New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

corporate accounting

Corporate Accounting As Per The Companies Act 2013 Including Rules 2014 And 2015 2nd Edition M Hanif, A Mukherjee - Solutions

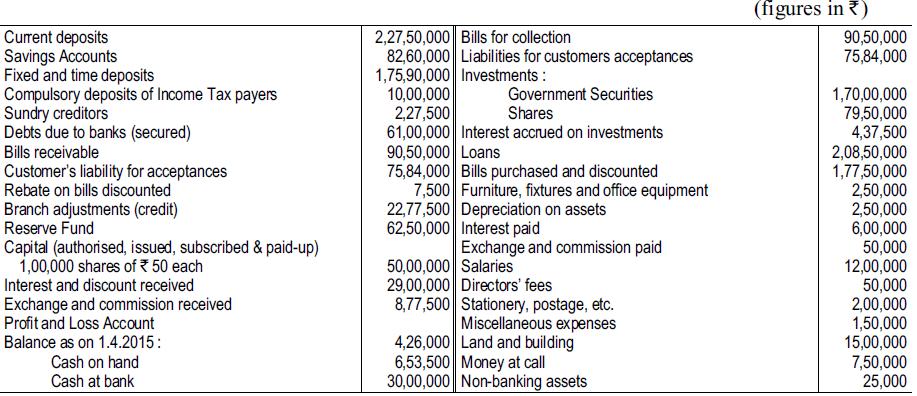

From the following balances of Punjab National Bank Ltd as on 31st March, 2016, prepare its Balance Sheet in the prescribed form:Adjustment:(a) Rebate on bills discounted ₹ 10,000.(b) Provide ₹ 80,000 for d oubtful debts.(c) Bank's acceptances on behalf of customers were ₹ 6,50,000. Paid-up

Prepare the Balance Sheet of Big Bank Ltd as on 31st March, 2016 from the following particulars:The reserve fund is equal to paid-up capital. The profit for the year is arrived at before making adjustment for unexpired discount ₹ 5,000 on bills discounted during the year not matured on 31st

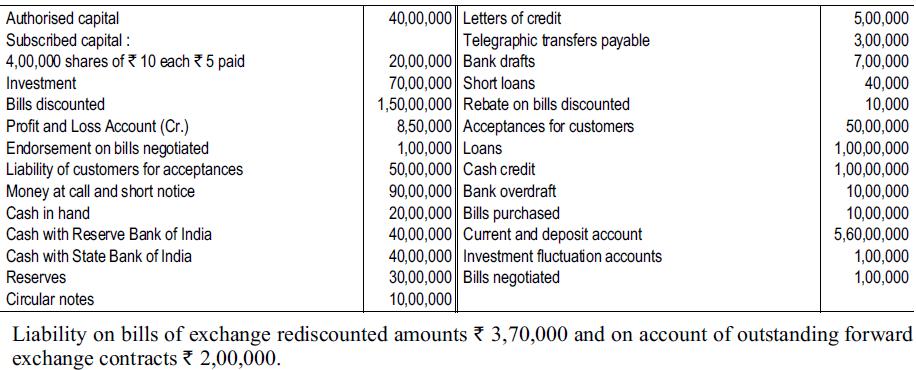

The Asoka Bank Ltd owns premises. From the following particulars relating to its accounts, prepare the Balance Sheet as on 31st March, 2016 (all figures in ₹). Authorised capital Subscribed capital: 4,00,000 shares of * 10 each * 5 paid Investment Bills discounted Profit and Loss Account

Following is the Trial Balance of the Kuber Bank Ltd as on 31st March, 2016 : (₹ ’000 omitted)Following information should be considered:(a) Provision for doubtful debts is required amounting to ₹ 5,000.(b) Interest accrued on investments ₹ 8,000.(c) Unexpired insurance ₹ 1,000.(d)

Some of the items in the trial balance of Modern Bank Ltd as on March 31, 2016 were as follows:You are required to prepare the Profit and Loss Account of the Bank, maintaining the provision for income-tax at ₹ 84,000 and provision for doubtful debts at ₹ 52,000 for the year ended March, 2016.

The following are the Ledger Balance (in ₹ thousands) extracted from the books of Vaishnavi Bank Ltd as on March 31, 2016.The bank's Profit and Loss Account for the year ended and Balance Sheet as at 31st March, 2016 are required to be prepared in appropriate form. Further information available

The following is the Trial Balance of Canara Bank Ltd as at 31st March, 2016Prepare Profit and Loss Account for the year ending 31st March, 2016 and a Balance Sheet as on that dateafter taking into account the following information.(1) Interest accrued on investments ₹ 10,000;(2) Rebate on bills

Following are the balances from the books of Everymans Bank Ltd as on March 31, 2016:Prepare the Profit and Loss Account for the year ending March 31, 2016 and also the Balance Sheet as on that date after taking note of the following:Provision needed for taxation: ₹ 5,00,000. Current Account

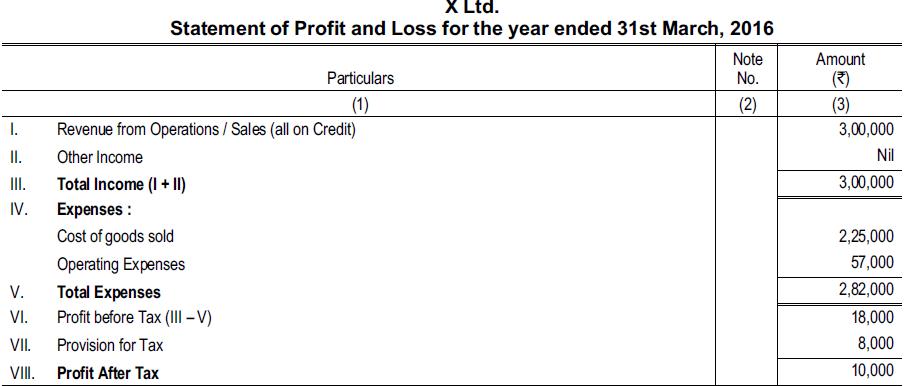

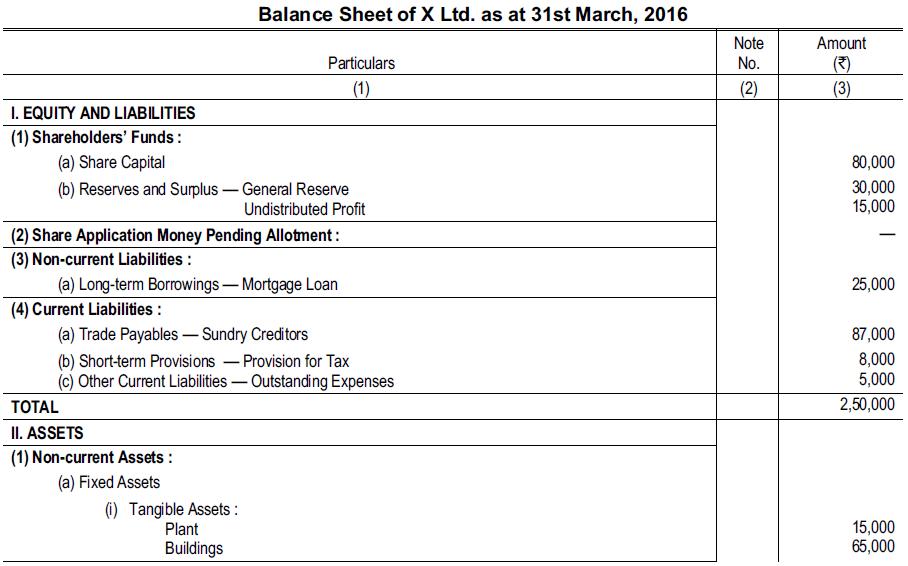

The following are abridged accounting reports prepared for X Ltd:Name and calculate the ratios which indicates:(a) The rapidity with which accounts receivable are collected;(b) The ability of the company to meet its current obligations;(c) What profitability on capital invested has been

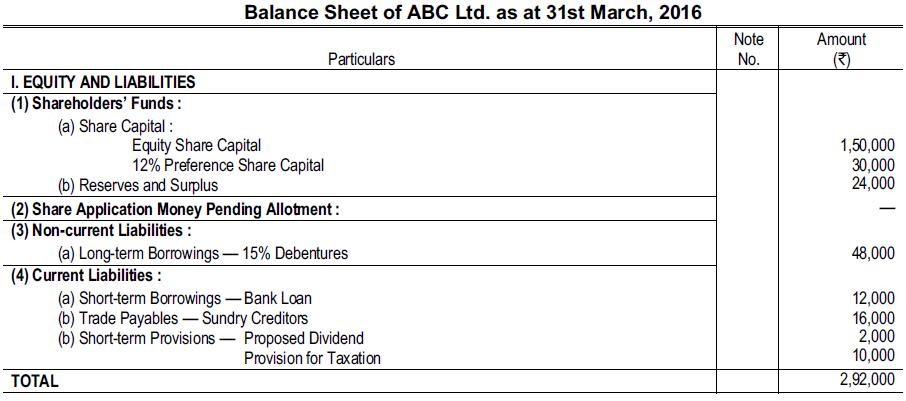

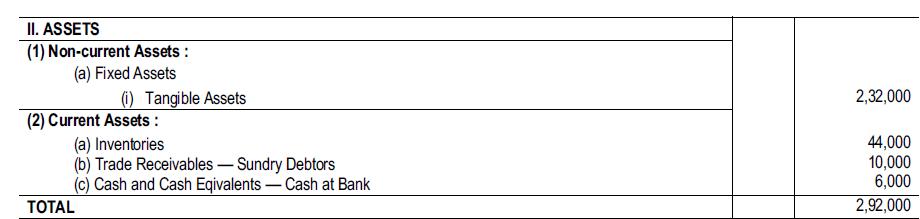

From the information given below, calculate :(i). Working Capital;(ii). Capital Employed;(iii). Current Ratio;(iv). Acid Test Ratio; and(v). Debt Equity Ratio. I. EQUITY AND LIABILITIES (1) Shareholders' Funds: (a) Share Capital: (b) Reserves and Surplus Equity Share Capital 12% Preference Share

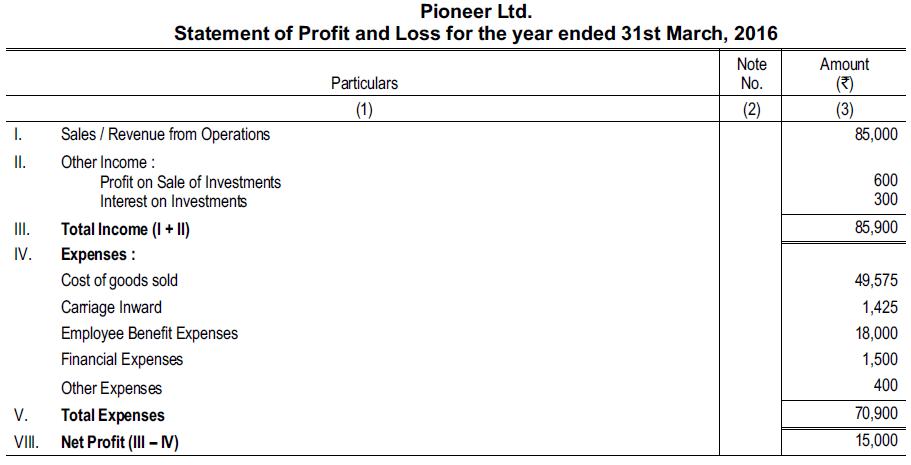

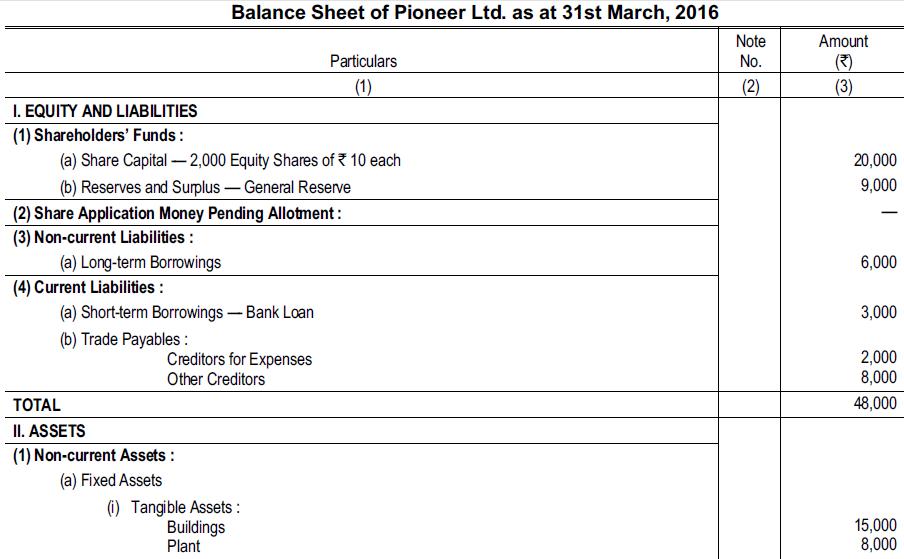

From the following annual statements of Pioneer Ltd., calculate the following ratios:(a) Gross Profit Ratio;(b) Current Ratio;(c) Liquid Ratio; and Debt Equity Ratio. I. II. III. IV. V. VIII. Pioneer Ltd. Statement of Profit and Loss for the year ended 31st March, 2016 Sales / Revenue from

Following items appear in the accounts of X Ltd. as on 31st March, 2016:The value of all fixed assets reflect current price levels and adequate depreciation has been provided. You are required to arrange the above items in the form of a financial statement to show the following accounting ratios

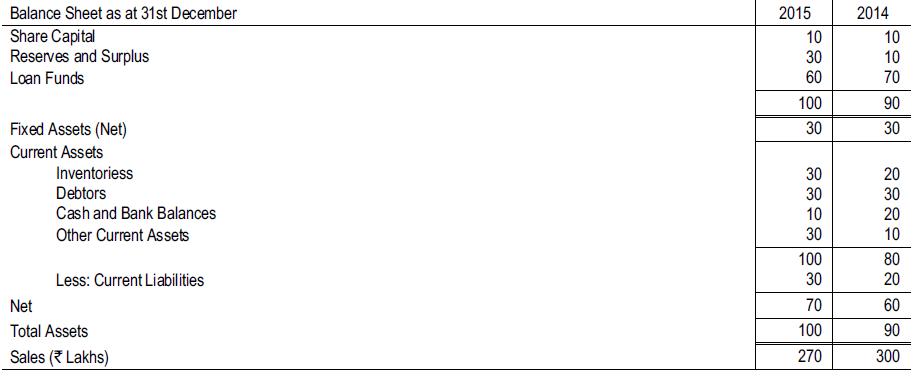

The following extracts of financial information relate to Curious Ltd. (figures in ₹ lakhs):(i) Calculate, for the two years Debt Equity Ratio, Quick Ratio and Working Capital Turnover Ratio; and(ii) Find the sales volume that should have been generated in 2015 if the company were to have

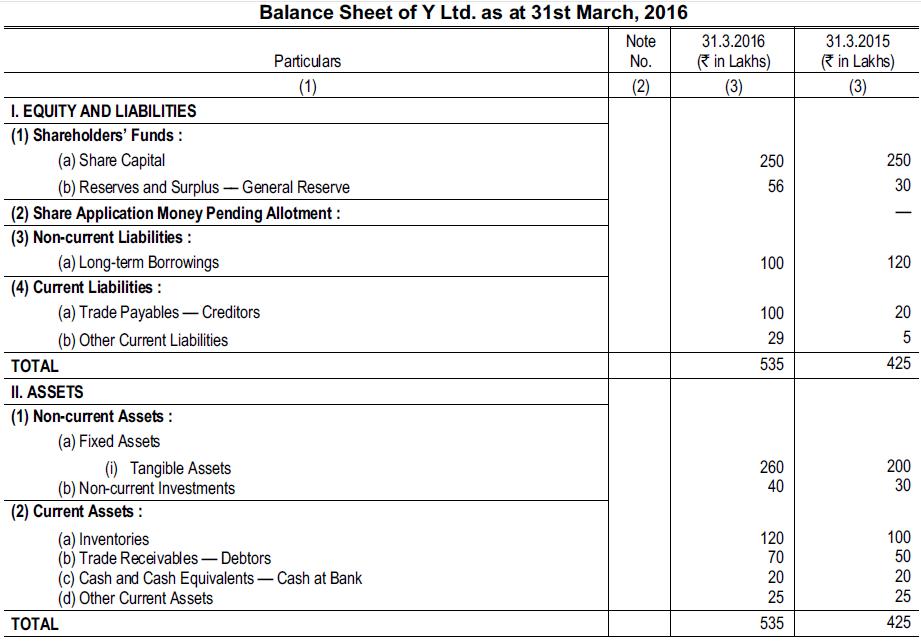

The Balance Sheet of Y Ltd. stood as follows as on:You are given the following information for the year 2015-16:Sales 600; PBIT 150; Interest 24; Provision for Tax 60; Proposed Dividend 30. All the figures given above are rupees in lakhs. From the above particulars, calculate for the year

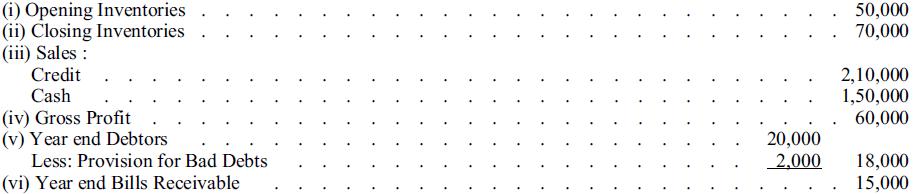

A business furnishes you with the following details:A year may be taken to be of 360 days. You are asked to:(i) Work out inventories turnover and debtors turnover ratios;(ii) calculate the operating cycle and state its significance. (i) Opening Inventories (ii) Closing Inventories (iii)

Important ratios of a firm for the year 2015 are given below:The firm expects an increase of 50% in sales in the ensuing year. Estimate the working capital requirement of the firm for the ensuing year. 1. Inventories velocity 2. Debt collection period 3. Creditors payment period 4 2 months 73 days .

From the following details available, prepare a summarised Balance Sheet of ABC Ltd., as at 31st December, 2015: Fixed assets to Networth Current Ratio Acid Test Ratio Reserves included in the Proprietors' Fund Current Liabilities Cash and Bank balances Fixed Assets.. * ₹ 0.75

From the following ratios and information relating to the activities of Bengal Traders Ltd., find out(a) Sales for the year 2015;(b) Sundry Debtors on 31.12.2015;(c) Sundry Creditors on 31.12.2015;(d) Closing Inventories: Debtors’ velocity 3 months; Inventories velocity 6 months; Creditors’

Shri Devdas asks you to prepare his Balance Sheet from the particulars furnished hereunder: Inventories velocity 6; Gross profit margin 20%; Capital turnover ratio 2; Fixed assets turnover ratio 4; Debt collection period 2 months; Creditors payment period 73 days; Gross Profit was ₹ 60,000;

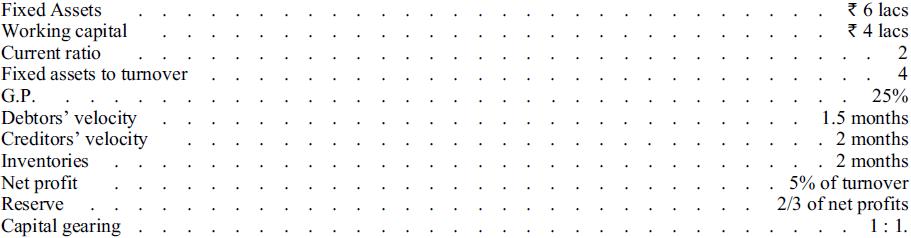

From the following information, prepare the Balance Sheet of Rameshpathy as on 31.3.2016: Fixed Assets Working capital Current ratio Fixed assets to turnover G.P. Debtors' velocity Creditors' velocity Inventories Net profit Reserve Capital gearing 6 lacs 4 lacs 2 4 25% 1.5 months 2 months 2

Prepare a Balance Sheet from the particulars furnished hereunder: Inventories velocity 6 Gross profit margin 20% Capital tumover ratio 2 Gross profit 60,000 Difference in Balance Sheet represents bank balance Fixed assets turnover 4 Debt collection period 2 months Creditors payment period 73

Based on the following information of the financial ratios prepare Balance Sheet of Star Enterprises Ltd as ofDecember 31, 2015. Explain your workings and assumptions: Current Ratio 2.5 Liquidity Ratio 1.5 Net Working Capital * 6,00,000 Inventories Tumover Ratio 5 Fixed assets to networth 0.8 Ratio

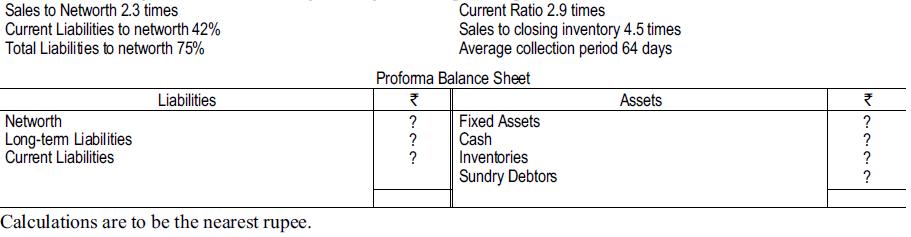

From the following information of X Engineering Co., computethe proforma Balance Sheet if its sales are ₹ 16,00,000. Sales to Networth 2.3 times Current Liabilities to networth 42% Total Liabilities to networth 75% Networth Long-term Liabilities Current Liabilities Liabilities Calculations are to

From the following information, make out a statement of proprietors’ fund with as many details as possible: (i) Current Ratio 2.5 (ii) Liquid Ratio 1.5 (iii) Proprietory Ratio (fixed assets/proprietory fund) .75 (iv) Working Capital * 60,000 (v) Reserve and Surplus 40,000 (vi) Bank Overdraft

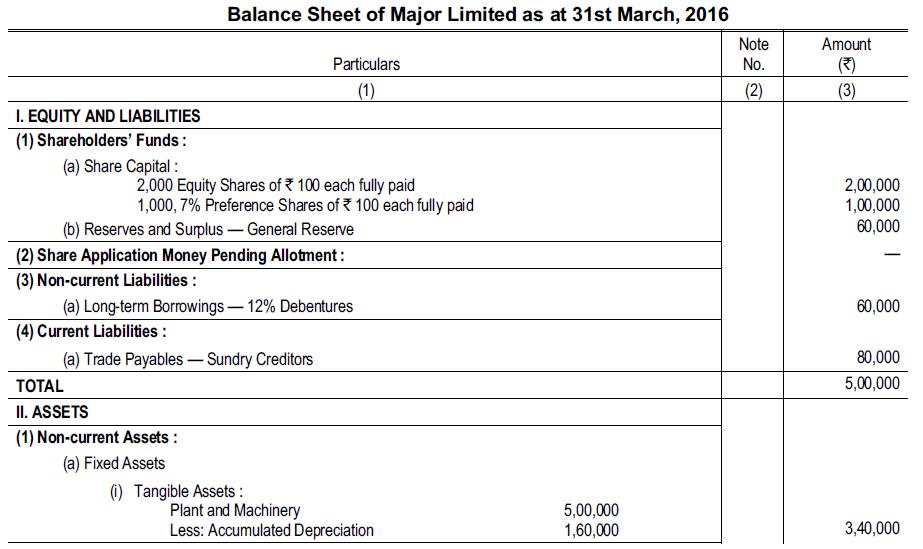

The Balance Sheet of Major Limited as on 31st March, 2016 is as under:The company wishes to forecast Balance Sheet as on 31st March, 2017.The following additional particulars are available:(i) Fixed assets costing ₹ 1,00,000 have been installed on 1.4.2016 but the payment will be made on

Following are the ratios relating to the trading activities of an organisation:Gross Profit for the year ended 31st March, 2016 was ₹ 7,50,000. Inventories as on 31st March, 2016 was ₹ 30,000 more than it was on 1st April, 2015. At the end of the year Bills Payable and Bills Receivable were ₹

With the help of information given below, prepare Statement of Profit and Loss and Balance Sheet of Sunshine Ltd.(a) Gross Profit ratio 25%;(b) Net Profit / Sales 20%;(c) Sales Inventory ratio 10;(d) Fixed Assets / Total Current Assets 5/8;(e) Current ratio 1;(f) Fixed asset /Share Capital 5/4;(g)

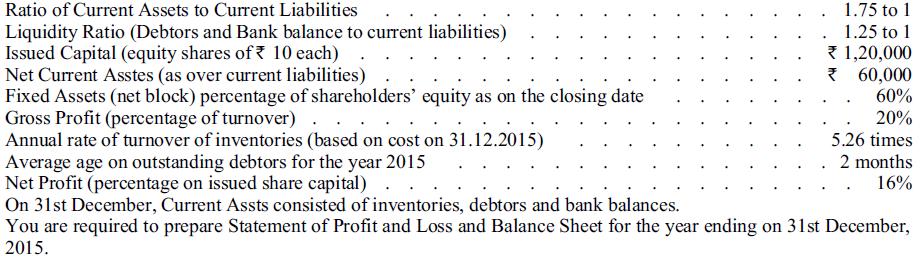

The financial information of Good Luck Ltd. for the year 2015 are given below: Ratio of Current Assets to Current Liabilities Liquidity Ratio (Debtors and Bank balance to current liabilities) Issued Capital (equity shares of 10 each) Net Current Asstes (as over current liabilities) Fixed Assets

From the following information, prepare the projected Trading and Profit and Loss Account for the next financial year ending December 31, 2015 and the projected Balance Sheet as on that date:Cost of sales consists of 40% for materials and balance for Wages and Overheads. Gross Profit ₹ 6,00,000.

