New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

corporate accounting

Corporate Accounting 1st Edition Anita Raman, P. Radhika - Solutions

True or False. The proceeds of fresh issue of debenture cannot be used for redemption of redeemable preference shares.

X co ltd has to redeem redeemable preference shares of the value of ₹2,00,000 at a premium of 10% for which the company has issued 10,000 equity shares of ₹10 each at a premium of 20. You are required to calculate the amount to be transferred to capital redemption reserve account.

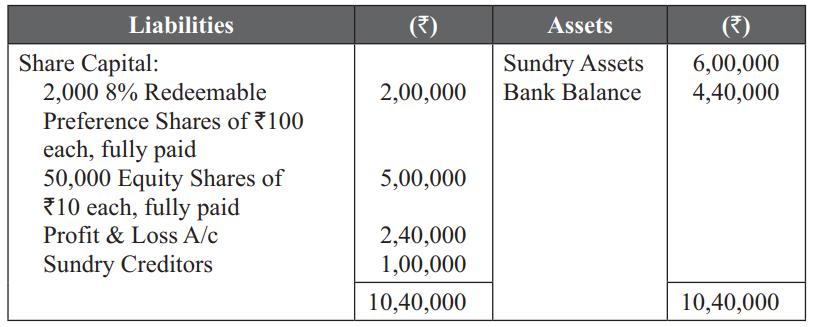

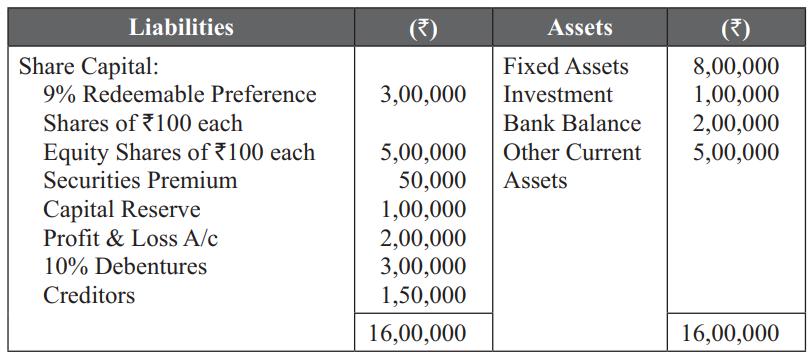

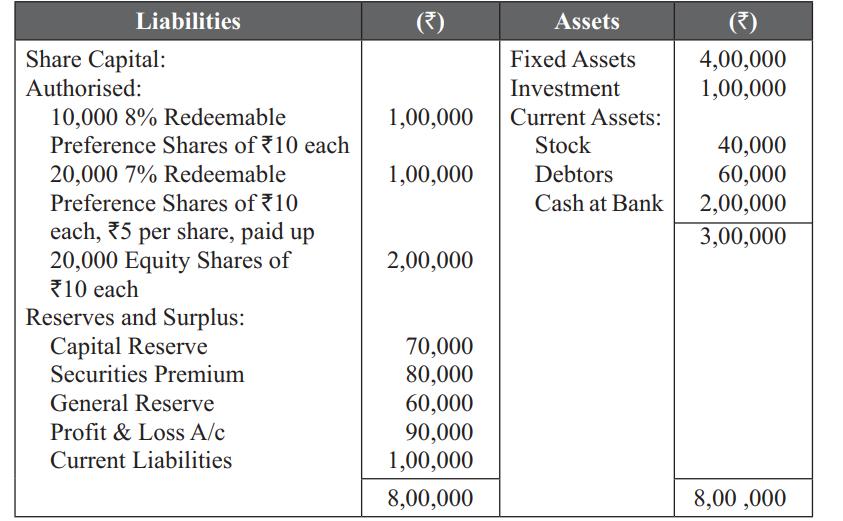

The following is the balance sheet of Raj Ltd., as on 31st December 2009:The company resolved to redeem its preference shares at a premium of 20% out of profits. Pass the necessary journal entries and show the important ledger accounts and the company’s balance sheet after completion of

Manu Ltd. has 10% 10,000 preference shares of ₹10 each fully paid. The shares became due for redemption and the company decided to redeem the whole amount out of a fresh issue of equity shares of ₹10 each fully paid.Show the necessary journal entries in the book of the company.

