st January 2006. The company has been redeeming every year on 1st January ₹1,00,000 debentures by drawings by lot, at par. Pass necessary journal entries: (a). If the redemption is out of profits. (b). If the redemption is out of

AXE Co. Ltd. issued ₹4,00,000, 10% debentures of ₹100 each, at a discount of 5%, which are repayable after 10 years, at a premium of 15%. Pass journal entry for the issue.

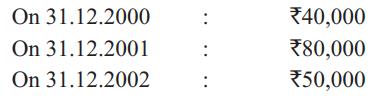

On 1st January 2000, Exe Ltd. issued ₹2,20,000, 9% debentures at a discount of 5% repayable as follows:Calculate the amount of discount to be written off in each of the three years. On 31.12.2000 On 31.12.2001 On 31.12.2002 : : *40,000 *80,000 *50,000

Pass journal entries for the following transactions: (a). Issue of debenture at a discount and redeemable at par.(b). Issue of debenture at a premium and redeemable at par. (c). Issue of debenture at par and redeemable at premium. (d). Issue of debenture at a discount and redeemable

Anil Ltd. issued 5,000, 5% debenture of ₹100 each, at a premium of 10%, payable ₹30 on application and balance with premium on allotment. Pass journal entries in the books of Anil Ltd.

A company authorised ₹2,20,000 debenture holders to convert their debentures into preference shares. Pass necessary journal entry, if.(a). Debentures were converted into 10% preference shares of ₹100 each at par. (b). Debentures were converted into 10% preference shares of ₹100 each at

Gowtham Ltd. issued 6,000 12% debentures of ₹100 each, at a discount of 5%, repayable after 5 years at a premium of 5%. Give journal entries both at the time of issue and redemption of debentures.

Amount needed after 5 years for debenture redemption: ₹60,00,000.Rate of interest on investments expected: 5% Annual investment needed to get ₹15 after 5 years: ₹2.71462.Ascertain the annual transfer to sinking fund.

Pradeep Ltd. has taken over the business of Mr. Sandeep and agreed to pay the purchase price as given below: (a) 2,800 shares of ₹50 each fully paid at ₹60 per share. (b) ₹25,000 in 8% preference shares of ₹100 each issued at premium of 25%.(c) ₹20,000 in Cash.You are required

What do you mean by “acquisition of business”?

Explain the steps to be taken by a purchasing company when new set of books are opened to record the transactions.

The purchasing company can record the transactions in their books as:(a). New set of books opened (b). To continue the same set of books (c). Any of the above two (d). None of these

A Ltd. purchased business of A & Co., and agreed to settle purchase consideration by the allotment of: 2,000 Equity shares of 10 each at 10% premium to partners. 1,000 10% Debentures of 100 each at par for loan creditors, and *1,00,000 in cash to partners. Calculate purchase consideration.

True and False. Purchase consideration must be paid only in cash.

The purchase price paid by the purchasing company to the selling company is called as ____________.

What are the two accounting approaches that can be adopted by the purchasing Company?

Explain the steps to be taken by a purchasing company when same set of books are Continued to record the transactions.

In the absence of a contract, which of the following item is not taken over by the purchasing company at the time of acquisition of business:(a). Profit and Loss Debit Balance (b). Cash Balance (c). Bank Balance (d). None of these

True and False. Purchase consideration is always given in the problems, so it need not be computed.

The newly formed limited companies purchase the business of ____________ or ____________ form of business concern.

How is Goodwill calculated?

State the accounting treatment to be adopted when the debtors and creditors are not taken over by the purchasing company when new set of books are opened.

X Ltd. issued 10,000 shares of ₹100 each at a premium of ₹15 each. Of the issue, 90% was underwritten by M/s. Broker & Co. at commission of 1% on the nominal face value.Applications were received for 8,000 shares and allotment was fully made. All the moneys due from allottees were received

The rate of ____________ payable on debentures is always stated at the time of issue of debenture.

M Ltd. issued 40,000 10% debentures of ₹10 each to the public at par, to be paid ₹3 on application and the balance on allotment. Applications were received for 35,000 debentures. Allotment was made to all the applicants and the amount due was received.Pass journal entries to record the

Journalise the following issues: (a). A company issued 1000, 6% debentures of ₹100 Each at par. (b). A company issued 1000, 6% debentures of ₹100 Each at 10% premium (c). A company issued 1000, 6% debentures of ₹100 Each at 10% discount

Goodwill Ltd. issued 1,000 6% debentures of ₹100 each. Give the journal entries in each of the following cases: (a). The debentures are issued and redeemable at par. (b). They are issued at a discount of 6%, but redeemable at par. (c). They are issued at a premium of 5%, but

What are the different types of debentures? Explain them in detail.

Long-term borrowing of a business: (a). Preference share capital. (b). Equity share capital.(c). Debentures. (d). None of the above.

The issue of debentures to vendor is known as issue of debentures for consideration___________.

True or False. Debentures will not be repaid on the date of redemption.

AB Ltd. issued 20,000 12% debentures of ₹100 each for public subscription, at a premium of 10% payable as to ₹20 on application, ₹50 on allotment (including premium) and the balance in one call. 30,000 applications were received. 5,000 applications were rejected and debentures were allotted

Pass journal entries for the following transactions:(a). Issue of debentures at a discount and redeemable at par. (b). Issue of debentures at a premium and redeemable at par. (c). Issue of debentures at par and redeemable at premium.(d). Issue of debentures at a discount and redeemable at

State the differences between debenture and share.

Enumerate the different methods of redemption of debentures and explain them.

The term, collateral security, implies additional security given for a ___________.

True or False. Both, premium on debentures and premium on redemption of debentures, carry the same meaning.

What do you mean by Convertible Debenture? State its significance.

Zel Ltd. issued 1,000 9% debentures of ₹100 each payable, ₹20 on application and the balance on allotment. Applications were received for 1,500 debentures; out of which, applications for 900 were allotted fully. Applications for 400 debentures were allotted 100 debentures and the remaining were

Debentures are shown under the following heading in a company’s balance sheet.(a). Secured loan. (b). Unsecured loan. (c). Share capital. (d). Current liabilities.

Premium on redemption of debentures account is transferred to ___________ at the time of redemption.

True or False. Debentures can be issued at par and can be redeemed at discount.

A company purchased land & building of the book value of ₹4,50,000 from Mr. Anand. It was agreed that the purchase consideration be paid by issuing 10% debentures of ₹100 each. Pass journal entries if the debentures have been issued: (i). At par; (ii). At discount of 10%;(iii). At

Write short notes on Own Debenture.

Narayanan & Co. Ltd. purchased assets worth ₹28,80,000. It issued debentures in satisfaction of the purchase price. Calculate how many debentures will be issued:(a). In case the debentures are of ₹100 each and are issued at a discount of 4% (b). In case the debenture are of ₹80 each

State the merits of Insurance Policy Method of redeeming debentures.

According to Companies (Amendment) Act, 1999, the premium on issue of debentures should be credited to: (a). Share Premium A/c (b). Debentures Premium A/c (c). Securities Premium A/c (d). None of the above

The interest paid on debentures appears on the ____________ side of the profit and loss account the company.

True or False. A company is not allowed to buy its own debentures in the open market.

Y limited has taken over the business of Krishnan, the asset and liabilities having been valued at ₹80,000 and ₹30,000 respectively. Y Co., agreed to pay ₹72,000 as the purchase price, to be settled by the issue of 12% debentures of ₹10 each at a premium of 20%. Give journal entries.

State the accounting treatment when debentures are issued as Collateral Security.

Discount on issue of debentures is shown under the following heading in a company’s balance sheet. (a). Fixed assets. (b). Non-current liabilities. (c). Investments. (d). Other current assets.

Write short notes as: (a). Debenture redemption reserve (b). Partly convertible debentures (c). Open Market buying method of redemption (d). Own Debentures acquired as Investments.

A company issued debentures of the face value of ₹1,00,000 at a discount of 6%. The debentures were repayable by annual drawings of ₹20,000. How would you deal with the discount on debentures? Show the discount account in the company’s ledger for the period of duration of debentures.

Premium on issue of debentures can be used to write off the ______ on issue of debentures.

True or False. A company can write off discount on issue of debentures from the revenue profits.

MN Ltd., issued 40,000 debentures of ₹50 each at a discount of 6%. Debentures were to be redeemed at the end of five years. Pass journal entry for the issue and show the amount of discount that should be written off to Profit & Loss A/c each year.

Showing 400 - 500

of 1507

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers