New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

essentials accounting

Essentials Of Accounting 11th International Edition Leslie K. Breitner - Solutions

Recall that many intangible assets are depreciated/amortized.Under both sets of standards, intangible assets with indefinite lives are not subject to a __________ . Instead, intangible assets are tested for impairment annually.

Recall that noncurrent assets are recorded at their original cost.U.S. GAAP prohibits revaluation of property, plant, and equipment based on market prices. IFRS allows companies to r _____ their property, plant, and equipment.

IFRS requires reviewing estimates of residual v ___ and d _________ n methods yearly, whereas U.S. GAAP requires review only when an event indicates that estimates or depreciation methods are no longer appropriate. This concept goes beyond the introductory nature of our treatment of this material.

U.S. GAAP and IFRS record property, plant, and equipment(PP&E) initially at c __ , which includes any expenditure that is directly related to purchasing the asset and preparing it for use.

When inventory loses value, it is considered impaired and its value must be reduced by the amount of the i _______ t.Under U.S. GAAP, any write-down of impaired or obsolete inventory cannot be reversed if an increase in value occurs. Under IFRS, impairment losses may be r ______ up to the amount of

The market cost of inventory is usually the current replacement cost. U.S. GAAP measures inventory at the lower of cost or m ____ .

The net realizable value of inventory is that amount at which it is expected to sell, less the expected costs to sell the inventory. IFRS measures inventory at either the lower of original cost or n _ r ________ v ___ (NRV).

With IFRS there are some constraints with regard to the use of inventory valuation methods. For example, the use of L __ is prohibited by IFRS. Companies can either account for inventory using FIFO or weighted average.

U.S. GAAP has very detailed guidance on revenue r _________ specific to different types of industry and contract. IFRS apparently [does / does not] have this.

There are various ways to record revenue as it is earned for longer term contracts like a construction project. Under both IFRS and U.S.GAAP, the percentage of completion method to record revenue is used when certain criteria are met. U.S. GAAP allows using the completed c ______ method, which

IFRS recognizes revenue on the same basis as U.S. GAAP, which is when the risks and rewards of ownership have been transferred from the buyer to the seller. At this moment, the seller no longer owns or controls what has been sold. However, the specific criteria that determine whether r ___ and r

The study of accounting is not limited to learning about how to structure f _______ s _______ s.Students must learn about many aspects of g ____ reporting.

There are many areas where GAAP and IFRS differ. For IFRS to become the accepted practice in the United States, the two systems for reporting must converge. Such c ________ e may not fully happen for some time.

Obviously, this is an area of [similarity / difference] between IFRS and GAAP.

The standard-setting board that defines the IFRS wants to use fair value as the measurement basis. It is because the board feels that f __ v ___ measurement meets the characteristics described in Frame 12.35.

Recall that we introduced the qualitative characteristics of the IFRS earlier. They are:u _______________y r_______________ e r_______________ y c_______________ y

According to GAAP, most assets are reported as an objective measure, which is ___ .

Because fair values are difficult to estimate, they are [objective /subjective], whereas costs are [objective / subjective].

So, if reliable information is available, the amount of an asset is measured at its fair value. Otherwise, the measurement is based on its ___ .

Because entities usually don’t know the fair value of their assets, they report them at c __ .

You learned in Part 1 that the fair value of most assets is known on the date the asset was acquired because the buyer and the seller agreed on the amount. You learned that if Garsden Company purchased a plot of land in 2002 for $100,000, this land would have been reported on its December 31, 2002,

The asset-measurement concept is: If r _____ e information is available, an asset is measured at its fair value.

Let’s use an example to illustrate a potential difference between GAAP and IFRS. Recall from Part 1 the asset-measurement concept. The name for what an asset is “worth” is its f __ v ___ .

Some of the changes necessary for adoption of the IFRS are minimal, whereas others will take a long time. Evidently, there are s _________ s as well as d ________ s between GAAP and IFRS. We have already mentioned some of these.

Bookkeeping uses fairly straightforward rules. Using guiding principles rather than rules calls for judgment. Evidently, today's student[can get by just learning the rules / must learn to think more broadly]about financial accounting.

Global f _______ reporting should allow us to analyze and c _____ financial statements from different countries. Financial reporting is not only about bookkeeping.

In Part 10 you learned about financial statement analysis.Obviously, there's more to accounting than bookkeeping. Financialstatement analysis allows us to interpret f _______ s _______ s and give meaning to them.