If any premium is to be payable on redemption, such premium has to be provided out of the securities premium A/c or ____________.

Enumerate the profits, which are eligible to be transferred to Capital Redemption Reserve.

What are the profits, which cannot be transferred to Capital Redemption Reserve? State the reasons.

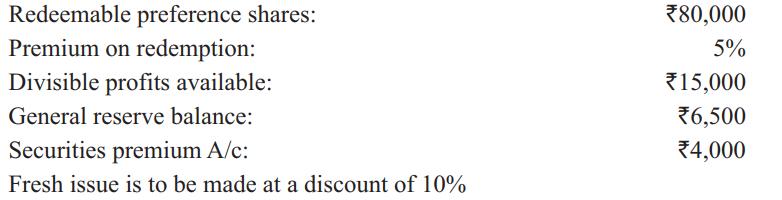

From the following data, calculate the amount of fresh issue of shares: Redeemable preference shares: Premium on redemption: Divisible profits available: General reserve balance: Securities premium A/c: Fresh issue is to be made at a discount of 10% *80,000 5% 15,000 6,500 €4,000

Amount can be transferred to capital redemption reserve from:(a). Capital reserve (b). Dividend equalization fund (c). Development rebate reserve (d). Securities premium A/c

True or False. Capital redemption reserve can be used to write off past losses of the company.

Companies (Amendment) Act 1988 prohibits issue of _________ preference shares.

A company wishes to redeem its preference shares amounting to ₹1,00,000 at a premium of 5% and for this purpose, issued 5,000 equity shares of ₹10 each at a premium of 5%. The company also has a balance of ₹1,00,000 on general reserve and ₹50,000 on profit and loss account. Pass the

What do you mean by Capital Redemption Reserve?

How do you calculate the ‘Minimum Fresh Issue of Shares’? Illustrate with an example.

Amount cannot be transferred to capital redemption reserve A/c from:(a). Profit & Loss A/c (b). Debenture Redemption Fund (c). Workmen’s Accident Fund (d). Capital portion of Profit on sale of fixed assets.

True or False. Workmen’s compensation fund can be transferred to capital redemption reserve A/c at the time of redemption of preference shares, if there is no liability for workmen for compensation.

Y Ltd. wishes to redeem its redeemable preference shares of ₹2,00,000 at a premium of 20%. For this purpose, it has decided to make a fresh issue of ₹100 shares at 10% premium and utilize the profits of ₹42,000 available for dividend. You are required to calculate the minimum fresh issue of

Capital Profits are __________ to be transferred to capital redemption reserve A/c.

B Ltd. had issued 50,000 redeemable preference shares of ₹10 each, ₹8 paid. In order to redeem these shares, the company issued for cash 30,000 equity shares of ₹10 each, at a premium of ₹2 per share. Out of the cash proceeds, the redeemable preference shares were paid and the balance was

Can partly paid-up redeemable preference shares be redeemed? If not, why?

What are the steps to be followed to redeem the preference shares?

Capital redemption reserve A/c is used:(a). To write off past losses. (b). To issue fully paid bonus shares.(c). To declare dividends. (d). To Capital Reduction A/c.

A company issued ₹1,80,000 redeemable preference shares at par on 1st January 1988, redeemable at the option of the company on or after 31st December 1992 in whole or in part.The following redemption was made from out of profits; In December 1994, the company issued equity shares of the

True or False. Capital redemption reserve can be used for converting partly paid shares into fully paid.

The following is the summarised balance sheet of a company as on 30th April 2001. It was decided to redeem both the classes of preference shares on 30th June at a premium of 5%. In May 2001, the company issued for cash so many equity shares of ₹10 each, as were necessary to provide for

General Reserve is _________ to be transferred to capital redemption reserve A/c.

What do you mean by Bonus Issue?

How do you create Capital Redemption Reserve? How can it be utilised?

