New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

essentials accounting

Essentials Of Accounting 11th International Edition Leslie K. Breitner - Solutions

Because of this, charging off an equal fraction of the asset cost each year is called the s ______ -line method of depreciation.Most companies use this method.

In the units-of-production method, a cost per unit of production is calculated, and depreciation expense for a year is found by multiplying this unit cost by the number of units that the asset produced in that year.Clark Company purchased a truck in 2011 for $44,000. It estimated that the truck

Here is a list of factors that are relevant to the depreciation of an asset:1. original cost 2. residual value 3. service life Which factors are used in arriving at the depreciable cost?. . . . . . . . . . . .The amount of depreciation expense in a given year?. . . . . . . . . . . . . . . . .Which

The difference between the cost of a plant asset and its residual value is called the depreciable cost . Thus, if an automobile purchased for$30,000 is expected to have a 5-year life and to have a residual value of$5,000 at the end of that life, $30,000 is the original and$25,000 is the .

Suppose a restaurant oven that cost $22,000 is expected to have a residual value of $2,000 at the end of its 10-year life. In this case, the total amount of depreciation that should be recorded during the service life of the asset is only $ . The depreciation expense for each of the 10 years would

In most cases, an entity expects that a plant asset will be worthless at the end of its service life. If so, its residual value is(how much?).

In some cases, an entity expects to be able to sell the plant asset at the end of its service life. The amount that it expects to sell it for is called its residual value . If an entity buys a truck for $75,000 and expects to sell it for $15,000 five years later, the estimated residual value is$ .

In the summary above, no mention was made of market value.Depreciation [is / is not] related to changes in the market value of an asset. This is consistent with the -concept.

To summarize:1. Depreciation is the process of converting the cost of an asset into expense over its service life.2. This process recognizes that an asset gradually loses its usefulness.3. An asset can lose its usefulness for either of two reasons:a. . . . . . . . . . . . . . . . . . . . . . . . .

Since depreciation considers obsolescence, it is [correct / not correct] to regard depreciation and obsolescence as two different things.

The service life of an asset considers both physical wear and obsolescence.The service life is the shorter of the two periods. Thus an asset with an estimated physical life of 12 years that is estimated to become obsolete in 8 years has an estimated service life of [8 / 12] years.

A plant asset can become useless for either of two reasons: (1) it may wear out physically, or (2) it may become obsolete (i.e., no longer useful). The latter reason is called obsolescence . Loss of usefulness because of the development of improved equipment, changes in style, or other causes not

The portion of the cost of a plant asset that is recognized as an expense during each year of its estimated service life is called depreciation. The $15,000 recorded as an expense during each one of the eight years of service life of the machine that cost $120,000 is called the expense for that

Since some portion of a plant asset is used up during each year of its service life, a portion of the cost of the asset is treated as a(n) [revenue /expense] in each year. For example, suppose a machine is purchased at a cost of $120,000. It has an estimated service life of eight years and will be

When a machine or other item of plant is acquired, we [know / do not know] how long it actually will be of service. Therefore, we [can know with certainty / must estimate] its service life.

The period of time over which a plant asset is estimated to be of service to the company is called its s _____ life.

Plant assets will become completely useless at some future time. At that time, the item is no longer an asset. Usually this process occurs gradually; that is, a portion of the asset is used up in each year of its life, until finally it is scrapped or sold and therefore is no longer __ ful to the

Unlike land, plant assets eventually become useless. They have a(n) [limited / unlimited] life.

Except in rare cases, land retains its usefulness indefinitely. Land therefore continues to be reported on the balance sheet at its acquisition cost, in accordance with the - concept.This is because land is a [monetary / nonmonetary] asset.If Hanover Hospital purchased a plot of land in 1996 at a

Even though the entity does not own the item, a capital lease is treated like other plant assets. A capital lease is an exception to the general rule that assets are property or property rights that are _ ____ by the entity.

The amount recorded for a capital lease is the amount the entity would have paid if it had purchased the item rather than leased it. If an entity leased a machine for 10 years, agreeing to pay $12,500 per year, and if the purchase price of this machine was $100,000, this c _____ l ___ would be

However, if an entity leases an item for a long period of time, it has as much control over the use of that item as if it owned it. A lease for a long time—almost the whole life of the asset—is called a capital lease . Because the entity controls the item for almost its whole life, a c _____ l

Most assets are owned by the entity. When an entity leases (i.e., rents) a building, a machine, or other tangible item, the item is owned by someone else (the lessor ); the entity [does / does not] own it. In other words, most leased items [are / are not] assets of the entity that leases them (the

If an entity constructs a machine or a building with its own personnel, all costs incurred in construction are included in the asset amount.Madrona Company built a new building for its own use. It spent$800,000 in materials, $2,850,000 in salaries to workers directly engaged in the building’s

Transportation and installation costs are usually included as part of equipment cost.Cascade Bank purchased a computer system for $42,000. The bank also paid $500 in freight charges and $2,600 in installation charges.This equipment should be recorded in the accounts at its cost,$ .

The cost of an asset includes all costs incurred to make the asset ready for its intended use.Northfield Corporation paid $125,000 for a plot of land. It also paid$5,000 as a broker’s fee, $1,250 for legal fees, and $12,000 to tear down the existing structures in order to make the land ready for

When an item of PPE is acquired, it is recorded in the accounts at its c (what value?). This is because it is a [monetary /nonmonetary] asset.

For brevity, we shall use the term PPE (property, plant, and equipment)for all tangible noncurrent assets except land. Thus, buildings, equipment, and furniture are items of __ . These assets are expected to be useful for longer than .

On the balance sheet, tangible noncurrent assets are often labeled fixed assets , or property , plant , and equipment . Equipment is a [current /noncurrent] and [tangible / intangible] asset.

Tangible assets are assets that can be touched. Intangible assets are assets that have no physical substance (other than pieces of paper) but give the entity valuable rights. Which of the following are tangible assets?Current Assets Noncurrent Assets 1. Prepaid rent 5. Goodwill 2. Inventory 6.

Earlier, you learned that current assets are cash or items likely to be converted to cash within one (what time period?).Evidently, noncurrent assets are expected to be of use to the entity for longer than .

Current assets are cash and other assets that are expected to be converted into cash or used up in the near future, usually within ___ .

Securities are stocks and bonds. They give valuable rights to the entity that owns them. The U.S. Treasury promises to pay stated amounts of money to entities that own treasury bonds. Therefore, U.S. Treasury Bonds owned by Garsden Company [are / are not] assets of Garsden Company.

Marketable securities are securities that are expected to be converted into cash within a year. An entity owns these securities so as to earn a return on funds that otherwise would be idle. Marketable securities are [current / noncurrent] assets.

An account receivable is an amount that is owed to the business, usually by one of its customers, as a result of the ordinary extension of credit. A customer’s monthly bill from the electric company would be an a _____ r ________ of the electric company until the customer paid the bill.

Inventories are goods being held for sale, as well as supplies, raw materials, and partially finished products that will be sold upon completion.For example, a truck owned by an automobile dealer for resale to its customers [is / is not] inventory. A truck owned by an entity and used to transport

In Exhibit 1 the inventories of Garsden Company are reported as$ .

An entity’s burglar-alarm system is valuable because it provides protection against loss. The burglar-alarm system is an asset. Would a fire insurance policy that protects the entity against losses caused by fire damage also be an asset? [Yes / No]

Entities buy fire insurance protection ahead of the period that the insurance policy covers. When they buy the insurance policy, they have acquired an a ___ . Because the policy covers only a short period of time, the asset is a [current / noncurrent] asset. Insurance protection can’t be touched.

Prepaid expenses is the name for intangible assets that will be used up in the near future; that is, they are intangible [current / noncurrent]assets. (The reason for using the word “expense” will be explained in Part 5 .)Exhibit 1 shows that Garsden Company had $ of prepaid expenses on

Tangible assets are assets that can be touched; they have physical substance. Buildings, trucks, and machines are t ______ assets. They are also [current / noncurrent] assets.

As indicated by the first item listed under Noncurrent Assets in Exhibit 1, the usual name for tangible, noncurrent assets is, , and . Because they are noncurrent, we know that these assets are expected to be used in the entity for more than (how long?).

Exhibit 1 shows the [cost / market value] of property, plant, and equipment to be $33,360,000. It shows that a portion of the cost of this asset has been subtracted from the original cost because it has been “used up.” This “used-up” portion is labeled and totals $ .

After this amount is subtracted, the asset amount is shown as $ . This is the amount of cost that [has / has not] been used up. (In Part 7 , we shall explain this amount further.)

The other noncurrent asset items are intangible assets ; that is, they have no physical substance, except as pieces of paper. The Investments item consists of securities, such as bonds. Evidently Garsden Company does not intend to turn these investments into cash within(how long?). If these

The next noncurrent asset reported is titled Patents and Trademarks . These are rights to use patents and rights to valuable brand names or logos (such as “ADVIL”). Because they are assets, we know that 1. they are v ______ ;2. they are o ___ by Garsden Company; and 3. they were acquired at a

Goodwill , the final item on the asset side, has a special meaning in accounting. It arises when one company buys another company and pays more than the value of its net identifiable assets. Grady Company bought Baker Company, paying $1,400,000 cash. Baker Company’s identifiable assets were

In Exhibit 1, the first category of liabilities is liabilities. As you might expect from the discussion of current assets, current liabilities are claims that become due within a [short / long] time, usually within (how long?).

The first current liability listed in Exhibit 1 is. These are the opposite of Accounts Receivable; that is, they are amounts that [the company owes to its suppliers / are owed to the company by its customers].

In December 2011, Green Company sold a personal computer to Brown Company for $3,000. Brown Company agreed to pay for it within 60 days. On its December 31, 2011, balance sheets, Green Company would report the $3,000 as Accounts [Receivable / Payable] and Brown Company would report the $3,000 as

The next item, titled “Bank Loan Payable,” is reported separately from Accounts Payable because the debt is evidenced by a promissory n __ . Which statement is true?A. Garsden owes the bank $1,250,000.B. Garsden will pay the bank $1,250,000.C. Both A and B are true.

Estimated Tax Liability is the amount owed to the government for taxes. It is shown separately from other liabilities, both because the amount is large and also because the exact amount owed may not be known as of the date of the balance sheet. In Exhibit 1 this amount is shown as $

Two items under Long-term Debt are shown as liabilities. One, labeled “current portion,” amounts to $ ___________. The other, listed under noncurrent liabilities, amounts to $ _______________ Evidently, the total amount of long-term debt is $

The $705,000 is shown separately as a current liability because it is due within ___________ ____________ (how soon?), that is, before December 31, ________________ The remaining $2,876,000 does not become due until after December 31,_________________.

Suppose the $705,000 current portion was paid in 2013, and an additional $500,000 of debt became due in 2014. On the balance sheet as of December 31, 2013, the current portion of long-term debt would be reported as $ , and the noncurrent liability would be reduced to $ .

Recall that equity consists of capital obtained from sources that are not liabilities. The two sources of equity capital for Garsden Company are total - and.

Recall also that the amount of equity that has been earned by the profitable operations of the company and that has been retained in the entity is called .

The amounts of assets, liabilities, and equity of an entity [remain constant / change from day to day]. Therefore, the amounts shown on its balance sheet also [remain constant / change].

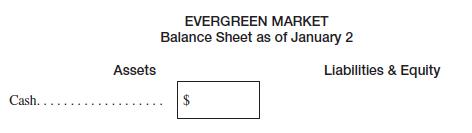

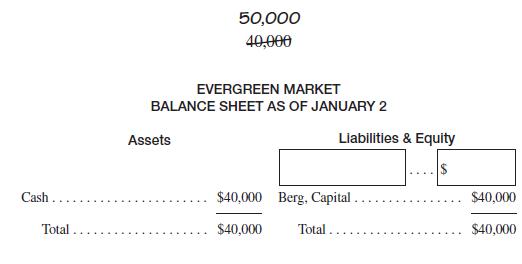

Although a balance sheet must be prepared at the end of each year, it can be prepared more often. In this part, you will be asked to prepare a balance sheet at the end of each day. We shall consider a business named“Evergreen Market,” owned by a proprietor, Henry Berg. The entity here is [Henry

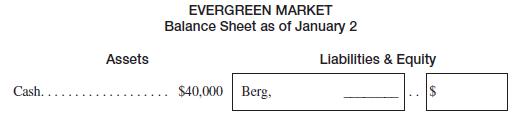

On January 2, Berg started Evergreen Market by opening a bank account in its name and depositing $40,000 of his money in it. In the assets column of the following balance sheet, enter the amount of cash that Evergreen Market owned at the close of business on January 2. EVERGREEN MARKET Balance

Cash is money on hand and money in bank accounts that can be withdrawn at any time. On January 2, if Henry Berg deposited $8,500 in the bank instead of $40,000 and kept $31,500 in the cash register, its cash at the close of business on January 2 would be .

Recall that a name for equity capital is “paid-in capital” in a corporation. Since Evergreen Market is a sole proprietorship, record this in the space below as of the close of business on January 2. EVERGREEN MARKET Balance Sheet as of January 2 Assets Liabilities & Equity Cash. $40,000 Berg, $

This balance sheet tells us how much cash [Evergreen Market /Henry Berg] had on January 2. The separation of Evergreen Market from Henry Berg, the person, is an illustration of the e ____ concept.

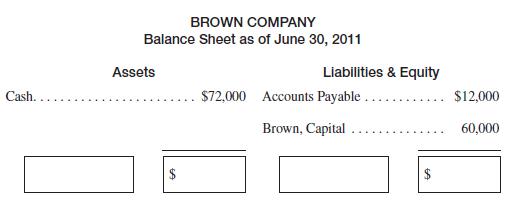

A total should always be given for each side of the balance sheet.Complete the following balance sheet. BROWN COMPANY Balance Sheet as of June 30, 2011 Assets Cash. Liabilities & Equity $72,000 Accounts Payable. $12,000 Brown, Capital 60,000

The totals of the above balance sheet [are equal by coincidence /are necessarily equal].

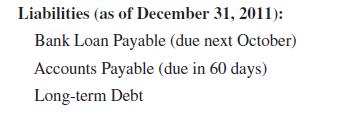

Amounts on a balance sheet are generally listed with the mostcurrent items first. Correct the following list to make it in accord with this practice. Liabilities (as of December 31, 2011): Bank Loan Payable (due next October) Accounts Payable (due in 60 days) Long-term Debt

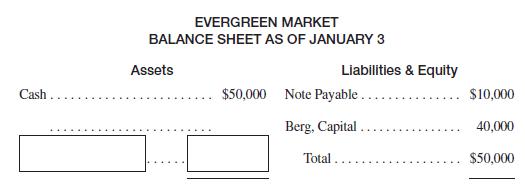

When an entity borrows money, it may sign a written promise to repay.Such a written promise is termed a note . For example, if Business A borrows money from Business B, signing a note, Business A will record a [note receivable / note payable] on its balance sheet, and Business B will record a [note

On January 3, Evergreen Market borrowed $40,000 cash from a bank, giving a note therefor.Change the following January 2 balance sheet so that it reports the financial condition on January 3. In making your changes, cross out any material to be changed and write the corrections like this: Cash..

To record the effect of the event of January 3, you made(how many?) change(s) to the balance sheet (not counting the new totals and the new date) that were necessary. The change(s)[did / did not] affect the equality that had existed between assets and liabilities 1 equity.

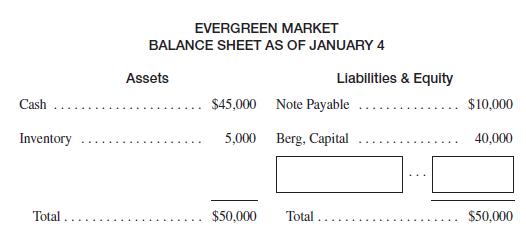

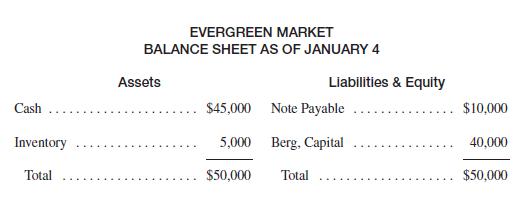

On January 4, Evergreen Market purchased and received inventory costing $5,000, paying cash.Change the following January 3 balance sheet so that it reports the financial condition on January 4. Strike out any items that must be changed, and write the corrections above (or below) them. EVERGREEN

The event of January 4 required two changes on the balance sheet, even though [only one / both] side(s) of the balance sheet was(were) affected.

Each event that is recorded in the accounting records is called a transaction . When Evergreen Market received $40,000 from Henry Berg and deposited it in its bank account, this qualified as a under the definition given earlier because it was “an event that was _______ in the _________ ______ .”

Each transaction you recorded has caused at least(how many?) change(s) on the balance sheet (not counting the changes in the totals and in the date), even when only one side of the balance sheet was affected. This is true of all transactions, and this is why accounting is called a [single / double

Earlier we described the fundamental accounting equation, assets 5 liabilities 1 equity. If we were to record only one aspect of a transaction, this equation [would / would not] continue to describe an equality.

The fundamental accounting equation, which is 5 1 , was also referred to in Part 1 as the d __ -aspect concept.

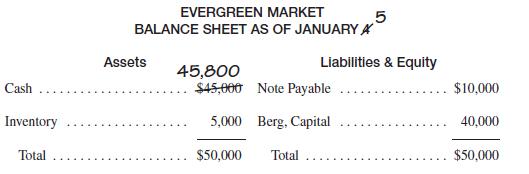

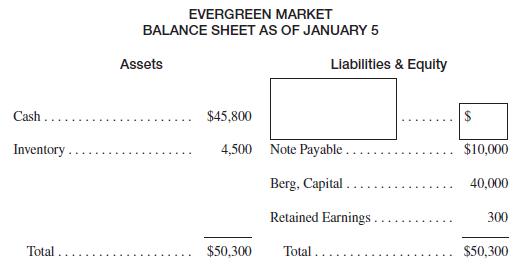

On January 5, Evergreen Market sold merchandise for $800, receiving cash. The merchandise had cost $500.Change the following January 4 balance sheet so that it reports the financial condition on January 5. (If you cannot do this frame, skip to the next without looking at the answer to this one.)

On January 5, Evergreen Market sold merchandise for $800 cash that cost $500.To record this transaction, let’s handle its individual parts separately.Change the date. Then, record only the amount of cash after the receipt of the $800. (Disregard, for the moment, any other changes, including

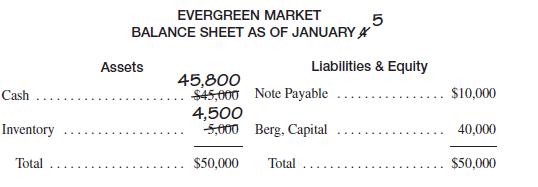

On January 5, Evergreen Market sold merchandise for $800 cash that cost $500. Merchandise that had cost $500 was removed from its inventory.Record the amount of inventory after this transaction. EVERGREEN MARKET BALANCE SHEET AS OF JANUARYA Assets Cash Inventory Total Liabilities & Equity 45,800

On January 5, Evergreen Market sold merchandise for $800 cash that cost $500.Now total the assets as of the close of business on January 5, and show the new total. EVERGREEN MARKET BALANCE SHEET AS OF JANUARY Assets Cash Inventory Total 5 Liabilities & Equity 45,800 $45,000 Note Payable $10,000

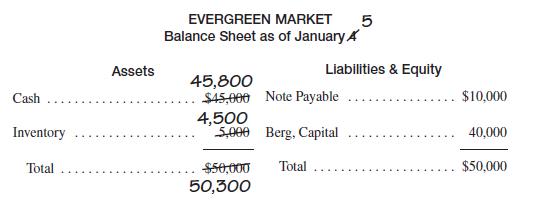

On January 5, Evergreen Market sold merchandise for $800 cash that cost $500.Evidently the transaction of January 5 caused a net [decrease / increase]of $ in the assets of Evergreen Market from what they had been at the close of business on January 4. Assets Cash EVERGREEN MARKET Balance Sheet as

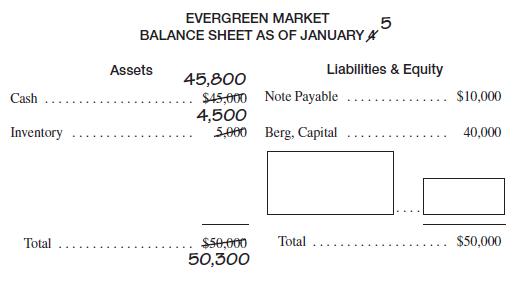

On January 5, Evergreen Market sold merchandise for $800 that cost $500. The assets of the entity increased by $300. The increase was the result of selling merchandise at a profit. As we learned in Part 1 , profitable operations result in an increase in equity, specifically in the item R E .

On January 5, Evergreen Market sold merchandise for $800 that cost $500. Add $300 of Retained Earnings and show the new total of the right-hand side. EVERGREEN MARKET BALANCE SHEET AS OF JANUARY Assets Cash Inventory 45,800 5 Liabilities & Equity $10,000 40,000 $45,000 Note Payable 4,500 5,000

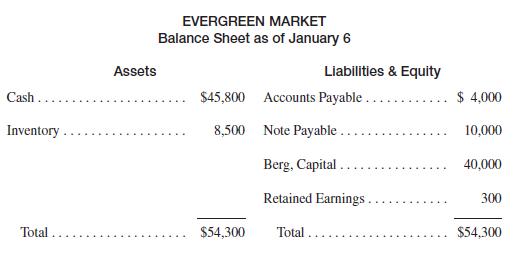

On January 6, Evergreen Market purchased merchandise for $4,000 and added it to its inventory. It agreed to pay the vendor within 30 days.Change the following January 5 balance sheet so that it reports the financial condition on January 6. Recall that an obligation to pay a vendor is called an

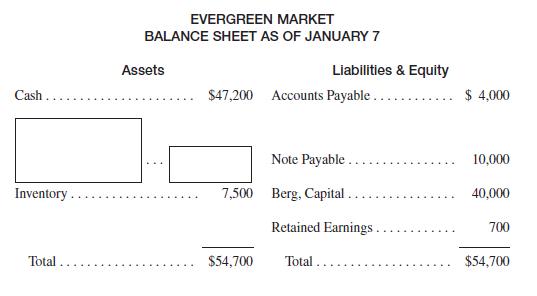

On January 7, merchandise costing $1,000 was sold for $1,400, which was received in cash.Change the following January 6 balance sheet so that it reports the financial condition on January 7. EVERGREEN MARKET Balance Sheet as of January 6 Assets Liabilities & Equity Cash. $45,800 Accounts

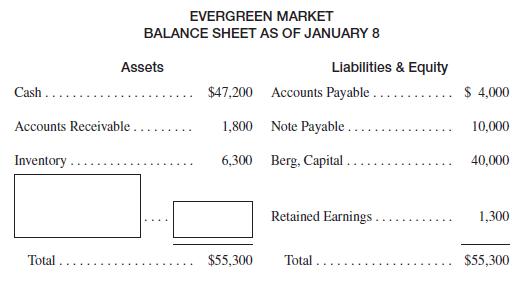

On January 8, merchandise costing $1,200 was sold for $1,800. The customer agreed to pay $1,800 within 30 days. (Recall that when customers buy on credit, the entity has an asset called “Accounts Receivable.” )Change the following January 7 balance sheet so that it reports the financial

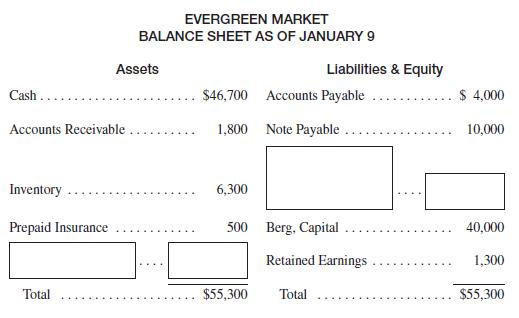

On January 9, Evergreen Market purchased a one-year insurance policy for $500, paying cash. (Recall that the right to insurance protection is an asset. For this asset, use the term “Prepaid Insurance.”)Change the following January 8 balance sheet so that it reports the financial condition on

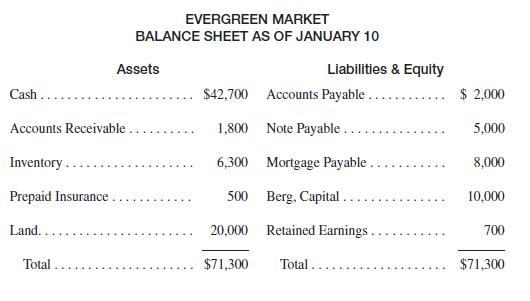

On January 10, Evergreen Market purchased two lots of land of equal size for a total of $20,000. It thereby acquired an asset, land. It paid$4,000 in cash and gave a 10-year mortgage for the balance of $16,000.(Use the term “Mortgage Payable” for the liability.)Change the following January 9

On January 11, Evergreen Market sold one of the two lots of land for $10,000. The buyer paid $2,000 cash and assumed $8,000 of the mortgage; that is, Evergreen Market was no longer responsible for this half of the mortgage payable.Change the following January 10 balance sheet so that it reports the