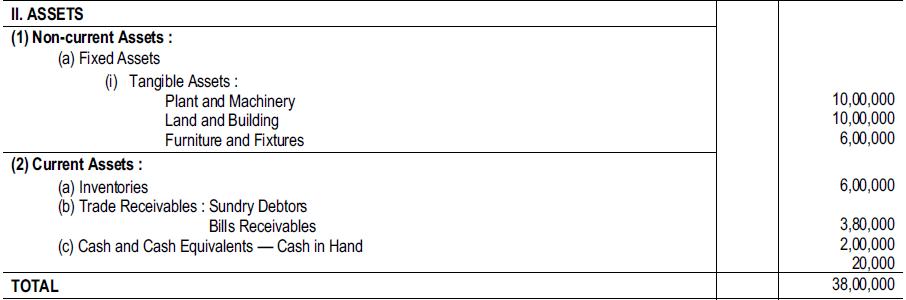

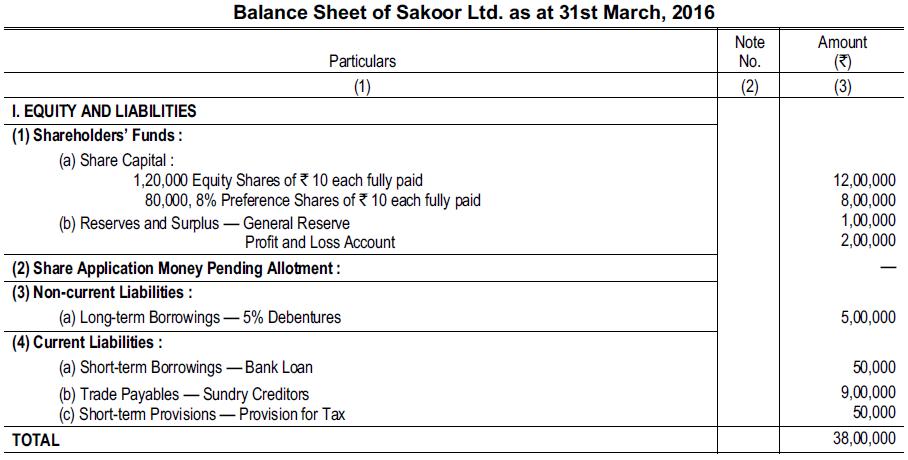

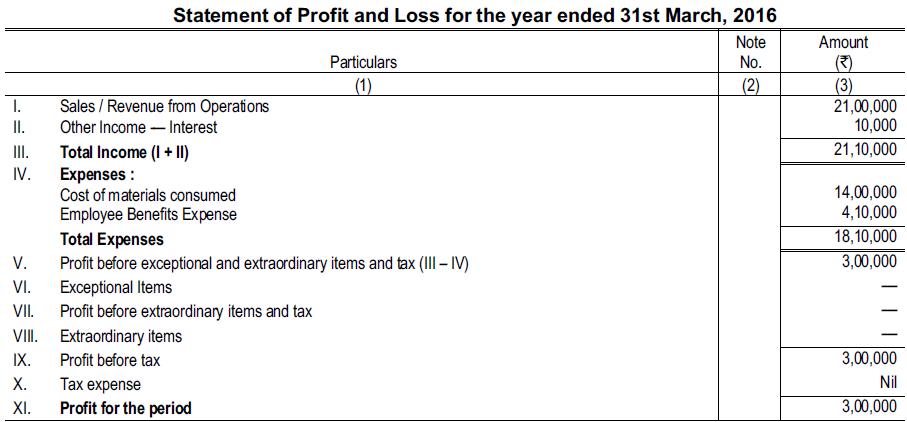

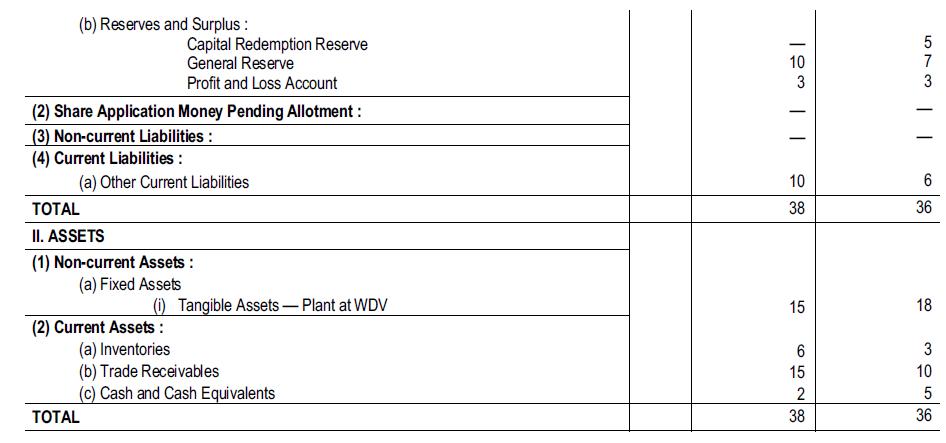

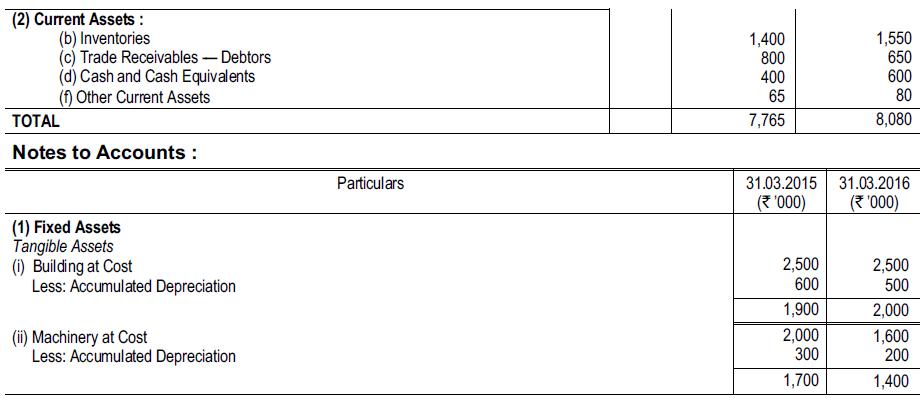

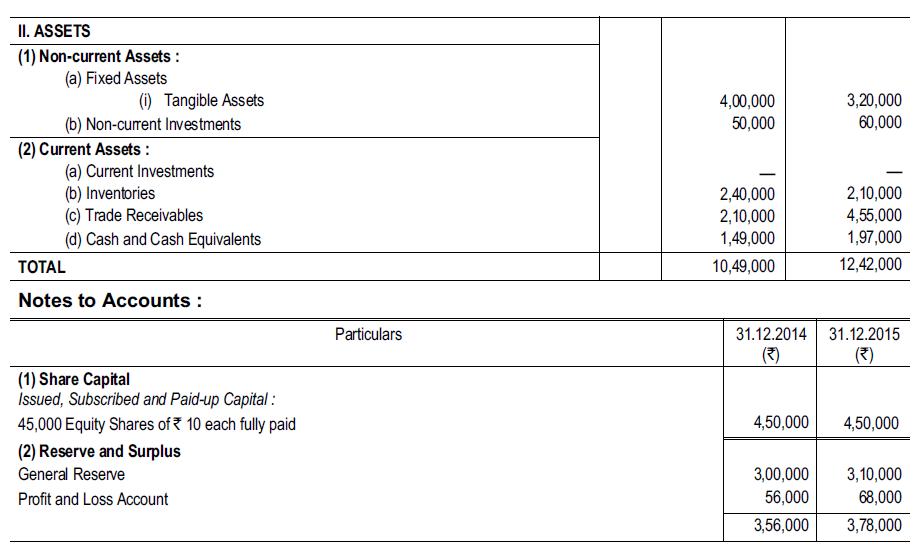

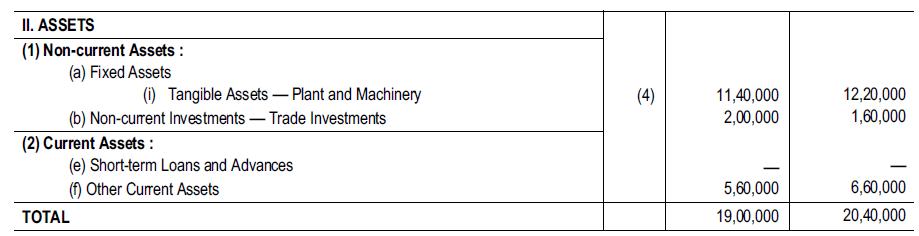

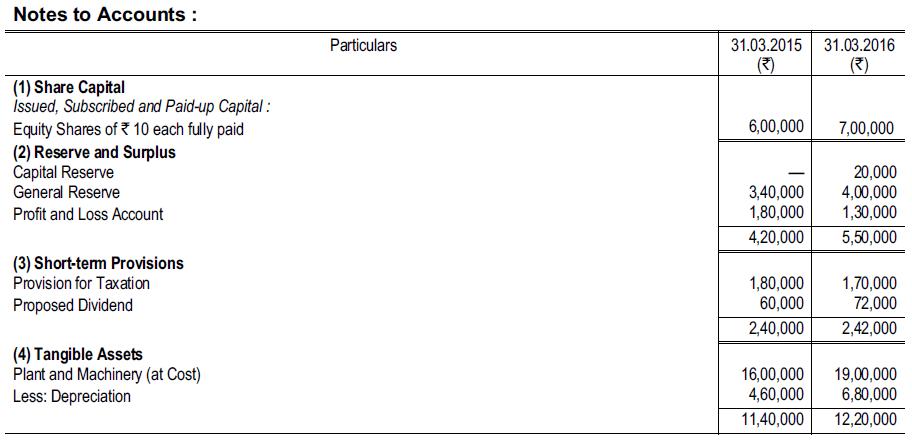

From the following information of Sakoor Ltd., for the year ending 31st March, 2016 examine the details from the point of view of(i) Solvency position(ii) Profitability position. Also comment on the condition of the business. II. ASSETS (1) Non-current Assets: (a) Fixed Assets (i) Tangible

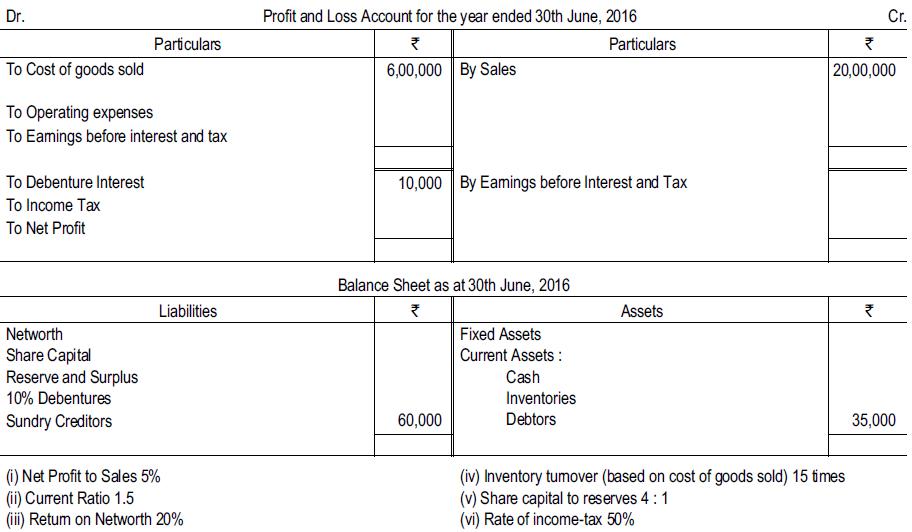

Complete the following annual financial statement on the basis of ratios given below: Dr. To Cost of goods sold To Operating expenses To Eamings before interest and tax To Debenture Interest To Income Tax To Net Profit Particulars Networth Share Capital Reserve and Surplus 10% Debentures Sundry

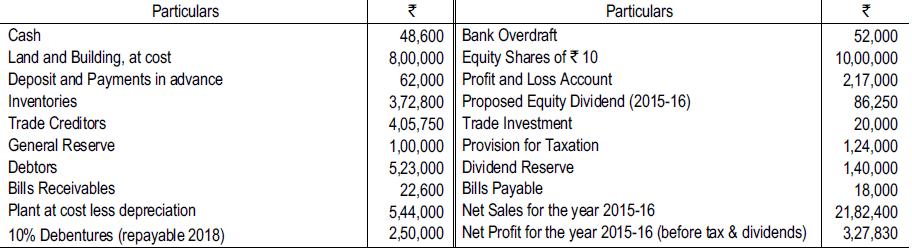

The Balance Sheet of Pilcom Ltd. for the last 3 years read as below (all figures in ₹ lakhs):Sales excludes excise duty and sales tax at 20%.Calculate for the years 2015 and 2016:(i) Fixed Assets Turnover Ratio;(ii) Inventories Turnover Ratio;(iii) Debtors Turnover Ratio in terms of number of

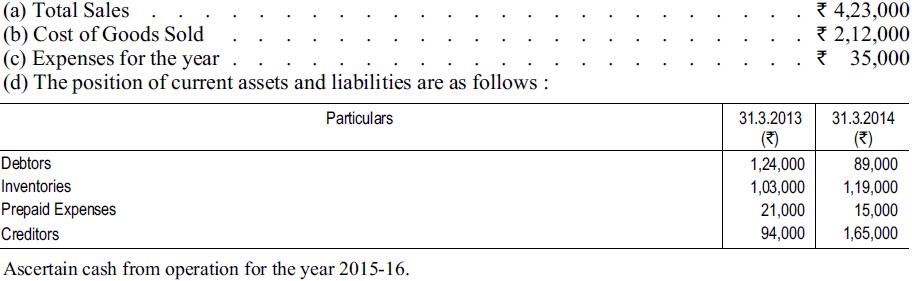

You are given the following particulars relating to the year ended 31st March, 2016: (a) Total Sales (b) Cost of Goods Sold (c) Expenses for the year (d) The position of current assets and liabilities are as follows: Particulars Debtors Inventories Prepaid Expenses Creditors Ascertain cash from

(a) What do you mean by Cash Flow Statement?(b) What are the objectives of Cash Flow Statement?

Dividends received by financial enterprise is shown in the Cash Flow Statement under :A. Operating ActivitiesB. Investing ActivitiesC. Financing Activities

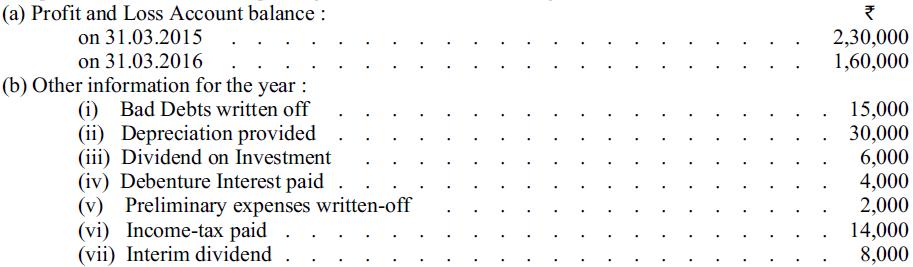

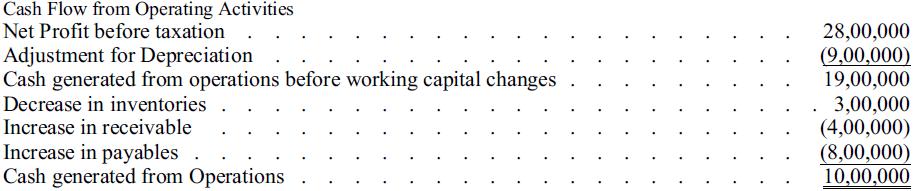

Ascertain cash from operation for the year 2015-16. Compute Net Cash Flow from Operating Activities from the following: (a) Profit and Loss Account balance : on 31.03.2015 on 31.03.2016 (b) Other information for the year : (1) Bad Debts written off (ii) Depreciation provided (iii) Dividend on

What are the advantages and limitations of Cash Flow Statement?

Dividends received by other than financial enterprises is shown in the Cash Flow Statement under :A. Operating ActivitiesB. Investing ActivitiesC. Financing Activities

From the following information, calculate Net Cash Flow from Investing Activities:Additional information:(1) During the year, a machine costing ₹ 80,000 with an accumulated depreciation of ₹ 48,000 was sold for ₹ 40,000.(2) Patents were written-off to the extent of ₹ 80,000 and some patents

Define:(i) Cash Equivalents;(ii) Operating Activities;(iii) Investing Activities;(iv) Financing Activities.

Interest paid by other than financial enterprise is shown in the Cash Flow Statement under :A. Operating ActivitiesB. Investing ActivitiesC. Financing Activities

From the information given below relating to Y Ltd., calculate Cash Flows from Operating Activities: (a) Operating profit before changes in Operating assets (b) Debtors (Decrease) (c) Stock (Increase) (d) Bills Payable (Decrease) (e) Creditors (Increase) (f) Cash at Bank

What are the different methods of calculating ‘Net Cash Flows from Operating Activities’? Explain any one of the methods in details.

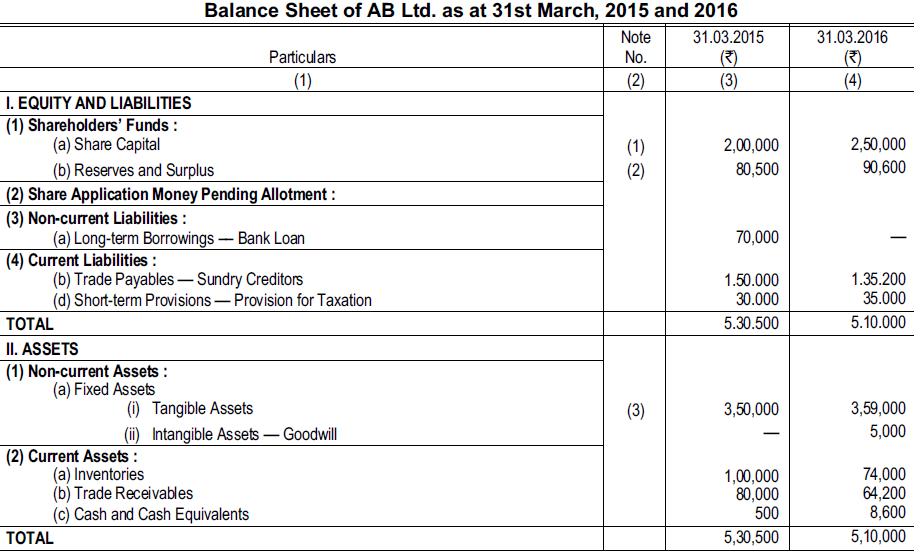

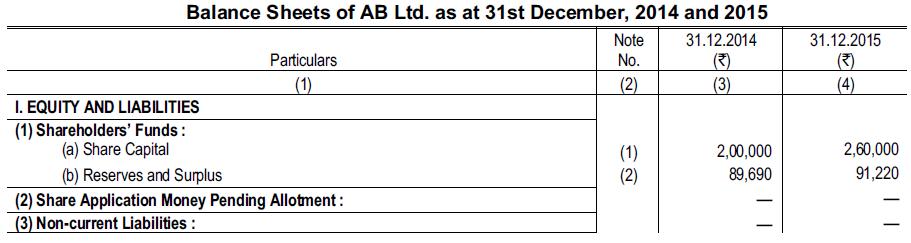

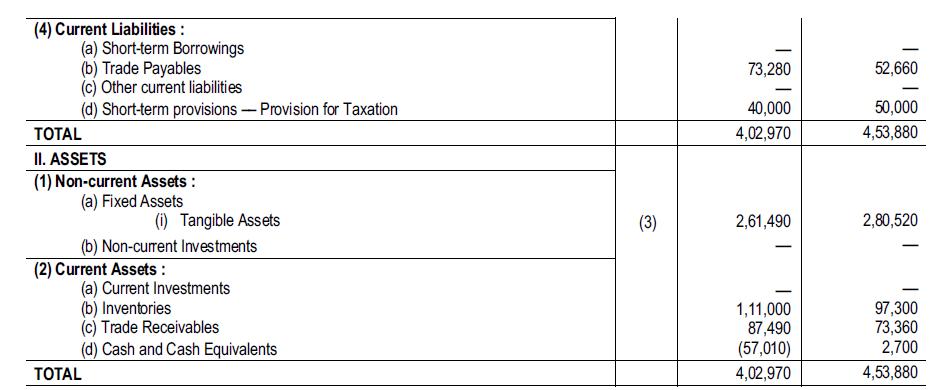

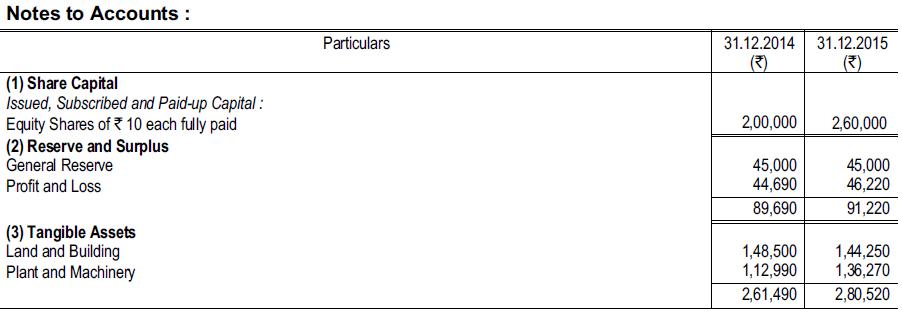

From the following Balance Sheet of AB Ltd. prepare a Cash Flow Statement for the year ended 31.3.2016:Additional information:(a) Dividend of ₹ 23,000 was paid.(b) Income tax paid during the year ₹ 28,000.(c) Machinery was purchased during the year ₹ 33,000.(d) Depreciation written off on

Interest received by other than financial enterprises is shown in the Cash Flow Statement under :A. Operating ActivitiesB. Investing ActivitiesC. Financing Activities

Explain why it is dangerous when analysing Balance Sheets to concentrate attention only on movements of cash balances rather than in working capital.

How should the revaluation of a fixed asset be treated in a cash flow statement ?A. It should be included in the cash flow from financing activities;B. It should be included in the cash flow from investing activities;C. It should not be included in the cash flow statement.

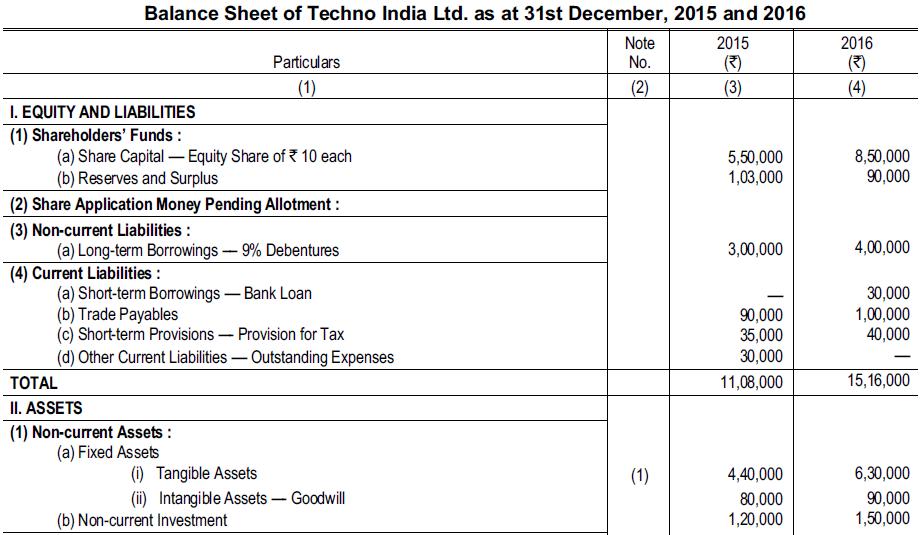

From the following Balance Sheet of Techno India Ltd., prepare a Cash Flow Statement as per AS----3: Balance Sheet of Techno India Ltd. as at 31st December, 2015 and 2016 2015 (3) (3) I. EQUITY AND LIABILITIES (1) Shareholders' Funds: (a) Share Capital - Equity Share of 10 each (b) Reserves and

Explain why it is more important to manage long-term profitability than short-term cash flow.