SJ Ltd. has part of their share capital in 3,000 8% redeemable preference shares of ₹100 each. The company decided to redeem the preference shares at premium of 10%. The general reserve of the company shows a balance of ₹4,00,000. The directors decided to utilise 70% of the reserve in redeeming

State the significance of ‘Minimum New Issue of shares’.

X Ltd. has issued 20,000 equity shares of ₹10 each at a premium of ₹2 for the redemption of preference shares. Which of the following amount would be considered as ‘proceeds of fresh issue’?(a). ₹2,00,000 (b). ₹2,20,000 (c). ₹2,40,000 (d). None of the above.

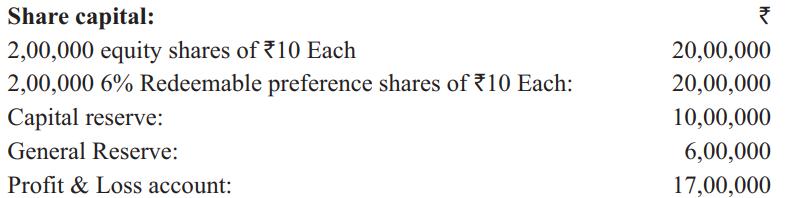

The following extract from the balance sheet of Vimala Ltd as on 31st December 1997 is given to you.The company exercises its option to redeem the preference shares on 1st January 2010. Share capital: 2,00,000 equity shares of 10 Each 2,00,000 6% Redeemable preference shares of ₹10 Each: Capital

True or False. Premium on issue of debentures can be used to pay premium on redemption of preference shares.

Profits which would otherwise be available for dividend is known as __________.

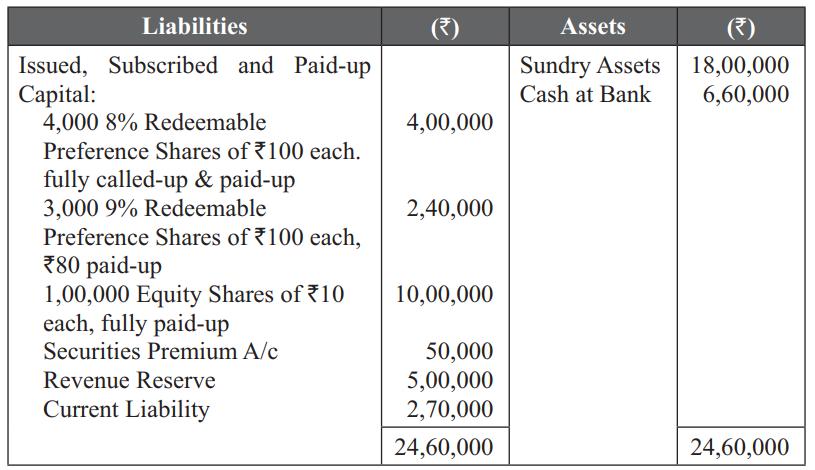

A company has 4,000 7% redeemable preference shares of ₹100 each, fully paid. The company decides to redeem the shares on 31st December 2004, at a premium of 5% .The company has sufficient profits but in order to augment liquid funds and redeem the shares, it makes the following issues:(a) 1,000

State the provisions of the Companies Act for Premium on Redemption of Preference Shares.

Redemption of preference shares does not affect:(a). Issued capital (b). Paid up capital (c). Authorised capital (d). Subscribed capital.

True or False. Redemption of preference shares can be considered as reduction of capital of the company.

The balance sheet of ABC & Co. Ltd. on 31st March 2009 stood as follows:Both the redeemable preference shares and debentures were due for redemption on 1st April 2009. The company arranged for the following:(a). It issued 2,000 equity shares of ₹100, at a premium of 10%. (b). It

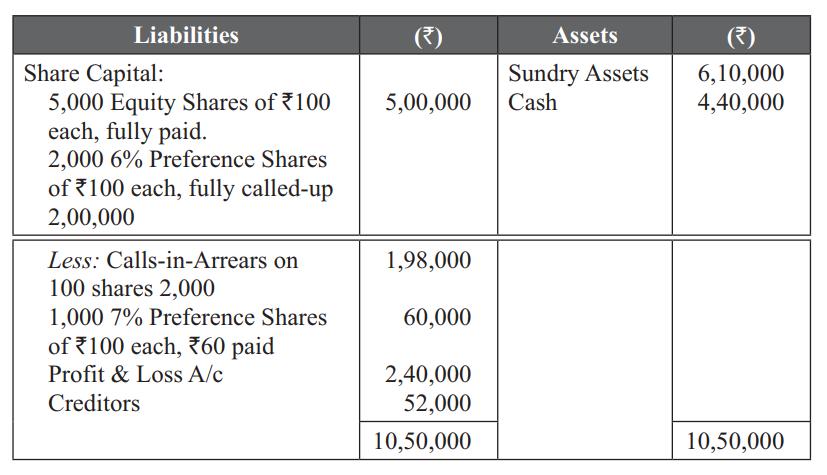

Following is the balance sheet of Raja Ltd., as on 31st December 1998.On the above date, preference shares are redeemed to the extent possible at a premium of 5%. Journalise and give the amended balance sheet. Liabilities Share Capital: 5,000 Equity Shares of ₹100 each, fully paid. 2,000 6%

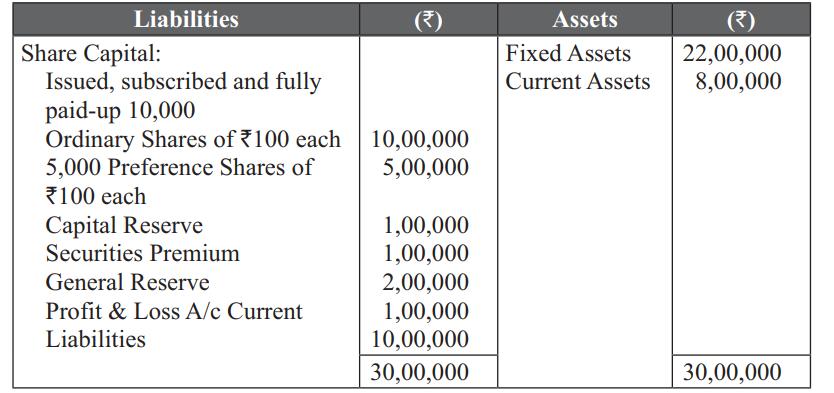

Balance sheet of X Ltd., as on 31st March 2007 is as follows. The preference shares are to be redeemed at 10% premium. Fresh issue of equity shares is to be made to the extent required under the Companies Act for the purpose of this redemption. The short fall in funds for the purpose of

A company wants to redeem its 10,000 6% preference shares of ₹10 each, fully paid at 10% premium. The ledger accounts show the following balances:The directors redeemed the shares by making minimum fresh issue of equity shares of ₹10 each, at a premium 5%. Give journal entries. Securities

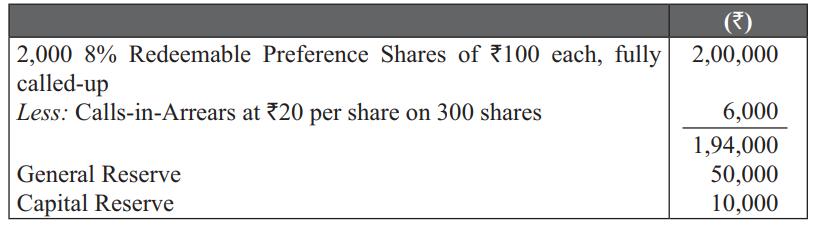

The balance sheet of Raman Ltd., as on 31st March 1987, is as follows:Redeemable preference shares were due for payment on 1st April 1987 at a premium of 10%. The company sent a reminder for the final call on the remaining 300 redeemable preference shares and could collect money from shareholders

