New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

corporate accounting

Corporate Accounting 1st Edition Anita Raman, P. Radhika - Solutions

Explain Ex-Interest and Cum-Interest quotation.

Interest on debenture is normally payable.(a). Every six months (b). Every three months (c). Annual payment (d). Every month

Suman Ltd. issued 40,000 debentures of ₹100 each, at a discount of 10%. The expenses of issue amounted to ₹1,00,000. The debentures were agreed to be redeemed at the rate of ₹8,00,000 each year, commencing from the end of the third year.Ascertain the amount of discount and expenses to be

If the purchase price for the debentures does not include interest for the expired period, the quotation is said to be _____________.

True or False. Interest on sinking fund investment is credited to general reserve.

What do you understand by Redemption Drawing by Lot?

Debenture issue is always made with a,(a). Fixed percentage of interest (b). Fixed percentage of dividend (c). Fixed percentage of dividend and interest (d). None of the above.

Z Ltd. issued 2,000 6% debentures of ₹100 each, on 1st January 2001 at a discount of 10%, redeemable at a premium of 5%. Give journal entries relating to issue of debenture and debenture interest for the period ended 1st December 2001, assuming that the interest was payable half yearly on 30th

If the purchase price for the debentures includes interest for the expired period, the quotation is said to be _____________.

True or False. Gain on sale of sinking fund investment is to be credited to sinking fund account.

G Ltd., issued 10,00012% debentures of ₹100 each at a discount of 5% repayable after 5 years at a premium of 5%. Give journal entries both at the time of issue and redemption of debentures.

How do you deal with Discount on Issue of Debenture in accounts?

Profit on cancellation of own debentures is transferred to:(a). Capital redemption reserve (b). General reserve (c). Capital reserve (d). None of the above

Own debentures account will appear on the ___________ side of the balance sheet.

Preference shares cannot be redeemed when they are ________ paid.

P, K and R underwrote 80% of an issue of 20,000 preferene shares of ₹10 each in the ratio of 2:2:1. The ‘firm’ and ‘marked’ applications of the underwriters are as follows:Applications for 16,000 shares were received in all. Prepare a statement showing the liability of each of the

The premium on redemption of preference shares can be provided out of: (a). Securities premium A/c (b). Capital redemption reserve A/c (c). Capital reserve (d). Depreciation reserve

A company, in a series of operations: (a). Issues at par 45,000 redeemable preference shares of ₹10 each, redeemable at a premium of 5%. (b). Redeems 15,000 of the redeemable preference shares out of the profit of the company. (c). Issues for cash 30,000 equity shares of ₹10,

A company had decided to issue 5,000 equity shares of ₹100 Each at a premium of 10% and utilize the proceeds to redeem 50,000 12% preference shares of ₹10 each at a premium of 5%. The New issue was fully subscribed and paid up. The preference shares were duly redeemed. Journalize.

True or False. The premium on redemption of preference shares cannot be debited to securities premium A/c.

Capital redemption reserve can be used for issuing fully paid _________ shares.

Who are Untraceable Shareholders? State the accounting treatment for them in redemption.

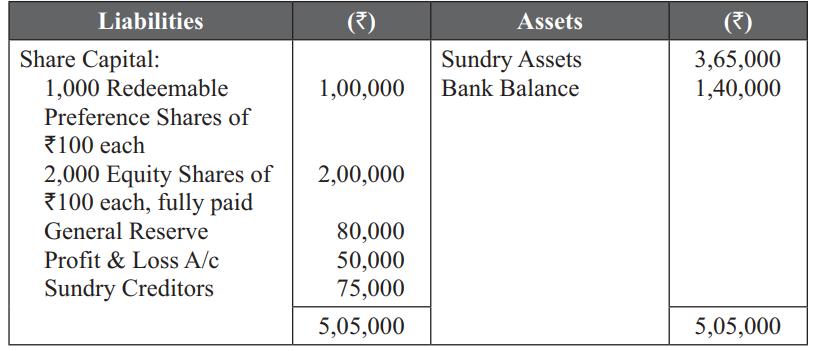

The following is the balance sheet of Ramani company limited as on 31.12.96: The company resolved to redeem its preference shares at a premium of 2% out of profits. Give the necessary journal entries. Liabilities Share capital: 1,000 6% Redeemable preference shares of ₹100 Each fully

The following is the summarised balance sheet of a company: For the purpose of redemption of preference shares, the company made a fresh issue of 4,500 equity shares of ₹10 each, at a premium of 10%. The preference shares were redeemed at a premium of 10%. Show journal entries and prepare

On 31st December 1993, the balance sheet of Sundaram Ltd., stood as follows:On the above date, the preference shares had to be redeemed. For this purpose, 1,000 equity shares of ₹100 each were issued at ₹110. The shares were immediately subscribed and paid for. The preference shares were duly

Sam Ltd. had as part of the share capital 20,000 preference shares of ₹100 each fully paid up. When the shares became due for redemption, the company had ₹12,00,000 in its reserve fund. The company issued necessary equity shares of ₹25 each specially for the purpose of redemption and carried

Explain the different types of Underwriting.

Nazar Ltd., issued 10,000 equity shares of ₹100 each at par. The whole issue has been underwritten by John & Co. for a commission of 2%. The company received applications only for 5,000 shares. All the applications were accepted. Give journal entries, assuming that all amounts due have been

When the entire issue is underwritten by only one person, his liability will be equal to: (a). Number of the shares underwritten.(b). Number of Shares underwritten minus number of shares applied for by the public.(c). Number of shares applied for by public.(d). None of the above.

True or False. Cash alone is paid as underwriting commission.

Under partial underwriting, the company itself becomes the underwriter for the shares _________.

The Chennai motors Ltd. issued 4,00,000 equity shares of Rs.10 each. The whole issue was underwritten by Malar. Applications for 3,20,000 shares were received in all. Determine the liability of the Underwriter.

What is Underwriting?

What is meant by Marked Applications?

State the provisions of the Companies Act, 1956, relating to underwriting of shares and debentures.

Marked application refers to: (a). Application bearing the stamp of the underwriters (b). Applications bearing the signature of the applicants (c). Applications bearing the stamp of the company. (d). None of the above.

True or False. The underwriters do not agree to purchase any shares in firm underwriting.

When an underwriter enters into an agreement with another person, he is known as __________.

The following underwriting of shares takes place: A—6,000 shares; B—2,500; C—1,500 shares. The issue consists of 10,000 shares. The total subscription was 7,100 shares and the forms included the following marked forms: A—1,000 shares; B—2,000

Explain the term Firm Underwriting.

What are the different methods of dealing with Unmarked Applications, in relation to an Underwriting Contract?

A company issued 20,000 equity shares of ₹100 each at par and 1,000 debentures of ₹1,000 each at ₹950. The whole of the issue has been underwritten by Paul & Co. The whole of the shares are applied for but applications were applied only for 800 debentures. All the applications were

Unmarked application refers to: (a). Application bearing the stamp of the underwriters. (b). Application received from the public without bearing the stamp of underwriters and also received directly by the company. (c). Applications issued by the company to underwriters (d).

True or False. The underwriters may be an individual, partnership firm, banks financial institutions or joint stock companies.

A company issued 30,000 equity shares which were underwritten by X. The company received application for 36,000 shares. Hence, X will get his commission on the issue price of ___________ shares.

Raj Ltd., issues 20,000 equity shares of Rs. 10 each at par. The issue was underwritten by Kala & Co. for maximum commission permitted by law. The public applied for and received 16,000 shares. Calculate the commission payable to the underwriter.

What do you mean by Unmarked Applications?

How do you calculate Underwriters’ Liability in Complete Underwriting and Partial Underwriting?

The remuneration of the underwriter is calculated on: (a). The issue price of the shares underwritten (b). The face value of shares actually purchased (c). The marked applications (d). None of the above.

True or False. The application received directly by the company which bears the stamp of the underwriters are called ‘marked application’

When _________are allotted to the underwriters, the underwriters A/c is debited.

Excel Ltd. issued 4,000 10% debentures of Rs.100 each at a discount of 6%. The whole of the issue was underwritten by M/s Mani & Co. for maximum commission permitted by law. The public applied for 3,200 debentures. Determine the Net Liability.

What do you mean by Gross Liability Ratio?

Write a note on Underwriting Commission.

Complete underwriting means: (a). The whole of the issue of shares or debentures is not underwritten (b). The whole of the issue of shares or debentures is underwritten (c). Only a part of the shares or debentures is underwritten. (d). None of the above

True or False. The net liability of underwriters, under complete underwriting, can be ascertained by deducting total applications received from shares or debentures offered.

When commission is payable to the underwriters, underwriters’ A/c is __________.

Gopu underwrites the new issue of 4,000 Preference shares of Rs.100 each at a premium of 10% of K.R. Ltd. The underwriting commission was payable as per the maximum rate allowed by law. The Public subscribed for 1,600 shares and the rest had to be taken by the underwriter. Calculate the commission

Arun Ltd. issued 1,00,000 equity shares. The whole of the issue was underwritten as follows: X: 40%; Y: 40%; Z: 20% Applications for 80,000 shares were received in all; out of which, applications for 20,000 shares had the stamp of X, those for 10,000 shares that of Y and 20,000 shares

If a part of the issue of shares or debenture is underwritten, it is termed as: (a). Partial underwriting.(b). Firm underwriting (c). Complete underwriting. (d). None of the above.

From the following details, compute the Net Liability of Underwriters: Total Number of shares offered to the Public: 10,000 Number of Shares Underwritten by X-5,000; Y-3,000; Z-2,000 Marked Applications (shares) X-1,500; Y-900; Z-600 Unmarked Applications: 3,000 shares

True or False. Unmarked application can be distributed among the underwriters in the ratio of gross liability.

Bank A/c is debited when the _________ due from the underwriters on the shares taken up by them is received.

Manu Ltd., issued 2,00,000 equity shares of which only 60% was underwritten by Gomathi. Applications for 1,80,000 shares were received in all out of which application for 1,04,000 were marked. Determine the liability of Gomathi.

In firm underwriting, the underwriter: (a). Does not agree to buy a definite number of shares in addition to unsubscribed shares (b). Agrees to buy a definite number of shares in addition to unsubscribed shares (c). Agrees to buy all the shares issued by the company (d). None of

Swetha Ltd. issued 40,000 equity shares of ₹100 each. Of the issue, 80% was underwritten by Prem. Applications for 28,000 shares were received in all by the company. Determine the liability of Prem.

True or False. Marked applications are also known as direct application.

The underwriting commission on shares should not exceed _____ per cent as per SEBI guidelines.

Sathya Ltd., issued 12%, 10,000 preference shares of Rs.10 each. The issue was underwritten as follows: Arul—30%; Madan—30%; Ganga—20%. Applications for 8,000 shares were received by the company in all. Determine the liability of the respective underwriters.

The Department of Economic Affairs, Ministry of Finance (F 14/1/SE/85-7-5- 85) and SEBI guidelines stipulates that the underwriting commission on shares should not exceed: (a) 5% (c) 10% (b) 2.5% (d) 1.5%

Charulatha Ltd. issued 80,000 8% debentures of ₹100 each. Of the issue, 75% were underwritten by Prabhu Brothers. Applications for 60,000 shares were received in all; out of which, applications for 38,000 were marked. Determine the liability of Prabhu Brothers.

True or False. Issue managers are responsible for the issue of shares right from the planning stage to the closing of all formalities related to the issue.

__________is the contract by each underwriter to sell a specified number of shares to the public.

The underwriting commission on debentures as per Companies Act 1956, should not exceed: (a). 5% of the issue price of debentures (b). 4% of the issue price of debentures (c). 2.5% of the issue price of debentures (d). None of the above.

As per SEBI guidelines, commission payable to underwriters for underwriting preference shares or debentures beyond Rs.5 lakhs, should not exceed: (a) 2% (c) 5% (b) 2.5% (d) 1.5%

The number of shares which are taken by each underwriter when the public has not subscribed is called as _________.

A Company issued 50,000 equity shares of ₹10 each at a premium of 10% and 2,000 debentures of ₹100 each at ₹95. Of the issue, 80% is underwritten by Sing & Co. at the maximum rate of commission allowed by law. Applications were received for 40,000 equity share and 1,500 debentures, which

AB Ltd. issued 10,000 shares of ₹10 each. These shares were underwritten as follows:X: 3,000 shares; Y: 5,000 shares. The public applied for 7,000 shares, which included marked applications, as follows: X: 1,000 shares; Y: 2,000 shares.Determine the liability of X and Y.

The underwriters’ liability is nil in case of __________ if the public has subscribed all the shares issued by the company.

X Ltd. issued 10,000 equity shares of ₹10 each. The issue was underwritten as follows: A: 30%; B: 30%; C: 20%:However, the company received applications for 8,000 shares only. Determine the liability of the respective underwriters and write the journal entries in the company’s

ABC Ltd. issued 30,000 shares of ₹100 each. The whole issue was underwritten by Gokul. In addition, there is a firm underwriting of 4,000 shares by Gokul. Applications for 20,000 shares were received by the company in all. Calculate the liability of Gokul.

