New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

derivative pricing

Derivative Pricing 1st Edition Ambrose Lo - Solutions

You enter into a long synthetic forward on a stock using 1-year European options. The price of a 50-strike call option is 6.8 and the price of a 50-strike put option is 4.2. The continuously compounded risk-free interest rate is 3%. The stock sells for 54 after 1 year. Determine your profit from

Student A constructs a K1-K2 bull spread using call options, while Student B constructs a K1-K2 bull spread using put options. All options are European with the same underlying asset and time to expiration.Determine which of the following statements about these two bull spreads is/are correct.I.

Determine whether each of the following positions has an unlimited loss potential from adverse price movements in the underlying asset, regardless of the initial premium received.(A) Long forward(B) Short naked call(C) Long collared stock(D) Short straddle(E) Long butterfly spread

Determine which of the following risk management techniques can hedge the financial risk of an oil producer arising from the price of the oil that it sells.I. Short forward position on the price of oilII. Long put option on the price of oilIII. Long call option on the price of oil(A) I only(B) II

Assume that a single stock is the underlying asset for a forward contract, a K-strike call option, and a K-strike put option.Assume also that all three derivatives are evaluated at the same point in time.Which of the following formulas represents put-call parity?(A) Call Premium – Put Premium =

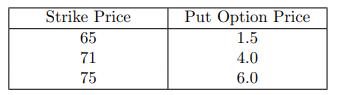

An investor bought a 70-strike European put option on an index with six months to expiration. The premium for this option was 1.The investor also wrote an 80-strike European put option on the same index with six months to expiration. The premium for this option was 8.The six-month interest rate is

You are given the following information:(i) The current price of the stock is 45 per share.(ii) The stock pays dividends continuously at a rate proportional to its price. The dividend yield is 2%.(iii) The price of a 9-month at-the-money European call option on the stock is 3.(iv) The continuously

A producer of gold has expenses of 800 per ounce of gold produced. Assume that the cost of all other production-related expenses is negligible and that the producer will be able to sell all gold produced at the market price. In one year, the market price of gold will be one of three possible

You buy a stock at $300 and buy an at-the-money 9-month European put option on the stock at a price of $15.The continuously compounded risk-free interest rate is 5%.Calculate your 9-month profit if the 9-month stock price is $280.

The PS index has the following characteristics:• One share of the PS index currently sells for 1,000.• The PS index does not pay dividends.Sam wants to lock in the ability to buy this index in one year for a price of 1,025. He can do this by buying or selling European put and call options with

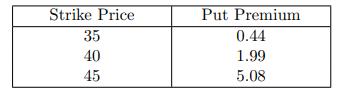

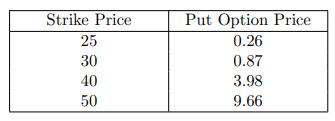

The current price of a nondividend-paying stock is 40 and the continuously compounded risk-free interest rate is 8%. The following table shows call and put option premiums for three-month European options of various exercise prices:A trader interested in speculating on volatility in the stock price

You are given:(i) The current price of a stock is 70.(ii) The continuously compounded risk-free interest rate is 5%.(iii) The price of a 70-strike 1-year European call option is 5.(iv) The price of a 75-strike 1-year European call option is 3.Calculate the amount of investment required to create a

A trader shorts one share of a stock index for 50 and buys a 60-strike European call option on that stock that expires in 2 years for 10. Assume the annual effective risk-free interest rate is 3%. The stock index increases to 75 after 2 years. Calculate the profit on your combined position, and

You are selecting among various put options with different strike prices to hedge a long asset position.Which of the following statements is true? Give your reasoning.(A) Higher-strike puts cost more and provide higher floors.(B) Higher-strike puts cost less and provide higher floors.(C)

For each ton of a certain type of rice commodity, the four-year forward price is 300. A four-year 400-strike European call option costs 110. The annual risk-free force of interest is a constant 6.5%. Calculate the cost of a four-year 400-strike European put option for this rice commodity. (A)