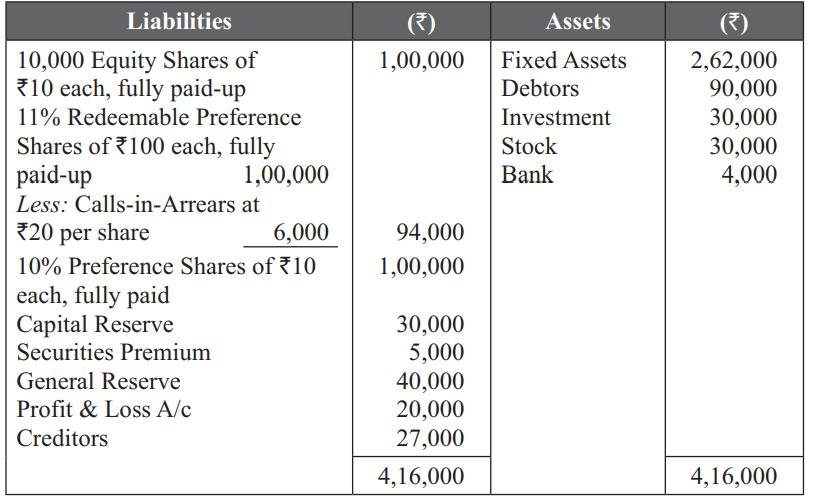

The following balances were extracted from the books of S Ltd., as on 31st December 1992.The preference shares were redeemed on 1st January 1993 at a premium of ₹5 per share. The company issued such further equity shares of ₹10 each, as were necessary for the purpose of redeeming the preference

Following was the balance sheet of Brite Ltd., as on 31st December 1996.On this date, the company redeemed, at a premium of 5%, all of its preference shares and debentures. For this purpose, it sold all the investments for ₹90,000 and allotted to its equity shareholders, 1,500 equity shares of

Following is the balance sheet of Manish Ltd., as on 31st December 2011.The preference shares were redeemed on 1st January 2012 at a premium of ₹2 per share, whereabouts of the holders of 1,200 such shares not being known. At the same time, a bonus issue of equity shares was made at par, one

The balance sheet of PQ Ltd. on 31st December 1985 is as under:The preference shares are to be redeemed at 10% premium along with dividend due for 1985. The company issued 45,000 equity shares of ₹10 each, at a premium of ₹5 per share. All shares were subscribed and cash was duly received. The

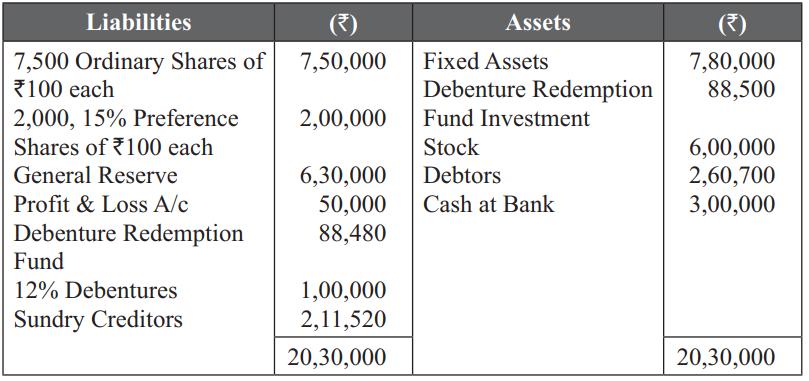

The balance sheet of Suraj Ltd., as on 31st December 2011, was as under.The company passed the following resolutions on 1st January 2012. (a). To redeem the entire preference share capital at a premium of 10%. (b). To issue 2,000 equity shares of ₹10 each, at a premium of ₹2 per