Earlier in the book you learned about T-accounts, the doubleentry system, ledgers, and journal entries. Such tools help us to keep the financial records, or books, of the entity. We usually refer to these activities as book ___ ing.

Global financial reporting covers more material than just focusing on the United States. Therefore, students must now learn the basics of both the U.S. system as well as IFRS. Global financial reporting is also concerned with global economic concepts. Thus, students must study e ______ s as well as

If the U.S. systems are more ____ -based and the IFRS is more _________ -based, it will not be easy for all countries to agree on the common set of standards.

G ____ financial reporting cannot be consistent around the world without a single set of standards. IFRS attempts to bring together many different sets of standards into a common set of standards.

Global financial reporting would help to make the qualitative characteristics of comparability [easier / nearly impossible]. Users of financial statements often need to compare the financial information across many organizations.

When we think of how many countries have financialreporting guidelines, we are thinking of countries around the world, or the g ___ . Sometimes we refer to international reporting as g ____ reporting.

The IFRS framework describes some qualitative characteristics of financial statements (understandability, relevance, reliability, and comparability). Obviously, an important issue is the ability to c ____ e financial statements of organizations from different countries. Needless to say, it will be

The underlying assumptions in IFRS are the going-concern and accrual-basis assumptions. Thus, there are [similarities / no connections]to U.S. Generally Accepted Accounting Principles.

In Part 4 you learned that transactions are recognized when they occur rather than when cash is received or paid. (See Frames 4-6 through 4-17.) This is called a ____ l accounting.

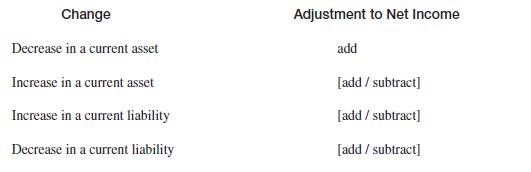

Users of financial statements need to understand these relationships, but there is no need to memorize them. The cash flow statement gives the net effect of each of the four types of adjustments in working capital items. Complete the following summary of them: Change Decrease in a current asset

In Part 1 you learned that financial statements are prepared assuming the entity will continue operations in the foreseeable future. (See Frames 1-40 through 1-43.) This concept is called the g ___ -c _____ concept.

The underlying assumptions used in the IFRS are similar to what you have already learned. One important difference is that U.S. accounting is ____ -based whereas the IFRS is _________ -based.

The overall framework of IFRS states that the objective of financial statements should help users to make economic decisions through understanding the f _______ status of an entity.

The U.S. standards are rules-based. But the IFRS are based on a set of guiding principles. We can conclude that the IFRS are p _______ s-based.

IFRS stands for I ___________ F _ _ _ _ _ _ _ R _ _ _ _ _ _ _ S _______ . These standards are intended to make it easier for a wide range of users to interpret financial statements.

Many countries have joined together to form a set of accounting standards to make it easier to read and compare f _______ s _______ s.

If every country has its own set of guidelines, this would make it [easy / incredibly difficult] to understand the financial statements of other countries.

Since we follow the guidelines of U.S. GAAP, [it seems logical /it would not be possible] that other countries have their own versions of ___ .

Although the complexity of GAAP is more advanced than this text, it is useful to know that such guiding p _______ s exist.

There is a standard set of guiding principles in the United States.These guidelines are called G enerally A ccepted A ccounting P rinciples.We usually shorten this to ___ . GAAP includes the rules, in the form of standards, that accountants follow when they prepare financial statements.

In almost anything we do, if there is a set of rules, it is clear what we need to do. If there are no formal rules, we must choose what to do based on guidelines or practice. You have learned that some accounting rules may depend on how the accountant chooses to apply the rules(FIFO/LIFO

In this book you have learned many rules that help to define the way financial statements are prepared. This suggests that U.S. accounting is primarily a r ___ -based set of standards.

One limitation is suggested by the word “financial”; that is, financial statements report only events that can be measured in m ___ ary amounts.

A second limitation is that financial statements are historical; that is, they report only events that [have happened / will happen], whereas we are also interested in estimating events that [have happened / will happen]. The fact that an entity earned $1 million last year [definitely predicts / is

Third, the balance sheet does not show the [cost / fair value]of nonmonetary assets. In accordance with the a ___ -m _________ concept, plant assets are reported at their [unexpired cost / fair value].Also, depreciation is a write-off of [cost / fair value]. It is not an indication of changes in

Fourth, the accountant and management have some latitude in choosing among alternative ways of recording an event in the accounts.An example of flexibility in accounting is that in determining inventory values and cost of sales, the entity may use the L __ , F __ , or average cost methods. Such

Fifth, many accounting amounts are estimates. In calculating the depreciation expense of a plant asset, for example, one must estimate its s _____ l __ and its r ______ v ___ .

All large companies and many small ones have their accounting records examined by independent, certified public accountants. This process is called auditing, and the independent accountants are called ___ tors.

After completing their examination, the ______ s write a report giving their opinion. This o _____ is reproduced in the company’s annual report. A typical opinion is shown in Exhibit 12.

The opinion says that the auditors [prepared / audited] the financial statements and that these statements are the responsibility of [the auditors / management].

The opinion further states that the financial statements [accurately /fairly] present the financial results.

In the last paragraph of the opinion, the auditors assure the reader that the statements were prepared in conformity with g a a p .

Equity investors (i.e., shareholders) invest money in a business in order to earn a profit, or return, on that equity. Thus, from the viewpoint of the shareholders, the best overall measure of the entity’s performance is the r ____ that was earned on the entity’s e ____ .(This is abbreviated

The accounting name for the profit or return earned in a year is n _ i ____ .Return on equity is the percentage obtained by dividing n _ i ____ by e ____ .

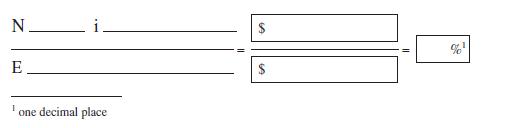

In 2009, Chico Company had net income of $30,000, and its equity on December 31, 2009, was $130,000. Calculate its ROE for 2009. N. E one decimal place

In order to judge how well Chico Company performed, its 23.1% ROE must be compared with something. If in 2008 Chico Company had an ROE of 20%, we can say that its performance in 2009 was [better / worse] than in 2008. This is the historical basis of comparison.

If in 2009 another company had an ROE of 25%, Chico’s ROE was [better / worse] than the other company’s. Or if in 2009 the average ROE of companies in the same industry as Chico was 25%, Chico’s ROE was [better / worse] than the industry average. This is the external basis of comparison. If

Finally, if from our experience we judge that a company like Chico should have earned a ROE of 20% in 2009, we conclude that Chico’s ROE was [better / worse] than this judgmental standard.

Most comparisons are made in one or more of the three ways described above. Give the meaning of each.1. Historical: comparing the entity with ______________________________________________________________ 2. External: comparing the entity with

Chico Company’s net income in 2009 was $30,000. Paul Company’s net income in 2009 was $60,000. From this information we cannot tell which company performed better. Why not?

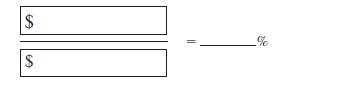

Paul Company’s equity was $1,000,000. Its net income in 2009 was $60,000. Its ROE was thereforeChico Company with an ROE of 23.1% performed [better / worse] than Paul Company. $ $ %

The comparison of Chico Company’s dollar amount of net income with Paul’s dollar amount [did / did not] provide useful information.The comparison of their ratios or percentages was [useful /not useful]. Useful comparisons involve r s or p s.

Ratios help explain the factors that influenced return on equity.We have already described the return on equity ratio, which is:Copy the numerator and denominator of this ratio on Line 1 of Exhibit 14. (numerator) Net income (denominator) Equity Return on Equity

One factor that affects net income is gross margin. In an earlier part, you calculated the gross margin percentage. Calculate it for Chico Company. Gross Margin $ Sales revenue 69 % gross margin

On Line 5 of Exhibit 14, write the name of the numerator and of the denominator of the gross margin percentage.

Gross margin percentages vary widely. A profitable supermarket may have a gross margin of only 15 percent. Many manufacturing companies can have gross margins of about 35 percent. Compared with these numbers, the gross margin of Chico Company is [low / high].

A high gross margin does not necessarily lead to a high net income.Net income is what remains after expenses have been deducted from the gross margin, and the higher the expenses, the [higher / lower]the net income.

The profit margin percentage is a useful number for analyzing net income. You calculated it in an earlier part. Calculate it for Chico Company. Net income % profit margin Sales revenue $

Copy the numerator and denominator of the profit margin percentage on Line 6 of Exhibit 14.

Statistics on the average profit margin percentage in various industries are published and can be used by Chico Company as a basis for comparison. Statistics on the average dollar amount of net income are not published. Such statistics [are / are not] useful because sheer size is not a good

The bottom section of the diagram in Exhibit 13 shows the main components of Chico Company’s capital. The information is taken from its [income statement / balance sheet]. We shall examine ratios useful in understanding these components.

