New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management accounting information

CIMA - C01 Fundamentals Of Management Accounting Revision Kit 1st Edition BPP Learning Media - Solutions

Using your answer to the previous question (apportioning overheads) and the following information, apportion the overheads of the two service departments using the repeated distribution method.Service department costs are apportioned as follows(a) The forming department overheads after service

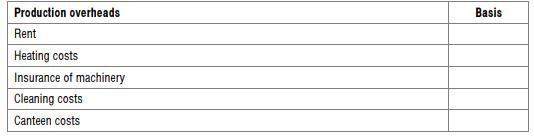

The following bases of apportionment are used by a factory.A Volume of cost centre B Value of machinery in cost centre C Number of employees in cost centre D Floor area of cost centre Complete the table below using one of A to D to show the bases on which the production overheads listed in the

The Valuation Department of a large firm of surveyors wishes to develop a method of predicting its total costs in a period. The following past costs have been recorded at two activity levels.Number of valuations Total cost(V) (TC)Period 1 420 82,200 Period 2 515 90,275 The total cost model for a

The staff at Underworld Co are paid a basic minimum wage plus an amount per item of inventory produced. What type of cost are the staff wages?A Fixed B Variable C Semi-variable D Step

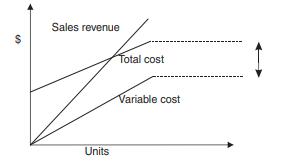

In the above graph, what does the arrow represent?A Fixed cost B Contribution C Profit D Breakeven quantity in units Sales revenue $ Units Total cost Variable cost I

Select the correct words in the following sentence.The basic principle of cost behaviour is that as the level of activity rises, costs will usually (a) rise/fall/stay the same. In general, as activity levels rise, the variable cost per unit will (b) rise/fall/stay the same, the fixed cost per unit

Tick the appropriate box for each cost. Fixed Variable Mixed (a) Telephone bill (b) Annual salary of the chief accountant (c) The management accountant's annual membership fee to CIMA (paid by the company) (d) Cost of materials used to pack 20 units of product X into a box

The cost of direct labour where employees are paid a bonus which increases as output levels increase might follow the cost behaviour pattern depicted in graph (a) above.True False The cost of direct material where quantity discounts are available might follow the cost behaviour pattern in graph

A company is considering its options with regard to a machine which cost $120,000 four years ago. If sold, the machine would generate scrap proceeds of $150,000. If kept, this machine would generate net income of $180,000. The current replacement cost of this machine is $210,000.What is the

Within the costing system of a manufacturing company the following types of expense are incurred.Reference number 1 Cost of oils used to lubricate production machinery 2 Motor vehicle licences for lorries 3 Depreciation of factory plant and equipment 4 Cost of chemicals used in the laboratory 5

A production worker is paid the following in week 5.$(a) Basic pay for normal hours worked, 36 hours at $4 per hour 144(b) Pay at the basic rate for overtime, 6 hours at $4 per hour 24(c) Overtime shift premium, with overtime paid at time-and-a-quarter¼ × 6 hours × $4 per hour 6(d) A bonus

Which of the following costs would be charged to the product as a prime cost?A Component parts B Part-finished work C Primary packing materials D Supervisor wages

Identify the following as suitable cost centres or cost units for a hospital.• Ward• Operating theatre• Bed/night• Patient/day• Outpatient visit• Operating theatre hour

Consider the following features and identify whether they relate to job costing, contract costing, service costing or none of these costing methods.J = Job costing C = Contract costing S = Service costing N = None of these costing methods(i) Production is carried out in accordance with the wishes

The following information is available for the Whiteley Hotel for the latest thirty day period.Number of rooms available per night 40 Percentage occupancy achieved 65%Room servicing cost incurred $3,900 The room servicing cost per occupied room-night last period, to the nearest cent, was:A $3.25 B

Which of the following would be appropriate cost units for a passenger coach company? (a) Vehicle cost per passenger-kilometre (b) Fuel cost for each vehicle per kilometre (c) Fixed cost per kilometre Appropriate Not appropriate

In which of the following situation(s) will job costing normally be used?Production is continuous Production of the product can be completed in a single accounting period Production relates to a single special order

JC Co operates a job costing system. The company's standard net profit margin is 20 per cent of sales value.The estimated costs for job B124 are as follows.Direct materials 3 kg @ $5 per kg Direct labour 4 hours @ $9 per hour Production overheads are budgeted to be $240,000 for the period, to be

P Co manufactures ring binders which are embossed with the customer's own logo. A customer has ordered a batch of 300 binders. The following data illustrate the cost for a typical batch of 100 binders.$Direct materials 30 Direct wages 10 Machine set up 3 Design and artwork 15 58 Direct employees

A firm uses job costing and recovers overheads as a percentage of direct labour cost.Three jobs were worked on during a period, the details of which are as follows.The overheads for the period were exactly as budgeted, $140,000.Job 3 was completed during the period and consisted of 2,400 identical

Which of the following is a feature of job costing?A Production is carried out in accordance with the wishes of the customer B Associated with continuous production of large volumes of low-cost items C Establishes the cost of services rendered D Costs are charged over the units produced in the

PA Co operates a job costing system. The company's standard net profit margin is 20 per cent of sales.The estimated costs for job 173 are as follows.Direct materials 5 metres @ $20 per metre Direct labour 14 hours @ $8 per hour Variable production overheads are recovered at the rate of $3 per

Contract number 724 commenced on 1 May and plant with a book value of $600,000 was delivered to the site from central stores. On 1 October further plant was delivered, with a book value of $48,000.Company policy is to depreciate plant at a rate of 25% of the book value each year.The book value of

A construction company has the following data concerning one of its contracts.$Contract price 1,800,000 Estimated total cost to complete contract 1,200,000 Value of work certified to date 1,170,000 No difficulties are foreseen on the contract.The profit to be recognised on the contract to date is $

A product is manufactured as a result of two processes, 1 and 2. Details of process 2 for the latest period were as follows.Opening work in progress Nil Materials transferred from process 1 10,000 kg valued at $40,800 Labour and overhead costs $8,424 Output transferred to finished goods 8,000 kg

A company makes a product, which passes through a single process.Details of the process for the last period are as follows.Materials 5,000 kg at 50c per kg Labour $700 Production overheads 200% of labour Normal losses are 10% of input in the process, and without further processing any losses can be

A company makes a product, which passes through a single process.Details of the process for the last period are as follows.Materials 5,000 kg at 50c per kg Labour $700 Production overheads 200% of labour Normal losses are 10% of input in the process, and without further processing any losses can be

A food manufacturing process has a normal wastage of 10% of input. In a period, 3,000 kgs of material were input and there was an abnormal loss of 75 kg. No inventories are held at the beginning or end of the process.The quantity of good production achieved was kg.

In process costing, if an abnormal loss arises, the process account is generally A debited with the scrap value of the abnormal loss units B debited with the full production cost of the abnormal loss units C credited with the scrap value of the abnormal loss units D credited with the full

What is a by-product?A A product produced at the same time as other products which has no value B A product produced at the same time as other products which requires further processing to put it in a saleable state C A product produced at the same time as other products which has a relatively low

What is an equivalent unit?A A unit of output which is identical to all others manufactured in the same process B Notional whole units used to represent uncompleted work C A unit of product in relation to which costs are ascertained D The amount of work achievable, at standard efficiency levels, in

Bonto Co produces a simple product in two processes, process R and process X. The following information relates to process X for period 4.Work in progress at start of period - nil.Material transferred from process R during the period - 2,500 kgs valued at $7,145.Wages paid - 234½ hours at $4 per

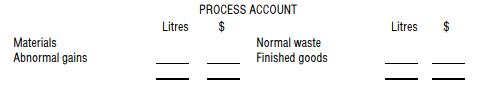

20,000 litres of liquid were put into a process at the beginning of the month at a cost of $4,400. The output of finished product was 17,000 litres. The normal level of waste in this process is 20% and the waste which is identified at the end of the process can be sold at $0.50 per litre. Use this

A company needs to produce 340 litres of Chemical X. There is a normal loss of 10% of the material input into the process. During a given month the company did produce 340 litres of good production, although there was an abnormal loss of 5% of the material input into the process.How many litres of

PC Co makes a product in two processes. The following data is available for the latest period, for process 1.Opening work in progress of 200 units was valued as follows.Material $2,400 Labour $1,200 Overhead $400 No losses occur in the process.Units added and costs incurred during the

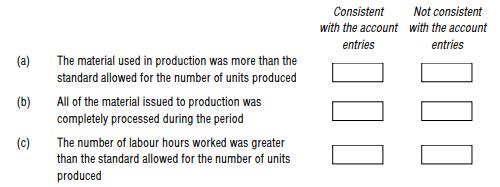

PB Co maintains a standard cost bookkeeping system. The work in progress account for the latest period is as follows.WORK IN PROGRESS CONTROL ACCOUNT$'000 $'000 Stores account 724 Finished goods control 3,004 Wages control 1,210 Material usage variance 180 Production overhead control 1,050 Labour

Which of the following statements is correct?A An adverse direct material cost variance will always be a combination of an adverse material price variance and an adverse material usage variance B An adverse direct material cost variance will always be a combination of an adverse material price

In a standard cost bookkeeping system, when the actual wage rate paid per hour is higher than the standard wage rate per hour, the accounting entries to record this are Debit Credit A Labour rate variance account Wages control account B Labour rate variance account Work in progress control account

The following extract is taken from the production cost budget of W Co:Production units 2,000 3,000 Production cost $17,760 $20,640 The budget cost allowance for an activity level of 4,000 units is A $11,520 B $23,520 C $27,520 D $35,520

A flexible budget is A a budget comprising variable production costs only B a budget which is updated with actual costs and revenues as they occur during the budget period C a budget which shows the costs and revenues at different levels of activity D a budget which is prepared using a computer

(a) Budgetary control procedures are useful only to maintain control over an organisation's expenditure(b) A prerequisite of flexible budgeting is a knowledge of cost behaviour patterns(c) Fixed budgets are not useful for control purposes True False

Which of the following best describes a flexible budget?A A budget which is designed to be easily updated to reflect recent changes in unit costs or selling prices B A budget which can be flexed when actual costs are known, to provide a realistic forecast for the forthcoming period C A budget

The following extract is taken from the distribution cost budget of DC Co:Volume delivered (units) 8,000 14,000 Distribution cost $7,200 $10,500 The budgeted cost allowance for distribution cost for a delivery volume of 12,000 units is A $6,600 B $9,000 C $9,400 D $10,800

When preparing a production budget, the quantity to be produced equals A sales quantity + opening inventory + closing inventory B sales quantity – opening inventory + closing inventory C sales quantity – opening inventory – closing inventory D sales quantity + opening inventory – closing

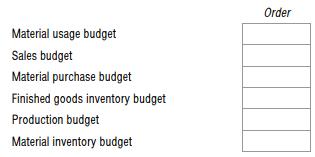

If a company has no production resource limitations, in which order would the following budgets be prepared? Material usage budget Sales budget Material purchase budget Finished goods inventory budget Production budget Material inventory budget Order

The following details have been extracted from the accounts receivable records of PR Co.Invoices paid in the month after sale 80%Invoices paid in the second month after sale 10%Invoices paid in the third month after sale 5%Bad debts (irrecoverable debts) 5%Invoices are issued on the last day of

In a situation where there are no production resource limitations, which of the following must be available for the material usage budget to be completed? Tick all that apply.(a) Production volume from the production budget(b) Budgeted change in materials inventory(c) Standard material usage per

PG Co makes a single product and is preparing its material usage budget for next year. Each unit of product requires 2 kg of material, and 5,000 units of product are to be produced next year.Opening inventory of material is budgeted to be 800 kg and PG Co budgets to increase material inventory at

Which of the following would help to explain a favourable sales volume variance?(i) Increased competitor activity led to a reduction in the number of units sold.(ii) Customers were given discounts at a higher level than standard in order to encourage increased sales.(iii) The unit cost of

J Co operates a standard cost accounting system. The following information has been extracted from its standard cost card and budgets.Budgeted sales volume 5,000 units Standard sales price $10.00 per unit Standard variable cost $5.60 per unit Standard total cost $7.50 per unit If it used a standard

J Co uses a standard costing system and has the following data relating to one of its products.$ $Selling price 9.00 Variable cost 4.00 Fixed costs 3.00 7.00 Profit per unit 2.00 Its budgeted sales for October 20X5 were 800 units, but the actual sales were 850 units. The revenue earned from these

P Co has the following data relating to its budgeted sales for October 20X7:Budgeted sales $100,000 Budgeted selling price per unit $8.00 Budgeted contribution per unit $2.50 During October 20X7, actual sales were 11,000 units for a sales revenue of $99,000.P Co uses a marginal costing system.The

Standard and budgeted data for the latest period for a company's single product are as follows:Budgeted sales volume 19,680 units Actual sales volume 18,780 units Standard selling price per unit $27.10 Standard variable cost per unit $21.70 Actual sales revenue $529,596 The sales price variance for

The material price variance for May is:A $8,900 (F) C $62,000 (F)B $51,150 (F) D $64,100 (F) Standard costing is used to control the material costs of product Alpha. No material inventories are held. The following data are available for product Alpha during May. Production units Material usage

The material usage variance for May is:A $750 (A) C $9,000 (A)B $6,000 (A) D $28,800 (F) Standard costing is used to control the material costs of product Alpha. No material inventories are held. The following data are available for product Alpha during May. Production units Material usage Material

SL Co has budgeted to make and sell 4,200 units of product S during the period.The standard variable overhead cost per unit is $4.During the period covered by the budget, the actual results were as follows.Production and sales 5,000 units Variable overhead incurred $17,500 The variable overhead

Which of the following would help to explain a favourable direct material price variance?(a) The standard price per unit of direct material was unrealistically high (b)Output quantity was greater than budgeted and it was possible to obtain bulk purchase discounts (c)The material purchased was of a

SG Co has extracted the following details from the standard cost card of one of its products.Direct labour 3.5 hours @ $9.20 per hour During period 4, SG Co produced 1,600 units of product and incurred direct labour cost of $55,100 for 5,800 hours.The direct labour rate and efficiency variances for

Calculate the standard cost of producing 100 wheels for a toy car using the information given below. Fill in the shaded box.Bending Cutting Assembly Standard labour rates of pay per hour $ 4 6 5 Standard labour rates per 100 wheels (hours) 0.8 0.5 1.2 Toy car wheels Direct materials STANDARD COST

PM Co is in the process of setting standard unit costs for next period. Period J uses two types of material, P and S. 7 kg of material P and 3 kg of material S are needed, at a standard price of $4 per kg and $9 per kg respectively.Direct labour will cost $7 per hour and each unit of J requires 5

CC Co manufactures a carbonated drink, which is sold in 1 litre bottles. During the bottling process there is a 20%loss of liquid input due to spillage and evaporation. The standard usage of liquid per bottle is A 0.80 litres B 1.00 litres C 1.20 litres D 1.25 litres

Standard costing provides which of the following? Tick all that apply.(a) Targets and measures of performance(b) Information for budgeting(c) Simplification of inventory control systems(d) Actual future costs

Fast Fandango Co manufactures a single product, the FF, which sells for $10. At 75% capacity, which is the normal level of activity for the factory, sales are $600,000 per period.The cost of these sales are as follows.Direct cost per unit $3 Production overhead $156,000 (including variable costs of

