New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management accounting

Management Accounting For Business Decisions 2nd Edition Colin Drury - Solutions

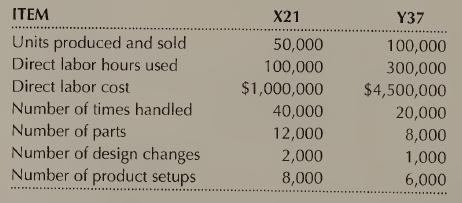

Cost distortions Ehsan Electronics Company manufactures two products, X21 and Y37, at its manufacturing plant in Duluth, Minnesota. For many years the company has used a simple plant-wide manufacturing support cost rate based on direct labor hours. A new plant accountant suggested that the company

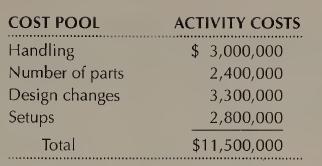

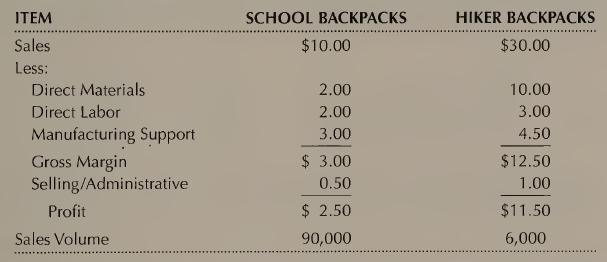

Product profitability analysis Kidspack, Inc., has recently expanded its line of LO 1, 3, 4, 5 backpacks to include high-quality, lightweight hiker backpacks. This new model uses more expensive material and takes longer to produce. While a basic school backpack can be cut and sewn together in 30

Activity cost drivers The Simply French Restaurant has identified the following activities performed by its staff:Set tables Seat customers Take orders Cook food Serve orders Take dessert orders Serve dessert Present bills and collect Clean tables REQUIRED(a) For each of the above activities, state

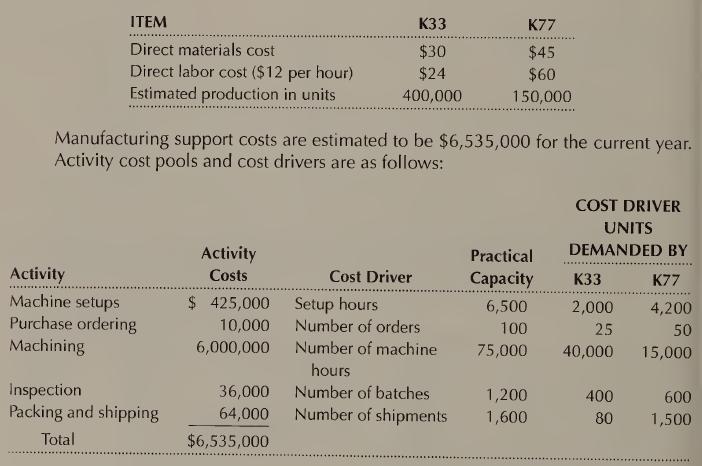

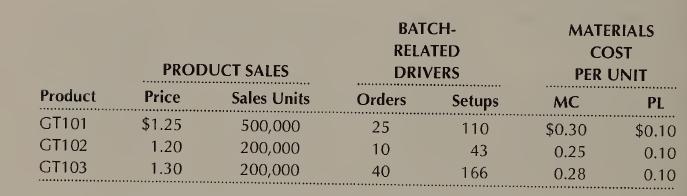

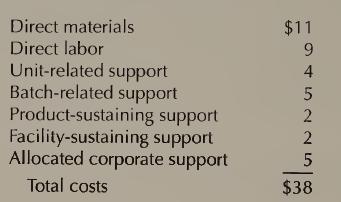

Cost driver rates with practical capacity Kohlman Company manufactures two products: K33 and K77. Estimated unit cost and production data follow:REQUIRED (a) Estimate the manufacturing cost per unit of each product if support costs are assigned to products using activity-based cost driver rates

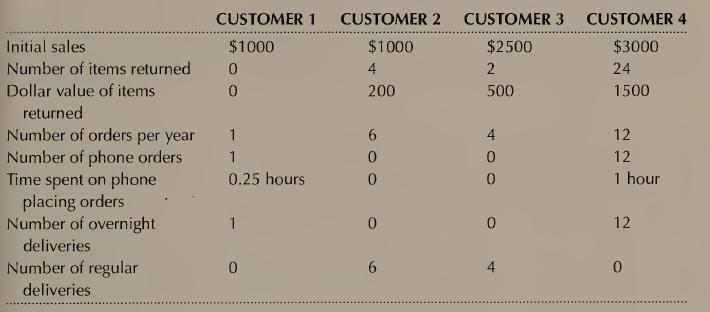

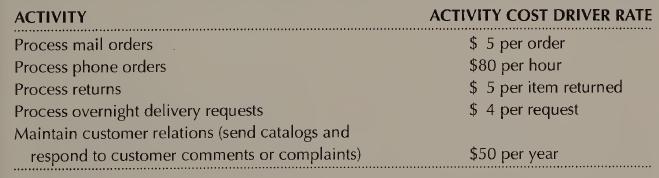

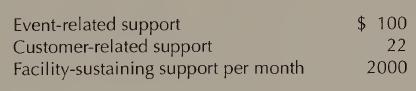

Customer profitability analysis Kronecker Company, a growing mail-order LO 3, 5, 7, 8, 9 clothing and accessory company, is concerned about its growing marketing, dis¬ tribution, selling, and administration expenses. It therefore examined its cus¬ tomer ordering patterns for the past year and

Activity cost driver rates The customer billing department at U.S. West Tele¬communication, Inc. currently employs 25 billing clerks on annual contract. Each clerk works 160 hours per month. The average monthly wages of billing clerks, including benefits, amount to $2800. Other billing-related

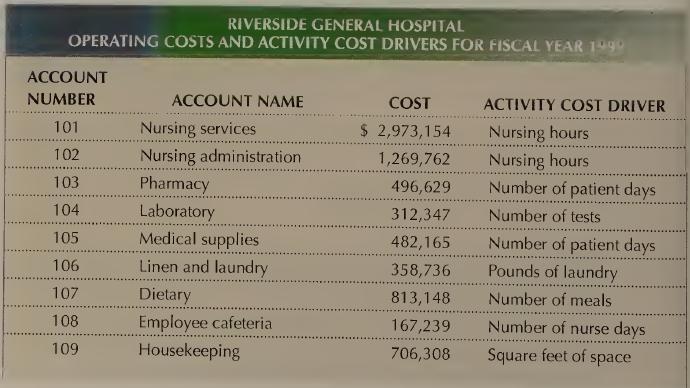

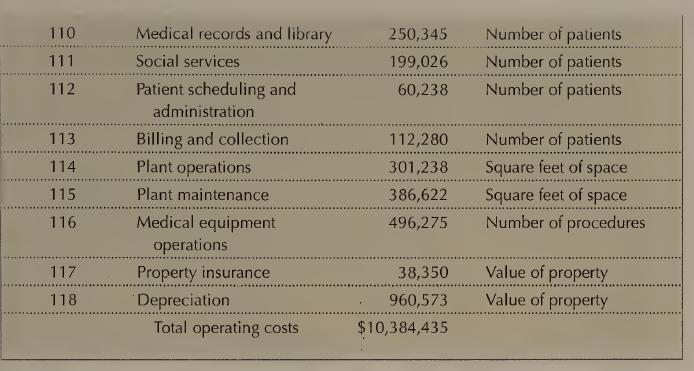

Activity-based costing in a health care organization In computing the cost of patient stays, Riverside General Hospital assesses physician costs and medication costs directly to each patient. Riverside has examined its support costs for patient stays, resulting in identification of 18 account

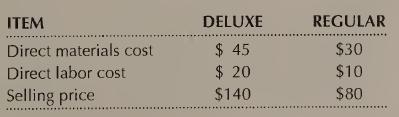

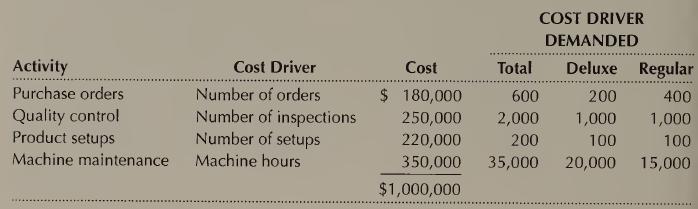

Product cost distortions The Manhattan Company manufactures two models of LO 1, 3, 4, 5 compact disc players: a deluxe model and a regular model. The company has manufactured the regular model for years; the deluxe model was introduced re¬ cently to tap a new segment of the market. Since the

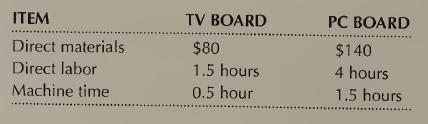

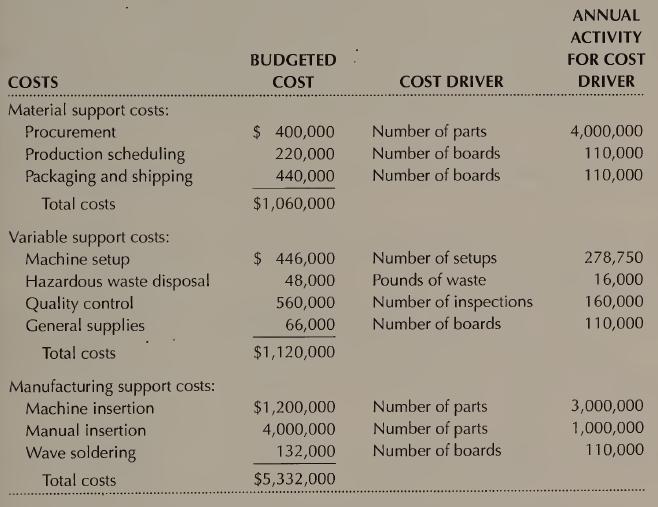

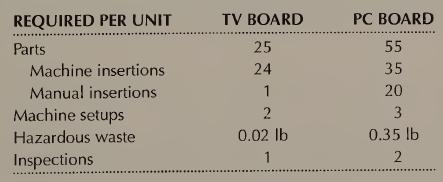

Activity-based costing (Adapted from CMA, June 1992) Alaire Corporation manufactures several different types of printed-circuit boards; however, two of the boards account for the majority of the company's sales. The first of these boards, a TV circuit board, has been a standard in the industry for

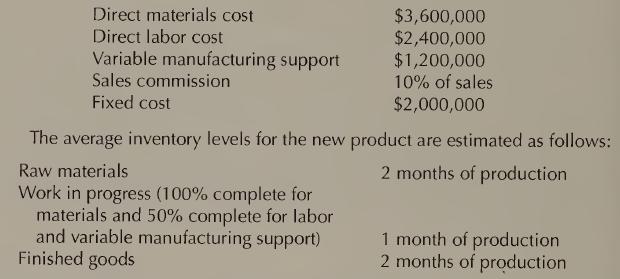

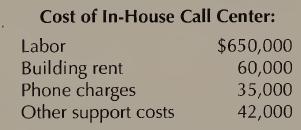

Activity-based costing for services, outsourcing Smithers, Inc. manufactures 10 and sells a wide variety of consumer products. The products are viewed as suffi¬ciently profitable, but recently, some product line managers have complained about the charges for the call center that handles phone

Comparison of two costing systems The Redwood City plant of Crimson Components Company makes two types of rotators, R361 and R572, for auto¬ mobile engines. The old cost accounting system at the plant traced support costs to four cost pools:Poo! SI included service activity costs related to

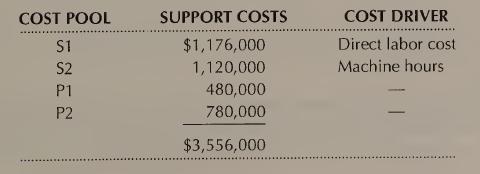

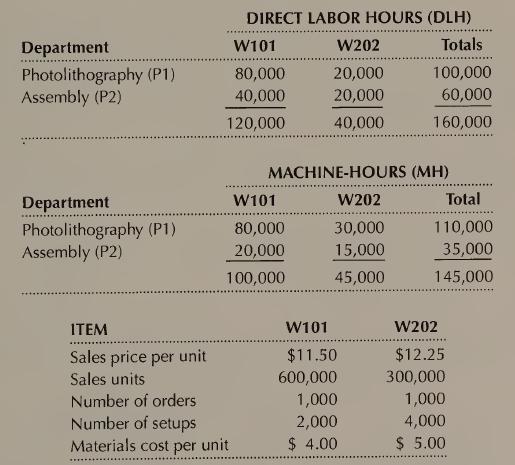

Activity-based costing The Fishburn plant of Hibeem Electronics Corporation LO 1, 3, 4, 5 makes two types of wafers, W101 and W202, for electronic instruments. The old cost accounting system at the plant traced support costs to three cost pools.Pool S included all service activity costs at the

Activity-based costing Sandra Slaughter, senior vice president for sales for Showman Shoes, Inc., noticed that the company had substantially increased its market share for the high-quality boomer boots (BB) and lost market share for the lower-quality lazy loafers (LL). Sandra found that Showman's

Product profitability analysis Petersen Pneumatic Company makes three products. Its manufacturing plant in Petersburg has three production depart¬ ments and three service departments.The profitability of the Petersburg plant has been declining for the past three years despite the successful

Product profitability analysis Pharaoh Phawcetts, Inc. manufactures two mod- LO 1, 3, 4, 5, els of faucets: a regular and a deluxe model. The deluxe model, introduced just 10 two years ago, has been very successful. It now accounts for more than half of the firm's profits as evidenced by the

Cost distortions Sweditrak Corporation manufactures two models of its exer- LO 1, 3, 4 cise equipment: regular (REG) and deluxe (DLX). Its plant has two production departments, fabrication (FAB) and assembly (ASM), and two service depart¬ ments, maintenance (MNT) and quality control (QLC). The

Identifying activity costs Linda Collins is manager in charge of cost analysis and LO 3, 4, 5 planning at Montex Company. Montex makes steel and brass pumps at its four plants located in Minnesota, Indiana, Illinois, and Michigan. Linda first examined the accounting and payroll records at the

Part proliferation: role for activity-based costing Discuss case 1-27.

Role for activity-based cost systems in implementing strategy Discuss case 1-28.

Financial versus management accounting: role for activity-based cost sys¬ tems in privatization ofgovernment services Discuss case 1 -29.

explain why sunk costs are not relevant costs LO1

analyze make-or-buy decisions LO1

demonstrate the influence of qualitative factors in making decisions LO1

compare the different types of facilities layouts LO1

explain the theory of constraints LO1

demonstrate the value of just-in-time manufacturing systems LO1

describe the concept of the cost of quality LO1

calculate the cost savings resulting from reductions in inventories, reduction in production cycle time, production yield improvements, and reductions in rework and defect rates LO1

Why should decision makers focus only on the relevant costs for decision making? (LO 1)

Are sunk costs relevant? Explain. (LO 1)

What behavioral factors many influence some managers to consider sunk costs as being rele¬ vant in their decisions? (LO 1)

Are direct materials and direct labor costs al¬ ways relevant? Explain with examples. (LO 1, 2)

When are (1) product-sustaining and (2) facility- sustaining (business sustaining) costs relevant? Give examples of each case. (LO 2)

Why can't we directly compare cash flows at different points in time? (LO 2)

Are avoidable costs relevant? Explain. (LO 2)

Give two examples of costs and decision con¬ texts in which the costs are not relevant for a short-term context but are relevant for a long¬ term context. (LO 2)

What qualitative considerations are relevant in a make-or-buy decision? (LO 2, 3)

What are the opportunity costs that are relevant in a make-or-buy decision? (LO 2)

What is the difference between process and product layout systems? (LO 5)

What is cellular manufacturing? (LO 5)

How is a just-in-time manufacturing system dif¬ ferent from a conventional manufacturing sys¬ tem? (LO 7)

What creates the need to maintain work- in-process inventory? Why is work-in-process inventory likely to decrease on the implementa¬ tion of cellular manufacturing, just-in-time pro¬ duction, and quality improvement programs?(LO 5, 7)

Why are production cycle time and the level of work-in-process inventory positively related? (LO 5, 7)

List two types of costs incurred when imple¬ menting a cellular manufacturing layout. (LO 5)

What are two types of financial benefits result¬ ing from a shift to cellular manufacturing, just- in-time production, or continuous quality improvements? (LO 5, 7)

What is meant by the term cost of nonconfor¬ mance? (LO 6)

Waste, rework, and net cost of scrap are exam¬ ples of what kinds of quality costs? (LO 6)

Quality engineering, quality training, statistical process control, and supplier certification are what kinds of quality costs? (LO 6)

List three examples for each of the following quality costing categories:(a) prevention costs(b) appraisal costs(c) internal failure costs(d) external failure costs (LO 6)

What is the additional cost of replacing one unit of a product rejected at inspection and scrapped? (LO 6, 8)

What is the additional cost if a unit rejected at inspection can be reworked to meet quality standards by performing some additional oper¬ ations? (LO 6, 8)

What costs and revenues are relevant in evalu¬ ating the profit impact of an increase in sales? (LO 8)

"Design an accounting system that routinely re¬ ports only relevant costs," advised a manage¬ ment consultant. Is this good advice? Explain. (LOG 2, 8)

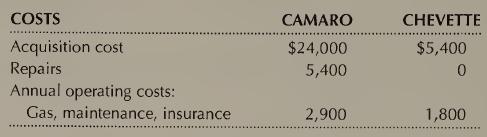

Relevant costs Don Baxter's five-year-old Camaro requires repairs estimated at $5400 to make it roadworthy again. His friend, Mike Blue, suggested that he buy a five-year-old Chevette instead for $5400 cash. Mike estimated the following costs for the two cars:REQUIRED (a) What costs are relevant

Relevant costs Gilmark Company has 10,000 obsolete lamps carried in inven¬ tory at a cost of $12 each. They can be sold as they are for $4 each. They can be reworked, however, at a total cost of $55,000 and sold for $10 each. Determine whether it is worthwhile to rework these lamps.

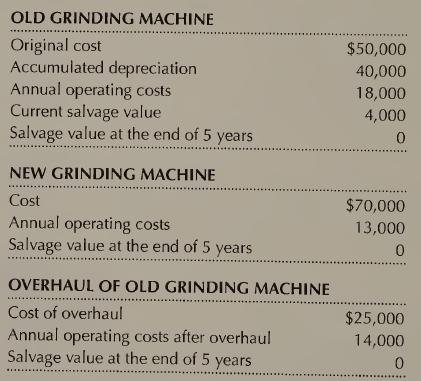

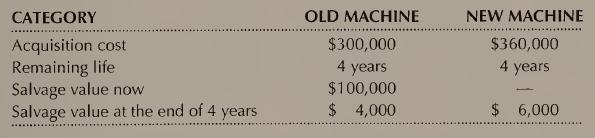

Sunk costs Ideal Company's plant manager is considering buying a new grind¬ ing machine to replace an old grinding machine or overhauling the old one to ensure compliance with the plant's high-quality standards. The following data are available:REQUIRED (a) What costs should the decision maker

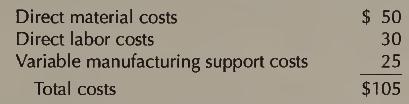

Make-or-buy Kane Company is considering outsourcing a key component. A LO 2 reliable supplier has quoted a price of $64.50 per unit. The following costs of the component when manufactured in-house are expressed on a per-unit basis.REQUIRED (a) What assumptions need to be made about the behavior of

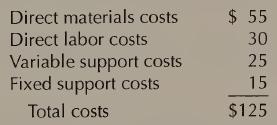

Relevant costs in the make-or-buy decision Premier Company manufactures LO 2 gear model G37 used in several of its farm-equipment products. Annual produc¬ tion volume of C37 is 20,000 units. Unit costs for G37 are as follows:Alternatively, Premier can also purchase gear model G37 from an outside

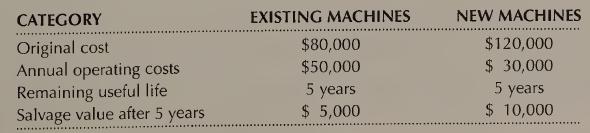

Relevant costs and revenues Joyce Printers, Inc. is considering replacing its cur- LO 1 rent printing machines with newer, faster, and more efficient printing technology.The following data have been compiled:The existing machines can be disposed of now for $40,000. Keeping them will cost $20,000

Relevant costs for decision making Kentucky Motors has manufactured com¬pressor parts at its plant in Pitcairn, Indiana, for the last 18 years. An outside sup¬ plier, Superior Compressor Company, has offered to supply compressor model A238 at a price of $200 per unit. Unit manufacturing costs for

Quality cost categories Regarding the quality costing categories, how do pre¬vention costs differ from appraisal costs? How do internal failure costs differ from external failure costs?

Quality cost categories Of the four quality costing categories, which quality cost is the most damaging to the organization? Explain.

Quality improvement programs and cost savings Pyro Valves Company manu¬factures brass valves meeting precise specification standards. All finished valves are inspected before packing and shipping to customers. Rejected valves are re¬ turned to the initial production stage to be melted and recast.

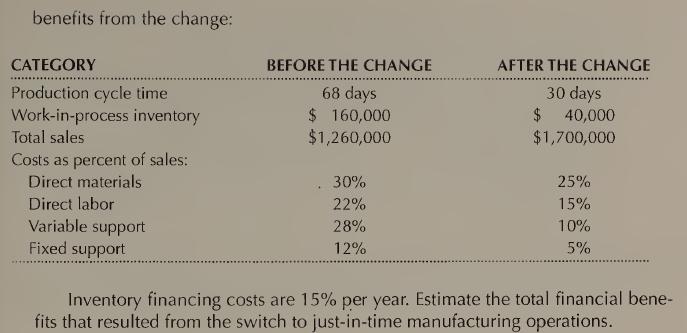

Just-in-time manufacturing and cost savings Bogden Company introduced just-in-time manufacturing last year and has prepared the following data to assess the benefits from the change: CATEGORY Production cycle time Work-in-process inventory Total sales Costs as percent of sales: Direct materials

Facilities layout How would you classify the layout of a large grocery store? Why do you think it is laid out this way? Can you think of any way to improve the layout of a conventional grocery store? Explain your reasoning. (Hint: Think about JIT, cycle time, etc.)

Relevant costs for decision making Carmen's Catering provides lunches and dinners for various groups or organizations in the locality. A new customer has approached Carmen's Catering to provide dinner for a special event featuring a well-known s-peaker, with estimated attendance of 100 people.