Neeraj Ltd. issued 10,000 shares of ₹10 each, at a premium of 10%. The shares were underwritten by Joseph and Jaleel to the extent of 5,000 shares and 3,000 shares respectively.The total applications received by the company were 8,000; of which, the marked applications were: Joseph: 1,200

Raja Ltd. issued 50,000 equity shares of ₹10 each. Of the issue, 70% was underwritten by Sarvan. In addition, there is a firm underwriting of 4,500 shares by marked application, totalled for 22,000 shares. Determine the liability of Sarvan.

The following underwriting took place: A: 5,000 shares B: 3,000 shares C: 2,000 shares In addition, there was firm underwriting: A: 1,000 shares B: 500 shares C: 1,500 shares The share issue was for 10,000 shares. Total subscription including firm underwriting was

ABC Ltd. issued 30,000, 9% Preference shares of ₹10 each. Of the issue, 80% was underwritten by Palani. In addition, there is a firm underwriting of 5,000 shares by Palani. Applications for 27,000 shares were received by the company in all. The marked applications totalled 13,000 shares.

Akbar Ltd. issued 1,00,000 equity shares of ₹10 each. Of the issue, 75% was underwritten by Kumar. In addition, there was a firm underwriting of 9,000 shares by Kumar. In all, applications for 84,000 shares were received by the company. The marked applications totalled 44,000 shares. Determine

True or False. A company cannot redeem its partly paid preference shares.

RKT Ltd. issued 40,000 equity shares of ₹10 each and 10,000 9% redeemable preference shares of ₹100 each being fully called and paid up on 31st March 2002. Profit and loss account showed undistributed profits of ₹8,00,000 and general reserves stood at ₹3,00,000. On 1st April 2002, the

The balance sheet of Wallace Ltd., as on 31st December 2009 was as under:On this date, the preference shares were redeemed at par. Journalise and prepare balance sheet after redemption. Liabilities Share Capital: 1,000 Redeemable Preference Shares of 100 each 2,000 Equity Shares of 100 each,

Redemption of 10,000 preference shares of ₹100 each was carried out of reserves and out of the issue of 4,000 shares of ₹100 each @ ₹95. What is the amount of capital redemption reserve account that is required?

What are Redeemable Preference Shares? How are such shares redeemed?

State the conditions and procedures for the Issue of Redeemable Preference Shares.

Redeemable preference shares can be redeemed out of:(a). Amount realized on sale of current assets (b). Profits prior to incorporation (c). Proceeds of fresh issue of shares (d). Both b and c.

When preference shares are redeemed out of the profits otherwise available for dividend, the sum equal to the nominal number of shares must be transferred to: (a). Capital redemption reserve (b). Reserve fund (c). Profit & Loss A/c (d). Depreciation fund.

True or False. The main purpose of creating capital redemption reserve is to maintain the capital structure of the company intact after redemption.

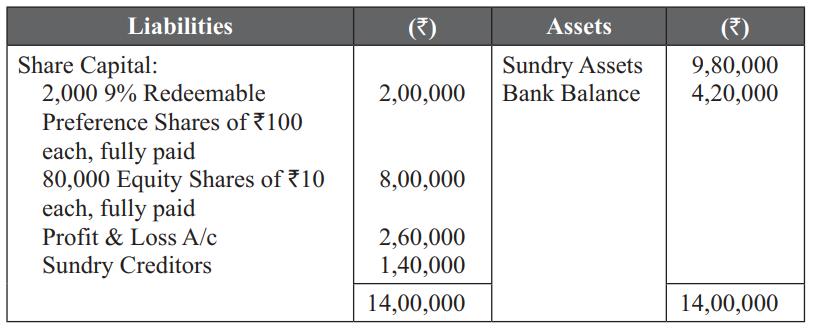

The summarised balance sheet of Gaur Ltd. on December 2004 was as follows:On the above date, the preference shares were redeemed at a premium of 10%. You are required to pass journal entries and give the amended balance sheet. Liabilities Share Capital: 2,000 9% Redeemable Preference Shares of

A company having free reserves of ₹1,20,000 wants to redeem ₹4,00,000 preference shares. Calculate the face value of fresh issue of shares of ₹10 each to be made at a premium of 10%.

If ______ shares are issued for the purpose of redemption of preference shares, it will not be treated as increase of capital.

Briefly explain the meaning of ‘Proceeds of Fresh Issue of Shares’.

Capital redemption reserve is created:(a). Out of shares forfeited A/c (b). Out of profits available for dividend (c). Out of securities premium (d). Out of capital reserve.

Showing 500 - 600

of 1507

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers