New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

essentials accounting

Essentials Of Accounting 11th International Edition Leslie K. Breitner - Solutions

The concept governing the recognition of expenses of a period is the matching concept . It is that costs associated with the revenues of a period are [cash payments / expenses] of that period .

As you learned in Part 4 , the concept governing the recognition of revenues of a period is the r _________ concept;revenue is recognized in the period in which goods or services are d _____ ed.

An important task of the accountant is to measure the net income of an accounting period. Net income is the difference between r _____ s and e _____ s of the period.Expenses are [expired / cash] costs.

Costs that have been consumed are gone; they have expired. Costs of resources still on hand are unexpired . You will find it useful to think of expenses as [expired / unexpired] costs and assets as [expired / unexpired]costs.

Costs that are used up or consumed in a period are e _____ s. Costs that are represented by resources on hand at the end of the period are a ___ s.

Expenditures result in costs. When inventory or other assets are acquired, they are recorded at their acquisition c __ . Expenses are the c __ of the resources used up in an accounting period.

Over the life of a business, most expenditures [will / will not] become expenses, but in a single accounting period, expenses [are / are not]necessarily the same as expenditures.

Sherbrooke Company purchased a two-year supply of fuel oil in 2011, paying $20,000. None was consumed in 2011, $16,000 was consumed in 2012, and $4,000 was consumed in 2013. The item Fuel Oil Expense on the income statements will be as follows:For the year 2011 . . . . . . . . . . . . . . . . . . .

Sherbrooke Company purchased a two-year supply of fuel oil in 2011, paying $20,000. None of it was consumed in 2011, $16,000 was consumed during 2012, and $4,000 was consumed in 2013. The balance sheet item for the asset Fuel Oil Inventory will show the following amounts:As of December 31, 2011 . .

Between the time of their purchase and the time of their consumption, the resources of a business are assets. Thus, when fuel oil is purchased, there is an expenditure. The fuel oil is an until consumed. When consumed, it becomes an .

When an asset is used up or consumed in the operations of the business, an expense is incurred. Thus, an asset gives rise to an [expenditure /expense] when it is acquired, and to an [expenditure / expense] when it is consumed.

In August, Juarez Shop paid an employee $2,000 cash for services rendered in August. It had both an and an of $2,000 for labor services in August.

Juarez Shop sold the remaining $2,500 of goods in September. In September it had an [expenditure / expense] of $2,500, but it did not have any [expenditure / expense] for these goods in September.

Juarez Shop had e _________ s of $3,000 in August for the purchase of goods for inventory. If $500 of these goods were sold in August, there was an expense in August of $500. The remaining$2,500 of goods are still in inventory at the end of August;they therefore are an asset . Thus, the

Thus, an expenditure results either in a decrease in the asset account C __ or an increase in a l _______ , such as Accounts Payable.

If in August, Juarez Shop purchased $2,000 of goods for inventory, agreeing to pay in 30 days, it had an e _________ of $2,000 in August. Accounts Payable, which is a liability account, increased.Juarez would record this transaction with the following journal entry:Dr. I ___________ . . . . . . . .

Revenues are [increases / decreases] in equity during an accounting period. Expenses are [increases / decreases] in equity during an accounting period. Just as revenues in a period are not necessarily the same as cash receipts in that period, the expenses of a period [are / are not] necessarily the

In Part 4 you learned that the revenues recognized in an accounting period were not necessarily associated with the cash receipts in that period. If $1,000 of goods were delivered to a customer in May, and the customer paid cash for these goods in June, revenue would be recognized in [May / June].

