New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management accounting

Management Accounting 3rd Edition Anthony A. Atkinson, Robert S. Kaplan, S. Mark Young, Rajiv D. Banker, Pajiv D. Banker - Solutions

Profit sharing Peterborough Medical Devices makes devices and equipment that it sells to hospitals. The organization has a profit-sharing plan that is worded as follows:The company will make available a profit-sharing pool that will be the lower of the following two items:1. 40% of net income

Gamsharing Lindsay Cereal Company manufactures a line of breakfast cere¬ als. The production workers are part of a gainsharing program that works as follows. A target level of labor costs is set based on the achieved level of pro¬ duction. If the actual level of labor costs is less than the

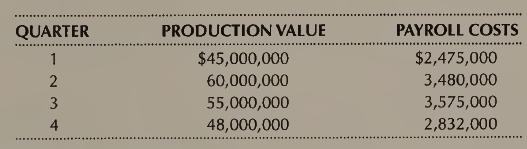

Scanlon plan Bathurst Company manufactures household paper products. LO 6 During a recent quarter, the value of the products made was $50 million and the labor costs were $3 million. The company has decided to use a Scanlon plan with this quarter being used to establish the base ratio for the

Characteristics of MACS design: ethical issues You are a management ac- LO 4 countant working in the controller's office. Rick Koch, a very powerful execu¬ tive, approaches you in the parking lot and asks you to do him a favor. The favor involves falsifying some of his division's records on the

Designing a balanced scorecard The following exhibit appeared in Weirton LO 5 Steel Corporation's 1990 annual report:We are bound together in these common beliefs and values. We must . . .For the Customer 1. Have a total quality commitment to consistently meet the product, deliv¬ ery, and service

Developing a balanced scorecard for a university Develop a balanced scorecard that the dean or director of your school may use to evaluate the school's operations. Be specific and indicate the purpose of each balanced scorecard measure.LO1

Choosing what to reward During the late 1970s, Harley-Davidson, the mo¬ torcycle manufacturer, was losing money and was very close to bankruptcy. Management believed that one of the problems was low productivity and, as a result, asked middle managers to speed up production. The employees who made

Characteristics of MACS design: participation vs. imposition Denver Jack's is a large toy manufacturer. The company has 100 highly trained and skilled employees who are involved with six major product lines, including the pro¬ duction of toy soldiers, dolls, etc. Each product line is manufactured

Evaluating a compensation plan Beau Monde, Inc., a manufacturer tributor of health and beauty products, made the following disclosu its compensation program:and dis- re about 432 Chapter 10 Our compensation philosophy is based on two simple principles: (1) we pay for performance; and (2) management

The mix of salary and commission Belleville Fashions sells high-quality LO 6 women's, men's, and children's clothing. The store employs a sales staff of 11 full-time people and 12 part-time people. Until recently, all sales staff were paid a flat salary and participated in a profit-sharing plan

Distributing a bonus pool Four broad approaches to distributing the pro¬ceeds of a bonus pool in a profit-sharing plan are listed below.(1) Each person's share is based on salary.(2) Each person receives an equal share.(3) Each person's share is based on position in the organization (larger pay¬

Characteristics of MACS design: types of information Chow Company is an insurance company in Hong Kong. Chow hires 55 people to process insur¬ ance claims. The volume of claims is extremely high and all claims examiners are kept extremely busy. The number of claims that have mistakes runs about

Implementing the balanced scorecard Find either by visiting a site or from a description in a published article a description of the implementation of a bal¬ anced scorecard.REQUIRED(a) Document in detail the elements of the balanced scorecard.(b) Identify the purpose of each balanced scorecard

Rewarding long-term performance In 1983, Johnson Controls Inc. devel- LO 6 oped a seven-year performance plan for two of their most senior-level execu¬ tives. In each of the seven years, the base amount of the plan (consisting of $300,000 and $100,000 for the two executives, respectively) is

Outline: (a) the objectives of budgetary planning and control systems; of a master budget. (b) the organization required for the preparation (7 marks) (10 marks) (Total 17 marks)

The preparation of budgets is a lengthy process which requires great care if the ultimate master budget is to be useful for the purposes of manage- ment control within an organization. You are required: (a) to identify and to explain briefly the stages involved in the preparation of budgets identi-

You are the management accountant of a group of companies and your managing director has asked you to explore the possibilities of introducing a zero-base budgeting system experimentally in one of the operating companies in place of its existing orthodox system. You are required to prepare notes

