New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

essentials accounting

Essentials Of Accounting 11th International Edition Leslie K. Breitner - Solutions

On line 2 of Exhibit 14 enter the numerator and denominator of the earnings-per-share ratio.

Earnings per share is used in calculating another ratio—the price-earnings ratio. It is obtained by dividing the average market price of the stock by the earnings per share. If the average market price for Chico Company stock during 2009 was $50, then the price-earnings ratio is the ratio of $50

On line 3 of Exhibit 14, enter the numerator and denominator of the price-earnings ratio.

Price-earnings ratios of many companies are published daily in the financial pages of newspapers. Often, the ratio is roughly 9 to 1, but it varies greatly depending on market conditions. If investors think that earnings per share will increase, this ratio could be much higher, such as 15 to 1.

We have focused on return on equity (ROE) as an overall measure of performance. Another useful measure is the return on permanent capital. This shows how well the entity used its capital, without considering how much of its permanent capital came from each of the two sources: d __ and e ____ . This

The return portion of this ratio is not net income. Net income includes a deduction for interest expense, but interest expense is the return on debt capital. Therefore, net income [understates / overstates] the return earned on all permanent capital. Also, income tax expense is often disregarded to

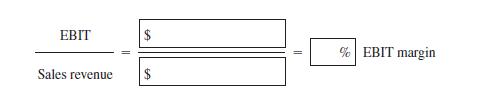

The return used in this calculation is earnings before the deduction of interest and taxes on income. It is abbreviated by the first letters of the words in boldface, or ___ .

As with other income statement numbers, Earnings Before Interest and Taxes (EBIT) is expressed as the percentage of sales revenue.This gives the EBIT margin. Calculate it for Chico Company.Enter the numerator and denominator of the EBIT margin ratio on Line 7 of Exhibit 14. EBIT Sales revenue EBIT

The permanent capital as of December 31, 2009, is the debt capital(i.e., noncurrent liabilities) of $ ,000 plus the equity capital of $ ,000, for a total of $ ,000. The return on permanent capital is found by dividing EBIT by this total. Calculate the return on permanent capital. $ % $

Copy the numerator and denominator of the return on permanent capital on Line 4 of Exhibit 14.

Another ratio shows how much sales revenue was generated by each dollar of permanent capital. This ratio is called the capital turnover ratio. Calculate it for Chico Company.Copy the numerator and denominator of this ratio on Line 13 of Exhibit 14. Sales revenue $ Capital turnover times Permanent

American manufacturing companies have a capital turnover ratio of roughly two times on average. A company that has a large capital investment in relation to its sales revenue is called a capital-intensive company. A capital-intensive company, such as a steel-manufacturing company or a public

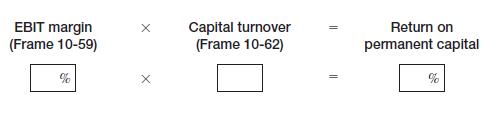

Another way of finding the return on permanent capital is to multiply the EBIT margin ratio by the capital turnover. Calculate this relationship. EBIT margin (Frame 10-59) % Capital turnover (Frame 10-62) Return on permanent capital %

This formula suggests two fundamental ways in which the profitability of a business can be improved:1. [Increase / Decrease] the EBIT margin ratio.2. [Increase / Decrease] the capital turnover.

In the previous analysis, we used ratios because absolute dollar amounts are [rarely / often] useful in understanding what has happened in a business.

Also, we focused on both income and the capital used in earning that income. Focusing on just one of these elements can be [just as good /misleading].

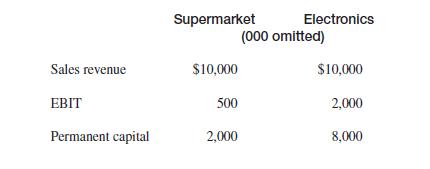

For example, consider the following results for a supermarket and an electronics store, each with $10 million of sales revenue.The EBIT margin for the supermarket is onlyand for the electronics store it isThe ratio for the electronics store is much [lower / higher]. Supermarket Electronics (000

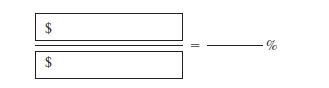

However, the electronics store has more expensive fixtures, a larger inventory, and a lower inventory turnover than the supermarket, so its capital turnover is lower. Calculate the capital turnover of each. Sales Permanent Capital = Capital turnover times Supermarket Electronics store $. times

The return on permanent capital is the same in both companies, as you can see for yourself in the following calculation. Supermarket EBIT margin X Capital turnover = Return on permanent capital 0. times % times % Electronics store 0.