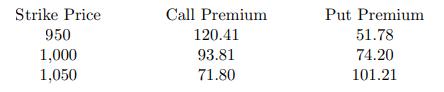

The current price for a stock index is 1,000. The following premiums exist for various options to buy or sell the stock index six months from now:Strategy I is to buy the 1,050-strike call and to sell the 950-strike call.Strategy II is to buy the 1,050-strike put and to sell the 950-strike

In the Midterm Exam of your favorite derivatives pricing course, a really “clever” student erroneously constructed a K1-K2 strangle by using in-the-money options. Specifically, he bought a call option with strike price K1, and bought a put option with strike price K2, where K1 < S(0) <

Supway is a sandwich shop, one of its main production inputs being wheat.Determine whether each of the following risk management techniques can hedge the financial risk faced by Supway arising from the price of wheat that it buys.(A) Long forward on wheat (B) Long call option on wheat (C) Short

Consider an airline company that faces risk concerning the price of jet fuel. Select the hedging strategy that best protects the company against an increase in the price of jet fuel.(A) Buying calls on jet fuel(B) Buying collars on jet fuel(C) Buying puts on jet fuel(D) Selling puts on jet fuel(E)

XYZ stock pays no dividends and its current price is 100.Assume the put, the call and the forward on XYZ stock are available and are priced so there are no arbitrage opportunities. Also, assume there are no transaction costs.The annual effective risk-free interest rate is 1%.Determine which of the

Joe believes that the volatility of a stock is higher than indicated by market prices for options on that stock. He wants to speculate on that belief by buying or selling at-the-money options.Determine which of the following strategies would achieve Joe’s goal.(A) Buy a strangle(B) Buy a

Box spreads are used to guarantee a fixed cash flow in the future. Thus, they are purely a means of borrowing or lending money, and have no stock price risk.Consider a box spread based on two distinct strike prices (K, L) that is used to lend money, so that there is a positive cost to this

Assume the same underlying stock, same time to expiration, and same strike price for all derivatives in this problem.Which of the following must have the same profit as a floor coupled with a cap? Give your reasoning.(A) Long stock(B) Short stock(C) Long straddle(D) Short straddle(E) None of the

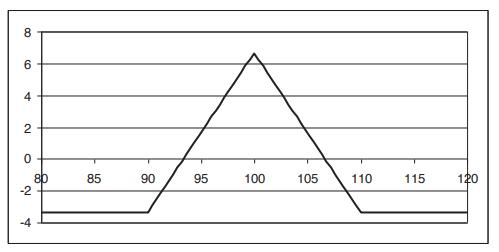

Stock ABC has the following characteristics:• The current price to buy one share is 100.• The stock does not pay dividends.• European options on one share expiring in one year have the following prices:A butterfly spread on this stock has the following profit diagram. The continuously

Determine which of the following statements about options is true. (A) Naked writing is the practice of buying options without taking an offsetting position in the underlying asset. (B) A covered call involves taking a long position in an asset together with a written call on the same asset. (C)

CornGrower is going to sell corn in one year. In order to lock in a fixed selling price, CornGrower buys a put option and sells a call option on each bushel, each with the same strike price and the same one-year expiration date.The current price of corn is 3.59 per bushel, and the net premium that

The following table shows 1-year European call and put option premiums at two strike pricesThe continuously compounded risk-free interest rate is 6%. Describe actions you could take to construct an arbitrage strategy that results in profits at the end of one year using the above options and/or

Assume the same underlying stock, same time to expiration, and same strike price for all derivatives in this problem.Which of the following must have the same profit as a floor coupled with a written covered call? Give your reasoning. There can be more than one answer.(A) Long stock(B) Short

