New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

cost accounting

Cost Accounting Foundations And Evolutions 6th Edition Michael R. Kinney, Jenice Prather-Kinsey, Cecily A. Raiborn - Solutions

(Conversion cost variances) The May budget for Mia Hamm Mfg. shows $1,080,000 of variable conversion costs, $360,000 of fixed conversion costs, and 72,000 machine hours for the production of 24,000 units of product. During May, 76,000 machine hours were worked and 24,000 units were pro¬ duced.

'Standards revision) Mariucci Company uses a standard cost system for its aircraft component manufacturing operations. Recently, the company’s direct material supplier went out of business, but Mariucci’s purchasing agent found a new source that produces a similar material. The price per pound

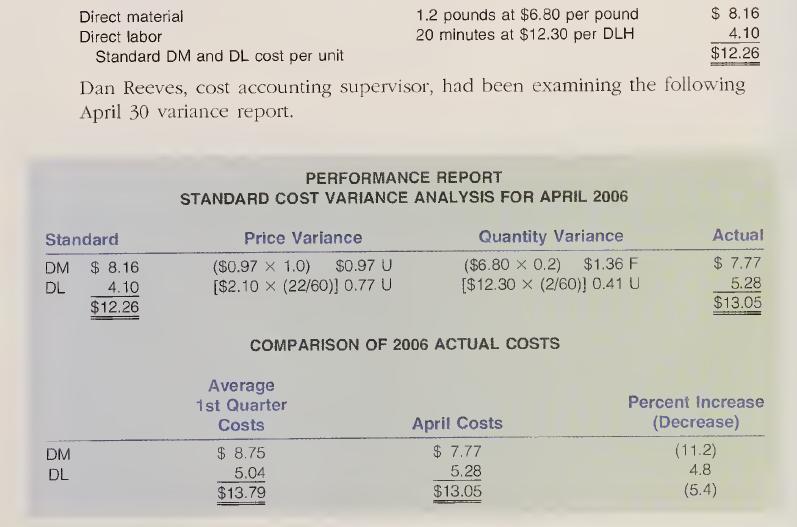

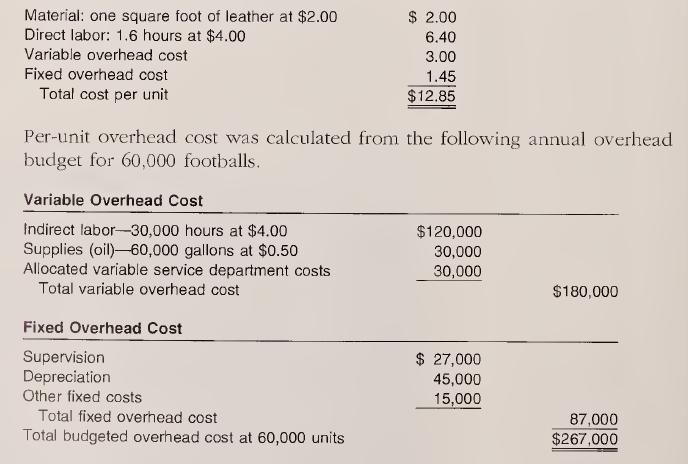

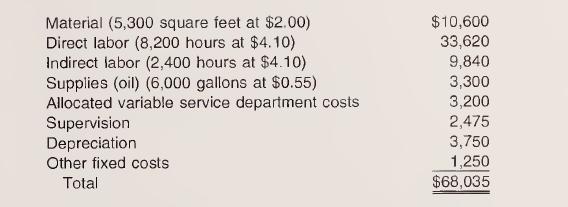

(Variances and variance responsibility) Linda Walters Co. produces miniature footballs with the following standard costs per unit:Following are the charges to the manufacturing department for November when 5,000 units were produced:Purchasing normally buys about the same quantity as is used in

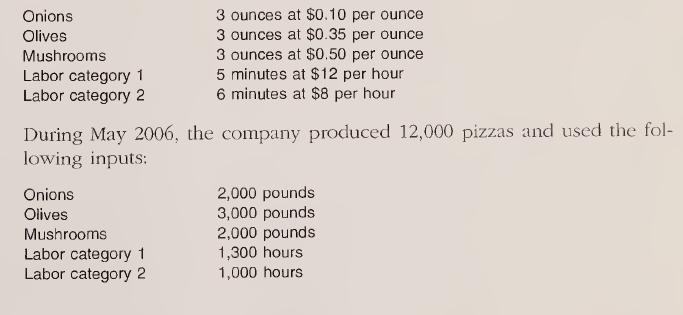

(Appendix} Venus Williams Food Industries produces three-topping, 18-inch frozen pizzas and uses a standard cost system. The three pizza toppings (in addition to cheese) are onions, olives, and mushrooms. To some extent, dis¬ cretion may be used to determine the actual mix of these toppings. The

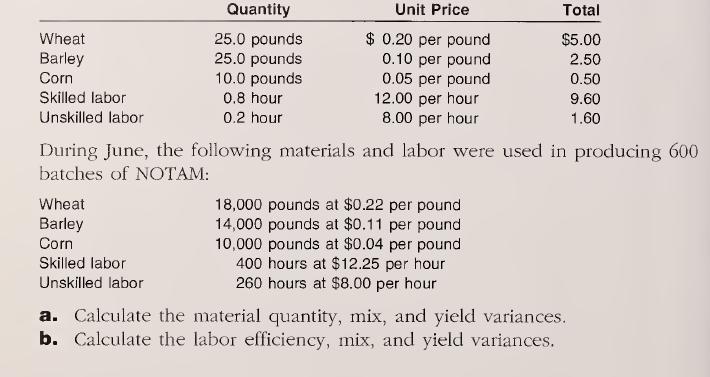

(Appendix) Dave McGinnis Products makes NOTAM, a new health food. For a 50-pound batch, standard material and labor costs are as follows:LO.1 Wheat Barley Corn Skilled labor Unskilled labor Quantity Unit Price Total 25.0 pounds $ 0.20 per pound $5.00 25.0 pounds 0.10 per pound 2.50 10.0 pounds 0.05

HOW ARE STANDARDS FOR MATERIAL, LABOR, AND OVERHEAD SET? LO.1

WHAT DOCUMENTS ARE ASSOCIATED WITH STANDARD COST SYSTEMS, AND WHAT INFORMATION DO THOSE DOCUMENTS PROVIDE?LO.1

HOW ARE MATERIAL, LABOR, AND OVERHEAD VARIANCES CALCULATED AND RECORDED?LO.1

WHY ARE STANDARD COST SYSTEMS USED?LO.1

HOW WILL STANDARD COSTING BE AFFECTED IF A SINGLE CONVERSION ELEMENT IS USED RATHER THAN THE TRADITIONAL LABOR AND OVERHEAD ELEMENTS? LO.1

Setting standards for• material requires that management identify the»- types of material inputs needed to make the product or perform the service.>■ quality of material inputs needed to make the product or perform the service.»- quantity of material inputs needed to make the product or

The documents used in a standard cost system in¬ clude the• bill of materials, which contains all quantity and quality raw material specifications to make one unit (or batch) of output.• operations flow document, which contains all la¬ bor operations necessary to make one unit (or batch) of

A variance is the difference between an actual and a standard cost. Standard costs are recorded in the Work in Process Inventory account, and variances are recorded as either debit (unfavorable) or credit (fa¬ vorable) differences between the standard cost and the actual cost incurred. In general,

A standard cost system is used to• provide clerical efficiency• assist management in its planning, controlling, decision making, and performance evaluation functions• motivate employees when the standards are>- set at a level to encourage high-quality pro¬ duction and promote cost

In highly automated companies, the standard cost sys¬ tem can use• only two elements of production cost, direct ma¬ terial and conversion.• ideal standards rather than expected or practical standards.• fixed overhead rates based on theoretical capac¬ ity rather than expected, normal, or

(APPENDIX) HOW DO MULTIPLE MATERIAL AND LABOR CATEGORIES AFFECT VARIANCES?LO.1

HOW DO JOB ORDER AND PROCESS COSTING SYSTEMS AS WELL AS THEIR RELATED VALUATION METHODS DIFFER? LO.1

WHAT CONSTITUTES A "JOB" FROM AN ACCOUNTING STANDPOINT?LO.1

WHAT PURPOSES ARE SERVED BY THE PRIMARY DOCUMENTS USED IN A JOB ORDER COSTING SYSTEM?LO.1

WHAT JOURNAL ENTRIES ARE USED TO ACCUMULATE COSTS IN A JOB ORDER COSTING SYSTEM?LO.1

HOW DO TECHNOLOGICAL CHANGES IMPACT THE GATHERING AND USE OF INFORMATION IN JOB ORDER COSTING SYSTEMS?LO.1

HOW ARE STANDARD COSTS USED IN A JOB ORDER COSTING SYSTEM?LO.1

HOW DOES INFORMATION FROM A JOB ORDER COSTING SYSTEM SUPPORT MANAGEMENT DECISION MAKING?LO.1

HOW ARE LOSSES TREATED IN A JOB ORDER COSTING SYSTEM?LO.1

Job order and process costing systems differ in that job order costing• is used in companies that make limited quanti¬ ties of customer-specified products or perform customer-specific services; process costing is used in companies that make mass quantities of ho¬ mogeneous output on a

From an accounting standpoint, a “job”• is the cost object for which costs are accumu¬ lated.• can consist of one or more units of output.• has its costs accumulated on a job order cost sheet.LO.1

The primary documents used in a job order costing system are the• job order cost sheets which, for incomplete jobs, serve as the Work in Process Inventory subsidiary ledger; cost sheets for completed jobs not yet de¬ livered to customers constitute the Finished Goods Inventory subsidiary ledger;

The typical journal entries used to accumulate costs in a job order costing system record the• purchase, for cash or on credit, of raw materials for use in production.• issuance of direct material to Work in Process Inventory.• incurrence of direct labor hours and pay.• incurrence of actual

Technological changes have impacted the gathering and use of information in job order costing systems by• including a job order costing module in even ba¬ sic accounting software.• aiding the product management of jobs through software programs that allow operational and financial data about

Standard costs may be used in a job order costing system by• establishing standards for quantities and/or costs of production inputs.• providing a basis for managers to evaluate the efficiency of operations through comparisons of actual and standard costs. Differences between actual costs and

Job order costing information helps support man¬ agement decision making by• assisting managers in their planning, controlling, decision making, and performance evaluating functions.• allowing managers to trace costs associated with specific current jobs to better estimate costs for future

Both normal and abnormal losses may occur in a job order system and they are accounted for in the fol¬ lowing manner• normal losses that are generally anticipated on all jobs are estimated and included in the devel¬ opment of the predetennined overhead rate.• normal losses that are associated

In choosing a product costing system, what are the two choices available for a cost accumulation system? How do these systems differ?LO1.

In choosing a product costing system, what are the three valuation method alternatives? Explain how these methods differ.LO1.

In a job order costing system, what key documents support the cost accu¬ mulation process?LO1.

In a standard costing system, discuss how information about variances can be used to improve cost control.LO1.

If normal spoilage is generally anticipated to occur on all jobs, how should the cost of that spoilage be treated?LO1.

Why are normal and abnormal spoilage accounted for differently? Typically, how does one determine which spoilage is normal or abnormal?LO1.

(Classifying) For each of the following firms, determine whether it is more likely to use job order or process costing. This firma. is a health care clinic.b. makes custom jewlery.c. manufactures hair spray and hand lotion.d. provides public accounting services.e. manufactures paint.f. cans

(Journal entries) Clara Inc. produces custom-made floor tiles. During April 2006, the following information was obtained relating to operations and production:1. Direct material purchased on account, $174,000.2. Direct material issued to jobs, $163,800.3. Direct labor hours incurred, 3,400. All

(Journal entries; cost flows) The following costs were incurred in February 2006 by Store-It-All, which produces customized storage buildings.The balance in Work in Process Inventory on February 1 was $8,400, which consisted of $5,600 for Job #217 and $2,800 for Job #218. The February be¬ ginning

(Cost flows) Brooke Landscapes began operations on May 1, 2006. Its Work in Process Inventory account on May 31 appeared as follows:The company applies overhead on the basis of direct labor cost. Only one job was still in process on May 31- That job had $132,600 in diiect material and $93,600 in

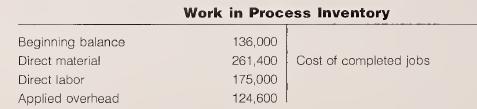

(Cost flow s) For 2006, Brown Mfg. decided to apply overhead to units based on direct labor hours. The company’s Work in Process Inventory account on January 31 appeared as follows:The beginning balance of $136,000 contained 5,000 direct labor hours. Dur¬ ing January, 14,000 direct labor hours

(Cost flows) Integrated Decisions Corp. applies overhead to jobs at a rate of 120 percent of direct labor cost. On December 31, 2006, a flood destroyed many of the firm's cost records, leaving only the following information:As the cost accountant of Integrated Decisions, you must find the following

(Cost flows) On March 18, 2006, a fire destroyed Weymann World’s work-in-process inventory, which consisted of two in-process custom jobs (B325 and Q428). The following information had, however, been contained in some off-site records:• Weymann World applies overhead at the rate of 85 percent

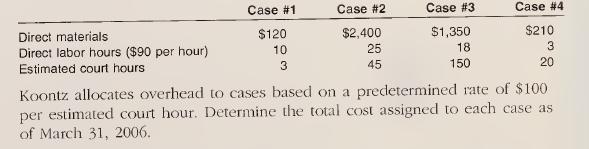

Job costs) Koontz & Assc., LLP, is a law firm that currently has four cases in process. Following is information related to those cases as of the end of March 2006:LO1. Direct materials Direct labor hours ($90 per hour) Estimated court hours Case #1 Case #2 Case #3 Case #4 $120 $2,400 $1,350

(Departmental overhead rates) Chalmette Company uses a normal cost, job order costing system. In the Mixing Department, overhead is applied using machine hours; in Paving, overhead is applied using direct labot hours. In December 2005, the company estimated the following data for its two de¬

(job cost and pricing) Jen Bernardi is an attorney who uses a job order cost¬ ing system to collect costs relative to client engagements. Bernardi is cur¬ rently working on a case for Joe Lundy. During the first three months of 2006, Bernardi logged 105 hours on the Lundy case.In addition to

(Underapplied or overapplied overhead) For 2006, Wilhem Co. applied over¬ head to jobs using a predetermined overhead rate of $18.40 per machine hour. This rate was derived by dividing the company’s total budgeted over¬ head by the 48,000 machine hours anticipated for the year.At the end of

(Assigning costs to jobs) Kilhenny Co. uses a job order costing system and applies overhead to jobs at a predetermined rate of $2.20 per direct labor dollar. During April 2006, the company spent $14,800 on direct materials and $23,900 on direct labor for Job #344. Budgeted factory overhead for the

(Assigning costs to jobs; cost flows) TORI’S, an interior decorating firm, uses a job order costing system and applies overhead to jobs using a predetei- mined rate of 60 percent of direct labor cost. On June 1, 2006, Job #918 was the only job in process. Its costs included direct material of

(Assigning costs to jobs) Tina Wheels is an advertising consultant; she tracks costs for her jobs using a job order costing system. During September, Tina and her staff worked on and completed jobs for the following companies.Direct materials can be traced to each job because these costs are

Standard costing) Fine Print, Inc., incurred the following direct material costs in November 2006 for high-volume routine print jobs:Calculate the material price variance and the material quantity variance.LO1. Actual unit purchase price Standard unit price Quantity purchased and used in November

(Standard costing) Delaware Inc. uses a standard cost system. The company experienced the following results related to direct labor in December 2006:c. Determine the labor quantity variance.d. What concerns do you have about the variances in parts (b) and (c)?LO1. Actual hours worked 49,500

(Cost control) Fabricated Steel Products makes steel storage containers for various chemical products. The company uses a job order costing system and obtains jobs based on competitive bidding. For each project, a budget is developed.One of the firm’s products is a 55-gallon drum. In the past

(Job order costing: rework) Oehlke Rigging manufactures pulley systems to customer specifications and uses a job order system. Mary Sue Co. recently ordered 10,000 pulleys, and the job was assigned number BA468. Informa¬ tion for Job #BA468 revealed the following:Final inspection of the pulleys

(Labor time) Choose a Web search engine and type in “time-and-attendance software.” Numerous sites will be displayed. Go to the Web sites of four companies that produce or sell such software. Prepare a brief report that compares and contrasts the software items. Choose one product that appeals

(Process differences) Go to the Web site for Green Design Furniture. Pre¬ pare a report that reviews and explains the design and manufacturing process of this company. Why would it be necessary for Green Design Fur¬ niture to use a job order costing system? How does this company’s produc¬ tion

(Strategic alliances) According to a Wall StreetJournal article (Wei, “Account¬ ing Alliances Gain Popularity,” February 11, 2004, p. B4A), many large pub¬ lic accounting firms are establishing alliances with smaller firms. Such alliances allow the smaller entities to use the larger firms’

(Ethics) Companies use time sheets for two primary reasons: to know how many hours an employee works and, in a job order production situation, to trace work hours to products. An article (“Altering of Worker Time Cards Spurs Growing Number of Suits” by Steven Greenhouse) in the New York. Times

journal entries) Shady Time installs awnings on residential and commercial structures. The company had the following transactions for February 2006:• Purchased $195,000 of building (raw) material on account.• Issued $185,000 of building (direct) material to jobs.• Issued $30,000 of building

(Journal entries; assigning costs to jobs) Omega Engineers uses a job order costing system. On September 1, 2006, the company had the following ac¬ count balances:a. Prepare journal entries for the transactions for September 2006.b. Use T-accounts to post the information from the journal entries

, Journul entries; cost flows) Excellent Components began 2006 with three jobs in process:During 2006, the following transactions occurred:1. The firm purchased and paid for $542,000 of raw material.2. Factory payroll records revealed the following:• Indirect labor incurred was $54,000.• Direct

(Simple inventory calculation) Production data for the first week in Novem- ber 2006 for Bryan Machinery were as follows:Overhead is charged to production at a rate of $30 per machine hour. Un¬ derapplied or overapplied overhead is treated as an adjustment to Cost of Goods Sold at year-end. (All

(Job cost sheet analysis) As a candidate for a cost accounting position with Romano Construction, you have been asked to take a quiz to demonstrate your knowledge of job order costing. Romano’s job order costing system is based on normal costs and overhead is applied based on direct labor cost.

(Departmental rates) Elegant Style Tile Corporation has two departments, Mixing and Drying. All jobs go through each department, and the company uses a job order costing system. Overhead is applied to jobs based on labor hours in Mixing and on machine hours in Drying. In December 2005, corpo¬ rate

(Comprehensive) Gary Construction Company uses a job order costing sys tern. In May 2006, Gary made a $1,650,000 bid to build a pedestrian over¬ pass over the beach highway in Gulfport, Mississippi. Gary won the bid and assigned #515 to the project. Its completion date was set at December 15,

(Comprehensive) Safety First, Inc., designs and manufactures perimeter fenc¬ ing for large retail and commercial buildings. Each job goes through three stages: design, production, and installation. Three jobs were started and completed during the first week of May 2006. No jobs were in process at

(Standard costing) MaMo Corp. specializes in making robotic conveyor sys¬ tems to move materials within a factory. Model #89 accounts for approxi¬ mately 60 percent of the company’s annual sales. Because the company has produced and expects to continue to produce a significant quantity of this

(Standard costing) During July 2006, Haul-It, Inc., worked on two production runs (Jobs #918 and #2002) of the same product, a trailer hitch component. Job #918 consisted of 1,200 units of the product, and Job # 2002 contained 2,000 units. The hitch components are made from 1" sheet metal. Because

(Defective units and rework) Hoffus Corporation produces plastic pipe to customer specifications. Losses of less than 5 percent are consideied normal because they are inherent in the production process. The company applies overhead to products using machine hours. Hoffus Corporation used the fol¬

(Coinprehensi\ t\; job cost sheet) Jefferson Construction Company builds bridges. In October and November 2006, the firm worked exclusively on a bridge spanning the Niobrara River in northern Nebraska. Jefferson Con¬ struction’s Precast Department builds structural elements of the bridges in

Comprehensive) Tiny Tots Corp. is a manufacturer of furnishings for infants and children. The company uses a job order cost system. Tiny Tots’ Work in Process Inventory on April 30, 2006, consisted of the following jobs:Tiny Tots applies factory overhead on the basis of direct labor hours.The

(Missing amounts; challenging) Riveredge Manufacturing Company realized too late that it had made a mistake locating its controller’s office and its electronic data processing system in the basement. Because of the spring thaw, the Mississippi River overflowed its banks on May 2 and flooded the

Ethics) One of the main points of using a job order costing system is to achieve profitability by charging a price for each job that is proportionate to the related costs. The fundamental underlying concept is that the buyer of the product should be charged a price that exceeds all costs related to

(Research) Timbuk2 is a San Francisco company that makes a variety of messenger, cyclist, and laptop bags. The company’s Web site allows cus¬ tomers to design their own size, color, and fabric bags with specific features and accessories; then the company sews the bags to the customers’

ON WHAT ITEMS DOES ACTIVITY-BASED MANAGEMENT FOCUS? LO.1

WHY DO NON-VALUE-ADDED ACTIVITIES CAUSE COSTS TO INCREASE UNNECESSARILY?LO.1

WHY MUST COST DRIVERS BE DESIGNATED IN AN ACTIVITY-BASED COSTING SYSTEM?LO.1

HOW DOES ACTIVITY-BASED COSTING DIFFER FROM A TRADITIONAL COST ACCOUNTING SYSTEM?LO.1

WHAT NEW TYPES OF INFORMATION DOES AN ACTIVITY-BASED COSTING/MANAGEMENT SYSTEM OFFER MANAGEMENT?LO.1

WHEN IS ACTIVITY-BASED COSTING APPROPRIATE IN AN ORGANIZATION?LO.1

Activity-based management focuses on• analyzing activities and identifying the cost dri¬ vers of those activities.• classifying activities as value-added or non-value- added (which includes business-value-added) and striving to eliminate or minimize the non¬ value-added costs.• making

Non-value-added (NVA) activities, such as inspection, transfer, and idleness, increase costs because• production or performance time is lengthened.• workers are engaged in activities for which cus¬ tomers are not willing to pay.• time is money.LO.1

Cost drivers are designated in an activity-based cost¬ ing system to• identify what causes a cost to be incurred so that it can be controlled.• indicate at what level (unit, batch, product/ process, or organizational) a cost occurs.• allow costs with similar drivers to be pooled to¬ gether

Activity-based costing differs from a traditional cost accounting system in that it• identifies several levels of costs rather than the traditional concept that costs are fixed unless they vary specifically at the unit level.• collects costs in cost pools based on the under¬ lying nature and

Installation of an activity-based management/costing system will allow management to• recognize the cost impact of cross-functional ac¬ tivities in an organization.• recognize that fixed costs are, in fact, long-run variable costs that change based on an identifi¬ able driver.• recognize

Activity-based costing is appropriate in an organiza¬ tion that has• a large variety of products being produced and sold.• products that can be customized to customer specifications.• wide diversity in manufacturing needs for its products.• a lack of commonality in overhead costs related

What is activity-based management (ABM), and what are the specific man¬ agement tools that fall beneath its umbrella?LO1.

Why are value-added activities defined from a customer viewpoint?LO1.

In a televised football game, what activities are value added? What activities are non-value added? Would everyone agree with your choices? Why or why not?LO1.

What is activity analysis, and how is it used in concert with cost driver analysis to manage costs?LO1.

Why do the more traditional methods of overhead assignment “overload” standard high-volume products with overhead costs, and how does ABC im¬ prove overhead assignments?LO1.

Are all companies likely to benefit to an equal extent from adopting ABC? Discuss.LO1.

(VA or NYA) Choose an activity related to this class, such as attending class or doing homework. Write down the answers to the question “why” five times to determine whether your activity is value added or non-value added.LO1.

(VA or NYA) Your boss wants to know whether quality inspections at your company add value. Use the “why” methodology to help your boss make this determination if you work at (a) a clothing manufacturer that sells to a discount chain and (b) a pharmaceutical manufacturer.LO1.

(VA or NVA) Go to a local department or grocery store.a. List five packaged items for which it is readily apparent that packaging is essential and, therefore, would be considered value added.b. List five packaged items for which it is readily apparent that packaging is nonessential and therefore

(VA and NVA) Lawrence Co. is experiencing a problem with schedule changes in its Toledo plant. To help assess the financial impact of the prob¬ lem, you have gathered the following information on the activities, estimated times, and average costs required for a single schedule change.a. Which of

(Cycle time and MCE) 2AM produces creole seasoning using the following process for each batch.LO1. Function Receiving ingredients Moving ingredients to stockroom Storing ingredients in stockroom Moving ingredients from stockroom Mixing ingredients Packaging ingredients Moving packaged seasoning to

Showing 4000 - 4100

of 6579

First

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

Last

Step by Step Answers