New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

cost accounting

Cost Accounting Foundations And Evolutions 6th Edition Michael R. Kinney, Jenice Prather-Kinsey, Cecily A. Raiborn - Solutions

Engineered cost variances) Management at Datong Industries has estimated that each quality control inspector should be able to make an average of 12 inspections per hour. Retired factoiy supervisors are excellent quality control inspectors because of their familiarity with the products and

(Revenue variances) The manager of a lumber mill has been asked to ex¬ plain to the company president why sales of scrap firewood were above budget by $4,200. He requests your help. On examination of budget docu¬ ments, you discover that budgeted revenue from firewood sales was $75,000 based on

(Revenue variances) “Snippets” is a videotape series that is marketed to day care centers and parents. The series has been found to make babies who watch it extremely contented and quiet. In 2005, Jaklo Ltd., maker of the tapes, sold 400 of the series for $60 per package. In preparing the 2006

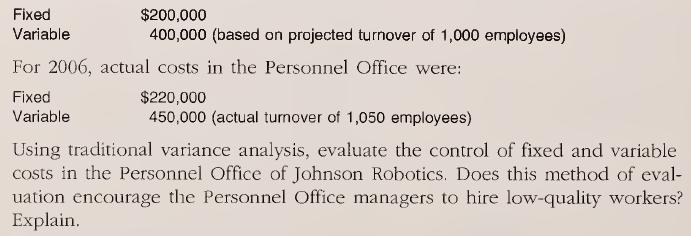

(Variance analysis) Cost control in the Personnel Office of Johnson Robotics is evaluated based on engineered cost concepts. The office incurs both vari¬ able and fixed costs. The variable costs are largely driven by the amount of employee turnover. For 2006, budgeted costs in the Personnel Office

(Cost consciousness; team activity) All organizations seek to be aware of and control costs. In a three- or four-person team, choose one of the following industries and do Web research to identify methods that have been used to control costs.• Internet e-tailers• Automobile manufacturers•

(Cost control) Hello! This communication lays out new guidelines for the spending of money while on Company time. Please look them over. Keep in mind that they are just suggested procedures to help us keep spending in line for the benefit of all. Each individual’s needs and requirements are

(Cost control; financial records) Minnesota Metals is a medium-size manufactur¬ ing corporation in a capital-intensive industry. Its profitability is currently very low. As a result, investment funds are limited and hiring is restricted. These consequences of the corporation’s problems have

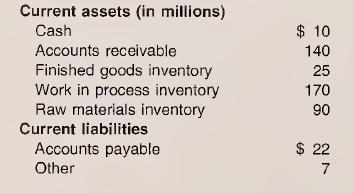

(Cash management) Indianapolis Tire Company manufactures tires that are sold to both car manufacturers and tire wholesalers. The following data have been taken from a recent balance sheet.Discuss recommendations that Indianapolis Tire Company managers could use to improve its cash position. Focus

(e-procurement) You are employed by a firm engaging in heavy manufactur¬ ing. Its direct materials are sourced globally, but its nonoperating inputs are sourced from a variety of U.S. vendors. You have been charged with making a presentation to the CFO about the benefits of e-procurement for

(Coping with uncertainty) You have been assigned the task of projecting the cost of 2008 employee fringe benefits for your firm and have identified number of employees, total labor hours and total labor cost as candidate in¬ dependent variables for use in the estimation equation. Using historical

(Coping with uncertainty) Metalworks, Inc., manufactures a variety of indus¬ trial products from sheet metal. The firm is engaged in its annual process of budgeting costs and revenues for the coming year. The cost of metal con¬ sumes approximately 50 percent of total revenues. Discuss which

(Coping with uncertainty ) Callahan Corp. operates in an industry in which the demand for products is cyclical. The cycles in the industry are often un¬ predictable. Discuss a strategy to deal with uncertainty associated with the cycles that would be appropriate for Callahan Corp. to employ to

(Cost consciousness) Lynn and Tim Robinson are preparing their household financial budget for December. They have started with their November bud¬ get and are adjusting it to reflect the difference between November and De¬ cember in planned activities. The Robinsons are expecting out-of-town

(Cost control) The following graph indicates where each part of the dollar that a student pays for a new college textbook goes.Students are frustrated with the cost of their textbooks, but most pub¬ lishers would say that the selling prices have merely kept pace with infla¬ tion. Buying used

[Efficiency standards) Do Little has been asked to monitor the efficiency and effectiveness of a newly installed machine. The specialized machine has been guaranteed by the manufacturer to package 7,800 engine gaskets per kilowatt hour (kWh). The rate of defects on production is estimated at two

(Effectiveness/eliiciency) Top management of Merlin Magic Stores observed that the budget for the EDP department had been growing far beyond what was anticipated for the past several years. Each year, the EDP manager would demonstrate that increased usage by the company’s non-EDP depart¬ ments

(Effectiveness versus efficiency) Thefounder and president of the Institute for Healthcare Improvement, Donald Berwick, is convinced that the U.S. health care system can reduce costs by 30 percent while improving overall quality—just by getting health care professionals to adopt improvements

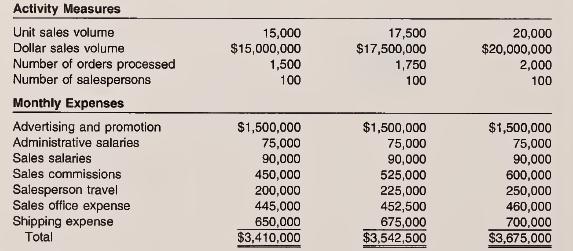

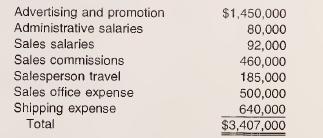

(Budget-to-actual comparison) Buzz Beverages evaluates performance in part through the use of flexible budgets. Selling expense budgets at three activity levels within the relevant range are shown below.The following assumptions were used to develop the selling expense flexible budgets:• The

(Cash management) As the economy entered the new millennium, Internet companies were competing head-to-head in many markets with established, traditional retailers for the consumer’s dollar. In comparing the financial statements of “e-tailers” relative to traditional retailing firms such as

Analyzing cost control) The financial results for the Continuing Education Department of BusEd Corporation for November 2006 are presented in the schedule at the end of this problem. Mary Ross, president of BusEd, is pleased with the final results but has observed that the revenue and most of the

(Clost control) The managers and partners that were interviewed listed re¬ duced manpower costs as the major advantagefor utilizing paraprofessionals [in CPA firms]. It seems that these savings were realized in a number of ways. First, there were significant savings in the salaries

(Supply chain management) Your employer, Southeast Industrial, imple¬ mented an e-procurement system last year for purchasing nonoperating in¬ puts. The installation has been such a success that the firm is now considering using the same system to acquire operating inputs (e.g., direct material

(Coping with uncertainty) After reviewing financial results for 2005, Midtown Industrial’s President sent the following e-mail to his CFO and Controller, Ja¬ son Sharp.DearJason:I'm disappointed in the financial results for the yearjust completed. As you know, profits were $2 million below

(Coping with uncertainty) Stanton Industries manufactures Christmas orna¬ ments in its sole plant located in Wisconsin. Because the demand for the company’s products is very seasonal, the company builds inventory through¬ out the first nine months of the year and draws down inventory the last

HOW ARE THE OUTPUTS OF A JOINT PROCESS CLASSIFIED? LO1.

AT WHAT POINT IN A PROCESS ARE JOINT PRODUCTS IDENTIFIABLE? LO1.

WHAT MANAGEMENT DECISIONS MUST BE MADE BEFORE BEGINNING A JOINT PROCESS? LO1.

HOW IS THE JOINT COST OF PRODUCTION ALLOCATED TO JOINT PRODUCTS? LO1.

HOW ARE BY-PRODUCTS AND SCRAP ACCOUNTED FOR? LO1.

HOW SHOULD NOT-FOR-PROFIT ORGANIZATIONS ACCOUNT FOR JOINT COSTS? LO1.

The possible outputs of a joint process include• joint products—output with a relative high sales value.• by-products—output with a higher sales value than scrap but less than joint products.• scrap—output with a low sales value.• waste—residual output with no sales value. LO1.

Joint products• are identified at the split-off point.• are assigned joint product cost.• could have their costs reduced by the net real¬ izable value of by-products and/or scrap. LO1.

Decisions that must be made in a joint product pro¬ duction process include• two that are made before the joint process is started:>■ Do total revenues exceed total (joint and sep¬ arate) costs?Is this the best use of available facilities?• two that are made at the split-off point:>- Which

Joint cost is commonly allocated to joint products us¬ ing one of two common methods:• physical measures that provide an unchanging yardstick of output over time and treat each unit of product as equally desirable.• monetary measures that consider different valu¬ ations of the individual

By-products and scrap can be accounted for using the• net realizable value (offset) approach in which the NRV of the by-products/scrap reduces either the>- work in process inventory of the joint prod¬ ucts when the by-products/scrap are pro¬ duced>■ cost of goods sold of the joint products

Using some reasonable measure, such as percentage of time or space, not-for-profits must allocate the joint cost incurred for a multipurpose advertisement among the categories of• fund-raising,• program, and/or• administrative activities. LO1.

How does management determine how to classify each type of output from a joint process? Is this decided before or after production? LO1.

In a company that engages in a joint production process, will all processing stop at the split-off point? Discuss the rationale for your answer. LO1.

By what criteria would management determine whether to proceed with processing at each decision point in a joint production process? LO1.

Why is cost allocation necessary in accounting? Why is it necessary in a joint process? LO1.

Compare the advantages and disadvantages of the two primary methods used to allocate joint cost to joint products. LO1.

Why are approximated, rather than actual, net realizable values at split-off sometimes used to allocate joint cost? LO1.

Which of the two common approaches used to account for by-products is better? Discuss the rationale for your answer. LO1.

When are by-product or scrap costs considered in setting the predetermined overhead rate in a job order costing system? When are they not considered? LO1.

Why must not-for-profit organizations allocate any joint costs incurred among fundraising, program, and administrative activities? LO1.

(Essay: Internet) Use the Internet to find five examples of businesses that have joint processes. For each business, describe:a. The various outputs from the processes; using logic, determine whether each output would be classified as a joint product, by-product, scrap, or waste.b. Your

(joint process decision making) Lauren Jackson's aged uncle has asked her to take over the family poultry processing plant. Jackson has learned that you are majoring in accounting—she majored in engineering—and asks you to help her understand the poultry shop business. She would like you to do

(Physical and sales value allocations) Holdsclaw Basketball Camp runs two training camps. During 2006, it generated the following operating data:The general ledger accounts show $38,000 for direct instructional costs and $4,000 for overhead associated with these two programs. The board of trustees

(Physical measure allocation) Swoopes Timber Company uses a joint process to manufacture two grades of wood: A and B. During October 2006, the company incurred $24,000,000 of joint production cost in producing 36,000,000 board feet of grade A and 12,000,000 board feet of grade B wood. The company

(Allocation of joint cost) T. Catchings Fish Processors produces three prod¬ ucts from its fish farm: fish, fish oil, and fish meal. During July 2006, the firm produced the following average quantities of each product from each pound (16 ounces) of fish processed:Of each pound of fish processed, 2

(Sales value allocation) S. Cattle produces milk and sour cream from a joint process. During June, it produced 240,000 quarts of milk and 320,000 pints of sour cream. (There are two pints in a quart.) Sales value at split-off point was $100,000 for the milk and $220,000 for the sour cream. The milk

(Net realizable value allocation) D. Staley Communications is a sports-band network and television company with three sendee groups: Games, News, and Documentaries. In May, the company incurred $12,000,000 of joint product cost for facilities and administration. Revenues and separate produc¬ tion

(Approximated net realizable value method) Hammon Perfume Company makes three products that can either be sold at split-off or processed further and then sold. April’s joint cost is $240,000.The number of ounces of product in each perfume bottle is 3; eau de toi¬ lette is 2; and body splash is

(Processing beyond split-off and cost allocations) Sue Bird Products has a joint process that makes three products from honey for institutional cus¬ tomers. Joint cost for the process is $60,000.A container of honey butter, jam, and syrup includes, respectively, 10 pounds, 6 pounds, and 2 pounds

Sell or process further) Smith Textiles harvests and processes cotton in a joint process that yields two joint products: fabric and yarn. May’s joint cost is $40,000, and the sales values at split-off are $120,000 for fabric and $100,000 for yarn. If the products are processed beyond split-off,

(Processing beyond split-off) Mabika Cannery makes three apple products from a single joint process. For 2006, the cannery processed all three prod¬ ucts beyond split-off. The following data were generated for the year:Analysis of 2006 market data reveals that candied apples, apple jelly, and

(Net realizable value method) Weatherspoon Processing produces fillet, smoked, and canned tuna in a single process. The joint cost is $64,000.a. Assume canned is a by-product, allocate the joint cost based on net re- alizable value at split-off. Use the net realizable value method to account for

(By-product accounting method selection) The company you work for en- gages in numerous joint processes that produce significant quantities and types of by-products. You have been asked to give a report to management on the best way to account for by-products. Develop a set of criteria for making

(Monetary measure allocation) Teasley Realty has two operating divisions: Rental and Sales. In March 2006, the firm spent $25,000 for general company promotions (as opposed to advertisements for specific properties). Lisa Leslie, the corporate controller, now has the task of fairly allocating the

(By-products and cost allocation) Yolanda Salsa has a joint process that yields three grades of tomatoes: premium, good, and fair. Joint cost is allo¬ cated to products based on bushels of output. One particular joint process batch cost $240,000 and yielded the following bushels of output:The

Sell or process further) Penicheiro Clothing produces precut fabrics for three products: dresses, jackets, and blouses from a joint process. Joint cost is al¬ located on the basis of relative sales value at split-off. Rather than sell the products at split-off, the company has the option to

(By-products and cost allocation) Dales-Schumantions Productions produced the movies Rare Debits & Credits and Rare Debits & Credits: The Sequel from the same original footage that cost $16,000,000. The company, therefore, considers these two movies as joint products. Because of the superb

(Accounting for by-products) Tamecka Company manufactures various wood products that yield sawdust as a by-product. Selling costs associated with the sawdust are $4 per ton sold. The company accounts for sawdust sales by deducting the sawdust’s net realizable value from the major products’ cost

(Accounting for by-products) In making frozen hash browns and potato chips, Azzi Potato Inc. generates potato skins as a by-product. It sells the potato skins to restaurants for use in appetizers. The processing and disposal costs associated with the sales of the by-product are $0.10 per pound of

(Accounting for by-products) Bolton-Holifield EDP provides computing ser¬ vices for its commercial clients. Records for clients are maintained on both computer files and paper files. After seven years, the company sells the pa¬ per records for recycling material.The net realizable value of the

(Accounting for scrap) Renaissance Creations restores antique stained glass windows. On all jobs, it generates some breakage or improper cuts. This scrap can be sold to amateur stained glass hobbyists. Renaissance Creations expects to incur approximately 30,000 direct labor hours during 2006. The

(Scrap; job order costing) Ruthie Architects offers a variety of architectural services for commercial construction clients. For each major job, architectural models of the completed structures are built for client presentations. The company uses a job order cost system. At the completion of a job,

(Net realizable value versus realized value) Indicate whether each item that follows is associated with (1) the realized value approach or (2) the net real¬ izable value approach.a. has the advantage of better timingb. ignores value of by-product/scrap until it is soldc. is easierd. is used to

(Not-for-profit program and support cost allocation) Kansas City Jazz Com¬ pany is preparing a pamphlet that will provide information on the types of jazz, jazz terminology, and biographies of some of the more well-known jazz musicians. In addition, the pamphlet will include a request for funding

(Web research) Go to the Web site for Perdue Farms Incorporated at http://www.perdue.coyn where the company provides information regarding its philosophies, product lines, strategy, and production systems. Review the information provided and then discuss how an operating environment such as

(Journal entries) Desirable Inc. uses a joint process to make two main prod¬ ucts: Forever perfume and Fantasy lotion. Production is organized in two se¬ quential departments: Combining and Heating. The products do not become separate until they have been through the heating process. After

Physical measure joint cost allocation) Lakeside Dairy began operations at the start of May. The company was founded by local dairy farmers to en¬ hance competition in the market for milk products produced by the farmers. 35. (Journal entries) Desirable Inc. uses a joint process to make two main

(Monetary measure joint cost allocation) Refer to the information in Problem 36.a. Calculate the sales price per pound for skim milk and cream.b. Using relative sales value, allocate the joint cost to the joint production. C. Calculate the cost of goods sold, cost of ending finished goods inven¬

(Physical measure joint cost allocation) Midwest Soybeans operates a process¬ ing plant in which soybeans are “crushed” to create soybean oil and soy¬ bean meal. The company purchases soybeans by the bushel (60 pounds). From each bushel, the normal yield is 11 pounds of soybean oil, 44 pounds

Monetary measure joint cost alloc.:' >n Refer to the information in Problem 38.a.Assume the net realizable value of the joint products is as follows:Soybean oil Soybean meal $0,339 per pound $0,169 per pound Allocate the joint cost incurred in March on the basis of net realizable value.b. Calculate

(Joint cost allocation; by-product; income determination) St. Cloud Bank & Trust has two main service lines, commercial checking and credit cards. The firm also generates some revenue from selling antitheft and embezzlement insurance as a by-product of its two main services. Joint costs for

(Joint cost allocation; scrap) Kelly’s Linens produces cloth products for ho¬ tels. The company buys fabric in 60-inch-wide bolts. In the first process, the fabric is set up, cut, and separated into pieces. Setup can be for either robes and bath towels or hand towels and washcloths.During July,

(joint products: by-product) Georgia Peach runs a fruit-packing business in central Georgia. The firm buys peaches by the truckload in season and sep¬ arates them into three categories: premium, good, and fair. Premium can be sold as is to supermarket chains and specialty gift stores. Good is

(Process costing; joint cost allocation; by-product) Michelle’s Fitness Center provides personal training services and sells a variety of apparel products for its clients. The center also generates some revenue from the sale of used towels, which are periodically sold to a rag-rug manufacturer.

(joint cost allocation; by-product) Muriel Orange Company produces orange juice and orange marmalade from a joint process. In addition, second-stage processing of the marmalade creates a residue mixture of orange pulp as a by-product. The company sells pulp for $0.08 per gallon. Expenses to dis¬

(By-product/joint product journal entries) Kansas Wheat Agricultural is a 5,000-acre wheat farm, which produces two principal products, wheat and straw. It sells wheat for $3.50 per bushel (assume that a bushel of wheat weighs 60 pounds). Without further processing, it sells the straw for $30 per

(Ending inventory valuation; joint cost allocation) During March 2006, the first month of operations, Nikki Dean’s Pork Packing Co. had the operating sta¬ tistics shown in the following table. Costs of the joint process were direct material, $40,000; direct labor, $23,400; and overhead, $10,000.

(Essay: ethics) Some waste, scrap, or by-product material have little value.In fact, for many meat and poultry producers, animal waste represents a sig¬ nificant liability because it is considered hazardous and requires significant disposal costs. For example, one environmental group filed a

WHY DO ORGANIZATIONS HAVE MANAGEMENT CONTROL SYSTEMS? LO.1

WHAT IS A COST MANAGEMENT SYSTEM, AND WHAT ARE ITS PRIMARY GOALS? LO.1

WHAT MAJOR FACTORS INFLUENCE THE DESIGN OF A COST MANAGEMENT SYSTEM? LO.1

WHAT THREE GROUPS OF ELEMENTS AFFECT THE DESIGN OF A COST MANAGEMENT SYSTEM, AND WHAT ARE THE PURPOSES OF THESE ELEMENTS? LO.1

WHAT IS GAP ANALYSIS, AND HOW IS IT USED IN THE IMPLEMENTATION OF A COST MANAGEMENT SYSTEM? LO.1

Organizations have management control systems to• implement strategic and operating plans.• provide a means for comparison of actual to planned results for management control purposes. LO.1

A cost management system (CMS)• is a set of formal methods developed for plan¬ ning and controlling an organization's cost¬ generating activities relative to its short-term objectives and long-term strategies.• has a short-term goal of making efficient use of organizational resources.• has

The design of a CMS is influenced by the• organizational form through, for example, laws that determine who within the organization is en¬ titled to be a decision maker.• organizational structure because it>- determines how authority and responsibility are distributed in an organization.>-

Elements that affect the design of a CMS are• motivational, which is used to influence man¬ agers and employees to exert high effort and to act in the organization’s interests.• informational, which is selected to provide the appropriate information to managers who are re¬ sponsible for

Gap analysis• is a tool that can help identify and prioritize nec¬ essary changes in a CMS.• assesses differences between an organization’s ideal CMS and the organization’s existing CMS. LO.1

How can a company evaluate whether it is effectively managing its costs? LO.1

What is a control system? What purpose does a control system serve in an organization? LO.1

Why does a cost management system necessarily have both a short-term and long-term focus? LO.1

Why is it not possible simply to take a cost management system “off the shelf”? LO.1

How does the choice of organizational form influence the design of a firm’s cost management system? LO.1

What information could be generated by a cost management system that would help an organization manage its core competencies? LO.1

How could an organization’s culture be used as a control mechanism? LO.1

Showing 3600 - 3700

of 6579

First

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

Last

Step by Step Answers