The chief executive of your organization has recently seen a reference to zero-base budgeting. He has asked for more details of the technique. You are required to prepare a report for him explaining: (a) what zero-base budgeting is and to which areas it can best be applied; (b) what advantages the

(a) corporate planning and budgeting are complementary, rather than the former super- seding the latter.' Compare the aims and main features of 'corporate planning' and 'budgeting' systems. (12 marks) (b) The aims of zero-base budgeting have been described recently in the following terms:

A budgetary planning and control system may include many individual budgets which are inte- grated into a 'master budget'. You are required to outline and briefly explain with reasons the steps which should normally be taken in the preparation of master budgets in a manufacturing company,

Traditional budgeting systems are incremental in nature and tend to focus on cost centres. Activity based budgeting links strategic planning to overall performance measurement aiming at continuous improvement. (a) Explain the weaknesses of an incremental budgeting system. (5 marks) (b) Describe the

Preparation of functional budgets D Limited is preparing its annual budgets for the year to 31 December 2001. It manufactures and sells one product, which has a selling price of 150. The marketing director believes that the price can be increased to 160 with effect from 1 July 2001 and that at this

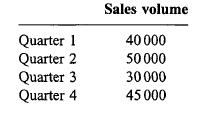

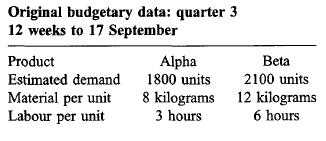

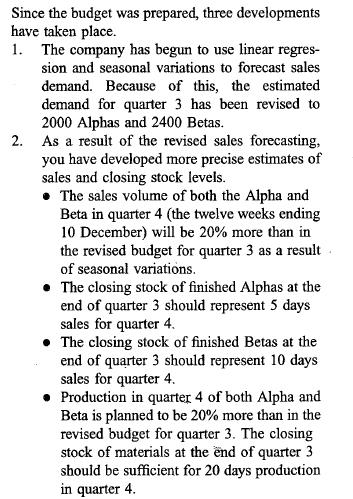

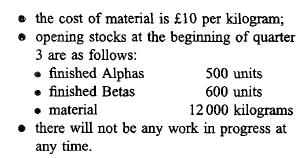

Preparation of functional budgets Data Wilmslow Ltd makes two products, the Alpha and the Beta. Both products use the same material and labour but in different amounts. The company divides its year into four quarters, each of twelve weeks. Each week consists of five days and each day comprises 7

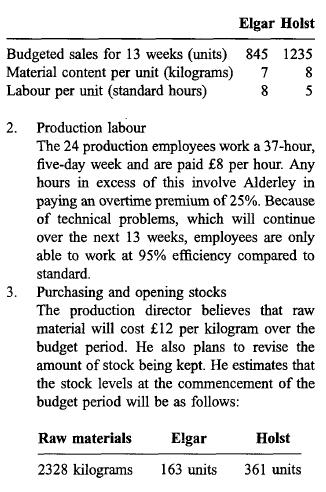

Budget preparation and comments on sales forecasting methods You have recently been appointed as the manage- ment accountant to Alderley Ltd, a small company manufacturing two products, the Elgar and the Holst. Both products use the same type of material and labour but in different proportions. In

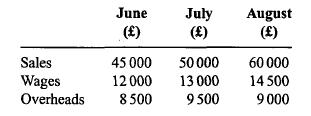

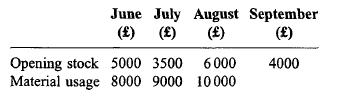

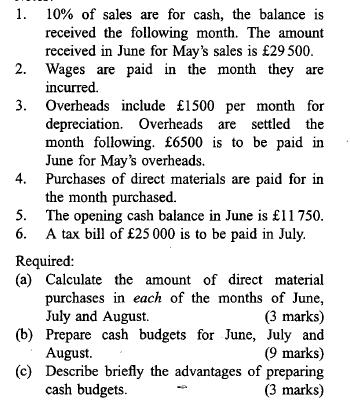

Preparation of cash budgets The following data and estimates are available for ABC Limited for June, July and August.The following information is available regarding direct materials: June July () () August () Sales Wages Overheads 45 000 50 000 60 000 12000 13.000 14 500 8500 9500 9000