An investor has written a covered call. Determine which of the following represents the investor’s position.(A) Short the call and short the stock(B) Short the call and long the stock(C) Short the call and no position on the stock(D) Long the call and short the stock(E) Long the call and long the

The current price of a nondividend-paying stock is 40 and the continuously compounded risk-free interest rate is 8%. You are given that the price of a 35-strike call option is 3.35 higher than the price of a 40-strike call option, where both options expire in 3 months.Calculate the amount by which

Consider the following investment strategy involving put options on a stock with the same expiration date.(i) Buy one 25-strike put(ii) Sell two 30-strike puts(iii) Buy one 35-strike putCalculate the payoffs of this strategy assuming stock prices (i.e., at the time the put options expire) of 27 and

Determine which of the following strategies creates a ratio spread, assuming all options are European.(A) Buy a one-year call, and sell a three-year call with the same strike price.(B) Buy a one-year call, and sell a three-year call with a different strike price.(C) Buy a one-year call, and buy

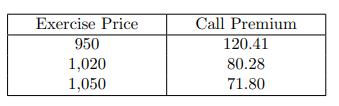

The current price of a nondividend-paying stock is 1,000 and the continuously compounded risk-free interest rate is 5%. Richard wants to lock in the ability to sell a unit of this stock in six months for a price of 1,020. He can do this by buying or selling 6-month 1,020-strike European put and

Assume the same underlying asset, same time to expiration, and same strike price for all concerned options. Which of the following must have the same profit as a written covered call?(A) Short call(B) Long call(C) Short put(D) Long put(E) Written covered put

An investor is analyzing the costs of two-year, European options for aluminum and zinc at a particular strike price.For each ton of aluminum, the two-year forward price is 1400, a call option costs 700, and a put option costs 550.For each ton of zinc, the two-year forward price is 1600 and a put

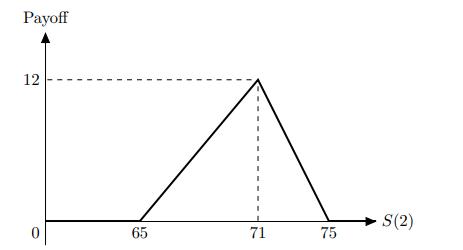

The payoff diagram of a certain investment strategy involving 2- year European put options on a stock is shown on the right.You are given: (i) (ii) The continuously compounded risk-free interest rate is 1.5%. Calculate the profit on the investment strategy assuming that the stock price at

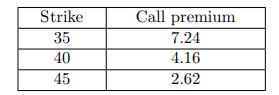

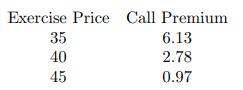

The current price of a nondividend-paying stock is 40 and the continuously compounded risk-free interest rate is 8%. You enter into a short position on 3 call options, each with 3 months to maturity, a strike price of 35, and an option premium of 6.13. Simultaneously, you enter into a long position

The current price of a stock is 100, and the continuously compounded risk-free interest rate is 10%. A $2.5 dividend will be paid every quarter, with the first dividend occurring 2 months from now. Roger uses a K-strike European call option and a K-strike European put option on the same stock to

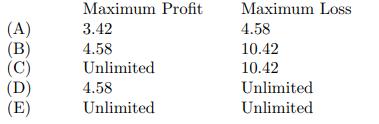

An investor has a long position in a nondividend-paying stock, and, additionally, has a long collar on this stock consisting of a 40-strike put and 50-strike call. Determine which of these graphs represents the payoff diagram for the overall position at the time of expiration of the options.

You are given:(i) The price of a nondividend-paying stock is $31.(ii) The continuously compounded risk-free interest rate is 10%.(iii) The price of a 3-month 30-strike European call option is $3.(iv) The price of a 3-month 30-strike European put option is $2.25. Construct a trading strategy that

The current price of a nondividend-paying stock is 60 and the continuously compounded risk-free interest rate is 6%.Actuary A writes a 1-year 70-strike call option whose price is 1.50. Actuary B enters into a 1-year synthetic long forward which permits him to buy the stock for 65 in one year.It is

You are given that one-year 15-strike European call and put premiums on a share of Iowa Inc. are 6.46 and 0.75, respectively. The stock pays dividends continuously at a rate proportional to its price. The dividend yield is 2%. The effective annual interest rate is 5%. Determine the strike price

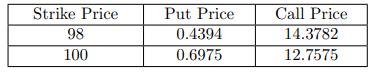

Stock X pays dividends continuously at a rate proportional to its price. The dividend yield is 2%. You are given the following option prices for European puts and calls, all written on stock X and with two years to expiration:Calculate the current price of stock X. Strike Price 98 100 Put

Determine which of the following statements about a long stock and a long K1-K2 collared stock is/are always correct.I. Both are long with respect to the underlying stock.II. The long collared stock requires a lower amount of initial investment than the long stock.III. The long collared stock has a

The current price of stock ABC is 40. Stock ABC pays dividends continuously at a rate proportional to its price. The dividend yield is 2%.You are given the following premiums of one-year European call options on stock ABC for various strike prices:The effective annual risk-free interest rate is

Farmer Brown grows wheat, and will be selling his crop in 6 months. The current price of wheat is 8.50 per bushel. To reduce the risk of fluctuation in price, Brown wants to use derivatives with a 6-month expiration date to sell wheat between 8.60 and 8.80 per bushel. Brown also wants to minimize

Happy Jalapenos, LLC has an exclusive contract to supply jalapeno peppers to the organizers of the annual jalapeno eating contest. The contract states that the contest organizers will take delivery of 10,000 jalapenos in one year at the market price. It will cost Happy Jalapenos 1,000 to provide

You are given:(i) An investor short-sells a nondividend-paying stock that has a current price of 44 per share.(ii) This investor also writes a collar on this stock consisting of a 40-strike European put option and a 50-strike European call option. Both options expire in one year.(iii) The prices of

Let C(K) and P(K) be the premiums of three-month K-strike European call and put options on the same stock, respectively. You are given that |C(60) − C(65)| = 3 and the continuously compounded risk-free interest rate is 5%. Calculate |P(60) − P(65)|.

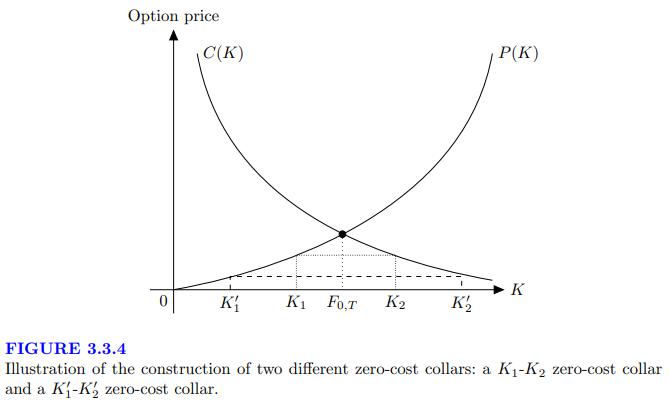

Determine which statement about zero-cost purchased collars is FALSE.(A) A zero-width, zero-cost collar can be created by setting both the put and call strike prices at the forward price.(B) There are an infinite number of zero-cost collars.(C) The put option can be at-the-money. (D) The call

You are given the following information:(i) The current price of stock Y is 30.(ii) Dividends of 1 per unit of stock will be paid in two months and in eight months.(iii) The continuously compounded risk-free interest rate is 6%.(iv) The price of a 1-year 32-strike European call option on stock Y is

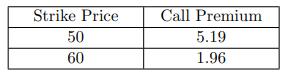

The current price of a nondividend-paying stock is 40 and the continuously compounded risk-free interest rate is 8%. The following table shows call option premiums for 3-month European options of various exercise prices:Student A constructs a 35-45 bull spread using call options. Student B