S Co manufactures a single product, V. Data for the product are as follows.$ per unit Selling price 40 Direct material cost 8 Direct labour cost 6 Variable production overhead cost 4 Variable selling overhead cost 2 Fixed overhead cost 10 Profit per unit 10 The profit/volume ratio for product V is

Product N generates a contribution to sales ratio of 20%. Annual fixed costs are $80,000.The breakeven point, in terms of units sold per annum, A is 96,000 B is 400,000 C is 480,000 D cannot be calculated without more information 29(a) H on the graph indicates the value of A contribution B fixed

V Co manufactures three products which have the following selling prices and costs per unit.V1 V2 V3$ $ $Selling price 30.00 36.00 34.00 Costs per unit Direct materials 8.00 10.00 20.00 Direct labour 4.00 8.00 3.60 Overhead Variable 2.00 4.00 1.80 Fixed 9.00 6.00 2.70 23.00 28.00 28.10 Profit per

J Co manufactures three products, details of which are as follows.Product K Product L Product M$ per unit $ per unit $ per unit Selling price 105 133 133 Direct materials ($3/litre) 15 6 21 Direct labour ($8/hour) 24 32 24 Variable overhead 9 12 9 Fixed overhead 23 50 42 In a period when direct

If the last-in, first-out method of pricing had been used the value of the issue on 9 September would have been:A $350 B $395 C $410 D $420 Date 1 Jan Units Unit Price Value $ $ Balance b/f 100 5.00 500.00 3 Mar Issue 40 4 June Receipt 50 5.50 275.00 6 June Receipt 50 6.00 300.00 9 Sept Issue 70

If the first-in, first-out method of pricing had been used the value of the issue on 9 September would have been:A $350 B $355 C $395 D $420 Date 1 Jan Units Unit Price Value $ $ Balance b/f 100 5.00 500.00 3 Mar Issue 40 4 June Receipt 50 5.50 275.00 6 June Receipt 50 6.00 300.00 9 Sept Issue 70

800 units of component L valued at a price of $4.20 each were in inventory on 1 May.The following receipts and issues were recorded during May. 9 May Received 2,500 units at $4.50 per unit 21 May Received 1,800 units at $4.80 per unit 24 May Issued 4,500 units Using the LIFO method of inventory

(a) Product S's unit cost is $5. A selling price is based on a margin of 25%. The selling price is $ to the nearest cent.(b) Product H sells for $175. The mark-up is 12%. The unit cost of product H is $ to the nearest cent.

R Co expects to sell 10,000 units of product Y in the coming year. The organisation makes an annual investment of$1,700,000 in production of product R and requires a return of 22% on its investment. The full cost of product Y is$15.The required selling price of product Y is $ .

A Co requires a 25% return on sales. The full cost of product R is $27.The selling price of product R should be $ .

B Company makes a product which has a variable production cost of $21 per unit and a sales price of $39 per unit.At the beginning of 20X5, there was no opening inventory and sales during the year were 50,000 units. Fixed costs(production, administration, sales and distribution) totalled $328,000.

Cost and selling price details for product Q are as follows.$ per unit Direct material 4.20 Direct labour 3.00 Variable overhead 1.00 Fixed overhead 2.80 11.00 Profit 4.00 Selling price 15.00 Budgeted production for month 10,000 units Actual production for month 12,000 units Actual sales for month

The budgeted production overheads and other budget data of Eiffel Co are as follows.Production Budget dept X Overhead cost $36,000 Direct materials cost $32,000 Direct labour cost $40,000 Machine hours 10,000 Direct labour hours 18,000 What would be the absorption rate for Department X using the

AC Co absorbs production overhead in the assembly department on the basis of direct labour hours. Budgeted direct labour hours for the period were 200,000. The production overhead absorption rate for the period was $2 per direct labour hour.Actual results for the period were as follows.Direct

Department L production overheads are absorbed using a direct labour hour rate. Budgeted production overheads for the department were $480,000 and the actual labour hours were 100,000. Actual production overheads amounted to $516,000.Based on the above data, and assuming that the production

