New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

essentials accounting

Essentials Of Accounting 11th International Edition Leslie K. Breitner - Solutions

On January 5, Evergreen Market sold merchandise for $800 cash that had cost $500. This transaction consists of two separate events:(1) the sale, which, taken by itself, [increased / decreased] Retained Earnings by $800, and (2) the decrease in inventory, which, taken by itself, [increased /

Taken by itself, the increase in Retained Earnings resulting from operations is called a revenue . When Evergreen Market sold merchandise for $800, the transaction resulted in $800 of .

And taken by itself, the associated decrease in Retained Earnings is called an expense . When Evergreen Market transferred merchandise to the customer, the transaction reduced inventory and resulted in $500 of.

Thus, when Evergreen Market sold merchandise for $800 that cost $500, the effect of the transaction on Retained Earnings can be separated into two parts: a of $ and an of $ .

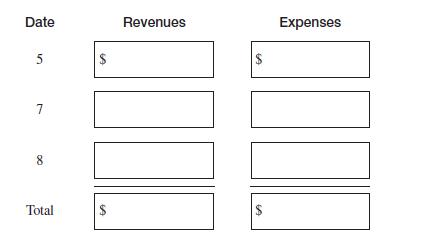

In accounting, revenues and expenses are recorded separately.From Exhibit 2, calculate the revenues and expenses for the period January 2 through 8 by completing the following table: Date 5 $ 7 8 00 Total Revenues $ Expenses $

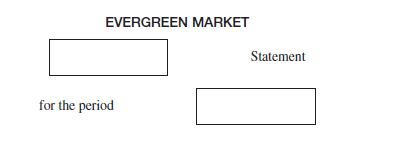

You can now prepare an income statement. Its heading shows the name of the accounting entity, the title of the statement, and the period covered. Complete the heading for Evergreen Market’s income statement for January 2–8: EVERGREEN MARKET for the period Statement

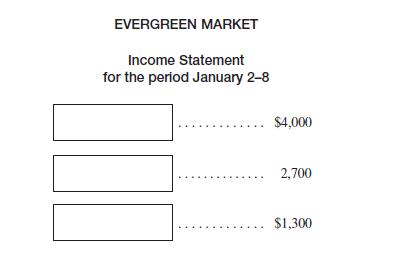

The income statement reports revenues and expenses for the period and the difference between them, which is income. Label the amounts in the following income statement for Evergreen Market. EVERGREEN MARKET Income Statement for the period January 2-8 $4,000 2,700 $1,300

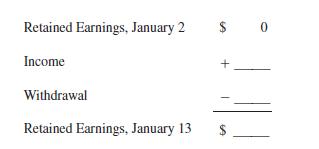

As the name suggests, Retained Earnings refers to the amount of income that has been r in the entity. On January 13, Berg withdrew $800 of assets for his personal use. This reduced R E by $ .

No other changes in Retained Earnings occurred. Complete the following table:The amount of Retained Earnings calculated [does / does not] equal the amount shown on the balance sheet of January 13. Retained Earnings, January 2 $ 0 + Income Withdrawal Retained Earnings, January 13

Assume that in the remainder of January, Evergreen Market had additional income of $1,500 and there were no additional withdrawals. Since Retained Earnings was $500 as of January 13, it would be $on January 31. Thus, the amount of Retained Earnings on a balance sheet is:A. the amount earned in the

The terms profit , earnings , and income all have the same meaning.They are the differences between the r ______ of an accounting period and the e ______ of that period. In nonprofit organizations, the term surplus refers to profit.

Remember that the equity section of the balance sheet reports the amount of capital that the entity has obtained from two different sources:1. The amount paid in by the owner(s), which is called P - C or simply C .2. The amount of income that has been retained in the entity, which is called R E .

The two financial statements may be compared to two reports on a reservoir. One report may show how much water flowed through the reservoir during the period, and the other report may show how much water was in the reservoir as of the end of the period. Similarly, the[balance sheet / income

Note also that withdrawals by owners (which are called dividends in a corporation) [are / are not] expenses. They [do / do not]appear on the income statement. They [do / do not] reduce income. They[do / do not] decrease Retained Earnings.

The two financial statements may be compared to two reports on a reservoir. One report may show how much water flowed through the reservoir during the period, and the other report may show how much water was in the reservoir as of the end of the period. Similarly, the [balance sheet / income

In Part 2 you recorded the effect of each transaction by changing the appropriate items on a balance sheet. Erasing the old amounts and writing in the new amounts [would / would not] be a practical method for handling the large number of transactions that occur in most entities.

Instead of changing balance sheet amounts directly, accountants use a device called an account to record each change. In its simplest form, an account looks like a large letter T, and it is therefore called a-account.

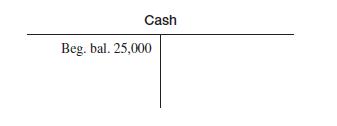

The title of the account is written on top of the T. Draw a T-account and title it “Cash.”

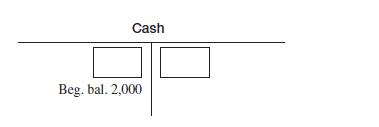

Following is how a T-account looks at the beginning of an accounting period.Evidently the amount of cash at the beginning of the accounting period was $ ______________ . Cash Beg. bal. 25,000

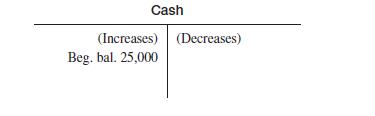

Transactions that affect the Cash account during the accounting period can either increase cash or decrease cash. Thus, one side of the T-account is for _______ s, and the other side is for _______ s.

Increases in cash add to the beginning balance. Because the beginning balance is recorded on the left side of the T-account, increases in cash are recorded on the [left / right] side of the T-account. Decreases are recorded on the [left / right] side.

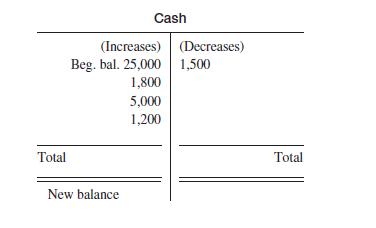

Here is the T-account for Cash.Record in the above T-account the effect of the following transactions on Cash:A. The entity received $1,800 cash from a customer.B. The entity borrowed $5,000 from a bank.C. The entity paid $1,500 cash to a supplier.D. The entity sold merchandise for $1,200 cash.

At the end of an accounting period, the increases are added to the beginning balance, and the total of the decreases is subtracted from it.The result is the new balance . Calculate the new balance for the Cash account shown below. Total Cash (Increases) (Decreases) Beg. bal. 25,000 1,500 1,800 New

The amount of the above Cash shown on the balance sheet at the end of the accounting period was $ __________________. The beginning balance of Cash in the next accounting period will be $ __________________.

In the T-account for Cash, increases are recorded on the [left /right] side. This is the rule for all asset accounts; that is, increases in accounts are recorded on the side.

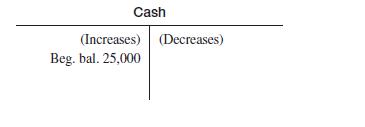

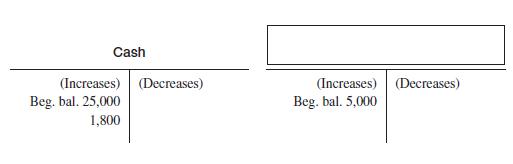

Suppose Brown Company received $1,800 cash from Sophie Michel to settle her Accounts Receivable. In the T-account below, the increase in Brown Company’s cash that results is recorded on the [left/right] side. Enter the amount. Cash (Increases) (Decreases) Beg. bal. 25,000

Sophie Michel, a customer of Brown Company, paid $1,800 cash to settle the amount she owed. The Cash account increased by$1,800. Michel no longer owed $1,800, so the A ______ R ________ account decreased by $1,800. In the T-account below, enter the name of this second account that must be changed

Accounts Receivable is an asset account. The dual-aspect concept requires that if the asset account, Cash, increases by $1,800, the change in the other asset account, Accounts Receivable, must be a(n) [increase /decrease] of $1,800.

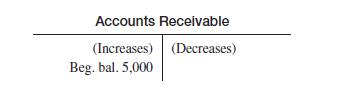

Record the change in Accounts Receivable resulting from the$1,800 payment in the account below. Accounts Receivable (Increases) (Decreases) Beg. bal. 5,000

The decrease in accounts receivable was recorded on the [left /right] side of the Accounts Receivable account. This balanced the [left /right] -side amount for the increase in Cash.

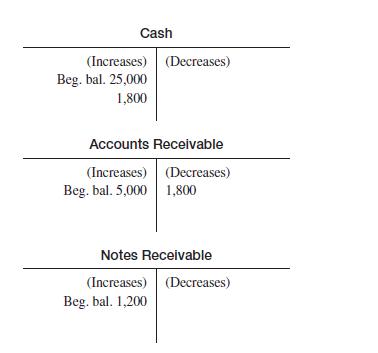

Another customer of Brown Company settled a $1,000 Accounts Receivable by paying $700 cash and giving a note for $300. Record this transaction in the Brown Company’s accounts, given below. Cash (Increases) (Decreases) Beg. bal. 25,000 1,800 Accounts Receivable (Increases) (Decreases) Beg. bal.