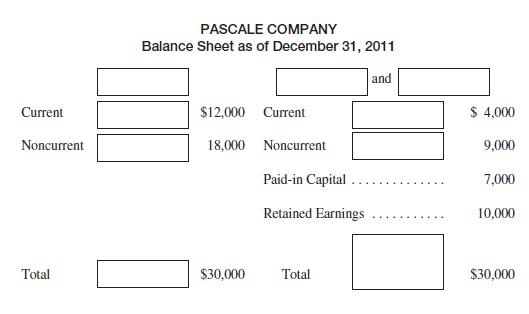

In earlier parts, you learned that the balance sheet has two sides with equal totals. Fill in the two missing names in the boxes in the simplified balance sheet given on the following page. PASCALE COMPANY Balance Sheet as of December 31, 2011 and Current $12,000 Current $ 4,000 Noncurrent 18,000

For Pascale Company, we can say that $4,000 of the $12,000 in current assets was financed by the c _____ liabilities. The remaining $8,000 of current assets and the $18,000 of noncurrent assets were financed by the $9,000 of plus the $17,000 of .

That part of the current assets not financed by the current liabilities is called working capital. Working capital is therefore the difference between c a and c l . In the example given above, working capital is:

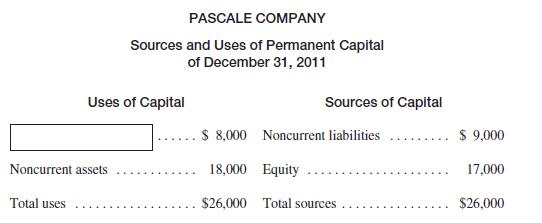

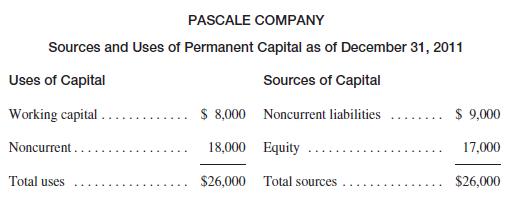

To highlight how working capital and the noncurrent assets were financed, we can rearrange the items on the balance sheet as follows:Fill in the box above. PASCALE COMPANY Sources and Uses of Permanent Capital of December 31, 2011 Uses of Capital Sources of Capital $ 8,000 Noncurrent liabilities

The right-hand side of the balance sheet given above shows the sources of capital used to finance the working capital and the noncurrent assets. Collectively, these sources are called permanent capital . As the balance sheet indicates, there are two sources of permanent capital:(1) N _______ t l

Although most liabilities are debts, the term debt capital refers only to noncurrent liabilities. Debt capital therefore refers to liabilities that come due [within 1 year / sometime after 1 year].

A common source of debt capital is the issuance of bonds . A bond is a written promise to pay someone who lends money to the entity.Since a bond usually is a noncurrent liability, the payments are due[within 1 year / sometime after 1 year].

The total amount that must be repaid is specified on the face of a bond and is termed the face amount .If Martine Company issues 10-year bonds whose face amounts total$120,000, Martine Company has a liability, Bonds Payable, of$ .

Suppose that Martine Company receives $120,000 cash from the issuance of bonds that have a face amount of $120,000. Write the journal entry necessary to record the effect of this transaction on the Cash and Bonds Payable accounts. Dr. Cr.

When they are issued, the bonds are [current / noncurrent] liabilities.However, as time passes and the due date becomes less than 1 year, a bond becomes a [current / noncurrent] liability. In 2011, a bond that is due on January 1, 2013, would be a [current / noncurrent] liability. In 2012, the same

When an entity issues bonds, it assumes two obligations: (1) to repay the face amount, the principal , on the due date, and (2) to pay interest , often, but not always, at semiannual intervals (i.e., twice a year). The obligation to pay the principal is usually a [current /noncurrent] liability.