Which of the following would be the most appropriate basis for apportioning machinery insurance costs to cost centres within a factory?A The number of machines in each cost centre B The floor area occupied by the machinery in each cost centre C The value of the machinery in each cost centre D The

Identify which type of cost is being described in (a)-(d) below.(a) This type of cost stays the same, no matter how many products you produce (b) This type of cost increases as you produce more products. The sum of these costs are also known as the marginal cost of a product (c) This type of cost

The following is a graph of cost against level of activityTo which one of the following costs does the graph correspond?A Sales commission payable per unit up to a maximum amount of commission B Electricity bills made up of a standing charge and a variable charge C Bonus payments to employees, paid

A delivery driver for a courier company is paid a salary of $1,000 per month, plus an extra 12 cents per delivery made. This labour cost is best described as:A a variable cost C a fixed cost B a step cost D a semi-variable cost

DP Co is preparing its estimate of distribution costs for the next period. Based on previous experience, a linear relationship has been identified between sales volume and distribution costs. The following information has been collected concerning distribution costs.Sales volume Distribution cost

A system of accounting that segregates revenue and costs into areas of personal responsibility in order to monitor and assess the performance of each part of the organisation is known as:A Control accounting C Controllable accounting B Responsibility accounting D Centre accounting

Direct costs are:A costs which can neither be identified with a cost centre nor identified with a single cost unit B costs which can be identified with a single cost unit C costs incurred as a direct result of a particular decision D costs incurred which can be attributed to a particular accounting

Fill in the blanks in the statements below, using the words in the box.• Costs can be divided into the following three categories (1)…………….; (2)………….. ; (3) …………..• There are a number of different ways in which costs can be classified.– (4)………… and

Employee A is a carpenter and normally works 36 hours per week, which is treated as direct labour. The standard rate of pay is $7.00 per hour. A premium of 50% of his basic hourly rate is paid for all overtime hours worked.During the last week of October, Employee A worked for 42 hours. The

Which of the following are part of the prime cost for a manufacturing company?A Maintenance cost of a machine used in production B Salary cost of a supervisor overseeing direct employees C Cost of a canteen used by production employees D Royalties payable to the designer of the basic product

Which two of the following might be characteristic of a hospital?Use of composite cost units Use of equivalent units High levels of indirect costs as a proportion of total cost Calculation of profit per patient

Value added is:A Sales less cost of materials and services B Sales less labour cost C Sales less internally generated costs D Sales less cost of bought-in materials and services

Average cost per unit of service = .......... ........................... .................

What are the specific characteristics of services.I Intangibility II Heterogeneity III Perishability IV Consistency V Regularity VI Simultaneity A I, III, V and VI B II, III, IV and V C I, II, III and VI D II, IV, V and VI

Match up the following services with their typical cost units Service Hotels Education Hospitals Catering organisations ? Cost unit Patient-day Meal served Full-time student Occupied bed-night

With many services the cost of direct materials will be relatively high.True False

HMF has a year end of 30 June. The following information is available for Contract W.Start date 1 July 20X5 Completion date 30 September 20X6$'000 Contract price 12,000 Materials sent to site 4,200 Materials returned to stores 480 Plant hire charges 1,200 Labour costs 1,800 Other expenses 600 Value

Job costing would be most appropriate for which of the following businesses?A A pizza manufacturer C A manufacturer of sugar B An architect designing a new school D A manufacturer of screws

The following information is available for contract AF3.Contract price $15 million Cost of work to date $5,040,000 Estimated costs to completion $3,960,000 The amount of profit to be recognised on the contract is A $0 B $3,360,000 C $6,000,000 D $8,400,000

How would you account for a loss on an incomplete contract?

List six features of contract costing• …………………………………………………………………………………………………..• ………………………………………………………………………….……………………….•

The cost of a job is $100,000(a) If profit is 25% of the job cost, the price of the job = $(b) If there is a 25% margin, the price of the job = $

Showing 2600 - 2700

of 4138

First

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

Last

Step by Step Answers