Ability to meet current obligations is called liquidity. The ratio of current assets to current liabilities, called the ratio, is a widely used measure of liquidity.

Solvency measures the entity’s ability to meet all its obligations when they come due. If a high proportion of permanent capital is obtained from debt, rather than from equity, this increases the danger of insolvency.The proportion of debt is indicated by the d __ r ___ .DUPONT ANALYSIS

As you learned earlier, the return on e ____ is an important measure of an organization’s success. One of the primary uses of ratio analysis is to compare organizations. But two organizations with the same R _ may not really be the same.

Do you remember the ROE formula?In the next frame we will see another way to arrive at the ROE. It is called the DuPont Identity or DuPont Analysis, developed by the DuPont Company many years ago.

In Frame 10-26 we looked at the profit margin. Recall that the profit margin is:____________ ________________ ______________________________ _____________ ________________ The profit margin helps to measure operating efficiency.

We might also be interested in other efficiencies, such as the use of a company’s assets. The asset turnover ratio measures how effectively a company uses assets to generate sales revenues. Thus, the asset turnover ratio is:S ___ R _____ ______________ A ____

Both the profit margin and the asset turnover ratios are efficiency ratios. They measure o _______ efficiency and a ___ u _ efficiency.

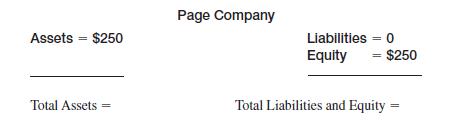

The financial leverage ratio is a measure of how much debt(leverage) a company has relative to the rest of the balance sheet.Consider the following example. Page Company Assets = $250 Liabilities = 0 Equity = $250 Total Assets Total Liabilities and Equity

The leverage ratio is Assets 4 Equity. What is the leverage ratio for Page Company?______________ _______________________ =________________

In a company with no liabilities (no debt), the leverage ratio will always be 1 because Total a ____ is equal to Total l _________ and E ____ .

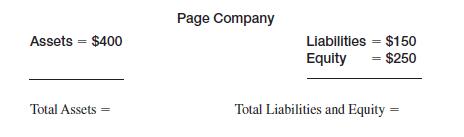

Now consider that Page Company has taken out a loan. Here is its new balance sheet. Page Company Assets = $400 Total Assets = Liabilities = $150 Equity $250 = Total Liabilities and Equity =

The leverage ratio is now:______________ _______________________ =________________

Evidently, as an organization takes on debt its leverage ratio[increases / decreases]. With zero debt the leverage ratio can never be lower than . This means that even a small amount of debt will make the leverage ratio greater than .

It is possible for a company with low efficiency ratios to increase its ROE by taking on debt. This works by breaking down the ROE into three components and multiplying the impact of debt on ROE. Thus, the leverage ratio is sometimes called the equity m _______ r.

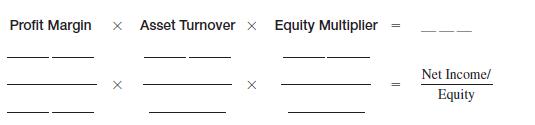

The DuPont system of ratios allows us to separate the components of the return on e ____ . Fill in the blanks below to show how this works and enter the numerator and denominator for each on lines 14–16 of Exhibit 14. Profit Margin Asset Turnover Equity Multiplier = Net Income/ Equity

It is easy to see that two companies may achieve the same __ in very different ways. Some ways are more attractive to investors for different reasons. A company with a lot of debt, for example, is[riskier than / not as risky as] a company with little or no debt.

A highly leveraged company is one with high levels of d __ .Generally speaking, such a company poses more r __ to investors because of the potential to go bankrupt if it cannot pay back the debt.