Interest on bonds is an expense and should be recognized in the accounting period to which the interest applies. Thus, if in January 2012 an entity makes a semiannual interest payment of $3,000 to cover the last six months of 2011, this interest expense should be recognized in 20 _ . This is

The $3,000 of unpaid interest that was an expense in 2011 is recorded in 2011 by the following entry: Dr. I E Cr. I 3,000 3,000

In 2012, when this interest was paid to the bondholders, the following entry would be made:Dr. . . . . . . . . . . . . . . . . . . 3,000 Cr. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,000 As the above entries indicate, on the balance sheet, at any given time, the

Some companies obtain funds by issuing an instrument that is backed by other instruments. For example, a bank may issue an instrument that promises to pay interest from a portfolio of mortgages it holds. The return on such an instrument is derived from the underlying mortgages, and the instrument

As noted in earlier parts, there are two sources of equity capital:1. Amounts paid in by equity investors, who are the entity’s owners.This amount is called [Paid-in Capital / Retained Earnings].2. Amounts generated by the profitable operation of the entity. This amount is called [Paid-in Capital

Some entities do not report these two sources separately. An unincorporated business owned by a single person is called a proprietorship .The equity item in a proprietorship is often reported by giving the proprietor’s name, followed by the word “Capital.”Dora Koop is the proprietor of

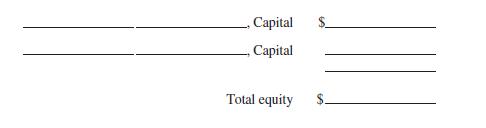

A partnership is an unincorporated business owned by two or more persons jointly. If there are only a few partners, the equity of each would be shown separately.Rick Crawley and Colette Webb are equal partners in a laundry business.On December 31, 2011, the equity in the business totaled $180,000.

Equity in a partnership consists of capital paid in by owners plus earnings retained in the business. Thus the item “Rick Crawley, Capital,$90,000” means (circle the correct answer) :A. Rick Crawley contributed $90,000 cash to the entity.B. The entity owes Rick Crawley $90,000.C. Rick

Owners of a corporation are called shareholders because they hold shares of the corporation’s stock. The equity section of a corporation’s balance sheet is therefore labeled s _________ e ___ y.

There are two types of shareholders: common shareholders and preferred shareholders . The stock held by the former is called c stock, and that held by the latter is called p stock. We shall first describe accounting for common stock.

Some stock is issued with a specific amount printed on the face of each certificate. This amount is called the par value . P _ v ___ often has no real meaning other than the nominal amount shown on the stock certificate. See below.

The amount that the shareholders paid the corporation in exchange for their stock is paid-in capital . The difference between par value and the total paid-in capital is called additional paid-in capital .Florent paid $10,000 cash to Pinnacle Company and received 1,000 shares of its $1 par-value

If Florent’s payment of $10,000 was the only equity transaction, this section of the Pinnacle Company balance sheet would appear as follows:Common stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $Additional paid-in capital . . . . . . . . . . . . . . . . . . .

Not all stocks have a par value. For these no-par-value stocks , the directors state a value. This value, called the s ___ d value, is usually set close to the amount that the corporation actually receives from the issuance of the stock. The difference between this amount and cash received is A

When a corporation is formed, its directors vote to authorize a certain number of shares of stock and generally to issue some of this authorized stock to investors. Thus, at any given time the amount of stock authorized is usually [larger than / the same as / smaller than] the amount issued.

A corporation may buy back some of the stock that it had previously issued. Such stock is called treasury stock . The outstanding stock consists of the issued stock less the treasury stock.If a company issues 100,000 shares and buys back 15,000 shares, its treasury stock is shares, and its

The balance sheet amount for common stock is the amount for the number of shares of stock outstanding.Adatto Company has authorized 100,000 shares of stock. It has issued 60,000 shares, for which it received the stated value of $10 per share. As of December 31, 2011, it has bought back 10,000

Shareholders may sell their stock to other investors. Such sales[do / do not] affect the balance sheet of the corporation. This is an example of the _____ concept.

When shareholders sell their stock to other investors, the price at which the sale takes place is determined in the marketplace. The value at which a stock is sold in such a transaction is called the [market / par /stated] value.

