New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

cost accounting

Cost Accounting Foundations And Evolutions 6th Edition Michael R. Kinney, Jenice Prather-Kinsey, Cecily A. Raiborn - Solutions

How does a product’s life-cycle stage influence the nature of information re¬ quired to successfully manage costs of that product? LO.1

In the present highly competitive environment, why has cost management risen to such a high level of concern while price management has declined in importance? LO.1

(Appendix) What was CAM-I, and why was it organized? LO.1

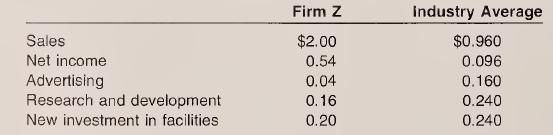

(Cost management and strategy) As a financial analyst, you have just been handed a 2006 financial report of Firm Z, a large, global pharmaceutical company. Firm Z competes in both traditional pharmaceutical products and in evolving biotechnology products. The following data (in billions) on Firm Z

(Cost management and strategy) Following are descriptions of three busi¬ nesses. For each, assume that you are the CEO. Identify the most critical in¬ formation you would need to manage the strategic decisions of that business.a. Private hospital that competes on the basis of delivering

Organizational form) Write a paper that compares and contrasts the corpo¬ rate, general partnership, limited partnership, LLP, and LLC forms of busi¬ ness. At a minimum, discuss issues related to formation, capital generation, managerial authority and responsibility, taxation, ownership

(Cost management and organizational culture) Use Internet resources to gather information on any two firms in the same industry. The following ex¬ amples are possible pairs to compare.• Delta Air Lines and Southwest Airlines• ChevronTexaco and BP• Nordstrom’s and Wal-Mart• Oracle and

(Cost management and technology) Many finns now engage in some form of B2B Internet-based commerce. A specific type is B2B buy-side, which is In¬ ternet technology that allows firms to solicit bids on inputs that the firms re¬ quire to support production, sales, and administration. Interested and

(Organizational strategy) Lise Internet resources to find a company (regard¬ less of where it is domiciled) whose managers have chosen to (a) avoid competition through differentiation, (b) avoid competition through cost leadership, and (c) confront competitors head on. Analyze each of these

(Cost management and organizational objectives) Prepare an oral presentation discussing how accounting information can (a) help and (b) hinder an orga¬ nization’s progress toward its mission and objectives. Be sure to differentiate between the effects of what you perceive as “traditional”

Organizational culture) Write a paper describing the organizational culture at a job you have held or at the college or university that you attend. Be sure to include a discussion of the value system and how it was communi¬ cated to new employees or new students.LO.1

(Cost management and strategy) You are the product manager at a silicone chip manufacturer. One of your products is a commodity chip that the elec¬ tronics industry widely uses in cell phones, printers, digital cameras, and so forth. As product manager, you have full profit responsibility for the

(Information and cost management) The price of a product or service is a function of the total costs of producing that product or service. In turn, the total cost of producing a product or service is a function of the aggregate of costs incurred throughout the supply chain.Higher education is one

(Alternative cost management strategies) In 1993, Procter & Gamble (P&G) management tried to control costs by eliminating many of its brands’ coupons while increasing print advertising. Only a miniscule portion of tire hundreds of billions of coupons distributed annually by P&G were ever redeemed

(Cost management and customer service) Companies sometimes experience difficult financial times, sometimes so drastic that they declare bankruptcy. If a firm either does not conduct sufficient R&D or if its R&D is not sufficiently effective, it will soon find that many of its products are in the

(Cost management: short term vs. long term) Northwest Metals Co. produces steel products for a variety of customers. One division of the company is Residential Products Division, created in the late 1940s. Since that time, this division’s principal products have been galvanized steel components

(Cost management and profitability) After graduating last year from an Ivy League university, Jill Young was hired as a stock analyst. Wanting to make her mark on the industry, Young issued a scathing report on a major dis¬ count department store retailer, Smart-Mart. The basis of her attack was a

(Cost management; product life cycle) In May 2004, Krispy Kreme Dough¬ nuts issued a profit warning to investors. In the warning, the company indi¬ cated full-year earnings would be 10 percent below previous expectations.In the weeks immediately following the profit warning, the stock price of

(Stakeholders; cost management) Laura Thompson, newly appointed con¬ troller of Allied Networking Services Inc. (ANSI), a rapidly growing com¬ pany, has just been asked to serve as lead facilitator of a team charged with designing a cost management system (CMS) at ANSI. Also serving on the team

(CMS; MIS; ethics in reporting) The value of an oil and gas company is tied to two fundamental circumstances. The first is the amount of oil and gas the company is presently producing. This amount, along with unit prices, deter¬ mines the revenue and cash inflow that the company generates. The

(Cost management; social responsibility) Through its three sets of elements (motivational, informational, and reporting), a CMS focuses the attention of a given decision maker on the data and information that are crucial to that de¬ cision maker’s responsibilities in the organization. However,

WHICH ORGANIZATIONAL CHARACTERISTICS DETERMINE WHETHER A FIRM SHOULD BE DECENTRALIZED OR CENTRALIZED? LO.1

HOW ARE DECENTRALIZATION AND RESPONSIBILITY ACCOUNTING RELATED? LO.1

WHAT ARE THE DIFFERENCES AMONG THE FOUR PRIMARY TYPES OF RESPONSIBILITY CENTERS? LO.1

WHY AND HOW ARE SERVICE DEPARTMENT COSTS ALLOCATED TO REVENUE-PRODUCING DEPARTMENTS? LO.1

WHAT TYPES OF TRANSFER PRICES ARE USED IN ORGANIZATIONS, AND WHY ARE SUCH PRICES USED? LO.1

WHAT DIFFICULTIES CAN BE ENCOUNTERED BY MULTINATIONAL COMPANIES USING TRANSFER PRICES? LO.1

Decentralization is generally appropriate for compa¬ nies that• are mature.• are large.• are in a growth stage of product development.• are expanding operations rapidly.• can financially withstand incorrect decisions.• have high confidence in the employees’ decision¬ making

Decentralization and responsibility accounting are re¬ lated in that decentralization• is made to work effectively though the use of re¬ sponsibility accounting which provides informa¬ tion about the performance, efficiency, and effectiveness of organizational responsibility cen¬ ters and

The four primary types of responsibility centers and the characteristics of each are• cost centers in which managers are primarily re¬ sponsible for controlling costs.• revenue centers in which managers are primar¬ ily responsible for generating revenues; in some instances, managers have

Service department costs are allocated to producing departments• to meet the objectives of full cost computation, managerial motivation, or managerial decision making.• by using the direct, step, or algebraic method.>- The direct method assigns service depart¬ ment costs only to

Transfer prices, or intracompany charges for goods or services bought and sold between segments of a decentralized company, are• typically cost based, market based, or negotiated; a dual pricing system can also be used to assign different transfer prices to the selling and buying units.• set

Multinational companies using transfer prices en¬ counter difficulties including• differences in tax systems, customs duties, freight and insurance costs, import/export regulations, and foreign-exchange controls.• the ability to determine what transfer price would be considered

Bill Barnes is the president and chief operating officer of Barnes Electronics. He founded the company and has led it to its prominent place in the elec¬ tronics field. He has manufacturing plants and outlets in 40 states. Barnes is finding, however, that he cannot “keep track’’ of things

Why are responsibility reports prepared? Is it appropriate for a single re¬ sponsibility report to be prepared for a division of a major company? Why or why not? LO.1

What is suboptimization, and what factors contribute to it in a decentralized firm? LO.1

Why are service department costs often allocated to revenue-producing de¬ partments? Is such an allocation process always useful from a decision-making standpoint? How might service department cost allocation create a feeling of cost responsibility among managers of revenue-producing

“The four criteria for selecting an allocation base for service department costs should be applied equally.” Discuss the merits of this statement. LO.1

Compare and contrast the direct, step, and algebraic methods of allocating service department costs. What are the advantages and disadvantages of each method? LO.1

When the algebraic method of allocating service department costs is used, to¬ tal costs for each service department increase from what they were prior to the allocation. Why does this occur, and how are the additional costs treated? LO.1

What are transfer prices, and why do companies use them? How could the use of transfer prices improve or impair goal congruence? LO.1

Would transfer prices be used in each of the following responsibility centers: cost, revenue, profit, and investment? If so, how would they be used? LO.1

What problems might be encountered when attempting to implement a cost- based transfer pricing system? A market-based transfer price system? LO.1

What is dual pricing? What is the intended effect of dual pricing on the per¬ formance of each division affected by the dual price? LO.1

How can service departments use transfer prices, and what advantages do transfer prices have over cost allocation methods? LO.1

Explain why the determination of transfer prices could be more complex in a multinational setting than in a domestic setting. LO.1

(Centralization versus decentralization) Indicate whether a firm exhibiting each of the following characteristics would more likely be centralized (C) or decentralized (D).a. Two years oldb. Growth stage of product development C. Tight management controld. Widely dispersed operating unitse. Waiy of

(Decentralization advantages and disadvantages) Indicate whether each of the following is a potential advantage (A) or disadvantage (D) of decentraliza¬ tion. If an item is neither an advantage nor a disadvantage, use N.a. Provision of increased job satisfactionb. Development of leadership

(Decentralization; Internet) Search the Internet to identify three decentralized companies. Based on the information you find on each, either determine di¬ rectly or infer from the information given the types of responsibility centers used by these companies. Also, determine or speculate about

Profit centers and allocations) Multiple-doctor medical practices are often structured with each doctor acting as a profit center.a. Discuss why such an organizational structure would be useful.b. Go to the Web and find some software packages that could be used to account for such an organizational

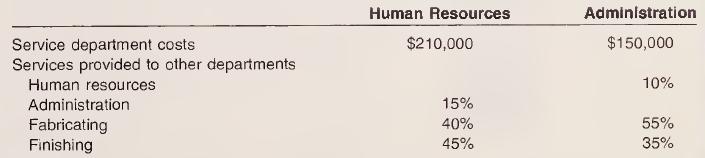

(Direct method) Adelaide Corporation uses the direct method to allocate ser¬ vice department costs to production departments (Fabricating and Finishing). Information for June 2006 follows:a. What amounts of human resource and administration costs should be as¬ signed to fabricating for June?b.

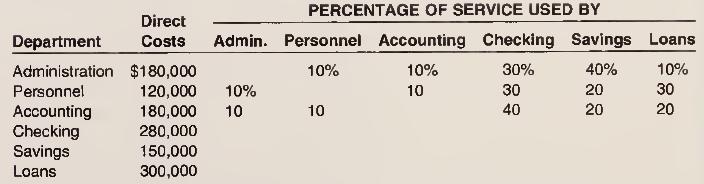

(Direct method) Imbornone Bank has three service areas (administration, personnel, and accounting) and three revenue-generating areas (checking ac¬ counts, savings accounts, and loans). Monthly direct costs and the interde¬ partmental service structure are shown in the following benefits-provided

(Step method) Use the information in Exercise 20 to compute total cost for each revenue-generating area if the bank allocates costs under the step method of cost allocation. LO.1

(Step method) Rapp Company has three service departments (human re¬ sources, administration, and maintenance) and two revenue-generating de¬ partments (assembly and finishing). It uses the step method to allocate service department costs to operating departments. In October 2006, human resources

(Algebraic method) Use the information for Imbornone Bank in Exercise 20 to compute the total cost for each revenue-generating area using the alge¬ braic method. LO.1

(Algebraic method) The following chart indicates the percentage of service department services used by other departments. Service departments are des¬ ignated SI, S2, and S3; revenue-producing departments are designated RP1 and RP2.Costs of the period were $112,000, $240,000, and $360,000 for SI,

(Transfer pricing in service departments) Indicate whether each of the fol¬ lowing statements constitutes a potential advantage (A), disadvantage (D), or neither (N) of using transfer prices for service department costs.a. Can increase resource wasteb. Can make a service department into a profit

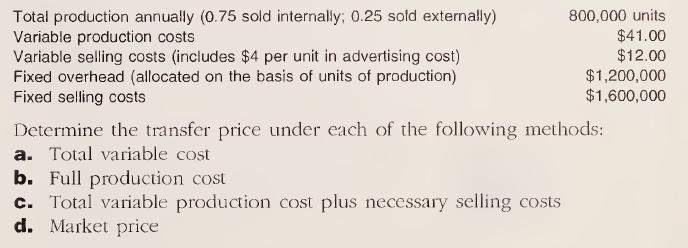

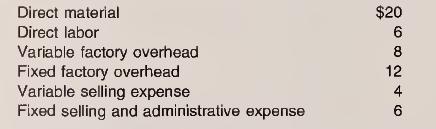

(Transfer pricing) Irmela Division, a subsidiary of Siberia Ltd., manufactures computer chips with the following costs:Some of the chips are sold externally for $108.75; others are transferred in¬ ternally to the Gerhardt Division. Irmela Division’s plant manager wants to establish a reasonable

Transfer pricing) Electronics and Appliances are two investment centers of At-Home Company. Electronics produces a microprocessor used by Appli¬ ances to manufacture several of its products; the microprocessor is also sold externally for $102.40. The following information is available about the

Transfer pricing) Lafayette Co., a profit center of Creole Enterprises, manu¬ factures brake pads to sell internally to other company divisions and exter¬ nally. A set of Lafayette brake pads normally sells for $36. Production and selling costs for a set of brake pads follow:Hammond Co., another

(Transfer pricing and management motivation) Yummy’s Food Stores operates 20 large supermarkets in the Midwest. Each store is evaluated as a profit cen¬ ter, and store managers have complete control over their purchases and inven¬ tory policy. Company policy is that transfers between stores

(Transfer pricing for sen ices) Walsdorf Company’s information technology department is developing a service department transfer price based on min¬ utes of computer time. For 2006, its expected capacity was 350,000 minutes, and theoretical capacity was 500,000 minutes. Costs of the IT

(Web research) Use the Internet to identify a multinational company encoun¬ tering tax problems related to transfer pricing between its organizational units in different countries. Prepare a brief discussion of the issues and the actual or potential consequences. LO.1

(Decentralization; ethics) A large U.S. corporation participates in a highly competitive industry. Company management has decided that decentraliza¬ tion will best allow the company to meet the competition and achieve profit goals. Each responsibility center manager is evaluated on the basis of

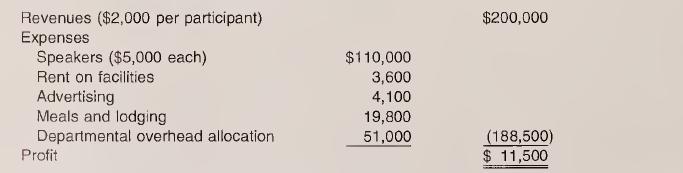

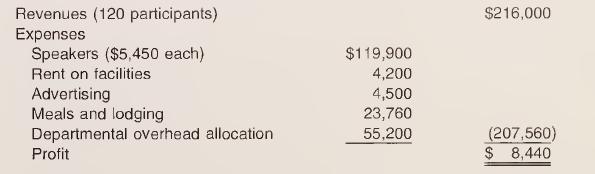

(Profit center performance) Mitchell Hardy, head of the accounting depart¬ ment at Hill Country College, has felt increasing pressure to raise external funds to compensate for dwindling state financial support. He decided to of¬ fer a three-day accounting workshop on income taxation for local