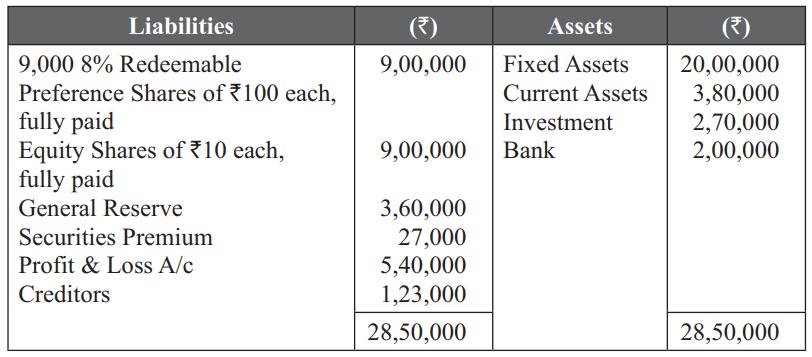

Following is the balance sheet of Nisha Ltd., as on 31st December 2011.On 1st January 2012, the company redeemed the preference shares at a premium of 10%. In order to pay-off the preference shareholders, it sold investments realising ₹95,000. All payments were made except to shareholders of

True or False. Fully paid up preference shares can be redeemed.

A company issued 5,000 equity shares of ₹10 each at a discount of ₹1 per share payable as follows:₹2 on application ₹3 on allotment (excluding discount) ₹3 on 1st call and balance on 2nd call.All the amounts were duly received. Pass the necessary journal entries in the books of

Paid-up capital does not ________________.

What are the provisions of the Companies Act under section 78 for the use of shares premium?

10,000 equity shares of ₹20 each are issued for public subscription at a premium of 10%. The full amount is payable on application. Applications were received for 20,000 shares and pro rata allotment was made to the applicants. Journalise the transactions.

The amount in the Securities Premium can be used for: (a). Distribution of dividend (b). Writing of capital losses (c). Transferring to general reserve (d). Paying fees to directors.

Satish Ltd. purchased land and buildings costing ₹5,00,000 and as payment towards purchase price, allotted equity shares of ₹10 each as fully paid. Pass journal entries in the books of Satish Ltd., if the company had issued shares at par, at a premium of 10% and at a discount of 10%.

On 1st April 2015, A Ltd. issued 50,000 shares of ₹100 each payable as follows: ₹20 on application.By 20th May, 40,000 shares were applied for and all applications were accepted. Allotment was made on 1st June. All sums due on allotment were received on 15th July. Those on 1st call were

True False. Dividend is declared and paid on the called-up capital.

State the legal provisions relating to allotment of shares?

Discount on issue of shares is a: (a). Capital loss (b). Revenue loss (c). Deferred revenue expenditure (d). Neither of the above.

A limited company having a pai-up capital of ₹5,00,000 in shares of ₹10 each had a Reserve of ₹1,20,000. It was resolved to capitalize ₹1,00,000 of the Reserve by issuing 10,000 fully paid Bonus shares of ₹10 each. Each shareholder to get one share for every ten shares held by him in the

What are Calls-in-Arrears? Explain the accounting treatment for Calls-in-Arrears.

True False. A company cannot ‘buy back’ partly paid up shares.

The name of the company are given in the ______ of the association.

6% is the rate of interest: (a). Calls in arrear (b). Calls in advance (c). Discount on issue of shares (d). Share allotment

True False. Equity Shareholders get dividend at fixed rate.

Define a share. What are the different kinds of shares that can be issued by a company?

Shareholders are called as __________ of the company.

Explain the different types of shares.

Ram Limited purchased assets of ₹10,00,000 from Rahul Limited. The company issued equity shares of ₹10 each fully paid up to the satisfaction of their claim. Pass journal entries to record these transactions.

A Ltd. issued shares for non-cash consideration in the following cases. Pass the necessary journal entries to record the transactions: 1. Issued 20,000 shares of ₹ 10 each in consideration for plant and machinery purchased on 10th January 2017. 2. Issued 30,000 shares of ₹10 each to B

A share allotment is classified as: (a). Personal A/c (b). Real A/c (c). Fictitious A/c (d). Nominal A/c

Journalise the following transactions: a. A Ltd. issued 40,000 shares of ₹10 each for cash. The whole amount is duly received. b. AB Ltd. issued 10,000 shares of ₹10 each for cash at premium of ₹2 each. The whole amount is duly received. c. ABC Ltd. issued 1,00,000 shares of

True False. A shareholder of the company is not liable for the act of the company.