The market value of a company’s stock has no necessary relation to its par value, its stated value, or the amount of paid-in capital. If the par value of a certain stock is $1, the market value [will be $1 / can be any value].If the stated value of another stock is $10, the market value [will be

The amount reported as total equity equals total assets less total liabilities.On the balance sheet, this is not likely to equal the total market value of all stock outstanding. Evidently accounting [does / does not]report the market value of the shareholders’ equity.

Some corporations issue stock that gives its owners preferential treatment over the common shareholders. As the word “preferential” suggests, such stock is called p _____ ed stock.

Usually preferred shareholders have a preferential claim over the common shareholders for the par value of their stock. Thus, if the corporation were liquidated, the owner of 500 shares of $100 preferred stock would have to receive $ before the common shareholders received anything.

As you learned earlier, par value of common stock has [some / almost no] significance. Because preferred stock usually does have a preferential claim on assets equal to its par value, its par value has [some /almost no] significance.

Preferred shareholders usually have rights to a stated amount of dividends. Stillwater Corporation has issued $100,000 of 9 percent preferred stock. No dividend can be paid to common shareholders until the preferred shareholders have received their full dividend of 9 percent of$100,000, amounting

The net income of a period increases e ____ . The directors may vote to distribute money to the shareholders in the form of dividends. Dividends decrease e ____ .

Earnings is another name for “net income.” If earnings are not distributed as dividends, they are retained in the corporation. This amount is reported on the balance sheet as R ______ E _____ s.

The Retained Earnings account [decreases / increases] by the amount of net income each period and [decreases / increases] by the amount of dividends. Thus, if Retained Earnings are $100,000 at the start of a period during which a dividend of $20,000 is declared and during which net income is

Net income refers to the increase in equity [in 1 year / over the life of the corporation to date], whereas retained earnings refers to the net increases, after deduction of dividends, [in 1 year / over the life of the corporation to date].

Retained earnings is one source of capital. It is reported on the[left / right] side of the balance sheet. The capital is in the form of assets, and assets are reported on the [left / right] side of the balance sheet.

Equity is sometimes called “net worth.” This term suggests that the amount of equity shows what the owners’ claim on the assets is worth. Because the amounts reported on the assets side of the balance sheet [do / do not] represent the real worth of these assets, this suggestion is

The actual worth of a company’s stock is what people will pay for it. This is the market price of the stock, which [does / does not] appear anywhere on the balance sheet.

Most corporations make an annual cash payment to their common shareholders. This is called a dividend. If Livingston Company declared and paid a dividend of $5 per share, and if it had 100,000 shares of common stock outstanding, the dividend would be $ .The journal entry to record the effect of

A company may distribute to shareholders a noncash asset, such as shares of stock in other companies it owns or even one of its products.The effect of this distribution is a [debit / credit] to Retained Earnings and an equal [debit / credit] to the asset account.

Livingston Company might declare a stock dividend . If it distributed one share of its own stock for each 10 shares of stock outstanding, shareholders would have more shares. No asset decreased, so, in order to maintain equality, equity would [increase / decrease / be unchanged].

Similarly, Livingston might send its shareholders additional shares equal to the number of shares they own, or even double or triple this number of shares. Livingston may do this because it believes a high market price per share has an undesirable influence in trading the stock. This is called a

A stock split has the same effect as a stock dividend. Cash[increases / decreases / is unchanged]. Retained Earnings [increases /decreases / is unchanged]. The market price per share [increases /decreases / is unchanged].

A corporation obtains some capital from retained earnings. In addition, it obtains capital from the issuance of stock, which is [debt /equity] capital, and from the issuance of bonds, which is [debt / equity]capital.

A corporation has no fixed obligations to its common shareholders;that is, the company [must / need not] declare dividends each year, and [must / need not] repay the amount the shareholders have invested.