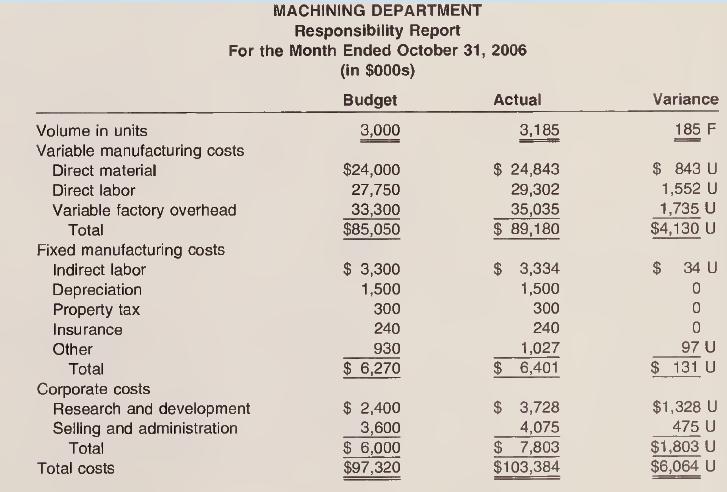

Responsibility accounting reports) Hendrix Inc. manufactures industrial tools and has annual sales of approximately $3.5 million with no evidence of cyclical demand. R&D is very important to Hendrix because its market share expands only in response to product innovation.The company controller

(Responsibility reports) To respond to increased competition and a reduction in profitability, a nationwide law firm, U.S. Law, recently instituted a respon¬ sibility accounting system. One of the several responsibility centers estab¬ lished was the Civil Litigation Division. This division is

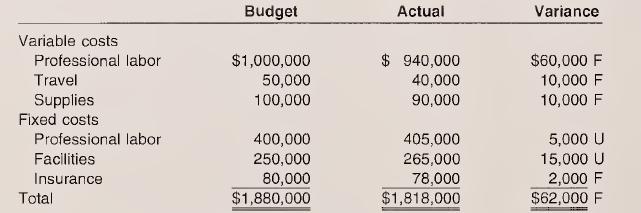

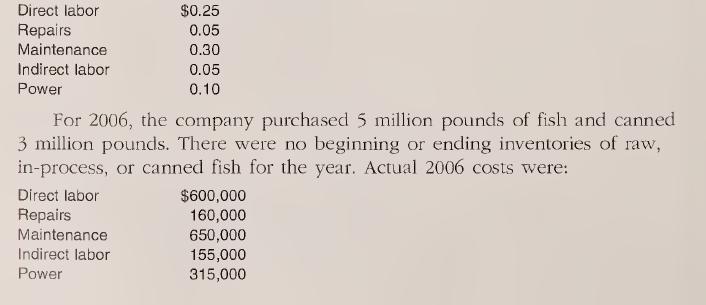

(Evaluating performance) On January 1, 2006, fast-tracker Michael Malicon was promoted to production manager of Salmon Company. The firm purchases raw fish, cooks and processes it, and then cans it in single-portion containers. It sells the canned fish to several wholesalers that specialize in

(Responsibility centers; research) According to Cutting Edge Information, Inc. (“Managing Financial Services Call Centers,” August 2003, http://www. mindbranch.com.), call center spending went from $717 million in 1998 to approximately $1.6 billion in 2003- Call centers are critical to

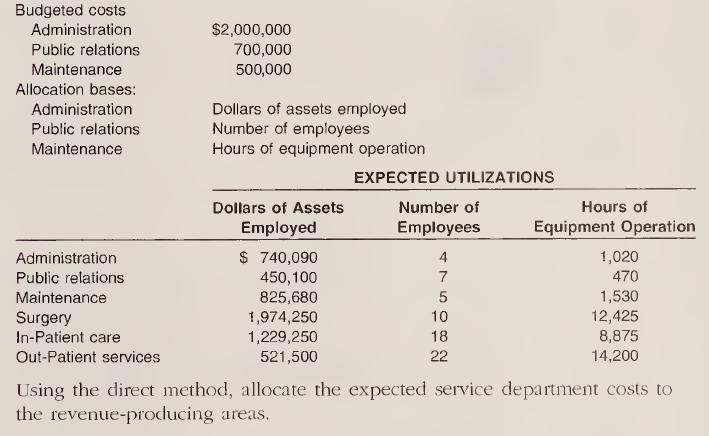

(Direct method) Management of Dekalb Community Hospital has decided to allocate the budgeted costs of its three service departments (administration, public relations, and maintenance) to its three revenue-producing programs (surgery, in-patient care, and out-patient services). Budgeted information

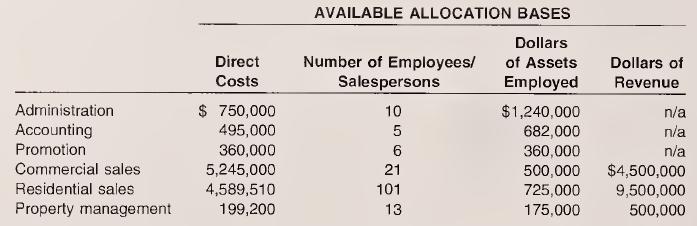

(Step method) Rodderick Properties classifies its operations into three depart¬ ments: commercial sales, residential sales, and property management. The owner, Sandy Rodderick, wants to know the full cost of operating each de¬ partment. Direct departmental costs and several allocation bases

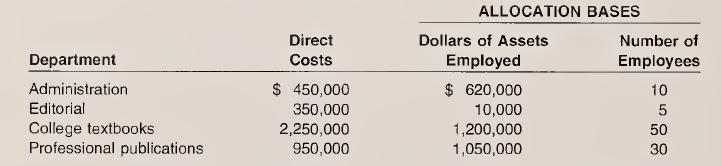

(Algebraic method) Leyh Press has two service departments (administration and editorial) and two revenue-producing divisions (college textbooks and professional publications). Following are the direct costs and allocation bases for each of these areas:Company management has decided to allocate

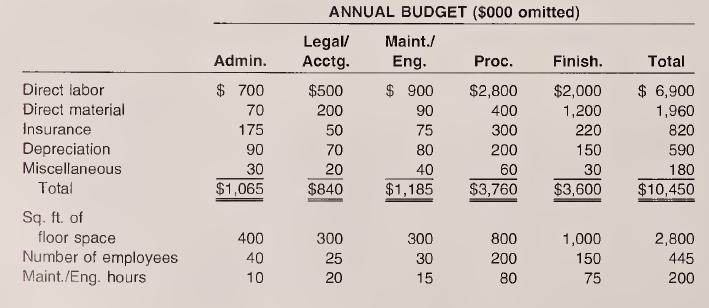

(Comprehensive service department allocations) Yolanda Company’s annual budget for its three service departments (administration, legal/accounting, and maintenance/engineering) and its two production departments (process¬ ing and finishing) follows:a. Prepare a cost distribution that allocates

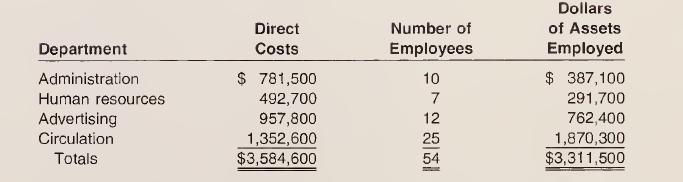

(Comprehensive service department allocations) As the controller for Reed Newspapers, you have been asked to allocate the costs of the paper’s two service departments, administration and human resources, to the two revenue-generating departments, advertising and circulation. Administration costs

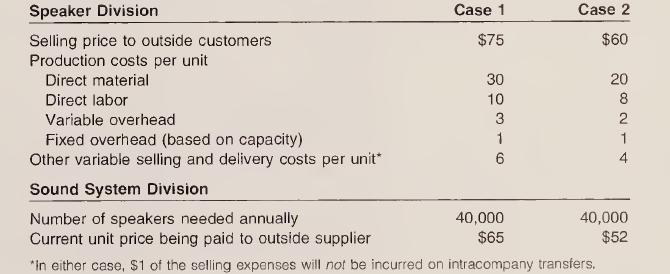

Transfer prices) In each of the following cases, the Speaker Division can sell all of its production of audio speakers externally or some internally to the Sound System Division and the remainder to outside customers. Speaker Division’s production capacity is 200,000 units annually. The data

(Transfer price) Miranda Company comprises the Engine Division and the Mobile Systems Division. The Engine Division produces engines used by both the Mobile Systems Division and a variety of external industrial cus¬ tomers. External sales orders are generally produced in 50-unit lots. Using this

(journal entries) Corporate Travel Division makes top-of-the-line computer bags and sells them to external buyers and to the Travel America Division in luggage sets sold. During the month just ended, Travel America acquired 4,000 bags from Corporate Travel Division, whose standard unit costs

(Interna! versus externai Providence Products Inc. consists of three de¬ centralized divisions: Park, Quayside, and Ricigetop. The president of Provi¬ dence Products has given the managers of the three divisions the authority to decide whether to sell externally or internally at a transfer price

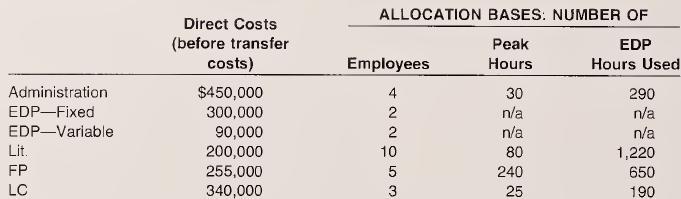

(Transfer prices) Green & Marshand LLC has three revenue departments: liti¬ gation (Lit.), family practice (FP), and legal consulting (LC). In addition, the company has two support departments, administration and EDP. Administra¬ tion costs are allocated to the three revenue departments on

(Inicrdivisional transfers; deciding on alternatives) Amy Keeler, a manage¬ ment accountant, has recently been employed as controller in the Fashions Division of Deluxe Products, Inc. The company is organized on a divisional basis with considerable vertical integration.Fashions Division makes

(Transfer prices; discussion) Biloxi Products Inc. is a decentralized company. Each division has its own sales force and production facilities and is oper¬ ated as an investment center. Top management uses return on investment (income divided by assets) for performance evaluation. Jackson Division

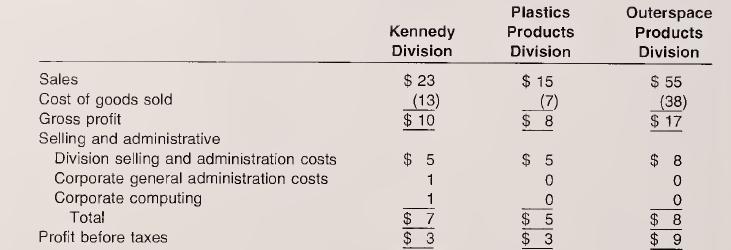

(Effect of service department allocations on reporting and evaluation) Kendra Corporation is a diversified manufacturing company with corporate head¬ quarters in Eagan, Minnesota. The three operating divisions are Kennedy Di¬ vision, Plastic Products Division, and Outerspace Products Division.

(Transfer prices) Schmidt Industries consists of eight divisions that are evalu¬ ated as profit centers. All transfers between divisions are made at market price. Precision Regulator is a division of Schmidt that sells approximately 20 percent of its output externally. The remaining 80 percent of

(Transfer prices; research) Go to the Ernst & Young Web site or to the Jour¬ nal of International Taxation (April, May, and June 2004) to find informa¬ tion on the E&Y 2003 Global Survey on Transfer Pricing. (Should a more recent survey be available, use its information.) Choose five countries

What information is provided by a variable costing income statement that is useful in computing the break-even point? Is this information on an absorp¬ tion costing income statement? Explain your answer.LO.1

How is the break-even point defined? What are the differences among the formula, graph, and income statement approaches for computing breakeven?LO.1

What is the contribution margin ratio? How is it used to calculate the break¬ even point?LO.1

Why is CVP analysis generally used as a short-run tool? Would CVP ever be appropriate as a long-run model?LO.1

What does the “bag” assumption mean, and why is it necessary in a multi¬ product firm? What additional assumption must be made in multiproduct CVP analysis that doesn’t pertain to a single-product CVP situation?LO.1

Define and explain the relationship between margin of safety and operating leverage.LO.1

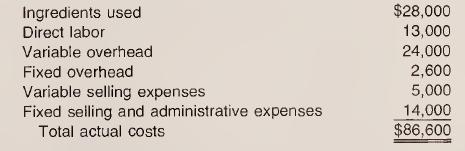

(Variable costing income statement) Gatorsip Beverages began business in 2006 selling bottles of a thirst-quenching drink. Production for the first year was 52,000 bottles of Gatorsip, and sales were 49,000 bottles. The selling price per bottle was $3-10. Costs incurred during the year were as

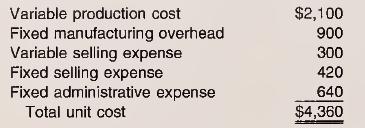

(Variable costing income statement) AEC manufactures automotive distributor caps. The following information is available for 2006, the company’s first year in business when it produced 75,000 caps. Revenue of $360,000 was generated by the sale of 45,000 caps.a. What is the variable production

(Cost and revenue behavior) The following financial data have been deter¬ mined from analyzing the records of Red Sox Gloves (a one-product firm):How does each of the following measures change when product volume goes up by one unit at Red Sox Gloves?a. Total revenueb. Total costc. Income before

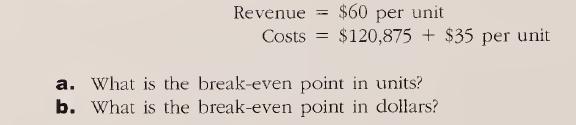

(Break-even point) Braves Company has the following revenue and cost functions:LO.1 Revenue = $60 per unit Costs = $120,875 + $35 per unit a. What is the break-even point in units? b. What is the break-even point in dollars?

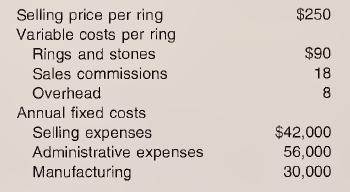

(Break-even point) HST makes and sells class rings for local schools. Operat¬ ing information follows:a. What is HST’s break-even point in rings?b. What is HST’s break-even point in sales dollars?C. What would HST’s break-even point be if sales commissions increased to $22?d.What would be

(Sales price computation) Sportswear Inc. has designed a new athletic suit. The company plans to produce and sell 60,000 units of the new product in the com¬ ing year. Annual fixed costs are $1,200,000, and variable costs are 70 percent of selling price. If the company wants a pre-tax profit of

(CVP) HG Industries makes children’s playhouses that sell for $3,000 each. Costs are as follows:a. How many playhouses must HG Industries sell to break even?b. If HG Industries’ management wants to earn a pre-tax profit of $78,000, how many playhouses must it sell?c. If HG Industries’

(CVP: taxes) Use the information for HG Industries in Exercise 14 and as¬ sume a tax rate for the company of 35 percent.a. If HG Industries’ management wants to earn an after-tax profit of $265,785, how many playhouses must it sell?b. How much revenue is needed to yield an after-tax profit of 13

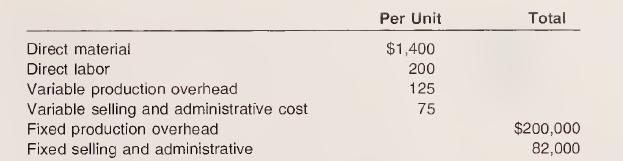

(CVP) Houston Corp. sells a product for $180 per unit. The company’s vari¬ able costs per unit are $30 for direct material, $25 per unit for direct labor, and $17 per unit for overhead. Annual fixed production overhead is $37,400, and fixed selling and administrative overhead is $25,240.a. What

(CVP; taxes) Use the information for Houston Corp. in Exercise 16 and as¬ sume a tax rate for the company of 30 percent.a. If Houston Corp. wants to earn an after-tax profit of $67,900, how many units must the company sell?b. If Houston Corp. wants to earn an after-tax profit of $2.80 on each unit

Showing 3700 - 3800

of 6579

First

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

Last

Step by Step Answers