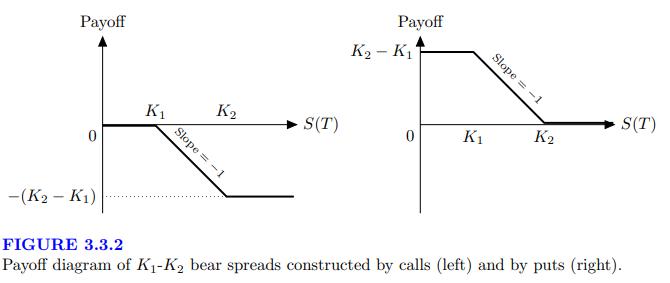

Determine whether each of the following strategies creates a long bear spread, assuming that all options are European and on the same underlying asset.(A) Buy a 45-strike call and sell a 50-strike call.(B) Buy a 45-strike put and sell a 50-strike put.(C) Buy a call with a price of 6 and sell a call

You are given that the price of a 70-strike call option is 8.3 and the price of a 80-strike call option is 2.7, where both options expire in one year and have the same underlying asset.The continuously compounded risk-free interest rate is 6%.You create a one-year 70-80 long bear spread using put

The following table shows the premiums of European call and put options having the same nondividend-paying stock, the same time to expiration but different strike prices:An investor constructs a 50-60 long bear spread using the above options and breaks even at expiration. Calculate the amount that

An investor wrote a 45-strike European call option on an index with three years to expiration. The premium for this option was 4.The investor also bought a 55-strike European call option on the same index with three years to expiration. The premium for this option was 2.5.The continuously

Consider a box spread based on two distinct strike prices K and L with K < L that is used to lend money, so that there is a positive cost to this transaction up front, but a guaranteed positive payoff at expiration.Determine which of the following sets of transactions is equivalent to this type of

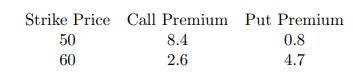

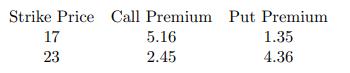

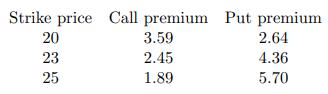

The following table shows the prices of European call and put options with the same underlying asset, time to expiration, but different strike prices:Calculate the profit on a 17-23 long collared stock position if the ending stock price is 22. Strike Price Call Premium Put

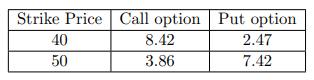

You are given the following information about four European options on the same underlying asset:(i) The price of a 25-strike 1-year call option is 6.85.(ii) The price of a 35-strike 1-year call option is 1.77.(iii) The price of a 25-strike 1-year put option is 0.63.(iv) The price of a 35-strike

The current price of a stock is 50. The stock will pay a single dividend of 0.75 in one month. The continuously compounded risk-free interest rate is 6%.The following table shows the premiums of 6-month European call options on the stock:Let S be the price of the stock six months from

Apple expects to sell pork bellies 3 months from now. The current 3-month forward price for pork belly is 4 per ton. Apple has decided to buy a zero-cost collar to reduce his exposure to the price of pork belly.Determine whether each of the following options could be a possible component of

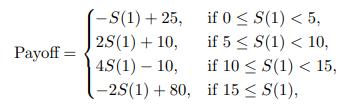

The payoff of a derivative contract maturing in one year is given bywhere S(1) is the one-year price of the underlying nondividend-paying stock. You are given:(i) The continuously compounded risk-free interest rate is 5%.(ii) The current stock price is 15.(iii) The price of a 10-strike 1-year call

Determine whether each of the following statements about zero-cost purchased collars on stocks is true or false. Assume that options at all positive strike prices are available for trading. Note that you are not given whether the underlying stock pays dividends or not. (A) A long zero-cost collar