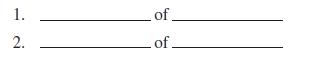

A company has two fixed obligations to its bondholders, however: 1. .of. 2. .of.

If the company fails to pay either the interest or the principal when due, the bondholders may force the company into bankruptcy.Evidently bonds are a [less / more] risky method of raising capital by the corporation than stock; that is, debt capital is a [less / more] risky source of capital than

Bonds are an obligation of the company that issues them, but stocks are not an obligation. Therefore, investors usually have more risk if they invest in a company’s stock than if they invest in the bonds of the same company. They are not certain to get either dividends or repayment of their

For example, if a company’s bonds had an interest rate of 7 percent, investors would invest in its stock only if they expected that the return on stock would be [at least 7 percent / considerably more than 7 percent]. (The expected return on stock consists of both expected dividends and an

Thus, from the viewpoint of the issuing company, stock, which is[debt / equity] capital, is a [more / less] expensive source of capital than bonds, which are [debt / equity] capital.

Circle the correct words in the following table, which shows the principal differences between debt capital and equity capital.Bonds (Debt) Stock (Equity)Annual payments required [Yes / No] [Yes / No]Principal payments required [Yes / No] [Yes / No]Risk to the entity is [High / Low] [High / Low]But

In deciding on its permanent capital structure, a company must decide on the proper balance between debt capital, which has a relatively[high / low] risk and a relatively [high / low] cost, and equity capital, which has a relatively [high / low] risk and a relatively [high / low] cost.

A company runs the risk of going bankrupt if it has too high a proportion of [debt / equity] capital. A company pays an unnecessarily high cost for its permanent capital if it has too high a proportion of [debt /equity] capital.

A company that obtains a high proportion of its permanent capital from debt is said to be highly leveraged . If such a company does not get into financial difficulty, it will earn a high return for its equity investors because each dollar of debt capital takes the place of a [more / less] expensive

However, highly leveraged companies are risky because the high proportion of debt capital and the associated requirement to pay interest[increases / decreases] the chance that the company will not be able to meet its obligations.

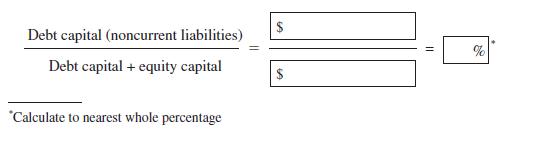

A common way of measuring the relative amount of debt and equity capital is the debt ratio , which is the ratio of debt capital to total permanent capital. Recall that debt capital is another name for [total /current / noncurrent] liabilities. Equity capital consists of total Paid-in Capital plus R

Earlier you worked with the following permanent capital structure:Calculate the debt ratio for Pascale Company. PASCALE COMPANY Sources and Uses of Permanent Capital as of December 31, 2011 Uses of Capital Sources of Capital Working capital $ 8,000 Noncurrent liabilities .... $ 9,000 Noncurrent...

Most industrial companies have a debt ratio of less than 50 percent.Pascale Company [is / is not] in this category.

A corporation that controls one or more other corporations is called the parent , and the controlled corporations are called subsidiaries .Palm Company owns 100 percent of the stock of Sea Company, 60 percent of the stock of Sand Company, and 40 percent of the stock of Shell Company. The parent

Since the management of the parent corporation, Palm Company, controls the activities of Sea Company and Sand Company, these three companies function as a single entity. The e ____ concept requires that a set of financial statements be prepared for this family.

Each corporation is a legal entity, with its own financial statements.The set of financial statements for the whole family brings together, or consolidates , these separate statements. The set for the whole family is therefore called a c _________ d financial statement.

For example, if Palm Company has $20,000 cash, Sea Company has $15,000 cash, and Sand Company has $14,000 cash, the whole family has $ cash, and this amount would be reported on the c balance sheet.