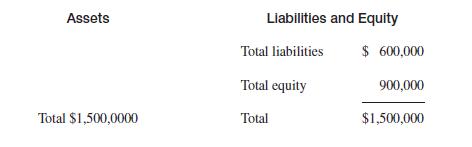

As background for this analysis, let’s examine some relationships in Stimson Company, which has the following condensed balance sheet:If net income was $81,000, Stimson Company’s return on equity (ROE)was Net income 4 Equity, or %. Assets Liabilities and Equity $ 600,000 Total liabilities Total

If Stimson Company could reduce its equity to $720,000, while still maintaining its net income of $81,000, its ROE would become%. Evidently, with net income held constant, Stimson Company can increase its ROE by [increasing / decreasing] its equity.

Since total assets always equal liabilities plus equity, equity can be decreased only if (1) assets are [increased / decreased], (2) liabilities are [increased / decreased], or (3) there is some combination of these two types of changes.

For example, Stimson Company’s equity would be decreased by$180,000 (to $720,000) if assets were decreased by $40,000 (to $960,000)and liabilities were [increased / decreased] by $(to $ ). If equity was $720,000 and net income was$81,000, ROE would be $ %

In earlier parts, two ratios for measuring current assets were described.One related to accounts receivable and was called the days’ sales uncollected. It shows how many days of sales revenue are tied up in accounts receivable.Calculate days’ sales uncollected for Chico Company. Accounts

Copy the numerator and the denominator of the days’ sales uncollected on Line 8 of Exhibit 14.

The amount of capital tied up in inventory can be examined by calculating the inventory turnover ratio. Since inventory is recorded at cost, this ratio is calculated in relation to cost of sales, rather than to sales revenue.Calculate the inventory turnover ratio for Chico Company (refer to Exhibit

Copy the numerator and the denominator of the inventory turnover ratio on Line 9 of Exhibit 14.

If Chico Company had maintained an inventory of $90,000 to support $260,000 cost of sales, its inventory turnover would have been(how many?) times, rather than 4.33 times. With this change, its ROE would have been [higher / lower] than the 23.1% shown in Exhibit 13.

The current ratio is another way of examining the current section of the balance sheet. In an earlier part we pointed out that if the ratio of current assets to current liabilities is too low, the company might not be able to pay its bills. However, if the current ratio is too high, the company

Calculate the current ratio for Chico Company.

Copy the numerator and the denominator of the current ratio on Line 10 of Exhibit 14.

If Chico Company decreased its current ratio to 1.5 by increasing its current liabilities, this would [increase / decrease] its ROE. However, such a low current ratio would [increase / decrease] the possibility that Chico would be unable to pay its current liabilities when they come due.

A variation of the current ratio is the quick ratio (also called the acid-test ratio ). In this ratio, inventory is often excluded from the current assets, and the remainder is divided by current liabilities. This is a more stringent measure of immediate bill-paying ability than the current

Copy the numerator and the denominator of the quick ratio on Line 11 of Exhibit 14.

The final ratio we will use in examining capitalization is the debt ratio . As explained in Part 8 , this is the ratio of debt capital to total permanent capital. Noncurrent liabilities are d __ capital, and noncurrent liabilities plus equity are t ___ p _______ capital. Calculate the debt ratio

Copy the numerator and denominator of the debt ratio on Line 12 of Exhibit 14.

The larger the proportion of permanent capital that is obtained from debt, the smaller is the amount of equity capital that is needed. If Chico had obtained $85,000 of its $170,000 permanent capital from debt, its debt ratio would have been %, and its ROE would have been[higher / lower] than the

A high debt ratio results in a [more / less] risky capital structure than does a low debt ratio.

In several of the calculations above, we used balance sheet amounts taken from the ending balance sheet. For some purposes, it is more informative to use an average of beginning and ending balance sheet amounts.Chico Company had $130,000 of equity at the end of 2009. If it had$116,000 at the

Another measure of performance is earnings per share. As the name suggests, the ratio is simply the total for a given period, divided by the number of of common stock outstanding.

Exhibit 10 shows that the earnings (i.e., net income) of Chico Company in 2009 was $ and that the number of shares outstanding during 2009 was . Therefore, earnings per share was $ .

Showing 300 - 400

of 1099

1

2

3

4

5

6

7

8

9

10

11

Step by Step Answers