Illustrate with an example how does a company issue shares at ‘par’, at ‘premium’ and at ‘discount’?

Shareholders receive dividend as return for their ____________.

Explain briefly the provisions of the Indian Companies Act 1956 regarding issue of shares at discount and at premium.

Vaishali Ltd., purchased the business of Vikram Ltd., for ₹4,00,000 payable in fully paid up shares of ₹100 each. What entries will be made in the books of Vaishali Ltd., if such issue is:(i) At Par; (ii) At a premium of 10% and (iii) at a discount of 10%?

The minimum share application money is: (a). 5% of the face value of shares (b). 10% of the face value of shares (c). 20% of the face value of shares (d). 15% of the face value of shares

Sumathi Ltd. issued 2,00,000 equity shares of ₹10 each to the public. The issue was fully subscribed by the public and the amount has been paid in one single instalment. Pass the required journal entries in the book of the company, if:(a) The shares were issued at par. (b) The shares were

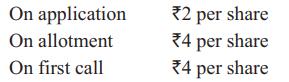

Ganesh Ltd. issued prospectus inviting applications for 10,000 equity shares of ₹10 each, payable as follows:The issue is fully subscribed. Pass journal entries in the books of Ganesh Ltd., assuming that all payments due as stated above were received. On application On allotment On first call *2

Bala Co Ltd. was registered with a share capital of ₹10,00,000 in shares of ₹100 each. The company acquired the business of M/s Sundari and Sons for ₹2,00000 payable as to ₹1,50,000 in fully paid shares and the balance in cash. The directors also decided to allot 150 shares credited as

True False. Equity shares and Preference shares are the two types of shares issued by a registered company in India.

What do you mean by allotment of shares?

Companies are now permitted to issue equity shares with disproportionate________ rights.

Can a new company issue shares at discount? If no, explain the provisions.

Anandhi Ltd., purchased Plant and Machinery worth ₹2,30,000 from Rajan Traders. Payment was made to ₹20,000 by cheque and the balance amount by issue of equity shares of ₹10 each fully paid at ₹10.50 each. Pass necessary journal entries.

Rajan Ltd. purchased the business of Raghu Bros. for ₹45,00,000, payable in fully paid shares of ₹100 each. What entries will be made in the books of Rajan Ltd., if such an issue is made: (a) At par. (b) At a premium of 10% (c) At a discount of 10%.

Securities Premium A/c is shown on: (a). Assets side of Balance Sheet (b). Liabilities side of Balance Sheet (c). Credit side of Profit and Loss A/c (d). Debit side of Trading A/c

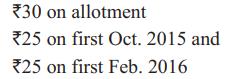

A company offered for public subscription 20,000 equity shares of ₹100 each payable as ₹20 per share on application, ₹30 on allotment, ₹20 three months after allotment and the balance six months after allotment. The offer was oversubscribed by 5,000 shares and the amount due on allotment

True False. A public limited company having share capital can start its operation after getting its incorporation certificate.

Explain ‘pro-rata’ allotment of shares.

A call money on shares should not exceed ________of the face value of shares.

Explain forfeiture and re-issue of shares.

A company issued 30,000 shares of ₹10 each at a discount of ₹1 per share payable ₹2 on application, ₹3 on allotment and the balance on the final call. All the shares offered were applied and allotted. Give journal entries.

The rate of discount on shares cannot exceed: (a). 4% (b). 6% (c). 10% (d). 8%

True False. Share premium amount can be used to write off premium on redemption of preference shares or debentures of the company.

CD Ltd. offered to the public 20,000 equity shares of ₹100 each at a premium of ₹10 per share. The payment was to be made as follows: On application ₹20; on allotment ₹40 (including premium); on 1st call ₹25; on 2nd call ₹25.Applications totalled for 35,000 shares; applications for

Preference shareholders have got preference as regards _______________.

Write short notes on:i. Bonus shares ii. Minimum subscription iii. Surrender of shares iv. Rights issue v. Stock- invest scheme vi. Sweat equity vii. Issue of shares for consideration other than cash.

Showing 600 - 700

of 1507

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers