New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

derivative pricing

Derivative Pricing 1st Edition Ambrose Lo - Solutions

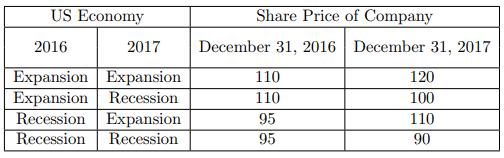

You are given the following with respect to a public company:• The common shares of the company were trading at 100 as of December 31, 2015.• No dividends are paid.• An industry analyst has projected the possible stock prices over the next two years as a function of the performance of the US

For a binomial option pricing model, you are given the following information:• The current stock price is $110.• The strike price is $100.• The interest rate is 5% (continuously compounded)• The continuous dividend yield is 3.5%.• The volatility is 0.30.• The time to expiration is 1

A three-month European call is modeled by a single period binomial tree using the following parameters:• Continuously compounded risk-free rate = 4%• Dividend = 0• Annual volatility = 15%• Current stock price = 10• Strike price = 10.5Calculate the value of the call option.(A) Less than

You use the following information to construct a binomial forward tree for modeling the price movements of a stock:(i) The length of each period is 1 year.(ii) The current stock price is 190.(iii) The stock’s volatility is 30%.(iv) The stock pays dividends continuously at a rate proportional to

A one-year European call option is currently valued at 0.9645. The following parameters are given.• Current stock price = 10• Continuously compounded risk-free rate = 6%• Continuously compounded dividend rate = 1%• Strike price = 10Using a single period binomial tree, calculate the implied

For a 10-period binomial stock price model, you are given:(i) The length of each period is one year.(ii) The current stock price is 1,000.(iii) At the end of every year, the stock price will either increase by 5% or decrease by 5% in proportion. (iv) The stock pays dividends continuously at a rate

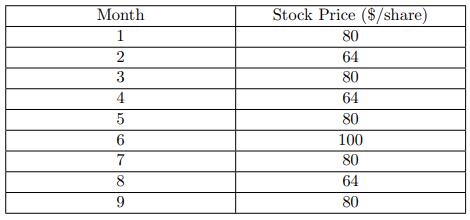

You are to estimate a nondividend-paying stock’s annualized volatility using its prices in the past nine months.Calculate the historical volatility for this stock over the period.(A) 83%(B) 77%(C) 24%(D) 22%(E) 20% Month 1 23 1678 5 6 9 Stock Price ($/share) 80 64 80 64 80 100 80 64 80

Let S(t) be the time-t price of a nondividend-paying stock. For a three-period binomial stock price model, you are given:(i) The length of each period is one year.(ii) S(0) = 100.(iii) u = 1.1, where u is one plus the percentage change in the stock price per period if the price goes up.(iv) d =

For a two-period binomial model for stock prices, you are given:(i) The length of each period is one year.(ii) The current price of a nondividend-paying stock is $150.(iii) u = 1.25, where u is one plus the percentage change in the stock price per period if the price goes up.(iv) d = 0.80, where d

For a two-period binomial model for stock prices, you are given:(i) The length of each period is one year.(ii) The current price of a nondividend-paying stock is $40.(iii) u = 1.05, where u is one plus the percentage change in the stock price per period if the price goes up.(iv) d = 0.9, where d is

For a binomial forward tree modeling the price movements of a stock, you are given:(i) The length of each period is 6 months.(ii) The current price of a nondividend-paying stock is $9,000.(iii) The stock’s volatility is 32%.(iv) The continuously compounded risk-free interest rate is 20%.Consider

You use the following information to construct a binomial forward tree for modeling the price movements of a nondividend-paying stock:(i) The length of each period is 6 months.(ii) The current stock price is 100.(iii) The stock’s volatility is 20%.(iv) The continuously compounded risk-free

You use the following information to construct a binomial forward tree for modeling the price movements of a stock.(i) The length of each period is 4 months.(ii) The current stock price is 100.(iii) The stock’s volatility is 30%.(iv) The stock pays no dividends.(v) The continuously compounded

The Ashwaubenon Company (Ash Co) needs to raise capital to support its rapidly growing business. One proposal is to publicly issue a certain number of equity units, each of which consists of one share of stock and a warrant to purchase one share of stock.Assume that the price of the underlying

You use the following information to construct a binomial forward tree for modeling the price movements of a stock:(i) The length of each period is 4 months.(ii) The current stock price is 55.(iii) The stock’s volatility is 30%.(iv) The stock pays dividends continuously at a rate proportional to

You use the following information to construct a two-period binomial forward tree for modeling the movements of the dollar-euro exchange rate:(i) The current dollar-euro exchange rate is $1.50/AC.(ii) The volatility of the exchange rate is 20%.(iii) The continuously compounded risk-free interest

For a four-period binomial tree model for the dollar/pound exchange rate, you are given:(i) The length of each period is 3 months.(ii) The current dollar/pound exchange rate is 1.4.(iii) u = 1.1 and d = 0.9, where u and d are one plus the percentage change in the dollar/pound exchange rate per

You use the following information to construct a binomial tree for modeling the price movements of a futures contract on the S&V 150:(i) The length of each period is 6 months.(ii) The initial futures price is 500.(iii) u = 1.2363, where u is one plus the percentage change in the futures price per

You use the following information to construct a one-period binomial forward tree for modeling the price movements of a nondividend-paying stock:(i) The current stock price is 82.(ii) The stock’s volatility is 30%.(iii) The continuously compounded risk-free interest rate is 8%.(iv) The

You use the following information to construct a binomial forward tree for modeling the price movements of a nondividend-paying stock:(i) The length of each period is 4 months.(ii) The current stock price is 50.(iii) The stock’s volatility is 30%.(iv) The continuously compounded risk-free

You use the following information to construct a binomial forward tree for modeling the price movements of a nondividend-paying stock:(i) The length of each period is 4 months.(ii) The current stock price is 123.(iii) The stock’s volatility is 30%.(iv) The continuously compounded risk-free

Assume the Black-Scholes framework. Let S(t) denote the time-t price of a nondividend-paying stock. You are given: (i) The current stock price is 38. (ii) The stock’s volatility is 35%. (iii) The continuously compounded expected return on the stock is 16%(iv) The continuously compounded

You are given the following information about a European call option. • The current stock price is $35.• The exercise price is $40.• The option matures in 6 months.• The expected return on the stock is 18% per annum.• The volatility, σ, of the stock price is 24% per annum.• The

Consider a nondividend-paying stock whose current price is 100.The stock-price process is a lognormal process with volatility 30%.The continuously compounded expected return on the stock is 10%.The continuously compounded risk-free interest rate is 7%.Calculate the probability that a nine-month

You are given the following information about a nondividend-paying stock:(i) The current stock price is 100.(ii) Stock prices are lognormally distributed.(iii) The continuously compounded expected return on the stock is 10%.(iv) The stock’s volatility is 30%.Consider a nine-month 125-strike

Assume the Black-Scholes framework. You are given:(i) The current stock price is 100.(ii) The stock pays dividends continuously at a rate proportional to its price. The dividend yield is 2.5%.(iii) The continuously compounded expected rate of return on the stock is 6%.(iv) The stock’s volatility

Assume the Black-Scholes framework.You are given the following information for a stock that pays dividends continuously at a rate proportional to its price.(i) The current stock price is 0.25.(ii) The stock’s volatility is 0.35.(iii) The continuously compounded expected rate of stock-price

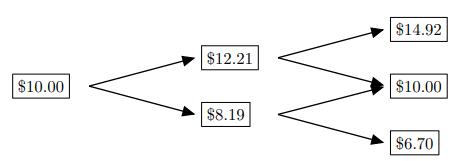

Two actuaries, A and B, use a two-period binomial forward tree to compute the prices of a European call and a European put using different parameters.You are given:Describe the relationship between the call price computed by Actuary A and the put price computed by Actuary B. Actuary

Showing 400 - 500

of 428

1

2

3

4

5

Step by Step Answers