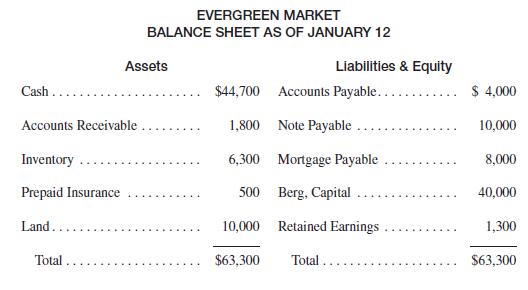

On January 12, Henry Berg received an offer of $50,000 for his equity in Evergreen Market. Although his equity was then only $41,300, he rejected the offer. This means that the store had already acquired goodwill with a market value of $8,700.What changes, if any, should be made in the January 11

On January 13, Berg withdrew for his personal use $300 cash from the Evergreen Market bank account, and he also withdrew merchandise costing $500.Change the following January 12 balance sheet so that it shows the financial condition on January 13. EVERGREEN MARKET BALANCE SHEET AS OF JANUARY 12

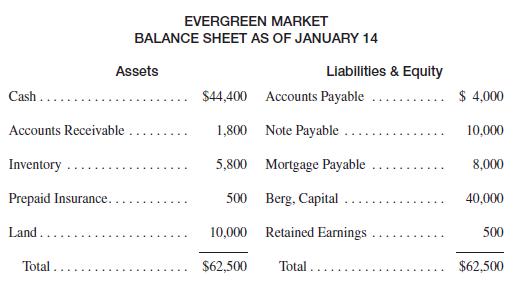

On January 14, Berg learned that the person who purchased the land on January 11 for $10,000 sold it for $15,000. The lot still owned by Evergreen Market was identical in value with this other plot.What changes, if any, should be made in the January 13 balance sheet so that it reports the financial

On January 15, Evergreen Market paid off $4,000 of its bank loan, giving cash (disregard interest).Change the following January 14 balance sheet so that it reports the financial condition on January 15. EVERGREEN MARKET BALANCE SHEET AS OF JANUARY 14 Assets Liabilities & Equity Cash.. Accounts

On January 16, Evergreen Market was changed to a corporation.Henry Berg received 400 shares of common stock in exchange for his$40,500 equity in the business. He immediately sold 100 of these shares for $10,000 cash.What changes, if any, should be made in the January 15 balance sheet so that it

As explained in Part 1, an entity’s equity increases for either of two reasons. One is the receipt of capital from owners. On January 2, Evergreen Market received $40,000 from Henry Berg, its owner. You recorded this as an increase in and an increase in the equity item, Berg, C .

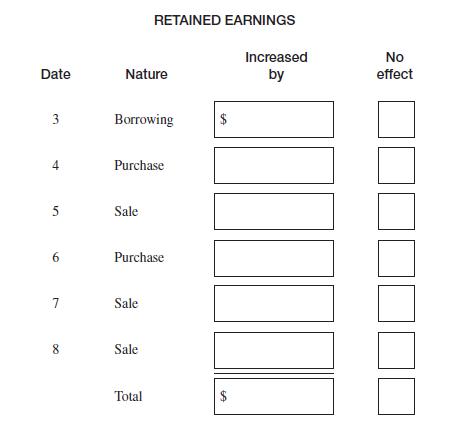

The other source of an increase in equity is the profitable operation of the entity. Transactions that increase profit also increase the equity item R E . Refer to the transactions for January 3 through 8. In the following table, show the dollar amount of the change in Retained Earnings, if any,

As can be seen from the table in Frame 2-65, three of these transactions did not affect Retained Earnings. Borrowing money [does / does not] affect Retained Earnings. The purchase of merchandise [does / does not] affect Retained Earnings. The sale of that merchandise, however,[does / does not]

The amount by which equity increased as a result of operations during a period of time is called the income ( profit ) of that period. You have just calculated that the total increase during the period January 2 through 8 was $ , so Evergreen Market’s i ____ for that period was $ .

The amount of income and how it was earned is usually the most important financial information about a business entity. An accounting report called the income statement explains the income of a period.Note that the income statement is for a [period of time / point in time], in contrast with the

The $1,300 increase in Retained Earnings during the period is reported on the i ____ s _______ . That statement explains how this increase occurred.

To understand how the income statement does this, let’s look at the January 5 transaction for Evergreen Market. On January 5, Evergreen Market sold for $800 cash some merchandise that had cost $500.This caused equity (Retained Earnings) to [increase / decrease] by$ .

Showing 800 - 900

of 1099

1

2

3

4

5

6

7

8

9

10

11

Step by Step Answers