As you can see, accounting requires that each transaction give rise to [equal / unequal] totals of left-side and right-side amounts.This is consistent with the fundamental equation: A ____ 5 L _________ 1 E ____ .

An increase in any asset account is always recorded on the left side. Therefore, since the totals of left-side and right-side amounts must equal each other, a decrease in any asset must always be recorded on the[left / right] side.

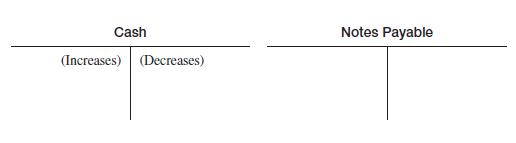

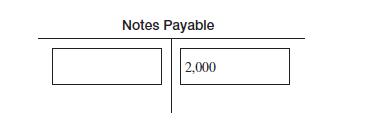

Black Company borrowed $2,000 from Northwest Bank, signing a note.Black Company’s Cash account [increased / decreased] by $2,000, and its Notes Payable account, which is a liability account, [increased /decreased] by the same amount.

Black Company borrowed $2,000 from Northwest Bank, signing a note.The $2,000 increase in Black Company’s cash is recorded on the [left /right] side of its Cash account. In order to show equal totals of right-side and left-side amounts, the corresponding change in the Notes Payable account is

Because left-side and right-side amounts must have equal totals, and because increases in assets are always recorded on the left side, increases in liability accounts, such as notes payable, are always recorded on the [left / right] side.

Similarly, because decreases in assets are always recorded on the right side, decreases in liabilities are always recorded on the [left side /right side].Show which side of the Notes Payable account is used to record increases and which side is used to record decreases by filling in the boxes

As the equation Assets 5 Liabilities 1 Equity indicates, the rules for equity accounts are the same as those for liability accounts, that is:Equity accounts increase on the [left / right] side.Equity accounts decrease on the [left / right] side.

One way to remember the above rules is to visualize the two sides of the balance sheet.Asset accounts are on the left side of the balance sheet, and they increase on the [left / right] side.Liability and equity accounts are on the right side of the balance sheet, and they increase on the [left /

The reasoning used in the preceding frames follows from the basic equation: __________________ = ______________________+ ______________________.

In the language of accounting, the left side of an account is called the debit side, and the right side is called the credit side. Thus, instead of saying that increases in cash are recorded on the left side of the Cash account and decreases are recorded on the right side, accountants say that

Debit and credit are also verbs. To record an increase in cash, you the Cash account. To record a decrease in cash, you the Cash account. Instead of saying, “Record an increase on the left side of the Cash account,” the accountant simply says,“ cash.”

Increases in all asset accounts, such as the Cash account, are recorded on the [debit / credit] side. To increase an asset account, you[debit / credit] the account.

The rules we just developed in terms of “left side” and “right side”can now be stated in terms of debit and credit.Increases in assets are [debits / credits].Decreases in assets are [debits / credits].Increases in liabilities are [debits / credits].Decreases in liabilities are [debits /

In everyday language the word credit sometimes means “good”and debit sometimes means “bad.” In the language of accounting, debit means only [left / right], and credit means only [left / right].

The word debit is abbreviated as “Dr.,” and the word credit is abbreviated as “Cr.” Label the two sides of the Cash account below with these abbreviations. Cash Beg. bal. 2,000

Exhibit 3 shows the accounts for Green Company, arranged as they would appear on a balance sheet. The sum of the debit balances is$ , and the sum of the credit balances is $ .

These totals are equal in accordance with the d __ -a ____ concept.

Record the following transactions in the accounts of Exhibit 3.Record increases in assets on the debit side and make sure that in each transaction the debit and credit amounts are equal.A. Inventory costing $600 was purchased for cash.B. Inventory costing $400 was purchased on credit.C. Green

Now calculate the new balances for each account and enter them in the accounts of Exhibit 3.

The total of the new balances of the asset accounts is$ . The total of the new balances of the liability and equity accounts is $ . Also, the total of the balances equals the total of the credit balances.3-36a. “Inventory costing $600 was purchased for cash.” There was a decrease in Cash; so

Because the total of the debit entries for any transaction should always equal the total of the credit entries, it is [difficult / easy] to check the accuracy with which bookkeeping is done. (We owe this ingenious arrangement to Venetian merchants, who invented it more than 500 years ago.)