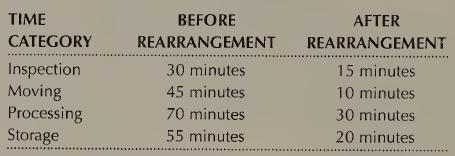

Relevant cost and revenues: changes in facilities layout To facilitate a move to¬ ward JIT production, AB Company is considering a change in its plant layout. The plant controller, Anita Bentley, has been asked to evaluate the costs and ben¬ efits of the change in plant layout. After meeting with

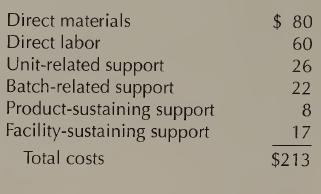

Relevant costs in the make-or-buy decision Tanner Appliance Company manu¬factures 12,000 units of part M4 annually. The part is used in the production of one of its principal products. The following unit cost information is available on part M4.A potential supplier has offered to manufacture this

Relevant costs: replacement decision Anderson Department Stores is consider¬ing the replacement of the existing elevator system at its downtown store. A new system has been proposed that runs faster than the existing system, experi¬ ences few breakdowns, and as a result promises considerable

Relevant costs: replacement decision Syd Young, the production manager at LO 1 Fuchow Company, purchased a cutting machine for the company last year. Six months after the purchase of the cutting machine, Syd learned about a new cut¬ ting machine that is more reliable than the machine that he

ABC and TOC Refer to the In Practice entitled "ABC versus TOC: Will Ever the LO 4 Twain Meet?" on p. 228. Discuss the similarities and differences between activ¬ ity-based costing and theory of constraints, and situations in which one ap¬ proach might be preferable to the other.

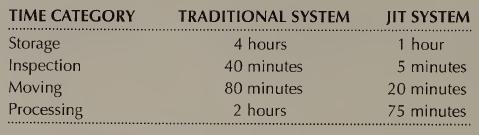

Cycle time efficiency and JIT Walker Brothers Company is considering in¬stalling a JIT manufacturing system in the hope that it will improve their overall manufacturing cycle efficiency. Data from the traditional system and estimates for the JIT system are presented below for their Nosun

JIT and cellular manufacturing You are a manufacturing manager faced with the decision to improve manufacturing operations and efficiency. You have been studying both cellular manufacturing and just-in-time manufacturing systems. Your boss expects you to prepare a report covering the costs and

Relevant costs: replacement decision Rossman Instruments, Inc. is considering leasing new state-of-the-art machinery at an annual cost of $900,000. The new machinery has a four-year expected life. It will replace existing machinery leased one year earlier at an annual lease cost of $490,000

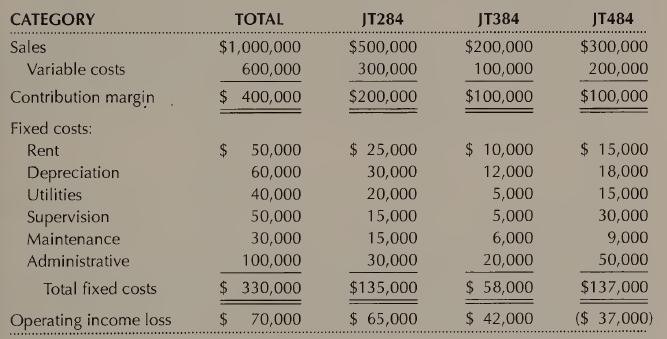

Relevant costs: dropping a product Merchant Company manufactures and LO 1 sells three models of electronic printers. Ken Gail, president of the company, is considering dropping model JT484 from its product line because the com¬ pany has experienced losses for this product over the last three

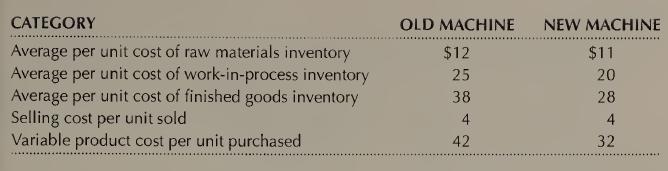

Relevant costs: introducing a new product Macready Company is consider¬ing introducing a new model of personal compact disc players at a price of $105 per unit. Its controller has compiled the following incremental cost in¬ formation based on an estimate of 120,000 units of sales annually for the

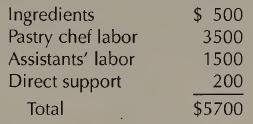

Make-or-buy Beau's Bistro has a reputation for providing good value for its menu prices. The desserts, developed by the pastry chef, are one of the distinc¬ tive features of the menu. The pastry chef has just given notice that he will relo¬ cate to another city in a month, and has volunteered to

Outsourcing, ethics Hollenberry, Inc. is a successful mail-order catalog busi¬ ness with customers worldwide. The company's headquarters are in a small town some distance from any major metropolitan area. Sales have grown steadily over the years, and the call center facilities are currently

Cellular manufacturing and cycle time efficiency Ray Brown's company, Whis¬ per Voice Systems, is trying to increase its manufacturing cycle efficiency (MCE). Because Ray has a very limited budget, he has been searching for a way to in¬ crease his MCE by using cellular manufacturing. One of Ray's

Facilities layout One aspect of facilities layout for McDonald's is that when cus¬tomers come into the building they can line up in one of several lines and wait to be served. In contrast, at Wendy's, customers are asked to stand in one line that snakes around the front of the counter and wait for

Relevant costs and revenues; marketing channels Diamond Bicycle Com¬pany manufactures and sells bicycles nationwide through marketing channels ranging from sporting goods stores to specialty bicycle shops. Diamond's av¬ erage selling price to its distributors is $185 per bicycle. The bicycles are

Relevant costs, qualitative factors, costs of quality framework, ethics Kwik 10 2,3,6 Clean handles both commercial laundry and individual customer dry clean¬ ing. Kwik Clean's current dry-cleaning process involves emitting a pollutant into the air. In addition, the commercial laundry dry cleaning

show how a firm chooses its product mix in the short term LO1

explain how a firm adjusts its prices in the short term depending on whether capacity is limited LO1

discuss how a firm determines a long-term benchmark price to guide its pricing strategy LO1

evaluate the long-term profitability of products and market segments LO1

A company absorbs overheads on machine hours which were budgeted at 11250 with overheads of 258 750. Actual results were 10980 hours with overheads of 254 692. Overheads were: A B under-absorbed by 2152 over-absorbed by 4058 C under-absorbed by 4058 D over-absorbed by 2152

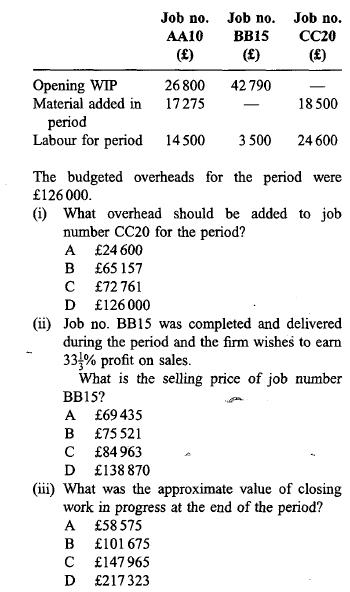

A firm makes special assemblies to customers' orders and uses job costing. The data for a period are: Opening WIP Job no. Job no. Job no. AA10 BB15 CC20 () () () 26 800 42 790 - 17275 - Material added in period Labour for period 14500 3500 18500 24 600 The budgeted overheads for the period were

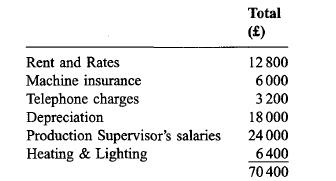

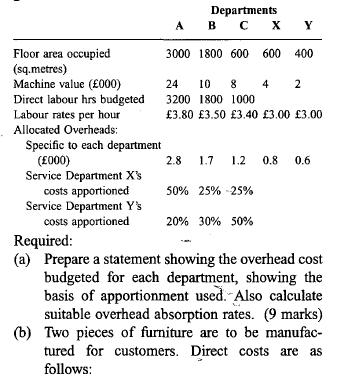

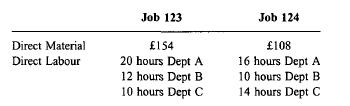

Overhead analysis and calculation of product costs A furniture-making business manufactures quality furniture to customers' orders. It has three produc- tion departments and two service departments. Budgeted overhead costs for the coming year are as follows: Rent and Rates Machine insurance

Calculation of overhead absorption rates and under/over-recovery of overheads BEC Limited operates an absorption costing system. Its budget for the year ended 31 December shows that it expects its production overhead expenditure to be as follows:(iii) that the actual production was 15 000 units.

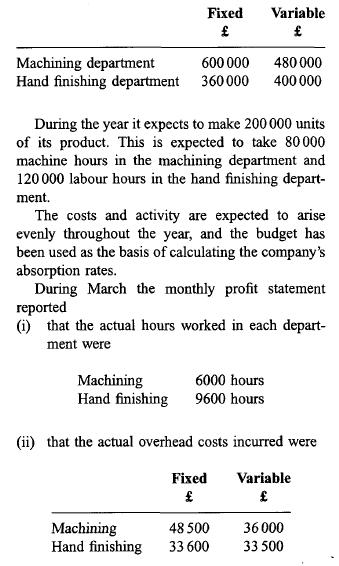

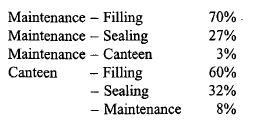

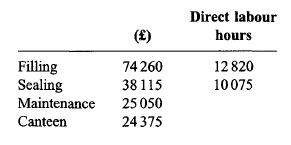

Calculation of under/over recovery of overheads A company produces several products which pass through the two production departments in its factory. These two departments are concerned with filling and sealing operations. There are two service departments, maintenance and canteen, in the factory.

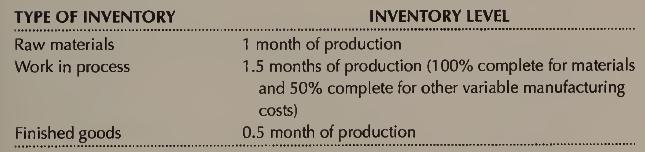

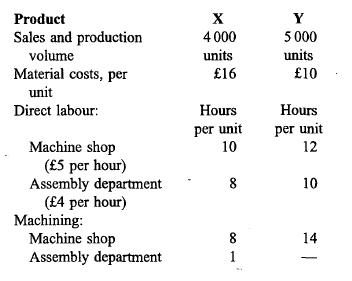

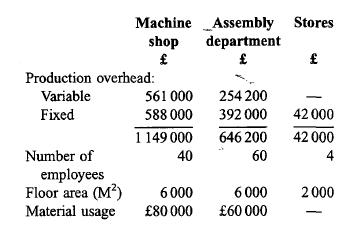

Product cost calculation and costs for decision-making Shown below is next year's budget for an engineer- ing company manufacturing two different products in two production departments, namely a machine shop and an assembly department. A stores depart- ment is responsible for storing and issuing

The following information provides details of the costs, volume and cost drivers for a particular period in respect of ABC plc, a hypothetical company:"The company operates a just-in-time inventory policy, and receives each component once per production run. In the past the company has allocated

'It is now fairly widely accepted that conventional cost accounting distorts management's view of business through unrepresentative overhead alloca- tion and inappropriate product costing. This is because the traditional approach usually absorbs overhead costs across products and orders solely on

'Attributing direct costs and absorbing overhead costs to the product/service through an activity- based costing approach will result in a better understanding of the true cost of the final output.' (Source: a recent CIMA publication on costing in a service environment.) You are required to explain

Large service organisations, such as banks and hospitals, used to be noted for their lack of stan- dard costing systems, and their relatively unsophis- ticated budgeting and control systems compared with large manufacturing organisations. But this is changing and many large service organisations

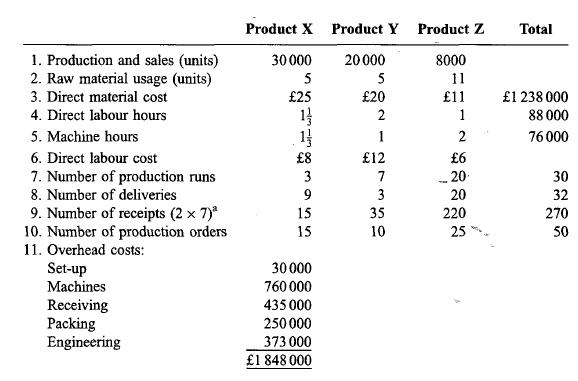

Calculation of ABC product costs and a discussion of the usefulness of ABC Trimake Limited makes three main products, using broadly the same production methods and equip- ment for each. A conventional product costing system is used at present, although an activity- based costing (ABC) system is

Preparation of conventional costing and ABC profit statements The following budgeted information relates to Brunti plc for the forthcoming period:Overheads allocated and apportioned to production departments (including service cost centre costs) were to be recovered in product costs as

Comparison of ABC with traditional product costing (a) In the context of activity-based costing (ABC), it was stated in Management Account- ing-Evolution not Revolution by Bromwich and Bhimani, that 'Cost drivers attempt to link costs to the scope of output rather than the scale of output thereby

Comparison of traditional product costing with ABC Duo plc produces two products A and B. Each has two components specified as sequentially numbered parts i.e. product A (parts 1 and 2) and product B (parts 3 and 4). Two production depart- ments (machinery and fitting) are supported by five service

Showing 2100 - 2200

of 5081

First

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

Last

Step by Step Answers