Preparation of cash budgets The management of Beck plc have been informed that the union representing the direct production workers at one of their factories, where a standard product is produced, intends to call a strike. The accountant has been asked to advise the manage- ment of the effect the

The Victoria Hospital is located in a holiday resort that attracts visitors to such an extent that the population of the area is trebled for the summer months of June, July and August. From past experience, this influx of visitors doubles the activity of the hospital during these months. The annual

The Viking Smelting Company established a division, called the reclamation division, two years ago, to extract silver from jewellers' waste materials. The waste materials are processed in a furnace, enabling silver to be recovered. The silver is then further processed into finished products by

Outline the main features of a responsibility accounting system. (6 marks)

(a) Budgetary controls have been likened to a system of thermostatic control. priate? (i) In what respects is the analogy inappro- (10 marks) (ii) What are the matters raised in (a) (i) above that need to be considered when setting a structure for an effective budgetary control system? (8 marks)

One common approach to organisational control theory is to look at the model of a cybernetic system. This is often illustrated by a diagram of a thermostat mechanism. You are required: (a) to explain the limitations of the simple feed- back control this model illustrates, as an explanation of the

(a) In the context of budgeting, provide defini- tions for four of the following terms:aspiration level; budgetary slack; feedback; zero-base budgeting; responsibility accounting. (8 marks) (b) Discuss the motivational implications of the level of efficiency assumed in establishing a budget. (9

You are required, within the context of budgetary control, to: (a) explain the specific roles of planning, motiva- tion and evaluation; (7 marks) (b) describe how these roles may conflict with each other; (c) give three examples of ways by management accountant may conflict described in (b). (7

(a) Explain the ways in which the attitudes and behaviour of managers in a company are liable to pose more threat to the success of its budgetary control system than are minor technical inadequacies that may be in the system. (15 marks)(b) Explain briefly what the management accoun- tant can do to

What are the behavioural aspects which should be bome in mind by those who are designing and operating standard costing and budgetary control systems? (20 marks)

In his study of 'The Impact of Budgets on People', published in 1952, C. Argyris reported inter alia the following comment by a financial controller on the practice of participation in the setting of budgets in his company: 'We bring in the supervisors of budget areas, we tell them that we want

You are required to: (i) discuss the factors that are likely to cause managers to submit budget estimates of sales and costs that do not represent their best estimates or expectations of what will actually occur, (8 marks) (ii) suggest, as a budget accountant, what pro- cedures you would advise in

The typical budgetary control system in practice does not encourage goal congruence, contains budgetary slack, ignores the aspiration levels of participants and attempts to control operations by feedback, when feedforward is likely to be more effective; in summary the typical budgetary control

Flexible budgets and the motivational role of budgets Club Atlantic is an all-weather holiday complex providing holidays throughout the year. The fee charged to guests is fully inclusive of accommoda- tion and all meals. However, because the holiday industry is so competitive, Club Atlantic is only

Criticism and redrafting of a performance report (a) The following report has been prepared, relat- ing to one product for March. This has been sent to the appropriate product manager as part of PDC Limited's monitoring procedures.The product manager has complained that the report ignores the

Preparation of flexible budgets Data Rivermede Ltd makes a single product called the Fasta. Last year, Steven Jones, the managing direc- tor of Rivermede Ltd, attended a course on budget- ary control. As a result, he agreed to revise the way budgets were prepared in the company. Rather than

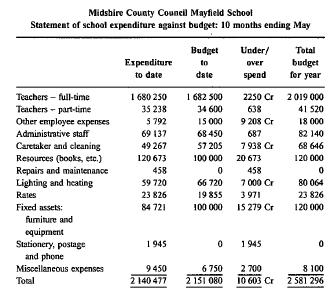

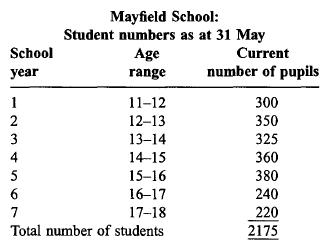

Responsibility centre performance reports Data Jim Smith has recently been appointed as the Head Teacher of Mayfield School in Midshire. The age of the pupils ranges from 11 years to 18 years. For many years, Midshire County Council was respon- sible for preparing and reporting on the school

BS Limited manufactures one standard product and operates a system of variance accounting using a fixed budget. As assistant management accountant, you are responsible for preparing the monthly operating statements. Data from the budget, the standard product cost and actual data for the month ended