Which of these items could appear in the company’s Cash Flow Statement prepared under AS----3 "Cash Flow Statement" ?1. Dividend received;2. Bonus issue of shares3. Dividend paid4. Surplus on revaluation of a non-current asset5. Loan repayment6. Accumulated profitA. 1, 3 and 5B. 1, 2, 4 and 5C.

Which of the following items could appear in a company’s cash flow statement prepared as per AS----3 (Cash Flow Statement) ?1. proposed dividends2. rights issue of shares3. bonus issue of shares4. repayment of loanA. 1 and 3B. 2 and 4C. 1 and 4

From the following Balance Sheet of JP International, prepare a Cash Flow Statement for the year ended 31st December, 2015 and 2016:Additional information available on 31.12.2016:(a) Accumulated depreciation on Fixed Assets amounted to ₹ 1,60,000 and ₹ 1,85,000 as on 31.12.2015 and 31.12.2016

An extract from a cash flow statement prepared by a trainee accountant is shown below:Which of the following criticisms of this extract are correct ?1. Depreciation charges should have been added, not deducted.2. Decrease in inventories should have been deducted, not added.3. Increase in

The following are Summarised Balance Sheet of CD Ltd. as on 31st March, 2015 and 2016:Additional information:(i) 10% Dividend was paid during 2015-16.(ii) Machinery for ₹ 60,000 was purchased and old machinery costing ₹ 24,000 (accumulated depreciation ₹ 12,000) was sold for ₹ 8,000.(iii)

Which of the following assertions about cash flow statements is / are correct ?1. A cash flow statement prepared using direct method produces a different figure for operating cash flow from that produced through indirect method.2. Rights issue of shares do not feature in cash flow statements.3. A

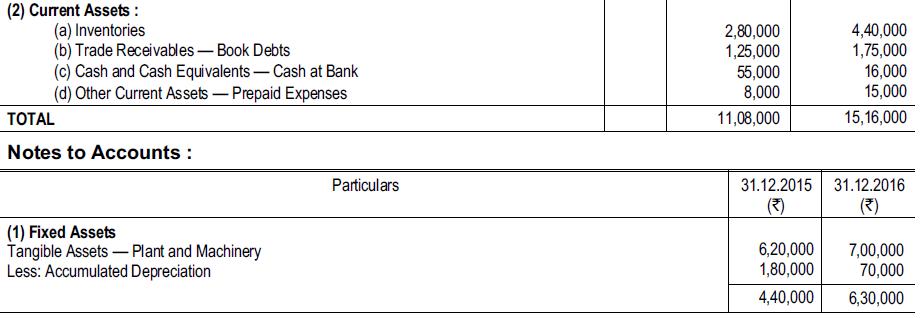

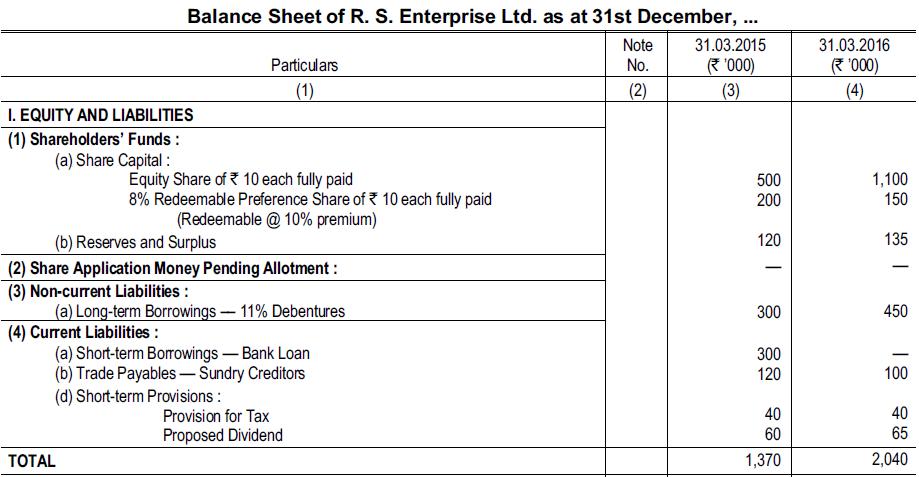

From the following Balance Sheet of R S Enterprise Ltd., prepare Cash Flow Statement as per AS----3 and comment on it.Other information available on 31.3.2016:(i) An old furniture (valued at ₹ 14,000 after 30% depreciation) sold for ₹ 12,000. Accumulated depreciation on fixed assets as on

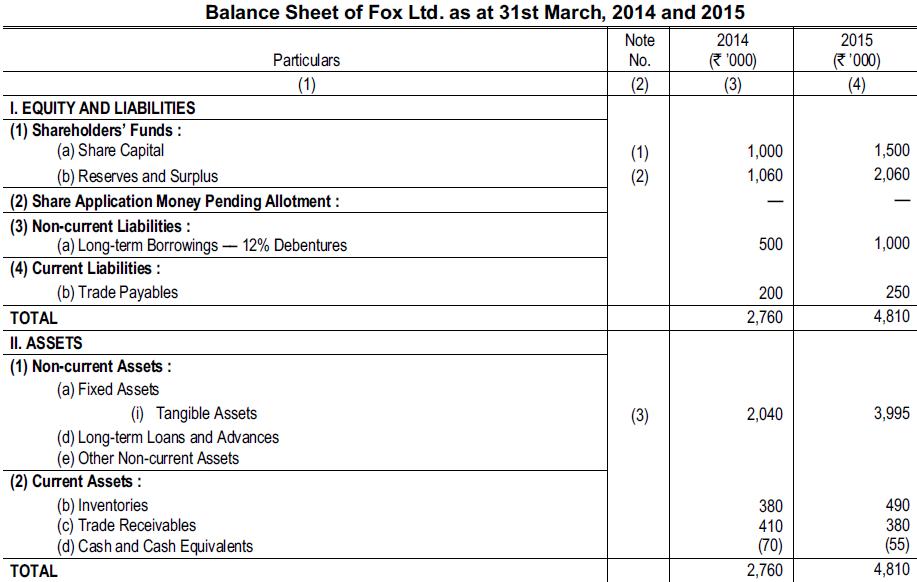

The Balance Sheet of Fox Ltd at 31st December, 2014 and 2015 are given below:Notes:1. Fixed AssetsDuring the year, land carried in the accounts at cost ₹ 8,00,000 was revalued to ₹ 12,00,000. No depreciation had been provided for this land.Also a fixed assets which had cost ₹ 2,00,000 were

Part of the process of preparing a company’s cash flow statement is the calculation of cash inflow from operating activities. Which of the following statements about that calculation using indirect method are correct ?1. Loss on sale of operating fixed assets should be deducted from net profit

Which of the following items could appear in a company’s cash flow statement ?1. Surplus on revaluation of fixed assets.2. Proceeds from issue of debentures.3. Proposed dividend.4. Bad debts written off.5. Dividend received.A. 1, 2 and 5 onlyB. 2, 3, 4 and 5 onlyC. 2 and 5 only

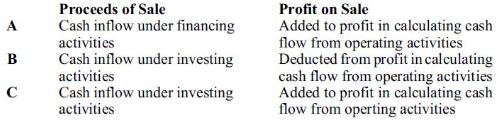

Kabir Limited sold a building at a profit. How this transaction be treated in the company’s cash flow statement? A B C Proceeds of Sale Cash inflow under financing activities Cash inflow under investing activities Cash inflow under investing activities Profit on Sale Added to profit in

Usha Limited had the following condensed Trial Balance as at 31.3.2015:During 2015-16, the following transactions took place:(i) A tract of land was purchased for ₹ 7,750 cash.(ii) Bonds payable in the amount of ₹ 6,000 were retired for cash at face value.(iii) An additional ₹ 20,000 equity

From the following information prepare a Cash Flow Statement as per AS-3:Additional information:(a) During the year the company paid ₹ 2,00,000 as equity dividend and ₹ 50,000 as preference dividend.(b) The company redeemed the preference shares at par after making a call of ₹ 50 per share to

A cash flow statement prepared in accordance with AS----3 "Cash Flow Statement" opens with the calculation of cash flow from operating activities from the net profit before taxation. Which of the following lists of items consists only of items that would be ADDED to net profit before taxation in

From the following information, prepare a Cash Flow Statement for the year ended 31st March, 2016:Additional information:(a) Dividend of ₹ 23,000 was paid during the year.(b) Net profit for the year ₹ 66,100.(c) Depreciation written-off on building ₹ 10,000 and on machinery ₹ 12,000.(d)

In the course of preparing a company’s cash flow statement, the following figures are to be included in the calculation of net cash from operating activities (all figures in rupees):Depreciation charges 9,80,000;Profit on sale of non-current assets 40,000;Increase in inventories 1,30,000;Decrease

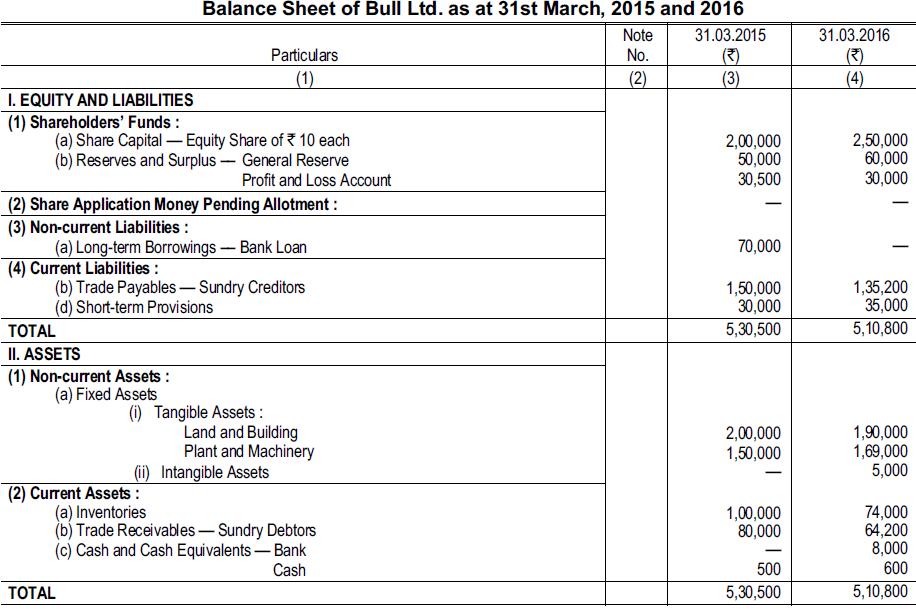

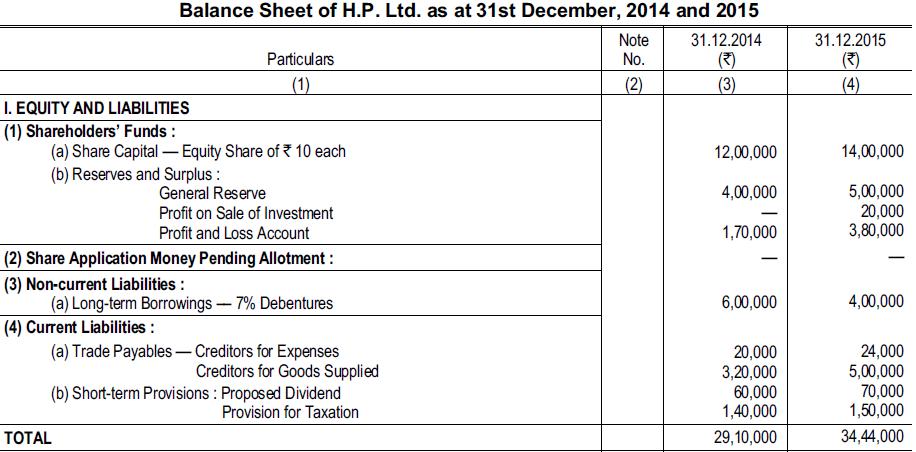

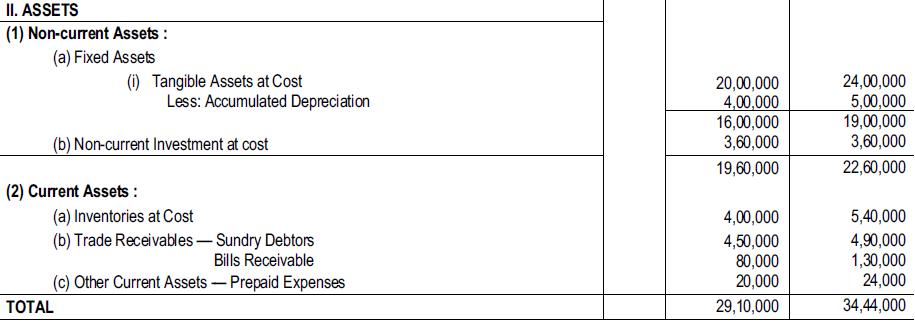

The Balance Sheets of H.P. Ltd.. are given below:Additional information:(i) During the year 2015, fixed assets (valued as ₹ 20,000 depreciation written-off ₹ 60,000) was sold for ₹ 16,000.(ii) The proposed dividend of last year was paid in 2015.(iii) During the year 2015, investments costing

The Balance Sheet of Steady Growth Ltd for the year ended 31st March, 2015 and 2016 are as follows:Additional information:(i) The company sold one fixed asset for ₹ 1,00,000, the cost of which was ₹ 2,00,000 and the depreciation of ₹ 80,000 was provided on it.(ii) Depreciation on fixed assets

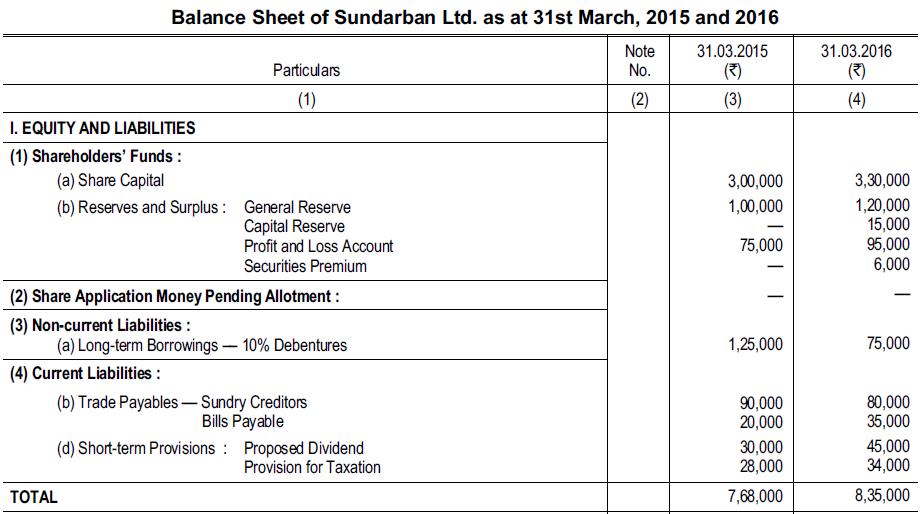

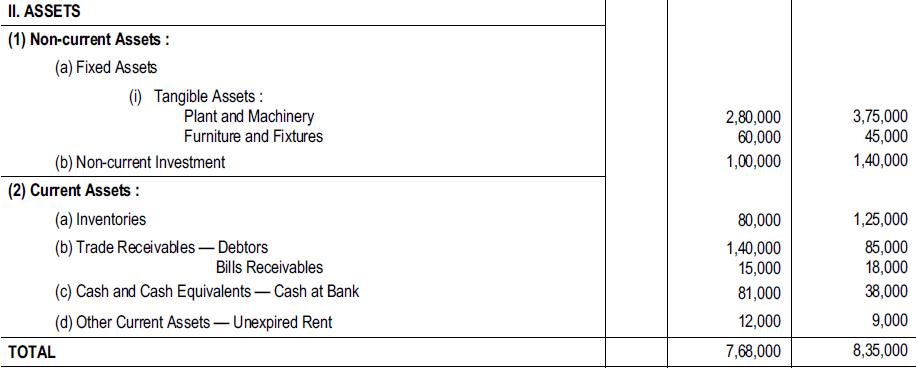

Sundarban Ltd. furnishes the following Balance Sheets for the year ended 31st March, 2015 and 31st March, 2016. You are required to prepare a Cash Flow Statement (as per AS--3) for the year ended 31.03.2016:Additional information:(a)(b) Plant costing ₹ 50,000 (accumulated depreciation ₹ 30,000)

A company purchased a motor vehicle for ₹ 5,00,000. Settlement was made by a payment of ₹ 4,40,000 and the part exchange of one of the company’s own vehicles for ₹ 60,000. The vehicle given in part exchange had a written down value of ₹ 1,40,000, but had a re-sale value of ₹ 40,000.

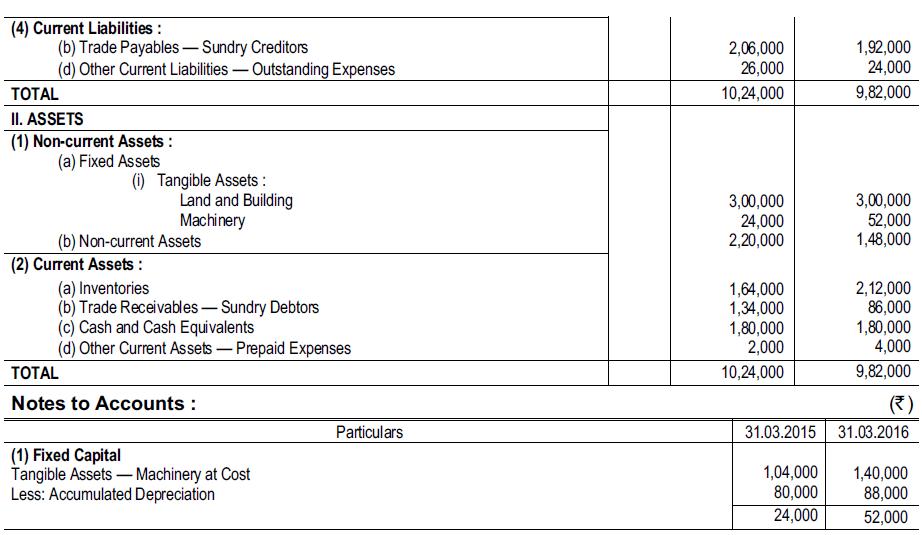

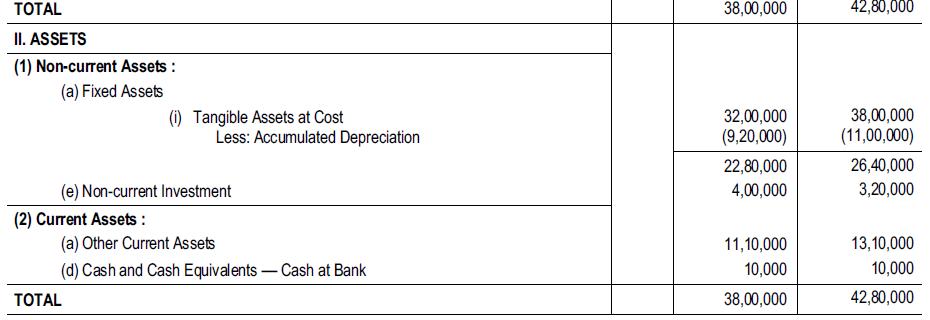

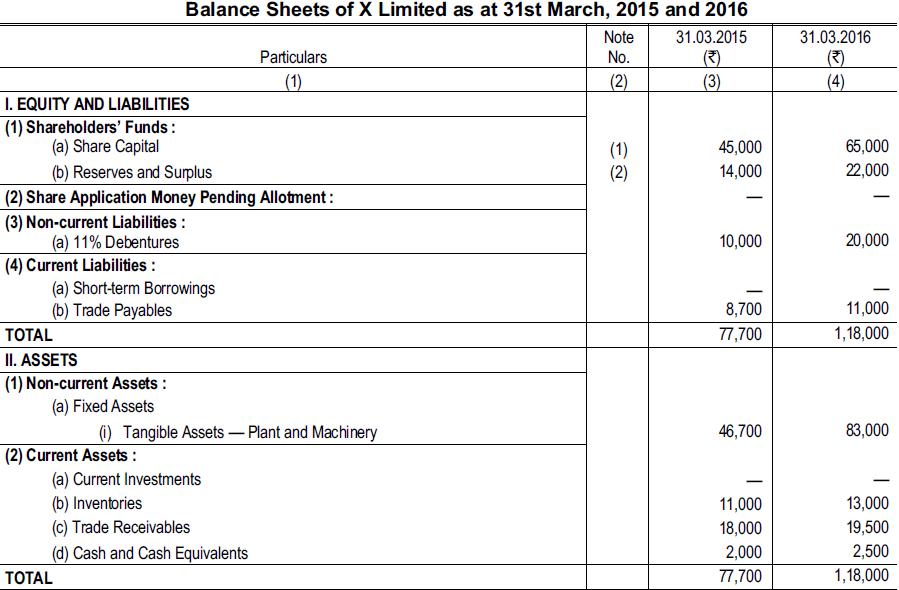

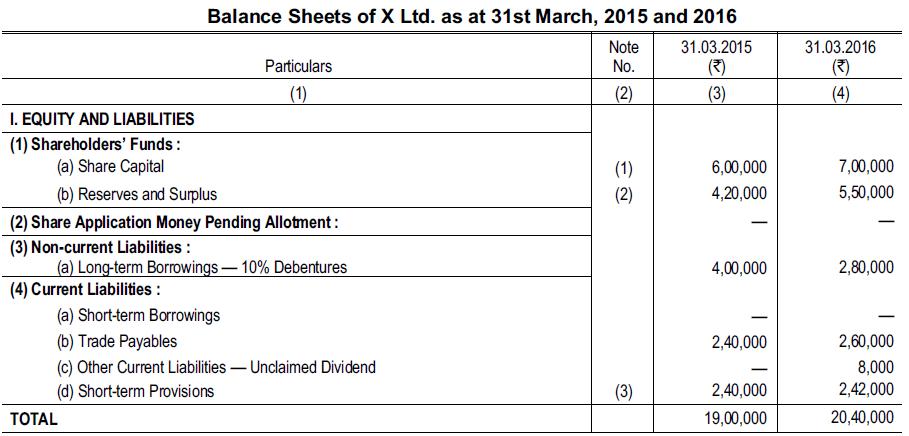

The Balance Sheets of X Limited as at 31.3.2015 and 31.3.2016 were as follows: (4) Current Liabilities: I. EQUITY AND LIABILITIES (1) Shareholders' Funds: (a) Share Capital (b) Reserves and Surplus (2) Share Application Money Pending Allotment: (3) Non-current Liabilities: (a) 11% Debentures (a)

(a) What do you mean by Funds Flow Statement?(b) What are the objectives of Funds Flow Statement?

Collection from debtors ₹ 50,000 would result inA. Sources of fundB. Use of fundC. Neither source or use of fund.

What are the advantages and limitations of Funds Flow Statement?

Increase in net working capital is aA. Source of fundB. Use of fundC. Neither source or use of fund

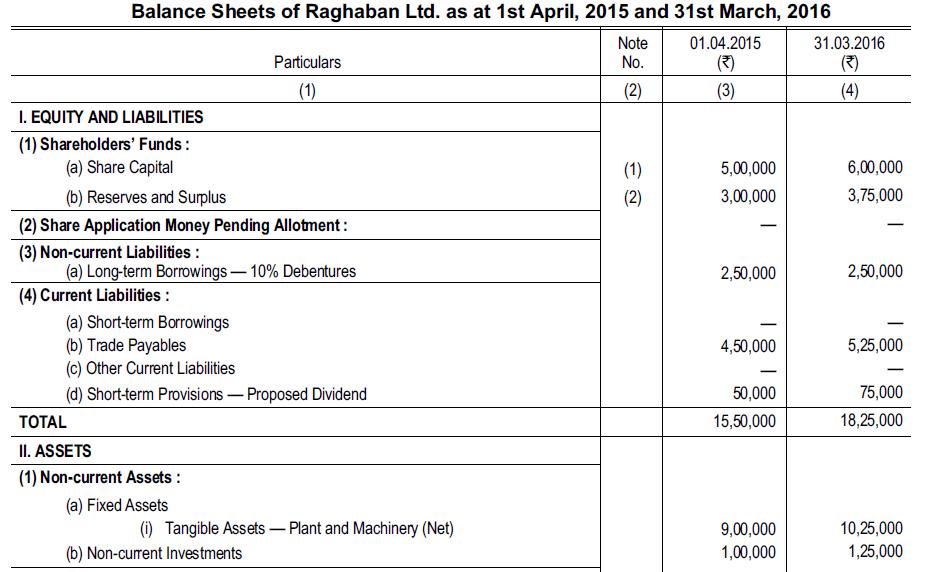

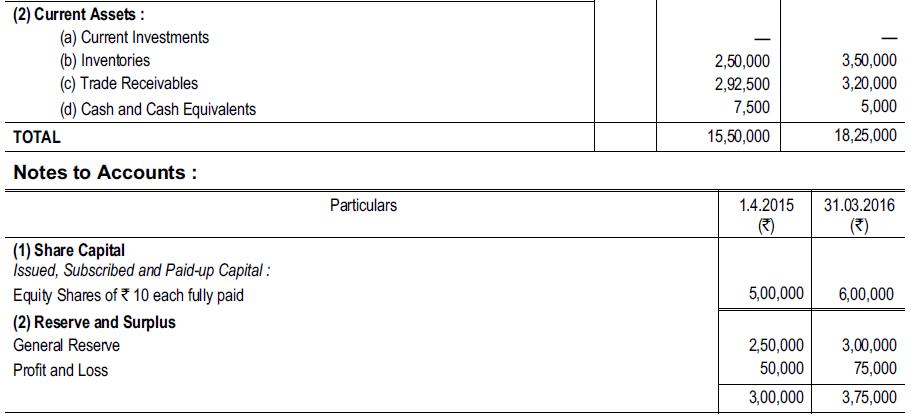

From the following summarised Financial Statement of Raghaban Ltd. as on 1.4.2015 and 31.3.2016 prepare:(a) Statement of Change in Working Capital for the year ended 31.3.2016 and(b) A Statement showing Sources and Application of Fund during the same year.During the year ended 31.3.2016, the

Conversion of debentures into equity share capital is aA. Source of fundB. Use of fundC. Neither source or use of fund

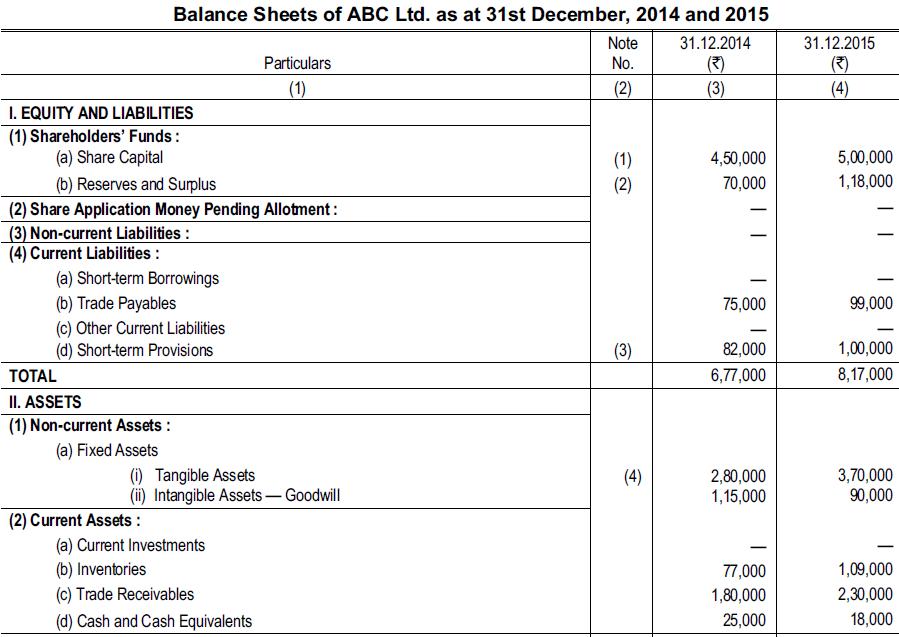

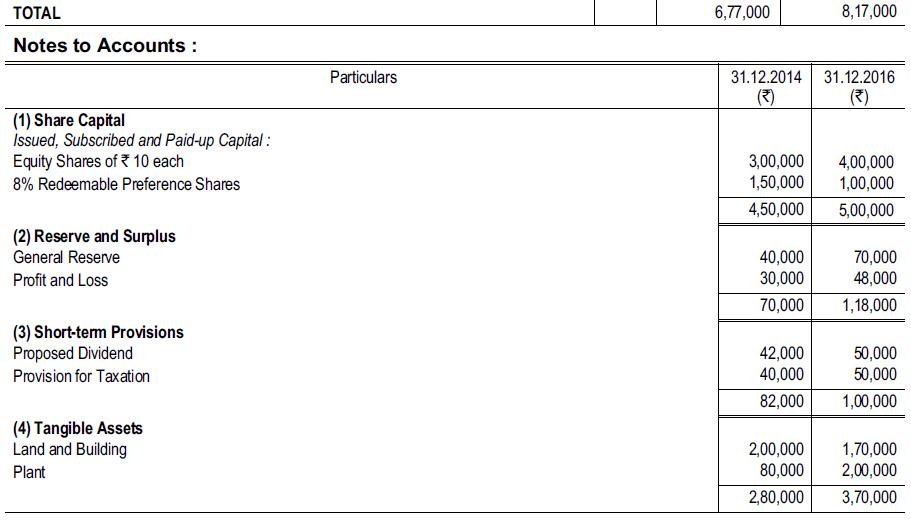

From the following Balance Sheets of ABC Ltd. make out:(i) Statement of Changes in Working Capital;(ii) Funds Flow Statement.Additional information:(a) Depreciation of ₹ 10,000 and ₹ 20,000 were charged on Plant and Buildings respectively in 2015.(b) An interim dividend of ₹ 20,000 was paid

Distinguish between Funds Flow Statement and Cash Flow Statement.

State which of the following transactions would result in source of fundA. Sale of stockB. Sale of old machineryC. Sale of short-term investment

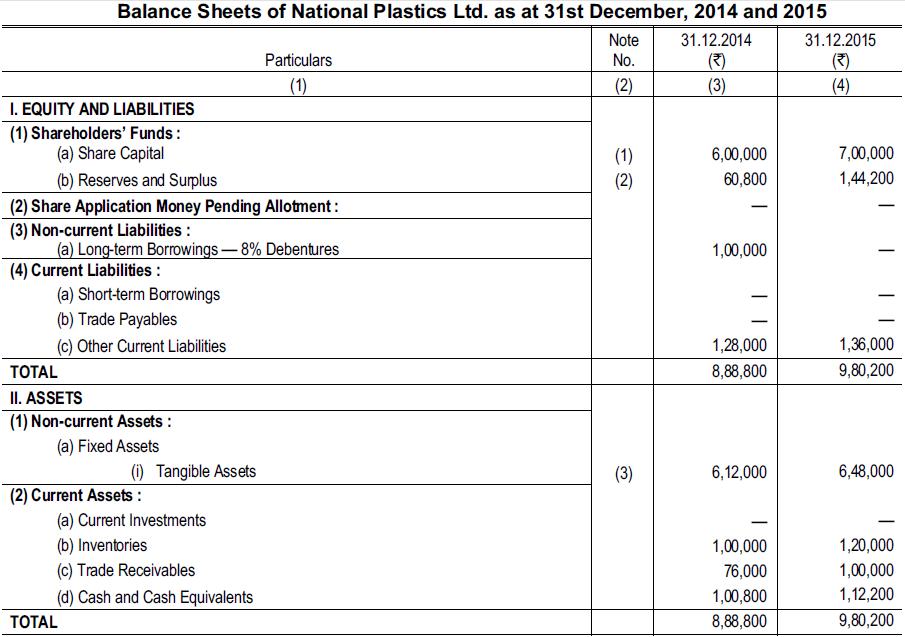

The Balance Sheet of National Plastics Ltd. as on 31.12.2014 and on 31.12.2015 are given below:The entire Share Capital of the Company was issued for cash. Depreciation on Plant and Machinery written off for the year 2015 amounted to ₹ 56,000. During the year, the company paid a dividend of ₹

What are the differenct methods of calculating Funds from Operation?

Prepare(i) A Statement of Changes in Working Capital;(ii) A Funds Flow Statement from the following dataNotes:(a) Fixed assets costing ₹ 1,200 were purchased for cash.(b) Fixed assets (original cost ₹ 400, accumulated depreciation ₹ 150) were sold for ₹ 200.(c) Depreciation for the year

State which of the following transactions would result in use of fundA. Payment to creditorsB. Conversion of preference shares into equity sharesC. Repayment of long term loan

From the following Balance Sheets of XYZ Ltd., make out(i) A Statement of Change in Working Capital;(ii) A Fund Flow Statement for the year 2015.Additional information:(a) A piece of land has been sold out in 2015 and the profit on sale has been credited to Capital Reserve Account.(b) A machine has

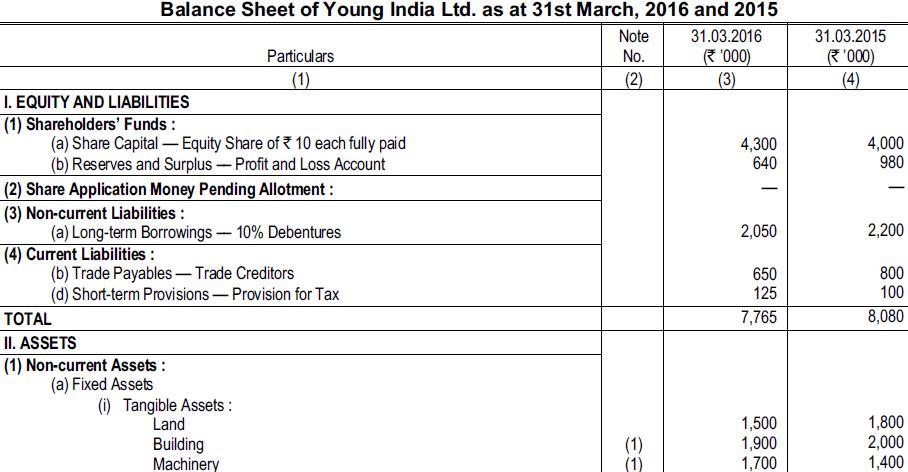

Following are the Balance Sheet of Young India Ltd.:Additional information:(a) Dividend paid during the year ₹ 4,50,000.(b) Land was sold for cash at a profit of ₹ 50,000.(c) Machinery costing ₹ 2,00,000 (W.D.V. ₹ 40,000) was sold for ₹ 30,000. Also machinery costing ₹ 6,00,000 was

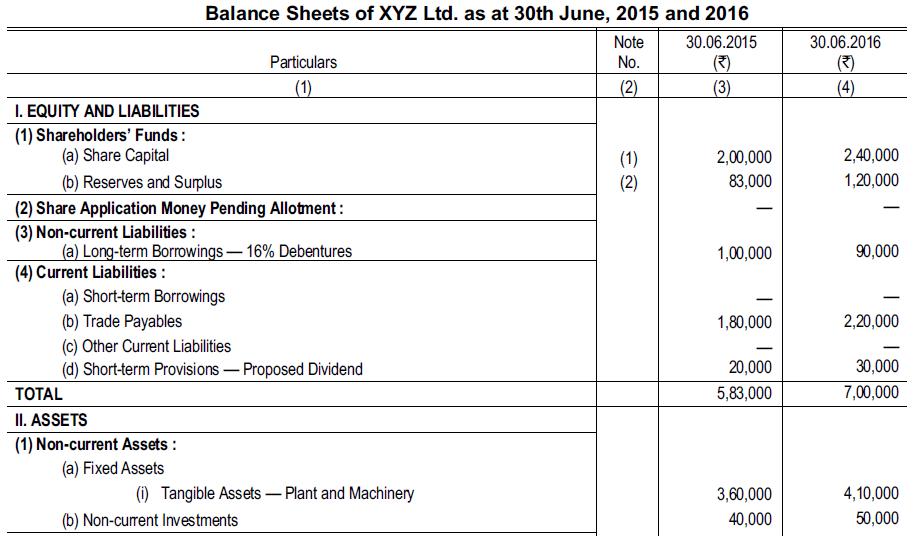

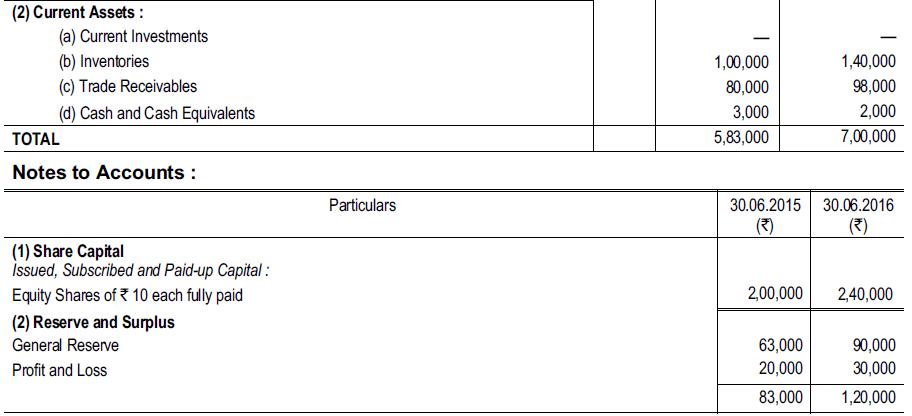

From the following summarised financial statements of XYZ Ltd., as at 30.6.2015 and 30.6.2016, prepare:(i) A statement of change in working capital for the year ended 30.6.2016(ii) A statement showing sources and application of funds during the same period:During the year ended 3.6.2016,

Distinguish between Balance Sheet and Funds Flow Statement.

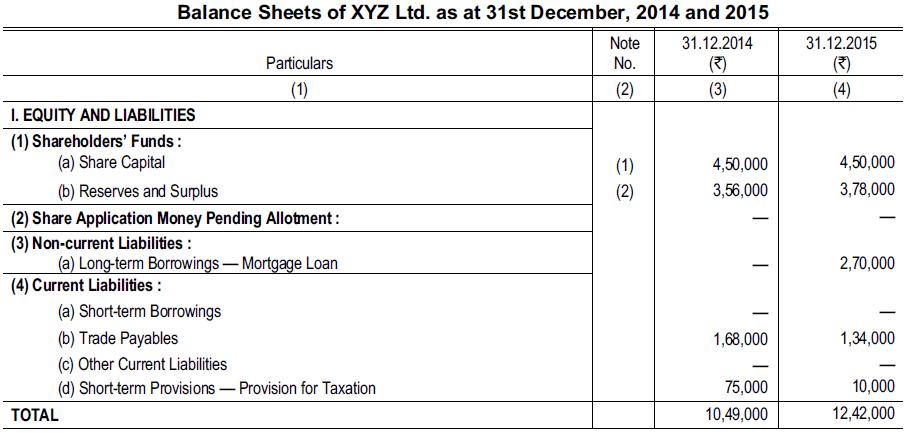

The summarised Balance Sheet of XYZ Ltd. as on 31st December, 2014 and 31st December, 2015 are given below:Additional information:(i) Investments costing ₹ 8,000 were sold during the year 2015 for ₹ 8,500.(ii) Provision for tax made during the year was ₹ 9,000.(iii) During the year part of

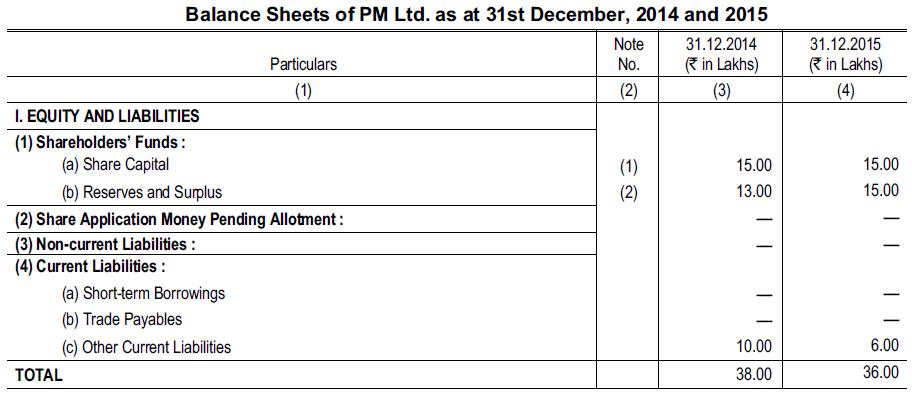

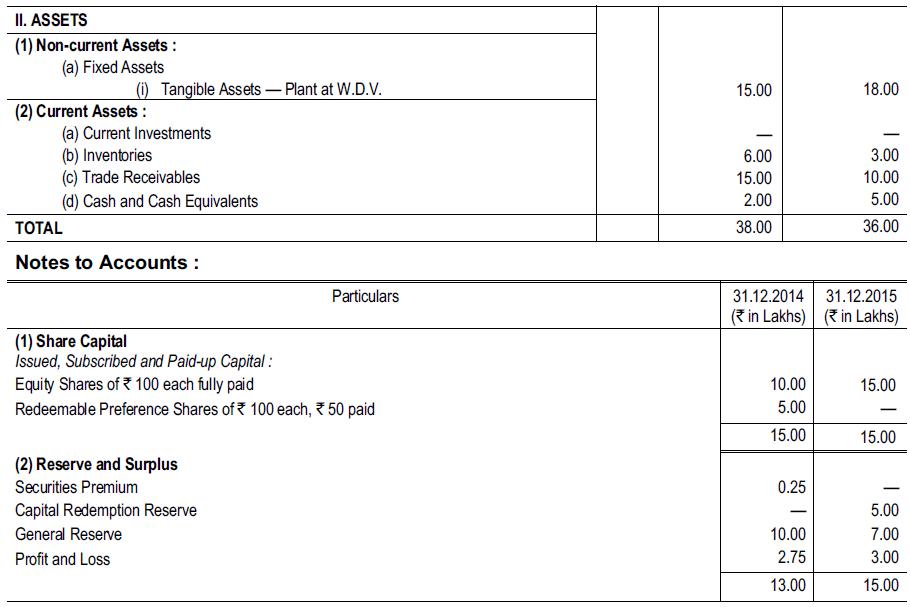

From the following Balance Sheets of PM Ltd. make out ----(i) A Statement of Changes in Working Capital;(ii) A Fund Flow Statement for the year 2015.Additional information:(a) During 2015 the Company paid ₹ 2,00,000 as Equity Dividend and ₹ 56,250 as Preference Dividend.(b) The company redeemed

The summarised Balance Sheets of X Ltd. as on 31st March 2015 and on 31st March 2016 are as follows:During the year ended 31st March 2016 the company:(i) Sold one machine for ₹ 50,000; the cost of the machine was ₹ 1,28,000 and the depreciation provided for it was ₹ 70,000.(ii) Redeemed 30%

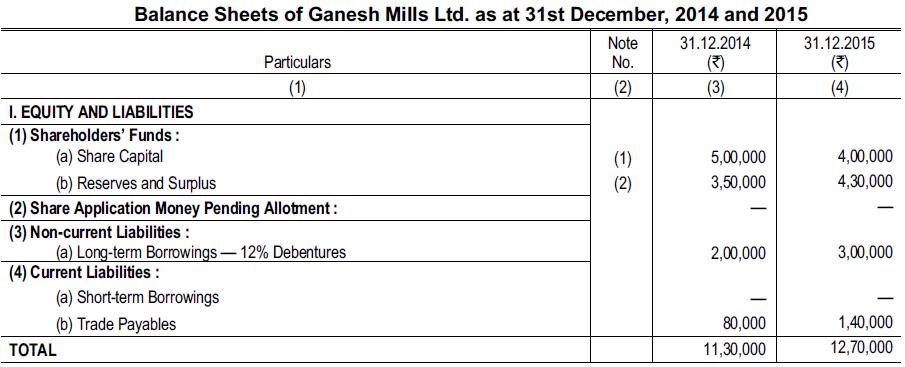

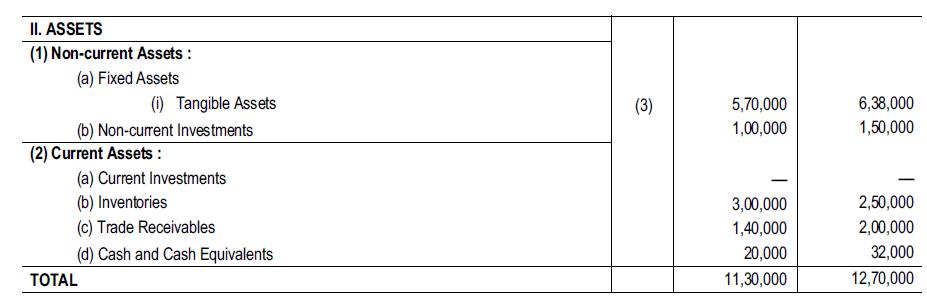

The following is the Balance Sheet of Ganesh Mills Ltd.:The following transactions took place during the year 2015:(a) Preference shares were redeemed at 10% premium.(b) ₹ 20,000 were transferred to Reserve Fund from Profit and Loss Account.(c) Investments (Book value ₹ 40,000) were sold for

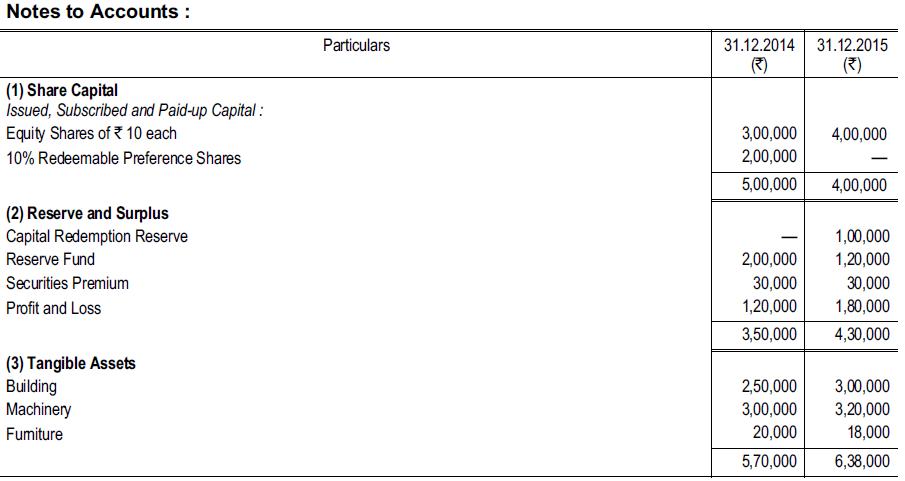

The following are the summaries of the Balance Sheets of AB Ltd. as on 31st December, 2014 and 31st December, 2015:The following additional information is obtained from the General Ledger:(i) During the year ended 31st December, 2015 an interim dividend of ₹ 26,000 was paid.(ii) The assets of

The following information relates to the business of Progressive Ltd for the year ended 31st December, 2015 :(i) The trading results disclosed an operating profit of ₹ 2,50,000.(ii) The position of some Fixed Assets at the year end was as follows:(iii) Construction-in-progress at 31st December,

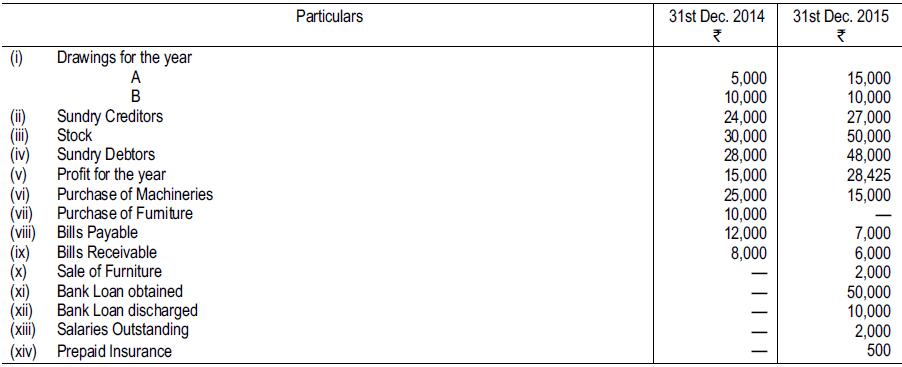

A and B are carrying on business in partnership since January 2014 sharing profits and losses in the ratio of 3 : 2. Not all the necessary books and records have been maintained. However, the following figures have been ascertained from the available records:Cash in hand and at bank amounted to

Ram Ltd had 12,00,000 equity shares on April 1, 2011. The company earned a profit of ₹30,00,000 during the year 2011-12. The average fair value per share during 2011-12 was ₹25. The company has given share option to its employees of 2,00,000 equity shares at option price of ₹15. Calculate

What are the objectives of Ratio Analysis?

Ideal Current Ratio = ?A. 0.75 : 1B. 1 : 1C. 2 : 1D. 4 : 1.

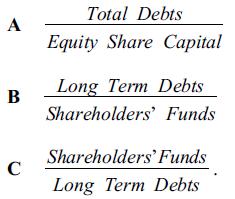

Debt Equity Ratio = ? A B C Total Debts Equity Share Capital Long Term Debts Shareholders' Funds Shareholders' Funds Long Term Debts S

Write short notes on:(a) Current Ratio;(b) Debt-Equity Ratio;(c) Total Assets to Debt Ratio;(d) Operating Ratio.

Quick Liabilities = ?A. Current liabilities - Outstanding expensesB. Current liabilities - Bank overdraftC. Current liabilities + Bank overdraftD. Current liabilities + Surplus

Showing 800 - 900

of 1507

First

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

Step by Step Answers