An entity earns income by making sales to outside customers. It cannot earn income by dealing with itself. Corporations in the consolidated family may buy from and sell to one another. Transactions between members of the family [do / do not] earn income for the consolidated entity. The effect of

In 2011, Palm Company had sales revenue of $1,200,000, Sea Company had sales revenue of $250,000, and Sand Company had sales revenue of $400,000. Palm Company sold $30,000 of products to Sea Company. All other sales were to outside customers. On the consolidated income statement, the amount of

Intrafamily transactions are also eliminated from the consolidated balance sheet. For example, if Sand Company owed Palm Company$10,000, this amount would appear as Accounts [Receivable / Payable]on the balance sheet of Palm Company and as Accounts [Receivable /Payable] on the balance sheet of Sand

The balance sheet of Palm Company reports as an asset the Sand Company and Sea Company stock that it owns. This asset [remains unchanged / must be eliminated] from the consolidated balance sheet.On the balance sheets of the subsidiaries, the corresponding amounts are reported as [noncurrent

Palm Company owns 40 percent of Shell Company stock. This asset is listed on Palm Company’s balance sheet at $100,000. This asset would not be eliminated from the consolidated balance sheet. Why not?

Palm Company owns 60 percent of the stock of Sand Company.This stock was reported on the balance sheet of Palm Company as an asset, Investment in Subsidiaries, at $60,000. The total equity of Sand Corporation is $100,000. On the consolidated balance sheet, the $60,000 asset would be eliminated, and

Palm Company owns 60 percent of Sand Company’s stock, which is a [majority / minority] of the stock. Other shareholders own the other 40 percent of Sand Company stock; they are [majority / minority] shareholders.They have an interest in the consolidated entity, and this interest is reported in

The consolidated income statement reports revenues from [all sales / sales to outside parties only] and expenses resulting from [all costs incurred / costs incurred with outside parties]. Intrafamily revenues and expenses are e ________ d.

The consolidated financial statements report on the entity called“Palm Company and Subsidiaries.” This family of corporations [is / is not] an economic entity, but it [is / is not] a legal entity.

Many corporations have subsidiaries. Since the consolidated financial statements give the best information about the economic entity, many published financial statements are c _________ d financial statements.

In the income statement in Part 5 , the first item subtracted from sales revenue was called Cost of Sales . It is the cost of the same products whose revenues are included in the sales amount. This is an example of the m ______ concept. (Some businesses call this item Cost of Goods Sold .) In most

In some entities, matching cost of sales and sales revenue is easy.For example, an automobile dealer keeps a record of the cost of each automobile in its inventory. If the dealer sold two automobiles during a given month, one for $40,000 that had cost $35,000, and the other for$30,000 that had cost

A dealer sold an automobile costing $35,000 for $40,000 cash.Write the journal entry that records the effect of this transaction solely on the Sales Revenue and Cash accounts: Dr. Cr.

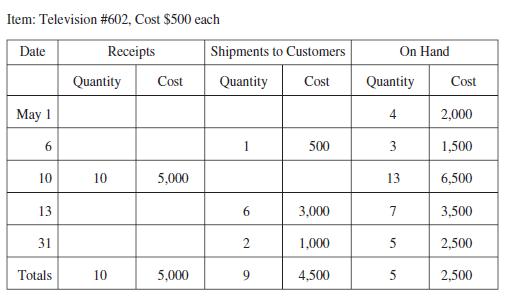

A dealer that sells televisions might keep a record of its inventory of each type of television, something like the following:This is called a perpetual inventory record. “Receipts” are [increases /decreases] in inventory, and “Shipments to Customers” are [increases /decreases] in

Information in the perpetual inventory records corresponds to that in the Inventory account. From the previous frame, we see that the beginning balance for Television #602 in the Inventory account on May 1 was$ ____ . There were receipts during May of $ _____ , which added to Inventory; these were

Showing 600 - 700

of 1099

1

2

3

4

5

6

7

8

9

10

11

Step by Step Answers