Sam Company has the following financial data:Sales Revenues $75,000 Net Income $10,000 Assets $50,000 Equity $40,000 Use the three components to arrive at ROE.Profit Margin 3 Asset Turnover 3 Equity Multiplier 5 ROE

What if Sam Company had no debt? The ROE would then be:

Now consider Black Company and Blue Company. Calculate the ROE for each company.Black Company Blue Company Profit margin 5 30% Profit margin 5 3%Asset turnover 5 0.45 Asset turnover 5 4.5 Leverage ratio 5 2.0 Leverage ratio 5 2.0

Black Company and Blue Company have [exactly the same / very different] profit margin and asset turnover ratios. They have [exactly the same / very different] ROEs.

Black Company has a [higher / lower] profit margin than Blue Company. Blue Company has a [higher / lower] asset turnover than Black Company. But they have the same __ .

You can see that there are (how many?) components that give rise to the calculation of ROE?

Without the use of debt (the equity multiplier or the leverage ratio), Black Company and Blue Company’s ROE would be:Profit Margin 3 Asset Turnover 5

We can see that by using leverage, a company can generate a higher return on equity, but with greater risk for the investor. This suggests that there is a tradeoff between r and r .

In summary, the DuPont system of ratios breaks the __ down into (how many?) parts.p_______________ m_______________ a_______________ t_______________ f_______________ l_______________

Profit margin measures efficiency.Asset turnover measures efficiency.The equity multiplier measures .Together these are the components of __ .

Financial analysts form their opinions about a company partly by studying ratios such as those we have presented. They also study the details of the financial statements, including the notes that accompany these statements. They obtain additional information by conversations and visits because they

Information found in the financial statements has limitations.Sometimes investors want to dig deeper to evaluate the quality of a company’s net income (earnings) or other reported financial data. A q _____ of e ______ analysis typically allows an analyst to evaluate performance in a more

Typically, ratio analysis involves the use of accounting data as reported. Since accountants have choices when preparing financial statements, the data presented could look different if different c _____ had been made. To evaluate the q _____ of a company’s earnings, analysts often make

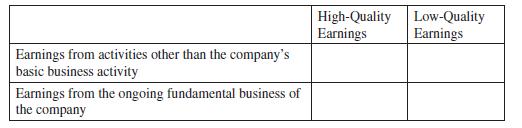

Golden Company’s net income might be exactly the same as Silver Company’s net income. Golden Company’s revenues and expenses might all come from regular and recurring business activities. Silver Company’s revenues might come partially from a one-time event not expected to happen again in

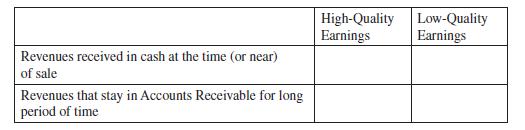

Evergreen Company turns its revenues into cash inflows within 30 days on a regular basis. River Company allows its customers to buy on credit and they typically don’t collect these accounts receivable for many months. The current ratios of both companies might be identical.Investors are likely to

Analysts and investors use indicators other than the performance ratios described earlier to evaluate the quality of a company’s reported earnings. Not all analysts define q _____ of earnings in the same way. Therefore a quality of earnings analysis is [an exact science / a very subjective

You have learned that not all revenues are received in c __ at the time of a sale. You have also learned that not all expenses are paid out in c __ at the time they are incurred. Therefore, net income [is /is not] necessarily a good indicator of c __ earnings.

Investors often equate “real earnings” with those that generate cash from year to year. For these investors r __ e _ _ _ _ _ _ may be more important than n _ i ____ when determining profitability.

You have also learned that the statement of cash flows indicates cash flow from o _______ activities, from i _______ activities, and from f _______ activities. Investors think of real earnings as normal, recurring operating activities that generate ___ . Obviously the statement of c __ f ___ is

Since investors and analysts look for different things in their analyses, there are no commonly agreed-upon standards for a q _____ of e ______ analysis. Some of the ratios you calculated earlier may be part of a quality of earnings analysis.

Lenders want to know if cash flows are adequate to pay i t on debt and to repay the p when it becomes due.

When a company is in financial difficulty, it may pay [more / less]attention to its cash flow statement than to its income statement. It pays bills with cash—not net income.

A forecast of cash flows helps management and other users of financial information to estimate future needs for cash. For example, when a company is growing, the increase in its accounts receivables, inventory, and fixed assets may require [more / less] cash. Therefore, although growth may result

Some of the characteristics of companies with high quality of earnings are:A. Consistent and conservative accounting p ______ B. Net income (earnings) from recurring rather than one-time e ____ C. Sales revenues that result in cash i _____ sooner rather than later D. Debt that is appropriate for

The cash flow statement shows that although net income was$ ,000 in 2012, Cash increased by only $ ,000. Operating activities generated $ ,000 in cash; $ ,000 of this cash was used to pay dividends. The remaining additional cash inflow was used to acquire new PPE. The cost of the new assets was$

To reconcile the statement of cash flows with the balance sheet, there is a section at the bottom. The net increase or decrease in c must equal the d ______ ce between beginning and ending cash. Enter these amounts at the bottom of Exhibit 11.

Calculate the increase in cash by summing the three categories in Exhibit 11, and enter this total. Note that the $ ,000 net increase in cash [equals / does not equal] the change in the Cash balance as reported on the two balance sheets of Chico Company.

An investing activity [is / is not] always a cash outflow, and a financing activity [is / is not] always a cash inflow.

Use the exhibits below to indicate whether you think the earnings would be considered high or low.A. Consistent and conservative accounting policies:B. Net income (earnings) from recurring activities:C. Sales resulting in timely cash inflows:D. Appropriate debt and capital structure levels:E.

Dividends paid are sometimes classified as a financing activity.Exhibit 10 shows that Chico Company paid $ ,000 of dividends in 2012. Enter this amount in Exhibit 11. Then enter the total of the financing activities in Exhibit 11. Note that although it is common to find dividend activity in the

Issuance of additional shares of a company’s stock is also a financing activity. Exhibit 10 shows that Chico Company’s Paid-in Capital was$ at the beginning of 2012 and $ at the end of 2012. Evidently, the company [did / did not] issue additional stock in 2012.

You learned that financial statements tell only a part of the story of a company. Red flags or warnings about a company’s financial condition that might not show in a typical ratio analysis might be detected in a q _____ o e ______ analysis. Warning signals are often identified early in the

The borrowings reported in the financing section are both shortterm and long-term borrowings. Whereas short-term borrowings often appear as current liabilities, changes in them are usually reported in the section on Cash Flow from F A .

As shown in Exhibit 10, Chico Company had a liability, mortgage bonds. The amount was $ ,000 at the beginning of 2012 and$ ,000 at the end of 2012. The increase of $ ,000 showed that Chico Company issued bonds of this amount. This was a(n)[investing / financing] activity. It represented a(n)

Companies may also obtain cash by issuing debt securities, such as bonds. Issuing debt securities is a(n) . . . [investing / financing] activity.

Similarly, if the PPE account decreased, representing the sale of plant assets, there would have been an [inflow / outflow] of cash.Thus, companies may cash to purchase property, plant, and equipment and they may sell property, plant, and equipment to get.

As shown in Exhibit 10, Chico Company had PPE at the beginning of 2012 that had cost $ ,000. It had $ ,000 of PPE at the end of 2012. The increase of $ ,000 was a(n)[investing / financing] activity in 2012. Enter this amount in Exhibit 11.(The parentheses indicate that this was a cash outflow.)

Quality-related red flags should not be ignored. They may suggest potential problems not indicated by a more typical r ___ analysis. This means that investors and analysts must understand fully the accounting practices as well as the nature and behavior of financial statement items to be able to

When a company invests in additional property or plant, the amount involved is a cash [inflow to / outflow from] the company.

Exhibit 11 shows that in addition to cash flow from operating activities, there are two other categories on a statement of cash flows: cash flow from activities and cash flow from activities.

If there was depreciation expense, cash flow from operations will be [lower than / the same as / higher than] net income.

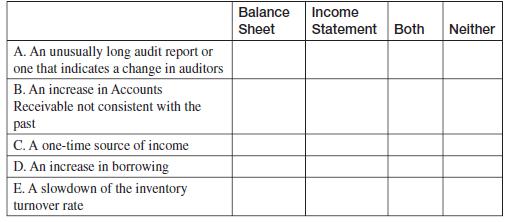

Below are some typical quality-related red flags. Indicate for each whether you would look at the balance sheet, income statement, neither, or both to detect the red flag. A. An unusually long audit report or one that indicates a change in auditors B. An increase in Accounts Receivable not

If the net amount of the working capital accounts (excluding cash)increased, cash flow from operations will be [lower than / higher than]net income.