The accounts in Exhibit 3 were for items that appear on the balance sheet. Accounts are also kept for items that appear on another financial statement, the i ____ statement. As we saw in Part 2 , this statement reports the revenues and the expenses of an accounting period and the difference between

Revenues are [increases / decreases] in equity during a period, and expenses are [increases / decreases] in equity.

For equity accounts, increases are recorded as [debits / credits].Because revenues are increases in equity, revenues are recorded as[debits / credits].

Similarly, decreases in equity are recorded as [debits / credits].Because expenses are decreases in equity, expenses are recorded as[debits / credits].

The complete set of rules for making entries to accounts is as follows:Increases in assets are [debits / credits].Decreases in assets are [debits / credits].Increases in liabilities and equity are [debits / credits].Decreases in liabilities and equity are [debits / credits].Increases in revenues

A group of accounts, such as those for Green Company in Exhibit 3, is called a ledger. There is no standard form, so long as there is space to record the d ___ s and c ____ s to each account. In Exhibits 4 and 5 we return to Evergreen Market, the same company we examined in Part 2 . Exhibit 5 is

In practice, transactions are not recorded directly in the ledger.First, they are written in a record such as Exhibit 4. The title of Exhibit 4 shows that this record is called a . The record made for each transaction is called a entry.

As Exhibit 4 shows, for each journal entry, the account to be[debited / credited] is listed first, and the [Dr. / Cr.] amount is entered in the first of the two money columns. The account to be [debited / credited]is listed below, and is indented. The [Dr. / Cr.] amount is entered in the second

On January 8, merchandise costing $1,200 was sold for $1,800, and the customer agreed to pay $1,800 within 30 days. Using the two journal entries for January 7 as a guide, record the two parts of this transaction in the journal. (If you are not sure about how to record this transaction, go to Frame

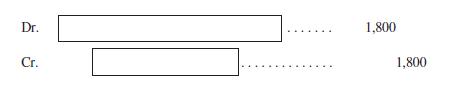

On January 8, merchandise costing $1,200 was sold for $1,800, and the customer agreed to pay $1,800 within 30 days.The first part of this transaction is that the business earned revenues of$1,800, and an asset, Accounts Receivable , increased by $1,800. Record this part of the transaction by

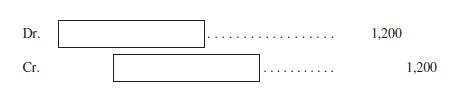

On January 8, merchandise costing $1,200 was sold for $1,800, and the customer agreed to pay $1,800 within 30 days.The other part of this transaction is that the business had an expense of$1,200 because its Inventory was decreased by $1,200. Record this part of the transaction by completing the

Journal entries are transferred to the l ____ (as in Exhibit 5). This process is called posting . The entries through January 7 have already been posted to the ledger, as indicated by the check mark opposite each one. Post the journal entries for January 8 to the proper ledger accounts in Exhibit

To summarize, any transaction requires at least(how many?) changes in the accounts. These changes are recorded first in the [ledger / journal]. They are then posted to the [ledger / journal].

The Revenues account in Exhibit 5 reports [increases / decreases]in Retained Earnings during the period, and the Expenses account reports[increases / decreases] in Retained Earnings. As we know, the difference between revenues and expenses is the net i ____ or n __ l ___ of the period.

The net income for the period is an increase in the equity account, R ______ E ______ . Net income is added to this account by a series of journal entries called closing entries .

In order to do this, we first must find the balance in the account that is to be closed. What is the balance in the Revenues account in Exhibit 5? $ _______________

An entry is made that reduces the balance in the account to be closed to zero and records the same amount in the Retained Earnings account. Because the Revenues account has a [Dr. / Cr.] balance, the entry that reduces Revenues to zero must be on the other side; that is, it must be a [Dr. / Cr.].

In Exhibit 4, write the journal entry that closes the $4,000 balance in the Revenues account to the Retained Earnings account. (Date it January 8, the end of the accounting period.)

Using similar reasoning, write the journal entry that closes the$2,700 balance in the Expenses account to the Retained Earnings account.

Next, post these two entries to the ledger in Exhibit 5.

To get ready for preparing the financial statements, the balance in each asset, liability, and equity account is calculated. (Revenue and expense accounts have zero balances because of the closing process.) For the Cash account in Exhibit 5, the calculation is as follows:Calculate the balance for

Journal entries change the balance in the account. The calculation of the balance does not change the balance. Therefore the calculation of a balance [does / does not] require a journal entry.

The balance sheet is prepared from the balances in the asset, liability, and equity accounts. Complete the balance sheet for Evergreen Market, as of January 8, in Exhibit 6.

