New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

cost accounting

Cost Accounting Traditions And Innovations 3rd Edition Jesse T. Barfield, Cecily A. Raiborn, Michael R. Kinney - Solutions

What is the focus of activity-based management?LO1

How does the installation of an activity-based costing system affect behavior?LO1

(Appendix) How can the theory of constraints help in determining production flow?LO1

What are the five stages in the product life cycle and why is each important?LO1

Why do costs, sales, and profits change over the product life cycle?LO1

Does target costing require that profitability be viewed on a period-by-period basis or on a long-term basis? Explain.LO1

From a marketing standpoint, why can some companies (such as Seiko and Rub¬ bermaid) introduce products with little or no product research and other com¬ panies cannot?LO1

Why would a cost table be a valuable tool in designing a new product or service?LO1

Discuss the concept of substitute goods and why these would affect pricing.LO1

How would focusing on total life cycle costs call for a different treatment of research and development costs than is made for financial accounting?LO1

Define value-added activities and non-value-added activities; compare and give examples of each type.LO1

What management opportunity is associated with identifying the non-value- added activities in a production process?LO1

How is a process map used to identify opportunities for cost savings?LO1

What is manufacturing cycle efficiency (MCE)? What would its value he in an optimized manufacturing environment and why?LO1

What is a cost driver and how is it used? Give some examples of cost drivers.LO1

Do cost drivers exist in a traditional accounting system? Are they designated as such? How, if at all, does the use of cost drivers differ between a traditional accounting system and an activity-based costing system?LO1

What is activity-based costing? How does it differ from traditional product cost¬ ing approaches?LO1

What characteristics of a company would generally indicate that activity-based costing might improve product costing?LO1

Why does activity-based costing require that costs be aggregated at different levels?LO1

List the benefits of activity-based costing. How could these reduce costs?LO1

How does attribute-based costing extend the concept of activity-based costing?LO1

(Appendix) What is meant by the theory of constraints? How is this concept appropriate for manufacturing and service companies?LO1

(Appendix) Why should quality control inspection points be placed in front of bottleneck operations?LO1

(Terminology) Match the following lettered terms on the left with the appropriate numbered description on the right.27.(Target costing) Headcrafts has developed a new material that has significant po¬ tential in the manufacture of sports caps. The firm has conducted significant market research and

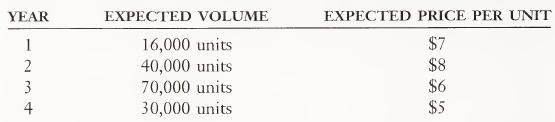

(Target costing) The marketing department at Bernie Manufacturing has an idea for a new product that is expected to have a life cycle of 5 years. After conducting market research, the company has determined that the product could sell for $250 per unit in the first 3 years of life and $175 per unit

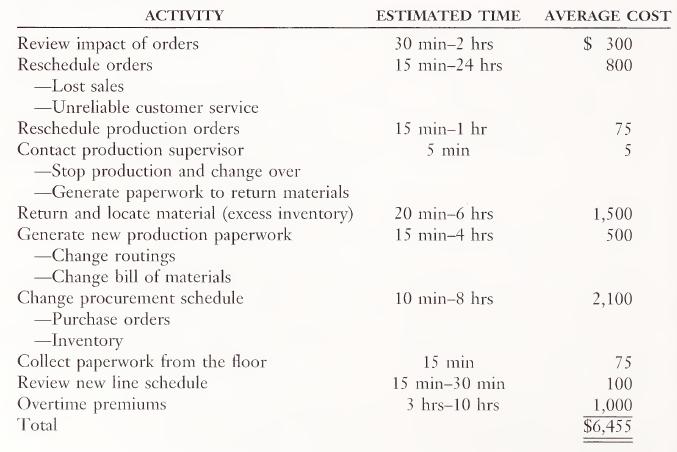

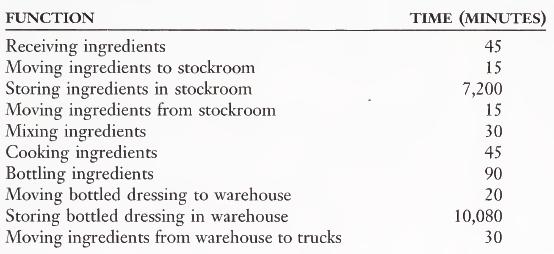

(Activity analysis) Butler Fasteners is investigating the costs of schedule changes in its factory. Following is a list of the activities, estimated times, and average costs required for a single schedule change.a. Which of the above, if any, are value-added activities?b. What is the cost driver in

(Identifying cost drivers) The Lunch Bucket is a highly automated, fast-food res¬ taurant that relies on sophisticated, computer-controlled equipment to prepare and deliver food to customers. Operationally and organizationally, the restaurant operates like other major franchise fast-food

(Cost drivers) For each of the following important costs in manufacturing com¬ panies, identify a cost driver and explain why it is appropriate.a. Equipment maintenanceb. Building utilitiesc. Computer operationsd. Quality controle. Material handlingf. Material storage g. Factory depreciation h.

(Cost allocation using cost drivers) Abramson Inc. has an in-house legal department whose activities fall into one of three major categories. Recently, operating costs in the department have risen dramatically. Management has decided to imple¬ ment an activity-based costing system to help control

(Activity-based costing) Management at Vancouver Ltd. has decided to institute a pilot activity-based costing project in its five-person purchasing department. An¬ nual departmental costs are $473,500. Because finding the best supplier takes the majority of effort in the department, most of the

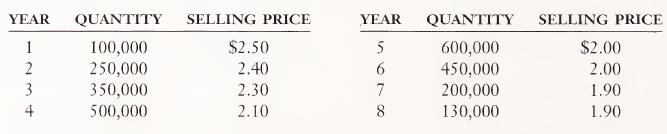

(Product profitability) Innovations manufactures two products: patio lights and commercial pole lights. Patio lights are relatively simple to produce and are made in large quantities. Pole lights must be more customized to individual customer sites. Innovations sells 100,000 patio lights annually

(Appendix) Albright Stationers produces commercial calendars in a two- department operation: Department 1 is labor intensive and Department 2 is automated. The average output of Department 1 is 45 units per hour. The units are then transferred to Department 2 where they are finished by a robot. The

(Product life cycles; team activity) [According to Barry Bayus, a marketing professor, the perception that product life cycles are getting shorter is a mistaken one.] Bayus identified three reasons for the appearance ofshortened product life cycles: 1. New knowledge is being applied faster. The

(Target costing) Snowden Corporation is in the process of developing an outdoor power source for various electronic devices used by campers. Market research has indicated that potential purchasers would be willing to pay $175 per unit for this product. Company engineers have estimated first-year

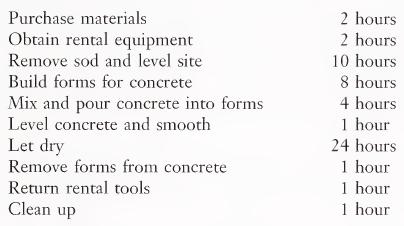

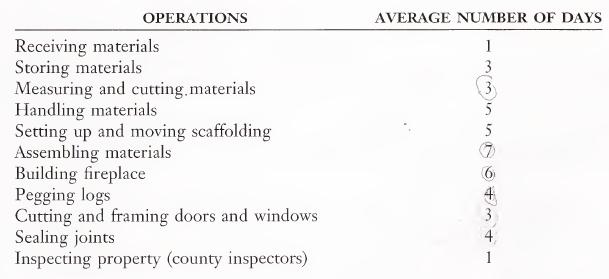

(Value chart) You are the new controller of a small shop that manufactures special-order desk nameplate stands. As you review the records, you find that all the orders are shipped late; the average process time for any order is 3 weeks; and the time actually spent in production operations is 2

(Controlling overhead) Industrial Paints Inc. has engaged you to help the company analyze and update its costing and pricing practices. The company product line has changed over time from general paints to specialized marine coatings. Al¬ though some large orders are received, the majority of

(Traditional vs. ABC methods) Many companies now recognize that their cost systems are inadequate in the context of today’s powerful global competition. Managers in companies selling multiple products are making important product decisions based on distorted cost information, as most cost systems

(Life cycle costing) The Products Development Division of Extralite Cuisine has just completed its work on a new microwave entree. The marketing group has decided on a very high original price for the entree, but the selling price will be reduced as competitors appear. Market studies indicate that

(Activity-based costing) Outdoor Life makes umbrellas, gazebos, and lawn chairs. The company uses a traditional overhead allocation scheme and assigns overhead to products at the rate of $10 per direct labor hour. In 1997, the company produced 100,000 umbrellas, 10,000 gazebos, and 30,000 lawn

(Activity-based costing) Goldstein and Marcus Company manufactures two products.Following is a production and cost analysis for each product for the year 1997.Roberto Lopez, the firm’s cost accountant, has just returned from a seminar on activity-based costing. To apply the concepts he has

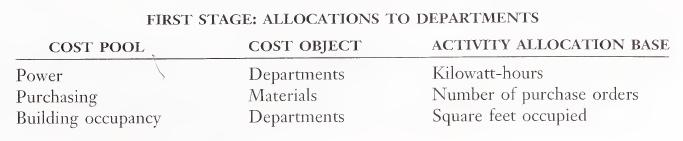

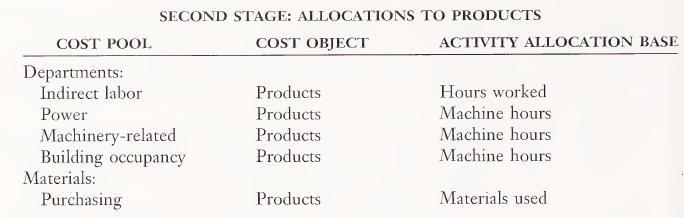

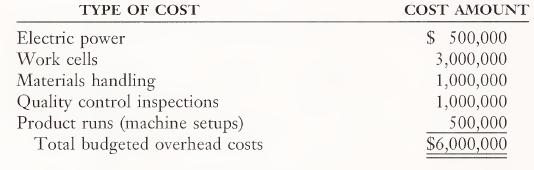

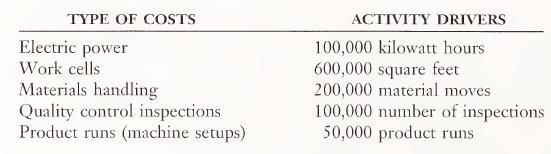

(Using ABC to set price) The budgeted manufacturing overhead costs of Beaver Door Company for 1997 are as follows:For the last 5 years, the cost accounting department has been charging overhead production costs based on machine hours. The estimated budgeted capacity for 1997 is 1,000,000 machine

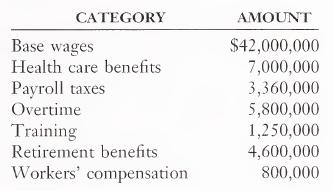

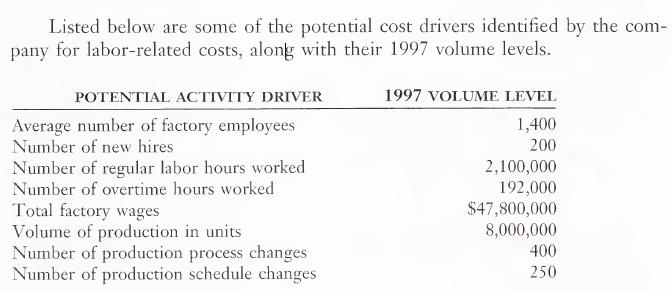

(Activity driver analysis and decision making) Thurgood Products is concerned about its ability to control factory labor-related costs. The company has recently finished an analysis of these costs for 1997. Following is a summary of the major categories of labor costs identified by Thurgood’s

(Activity-based costing and pricing) Covington Community Hospital has found it¬ self under increasing pressure to be accountable for the charges it assesses its patients. Its current pricing system is ad hoc, based on pricing norms for the geographical area, and it only explicitly considers direct

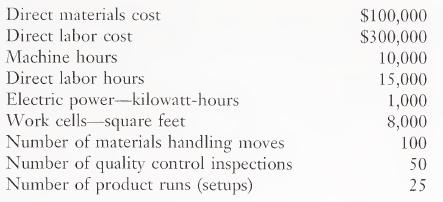

(Determining product cost) Pearson Custom Lumber Products has identified ac¬ tivity centers to which overhead costs are assigned. The cost pool amounts for these centers and their selected activity drivers for 1997 are as follows.a. Determine unit product cost using the appropriate cost drivers

(Product co??ipIexity) Tektronix Inc. is a world leader in the production of elec¬ tronic test and measurement instruments. The company experienced almost un¬ interrupted growth through the 1970s, but in the 1980s, the low-priced end of the Portables Division product line was challenged by an

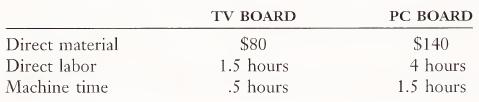

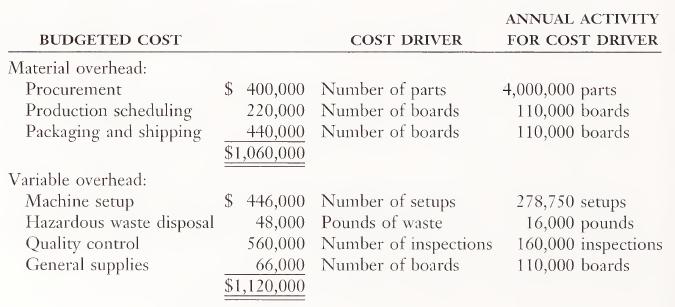

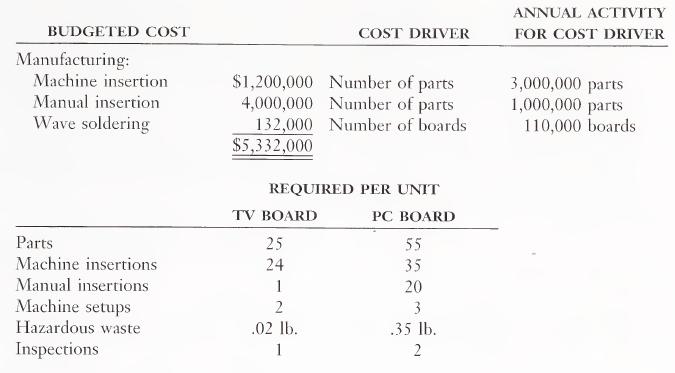

(Activity-based costing) Alaire Corporation manufactures several different types of printed circuit boards; however, two of the boards account for the majority of the company’s sales. The first of these boards, a television (TV) circuit board, has been a standard in the industry for several

(Activity-based costing) Miami Valley Architects Inc. provides a wide range of engineering and architectural consulting services through its three branch offices in Columbus, Cincinnati, and Dayton. The company allocates resources and bonuses to the three branches based on the net income reported

(Activity-based costing and pricing) Steven Haws owns and manages a commercial cold-storage warehouse. He stores a vast variety of perishable goods for his customers. Historically, he has charged customers using a flat rate of $.04 per pound per month for goods stored. His cold-storage warehouse

Many manufacturers are deciding to no longer service small retailers. For ex¬ ample, some companies have policies to serve only customers who purchase $10,000 or more of products from the companies annually. The companies de¬ fend such policies on the basis that they allow the companies to better

Evidence suggests that ABM implementations are more likely to succeed in more open organi¬ zations. The ground is especially fertile for companies that have a stated interest in becoming world-class competitors and have backed these ambitions up with other initiatives. ABM dovetails with these

As the chief executive officer of a large corporation, you have made a decision after discussion with production and accounting personnel to implement activity- based management concepts. Your goal is to reduce cycle time and, thus, costs. A primary way to accomplish this goal is to install highly

Find the IMA (Institute of Management Accountants) home page. Then find and read the article entitled “Practices and Techniques: Implementing Activity- Based Costing.” Write a brief summary of the article noting the major consid¬ erations in designing the implementation of an ABC system.LO1

On the Internet find the Activity Based Cost home page. On this page are discussions of statistical process control, parametric cost analysis, and business process reengineering. Considering the discussion provided, describe how these three tools tie to the concepts of activity based costing and

Included in the ABC materials provided by the IMA (Institute of Management Accountants) on the Internet is a discussion of ABC for logistics. After reading these materials, discuss how activity-based costing can be used to control and allocate the costs of logistics. In your discussion describe

How do job order and process costing systems, and actual, normal, and standard costing valuation methods differ?LO1

In what production situations is a job order costing system appropriate and why?LO1

What purposes are served by the basic documents used in a job order costing system?LO1

(Appendix) How are standard costs used in a job order costing system?LO1

Is allocation of manufacturing overhead to products necessary for external re¬ porting purposes? Internal purposes? Provide explanations for your answers.LO1

Why are departmental overhead rates more useful for managerial decision mak¬ ing than plantwide rates? Separate variable and fixed rates rather than total rates?LO1

Relative to a set of data observations, what is an outlier? Why is it inappropriate to use outliers to determine the cost formula for a mixed cost?LO1

Why would regression analysis provide a more accurate cost formula for a mixed cost than the high-low method?LO1

What is a flexible budget? How is it used to predict or budget future costs?LO1

When a normal cost system is used, how are costs removed from the Manufac¬ turing Overhead account and charged to Work in Process Inventory?LO1

What recordkeeping options are available to account for overhead costs in a normal cost system? Which would be easiest? Which would provide the best information and why?LO1

If overhead was materially underapplied for a year, how would it be treated at year-end? Why is this treatment appropriate?LO1

What factors may cause overhead to be underapplied or overapplied? Are all of these factors controllable by management? Why or why not?LO1

What is a cost pool? Why are multiple cost pools more effective for overhead allocation than single cost pools?LO1

Why is a multistage cost allocation system more effective than a single-stage system?LO1

Define and give four examples of a service department. How do service depart¬ ments differ from operating departments?LO1

Why are service department costs often allocated to revenue-producing depart¬ ments? Is such a process of allocation always useful from a decision-making standpoint?LO1

How might service department cost allocation create a feeling of cost respon¬ sibility among managers of revenue-producing departments?LO1

“There are four criteria to use in selecting an allocation base and all four should be applied equally.” Discuss the theoretical and practical merits of this statement.LO1

How do the direct, step, and algebraic methods of allocating service department costs differ? In what ways are these methods similar?LO1

What are the advantages and disadvantages of the direct, step, and algebraic methods of allocating service department costs?LO1

Why is a benefits-provided ranking necessary in the step method of allocation but not in the algebraic method?LO1

How has the evolution of computer technology enhanced the feasibility of using the algebraic method of service department cost allocation?LO1

(Appendix) How can correlation analysis be used to select an overhead allocation base?LO1

(Appendix) How is the coefficient of determination related to the coefficient of correlation? Can the coefficient of correlation ever be negative? Can the coef¬ ficient of determination ever be negative? Provide justification for your answers.LO1

(High-low method) Information about Brightman Corporation’s utility cost for the first 6 months of 1998 follows. The company’s cost accountant wants to use the high-low method to develop a cost formula to predict future charges and believes that the number of machine hours is an appropriate

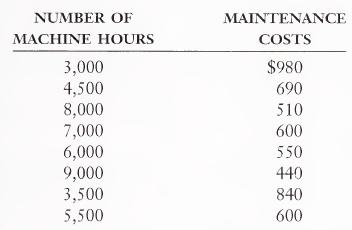

(High-low method) The Charlestonian builds tabletop replicas of some of the most famous lighthouses in North America. The company is highly automated and, thus, maintenance cost is a significant organizational expense. The com¬ pany’s owner has decided to use machine hours as a basis for

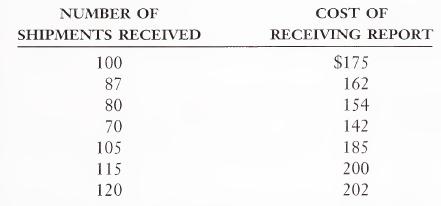

(Least squares) Below are data on number of shipments received and the cost of receiving reports for Savannah Supply Company for the first 7 weeks of 1997:a. Using the least squares method, develop the equation for predicting weekly receiving report costs based on the number of shipments

(Scattergraph; least squares) Richard’s Charters operates a fleet of powerboats in Naples, Florida. Richard wants to develop a cost formula for labor costs (a mixed cost). Fie has gathered the following data on labor costs and two potential pre¬ dictive bases: number of charters and gross

(Calculation offlexible budget) The monthly overhead cost formula for Issac Cor¬ poration is currently estimated as $36,000 T $42X, where X represents machine hours. Company management believes operations will expand into a new relevant range in the upcoming year. Fixed costs are expected to rise

(Flexible budget) Comet-Comet Enterprises produces glass paperweights, each of which requires one-fourth direct labor hour. The relevant range of activity per month is between 4,000 and 7,000 direct labor hours. The following cost for¬ mulas were derived for the company after analyzing cost

(Predetermined overhead rate) Porter Enterprises has developed a monthlv over¬ head cost formula of $2,760 T $4 per direct labor hour for 1997. The firm’s 1997 expected annual capacity is 24,000 direct labor hours, to be incurred evenly each month. Two direct labor hours are required to make one

(Overhead application) Koontz & Associates applies overhead at a combined rate for fixed and variable overhead of 175% of professional labor costs. During the first 3 months of 1997, the following professional labor costs and actual overhead costs were incurred:a. How much overhead was applied

(Underapplied or overapplied overhead) At the end of 1997, Juarez Corporation has the following account balances:a. Prepare the necessary journal entry to close the overhead balance is considered immaterial.b. Prepare the necessary journal entry to close the overhead balance is considered

(Underapplied or overapplied overhead) Rebecca Company uses a normal cost sys¬ tem. At year-end, the balance in the manufacturing overhead control account is a $50,000 debit. Information concerning relevant account balances at year-end are as follows:a. What overhead rate was used during the

(Direct method) Clang Corporation allocates its service department costs to its production departments using the direct method. Information for May 1997 follows:a. What amount of personnel and maintenance costs should be assigned to Fabricating for May?b. What amount of personnel and maintenance

(Direct method) Golden Home Savings Bank has three revenue-generating areas: checking accounts, savings accounts, and loans. The bank also has three service areas: administration, personnel, and accounting. The direct costs per month and the interdepartmental service structure are shown below in a

(Step method) Using the information in exercise 38, compute the total cost for each revenue-generating area using the step method.LO1

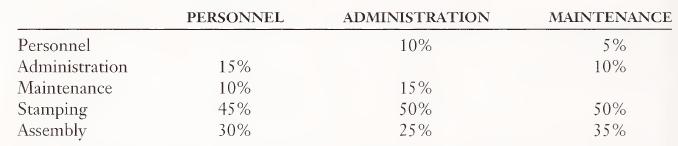

(Step method) Perez Inc. is organized in three service departments (Personnel, Administration, and Maintenance) and two revenue-generating departments (Stamping and Assembly). The company uses the step method to allocate service department costs to operating departments. In October 1997, Personnel

(Algebraic method) Use the information for Golden Home Savings Bank in ex¬ ercise 38 to compute the total cost for each revenue-generating area using the algebraic method.LO1

(Algebraic tnethod) Literary Legends has two revenue-producing divisions (Text¬ books and Trade Publications) and two service departments (Administration and Personnel). Direct costs and allocation bases for each of these areas are presented below:spectively. Use the algebraic method to allocate

(Appendix) Katie’s Kompany is dying to decide whether tons of material pro¬ cessed or machine hours is the better basis on which to predict and allocate its processing costs. The following data display the historical relationships among these variables for the past 8 years (inflation

(Appendix) Refer to the information in exercise 43.a. Using the least squares method, find the processing cost formula for each of the candidate bases.b. Find the standard error of the estimate for each of the bases.c. From your answer in partb, which of the bases is a better predictor of

(Service department allocations) As a team of three or four, select one of the fol¬ lowing types of organizations: hospital or clinic, accounting or law firm, com¬ munity theater, manufacturer, bank, or utility company. Make an appointment with a manager and interview him/her to learn answers to

(Cost allocations) Consider the case of the company that is decentrally organized into five operating divisions. The company pays $150,000 annually to subscribe to the Economic Facts and Projections Hotline (EFPH). This hotline is available via a computer link to all five of the division managers

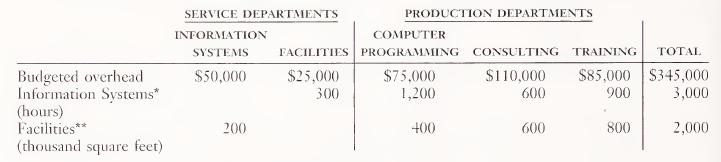

(Service department allocations) Computer Information Services is a computer soft¬ ware consulting company. Its three major functional areas are computer pro¬ gramming, information systems consulting, and software training. Carol Birch, a pricing analyst in the Accounting Department, has been

Showing 2900 - 3000

of 6579

First

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

Last

Step by Step Answers