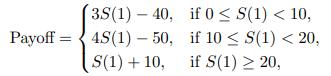

The payoff of a special 1-year derivative on a nondividend-paying stock is described by the following piecewise linear function:where S(1) is the one-year price of the stock.You are given:(i) The continuously compounded risk-free interest rate is 4%.(ii) The current stock price is 10.(iii) The

The stock of Iowa Actuarial Corporation has been trading in a narrow range around its current price of 45 per share for months. Dividends of 2 are payable quarterly, with the first dividend payable one month from now. The continuously compounded risk-free rate of interest is 6%.You are convinced

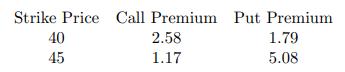

The current price of stock ABC is 40. Stock ABC pays dividends continuously at a rate proportional to its price. The dividend yield is 3%. The continuously compounded risk-free interest rate is 6%.The following table shows the premiums of two-year put options on stock ABC of various strike

The price of a stock has hovered around its current price of 70 for several months, but you believe that the stock price will break far out of that range over the next 4 months, without knowing whether it will go up or down. You have decided to take advantage of your conviction through an

The current price of stock XYZ is 1,000, and the continuously compounded risk-free interest rate is 8%. A dividend will be paid at the end of every 2 months over the next year, with the first dividend occurring 2 months from now. The amount of the first dividend is 12 = 1, that of the second

Determine whether each of the following statements about butterfly spread is true or false.(A) A long butterfly spread is a bet on the volatility of the underlying asset being higher than that perceived by the market.(B) Combining a long K1-K2 bear spread combined with a long K2-K3 bull spread

The following table shows the premiums of European call and put options having the same underlying stock, the same time to expiration but different strike prices:You use the above call and put options to construct an asymmetric butterfly spread with the following characteristics: (i) The maximum

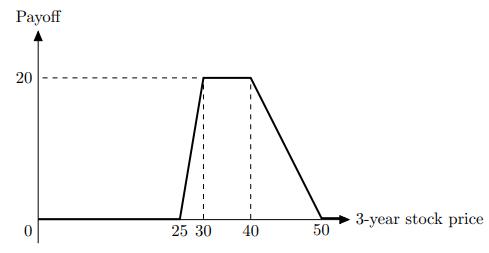

The payoff diagram of an investment strategy involving 3-year European put options on a stock is shown below:You are given:(i)(ii) The continuously compounded risk-free interest rate is 2.5%. Calculate the maximum possible profit of this investment strategy . Payoff 20 25 30 40 50 3-year stock

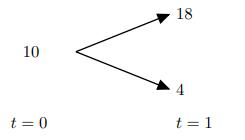

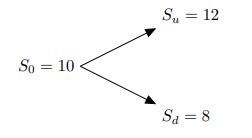

A nondividend-paying stock, S, is modeled by the binomial tree shown below.A European call option on S expires at t = 1 with strike price K = 12.Calculate the number of shares of stock in the replicating portfolio for this option.(A) Less than 0.3(B) At least 0.3, but less than 0.4(C) At least 0.4,

Consider the following information about a European call option on stock ABC:• The strike price is $95.• The current stock price is $100.• The time to expiration is 2 years.• The continuously compounded risk-free rate is 5% annually.• The stock pays no dividends.• The price is

Consider a 9-month dollar-denominated American put option on British pounds. You are given that:(i) The current exchange rate is 1.43 US dollars per pound.(ii) The strike price of the put is 1.56 US dollars per pound.(iii) The volatility of the exchange rate is σ = 0.3.(iv) The US dollar

Consider a 50-65 1-year strangle strategy. You are given:(i) The stock currently sells for $55.(ii) In one year, the stock will either sell for $70 or $45.(iii) The effective annual risk-free interest rate is 10%.Calculate the price you now pay for the strangle.

For a two-period binomial model, you are given:(i) Each period is one year.(ii) The current price for a nondividend-paying stock is 20.(iii) u = 1.2840, where u is one plus the rate of capital gain on the stock per period if the stock price goes up.(iv) d = 0.8607, where d is one plus the rate of

The price of a nondividend-paying stock is currently $50.00. It is known that at the end of two months, it will be either $54.00 or $46.00. The risk-free interest rate is 9.0% per annum with continuous compounding.Calculate the value of a two-month European call option with a strike price of $48 on

You are to price options on a futures contract. The movements of the futures price are modeled by a binomial tree. You are given:(i) Each period is 6 months.(ii) u/d = 4/3, where u is one plus the rate of gain on the futures price if it goes up, and d is one plus the rate of loss if it goes

For a two-year European put option, you are given the following information:• The stock price is $35.• The strike price is $32.• The continuously compounded risk-free rate is 5%.• The stock price volatility is 35%.Using a binomial tree with annual valuations, calculate the price of this

A price of a nondividend-paying stock is currently $40.It is known that at the end of one month the stock’s price will be either $42 or $38.The risk-free interest rate is 8% per annum with continuous compounding.(a) Determine the value of a one-month European call option with a strike price of

The current price of a nondividend-paying stock is S(0) = 100. The price of the stock at the end of one year, S(1), is either 90 or 120. The continuously compounded risk-free interest rate is 10%.Consider a derivative security that pays [S(1)]2 at the end of one year.(a) Determine the replicating

You use the following information to construct a binomial forward tree for modeling the price movements of a stock. (This tree is sometimes called a forward tree.)(i) The length of each period is one year.(ii) The current stock price is 100.(iii) The stock’s volatility is 30%.(iv) The stock pays

For a one-year straddle on a nondividend-paying stock, you are given:(i) The straddle can only be exercised at the end of one year.(ii) The payoff of the straddle is the absolute value of the difference between the strike price and the stock price at expiration date.(iii) The stock currently sells

The following one-period binomial stock price model was used to calculate the price of a one-year 10-strike call option on the stock.You are given:(i) The period is one year.(ii) The true probability of an up move is 0.75.(iii) The stock pays no dividends.(iv) The price of the one-year 10-strike

You use the following information to construct a binomial forward tree for modeling the price movements of a stock:(i) The length of each period is 4 months.(ii) The current stock price is 41.(iii) The stock’s volatility is 30%.(iv) The stock pays no dividends.(v) The continuously compounded

Suppose that the current stock price is $30 per share. At the end of 6 months, the stock price will be either $25 or $38. The 6-month effective risk-free interest rate is 10%.A European-type derivative written on this stock has its payoff in 6 months equal towhere S(T) is the stock price at

For a two-period binomial model for stock prices, you are given:(i) Each period is 6 months.(ii) The current price for a nondividend-paying stock is $70.00.(iii) u = 1.181, where u is one plus the rate of capital gain on the stock per period if the price goes up.(iv) d = 0.890, where d is one plus

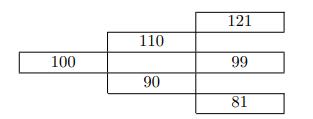

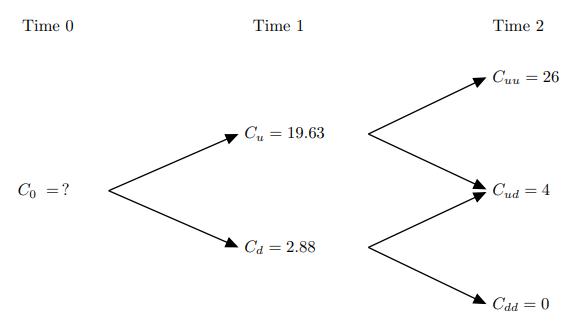

For a two-period binomial stock price model, you are given:(i) The length of each period is 1 year.(ii) The (incomplete) price evolution of a 2-year European call option on the stock:Calculate the current price of the call option. Time 0. Co=? Time 1 Cu = 19.63 Ca = 2.88 Time 2 Cuu = 26 Cud =

Rework Example 4.1.3 using risk-neutral valuation.Data from Example 4.1.3For a one-year straddle on a nondividend-paying stock, you are given:(i) The straddle can only be exercised at the end of one year.(ii) The payoff of the straddle is the absolute value of the difference between the strike

You are given:(i) The current price of a stock is $65.(ii) One year from now the stock will sell for either $60 or $70.(iii) The stock pays dividends continuously at a rate proportional to its price. The dividend yield is 4%.(iv) The continuously compounded risk-free interest rate is 6%.(v) The

You are given the following information about American options on a stock:• The current stock price is 72.• The strike price of the options is 80.• The continuously compounded risk-free rate is 5%.• Time to expiration is 1 year.• Every six months, the stock price either increases by 25%

You are given the following regarding stock of Widget World Wide (WWW):(i) The stock is currently selling for $50.(ii) One year from now the stock will sell for either $40 or $55.(iii) The stock pays dividends continuously at a rate proportional to its price. The dividend yield is 10%.The

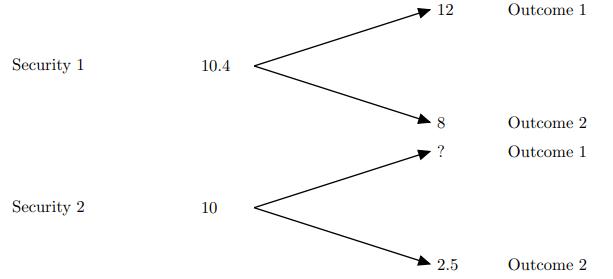

For a one-period arbitrage-free binomial model with two nondividend-paying securities, you are given:(i) The following price evolution of the two securities:(ii) The following information about two European call options: Calculate the current price of call option B. Security 1 Security

For a 10-period binomial stock price model, you are given:(i) The length of each period is one year.(ii) The current stock price is 1,000.(iii) At the end of every year, the stock price will either increase by 5% or decrease by 5% in proportion.(iv) The stock pays dividends continuously at a rate

You use the following information to construct a binomial forward tree for modeling the price movements of a stock.(i) The length of each period is one year.(ii) The current stock price is 82.(iii) The stock’s volatility is 30%.(iv) The stock pays no dividends.(v) The continuously compounded

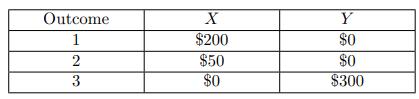

You are given the following information about a securities market:• There are two nondividend-paying stocks, X and Y .• The current prices for X and Y are both $100.• The continuously compounded risk-free interest rate is 10%.• There are three possible outcomes for the prices of X and Y one

You use the following information to construct a one-period binomial forward tree for modeling the price movements of a nondividend-paying stock. (The tree is sometimes called a forward tree.)(i) The period is 3 months.(ii) The initial stock price is $100.(iii) The stock’s volatility is 30%.(iv)

In an arbitrage-free securities market, there are two nondividend-paying stocks, A and B, both with current price $90. There are two possible outcomes for the prices of A and B one year from now:The current price of a one-year 100-strike European put option on B is $15. Determine all possible

An arbitrage-free securities market model consists of a bank account and one security. The security price today is 100. The security price one year from now will be either 104 or 107.Determine which of the following can be the bank account interest rate.(A) 0%(B) 3%(C) 5%(D) 8%(E) 10%

You are to use a binomial forward tree model to model the price movements of a stock that pays dividends continuously at a rate proportional to its price. The length of each period is three months. If Var[ln[S(t)]] = 0.25t for t > 0, find p∗ , the risk-neutral probability of an up move.

Showing 300 - 400

of 428

1

2

3

4

5

Step by Step Answers