The income statement is prepared from information in the Retained Earnings account. Complete the income statement in Exhibit 6.

After the closing process, the revenue and expense accounts have[debit / credit / zero] balances. These accounts are therefore temporary accounts . They are started over at the beginning of each period. The asset accounts have [debit / credit / zero] balances, and the liability and equity accounts

Most entities report individual items of revenues and expenses(such as salary expense, maintenance expense, insurance expense) on their income statement. In order to do this, they set up an account for each expense item. Thus, if the income statement reported 2 revenue items and 10 expense items,

Management needs more detailed information than is contained in the financial statements. For example, instead of one account, Accounts Receivable, it needs an account for each customer so that the amount owed by each customer is known. Therefore the ledger usually contains[the same number of /

In Part 3 we introduced the idea of net income , which is the difference between r ______ and e ______ .

Net income increases Retained Earnings. Retained Earnings is an item of [liabilities / equity] on the balance sheet. Any increase in Retained Earnings is also an increase in [liabilities / equity].

An income statement reports the amount of net income [at a moment in time / over a period of time]. The period of time covered by one income statement is called the accounting period .

For most entities, the official accounting period is one year, referred to as the fiscal year . However, financial statements, called interim statements, usually are prepared for shorter periods. In Part 3 you prepared an income statement for Evergreen Market for the period January 2 through

Entities don’t fire their employees and cease operations at the end of an accounting period. They continue from one accounting period to the next. The fact that accounting divides the stream of events into f ____ y __ s makes the problem of measuring revenues and expenses in a fiscal year [an

On January 3, Evergreen Market borrowed $10,000 from a bank.Its cash therefore [increased / decreased / did not change]. A liability[increased / decreased / did not change].

Revenues are increases in equity. The receipt of $10,000 cash as a loan from the bank on January 3 [increased / decreased / did not change].Evergreen Market revenues and therefore [increased / decreased / did not change] equity.

On January 4, Evergreen Market purchased $5,000 of inventory, paying cash. This was an increase in one asset and a decrease in another asset. Since equity was unchanged, the payment of cash on January 4[was / was not] associated with an expense.

On January 8, Evergreen Market sold merchandise for $1,800, and the customer agreed to pay $1,800 within 30 days. This transaction resulted in [an increase / a decrease / no change] in cash. Revenue was$ . This revenue [was / was not] associated with a change in cash on January 8.

Evidently revenues and expenses [are / are not] always accompanied, at the same time, by changes in cash. Moreover, changes in cash[are / are not] always coupled with corresponding changes in revenues or expenses.

Increases or decreases in cash are changes in an [equity / asset] account.Revenues or expenses are changes in an [equity / asset] account.

Net income is measured as the difference between [cash increases and cash decreases / revenues and expenses].

Net income measures the increase in e ____ during an accounting period that was associated with earnings activities.

Many individuals and some small businesses keep track only of cash receipts and cash payments. This type of accounting is called c __ accounting. If you keep a record of your bank deposits, the checks you write, and the balance in your bank account, you are doing ___ accounting. Cash accounting

Most entities, however, account for revenues and expenses, as well as for cash receipts and cash payments. This type of accounting is called accrual accounting . Evidently, accrual accounting is [simpler / more complicated] than cash accounting, but accrual accounting [does / does not] measure

Because net income is the change in equity and measures the entity’s financial performance, accrual accounting provides [more / less]information than cash accounting.

In order to measure the net income of a period, we must measure r _____ s and e _____ s of that period, and this requires the use of ______ accounting.

Suppose that in January, Bina Silver agreed to buy an automobile from Ace Auto Company; the automobile is to be delivered to Silver in March. Because Ace Auto Company is in the business of selling automobiles, it [would / would not] be happy that Silver has agreed to buy one.

Silver agreed in January to buy an automobile for delivery in March. Although Silver is [likely / unlikely] to take delivery in March, it is possible that she will change her mind. The sale of this automobile therefore is [absolutely certain / uncertain].

Silver agreed in January to buy an automobile for delivery in March.Because in January the sale of this automobile is uncertain, accounting[does / does not] recognize the revenue in January. If Jones does accept delivery in March, accounting recognizes r _____ in March.This is a [conservative /

Increases in equity are recognized only when they are reasonably certain . To be conservative, decreases in equity should be recognized as soon as they probably occurred. Suppose an automobile was stolen from Ace Auto Company in January, and the company waits until March to decide that the

Showing 900 - 1000

of 1099

1

2

3

4

5

6

7

8

9

10

11

Step by Step Answers