Sarbanes-Oxley is a law passed in ___ to strengthen corporate governance and restore investor confidence. The law is complex.It specifies corporate responsibilities and criminal penalties for noncompliance with the standards. Company management and boards of directors must now be familiar with the

If the net amount of the working capital accounts (excluding cash)decreased, cash flow from operations will be [lower than / higher than]net income.

If the total amount of working capital (excluding cash) did not change, and if there are no noncash expenses, such as depreciation, cash flow from operations will be [lower than / the same as / higher than] net income.

As a shortcut, therefore, some analysts arrive at the operating cash flow simply by adding Depreciation Expense to Net Income. They disregard changes in the working capital accounts on the assumption that these changes net out to a minor amount. This shortcut may give the impression that

The Sarbanes-Oxley Act was an enormous change to federal securities laws in the United States. It came in response to the collapse of Enron (and other companies) and the related accounting scandal by Enron’s auditor, Arthur Andersen. Public companies are now required to submit annual reports of

Note that the $ ,000 adjustment for Depreciation Expense is [larger than / smaller than / about the same as] the net amount of all the working capital account adjustments. This is the case in some companies, especially manufacturing companies, that have relatively large amounts of fixed assets.

Complete the “Cash Flow from Operating Activities” section of Exhibit 11. (Remember that numbers in parentheses are subtracted.) The cash flow from operating activities was $ ,000.

An increase in current liabilities means that [more / less] cash was freed up. The cash not paid to suppliers is still in the C account.This is why, in times when cash is low, a business tries to keep current liabilities as [high / low] as feasible.

In summary, an increase in current assets means that [more / less]of the cash inflow was tied up in accounts receivable, inventory, and/or other current assets, with a corresponding [increase / decrease] in Cash.This is why, in times when cash is low, a business tries to keep the other current

All companies should be concerned about governance (authority and control). Since SOX generally affects only publicly traded companies, it is about corporate g ________ . SOX affects U.S. companies as well as foreign companies operating in the U ____ S ____ .

Exhibit 10 shows that Accrued Wages [increased / decreased]by $ ,000. Therefore, net income is adjusted to a cash basis by[adding / subtracting] this amount. Enter this change in Exhibit 11.

Exhibit 10 shows that Accounts Payable [increased / decreased] by$ ,000. Therefore, net income is adjusted to a cash basis by [adding /subtracting] this amount. Enter this change in Exhibit 11.

The Sarbanes-Oxley Act is detailed and technical. Most issues related to compliance are well beyond the introductory nature of this book. However, there are some general areas related to SOX that we will examine. Since SOX is law it is critical that companies know how to conform or make their

Changes in current liabilities have the opposite effect on Cash than changes in current assets. An increase in a current liability requires that the net income amount be adjusted to a cash basis by [adding to it / subtracting from it]. A decrease in a current liability requires that the adjustment

This makes sense because if everything else remains the same, a decrease in Accounts Receivable means the company received more c __ payments during the accounting period compared to last period’s Accounts Receivable.

This follows from the fundamental accounting equation:5 1 . To keep this equation in balance, a decrease in Accounts Receivable would necessarily mean an equal [increase / decrease] in Cash, if these were the only two accounts involved.

An easy way to remember whether the impact on Cash (and hence the adjustment to net income) is an addition or a subtraction is to pretend that only that one account and Cash exist, at least for a moment in time.For example, if Cash and Accounts Receivable were the only accounts, a decrease in

The costs of noncompliance may be great. They may include both civil and criminal penalties. Since managers concerned with internal operations are not generally experts in SOX compliance, they often hire e ______ consultants to help identify areas of potential noncompliance. Evidently those who are

To summarize, we must analyze changes in the balance sheet accounts to determine their impact on Cash. We are interested in the w c accounts to prepare the “cash flows from o _______ activities” section of the statement of cash flows.

If the balance in a working capital account is unchanged, the inflow to Cash [is / is not] the same amount as revenue, and an adjustment[is / is not] necessary.

As shown in Exhibit 10, the beginning balance in Inventory was$ ,000, and the ending balance was $ ,000, which shows that this asset [increased / decreased] by $ ,000 during the year.This change had the opposite effect on Cash than the change in Accounts Receivable. Therefore, we must [add to /

Showing 400 - 500

of 1099

1

2

3

4

5

6

7

8

9

10

11

Step by Step Answers