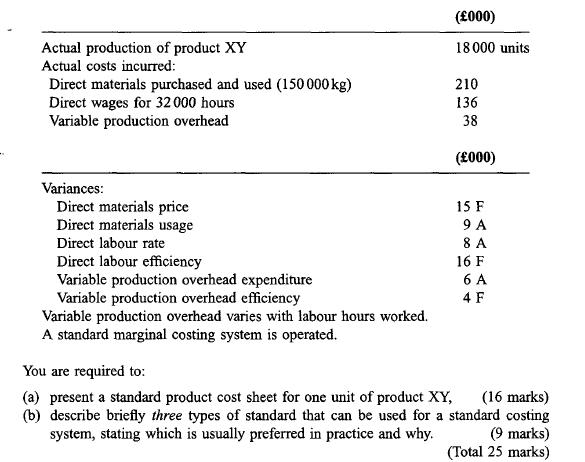

The following data relate to actual output, costs and variances for the four-weekly accounting period number 4 of a company that makes only one product. Opening and closing work in progress figures were the same. (000) 18000 units Actual production of product XY Actual costs incurred: Direct wages

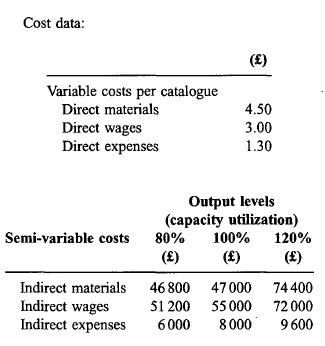

Preparation of project statements for different demand levels and calculations of expected profit Seeprint Limited is negotiating an initial one year contract with an important customer for the supply of a specialized printed colour catalogue at a fixed contract price of 16 per catalogue.

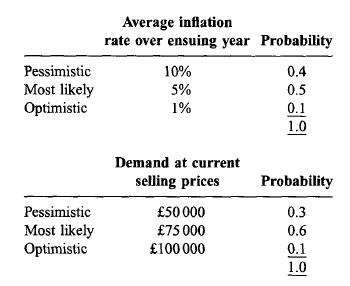

CVP analysis and uncertainty (a) The accountant of Laburnum Ltd is preparing documents for a forthcoming meeting of the budget committee. Currently, variable cost is 40% of selling price and total fixed costs are 40000 per year. The company uses an historical cost accounting system. There is

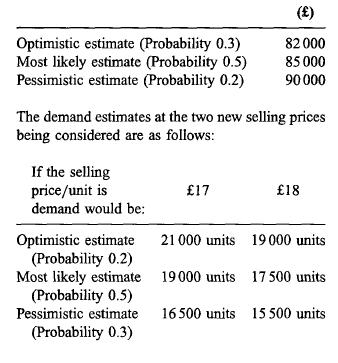

Pricing decision and the calculation of expected profit and margin of safety E Ltd manufactures a hedge-trimming device which has been sold at 16 per unit for a number of years. The selling price is to be reviewed and the following information is available on costs and likely demand. The standard

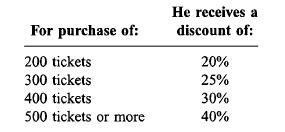

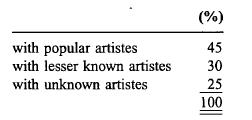

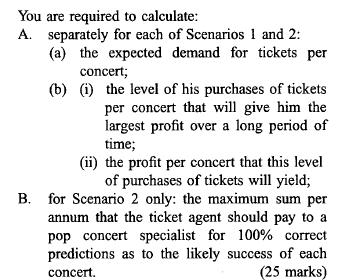

Output decision based on expected values A ticket agent has an arrangement with a concert hall that holds pop concerts on 60 nights a year whereby he receives discounts as follows per concert:Purchases must be in full hundreds. The average price per ticket is 3. He must decide in advance each year

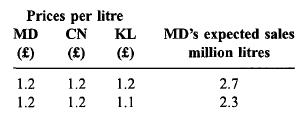

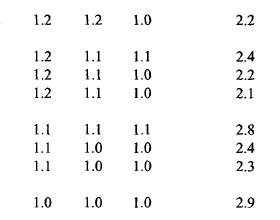

Pricing decision based on competitor's response In the market for one of its products, MD and its two major competitors (CN and KL) together account for 95% of total sales. The quality of MD's products is viewed by customers as being somewhat better than that of its competitors and therefore at

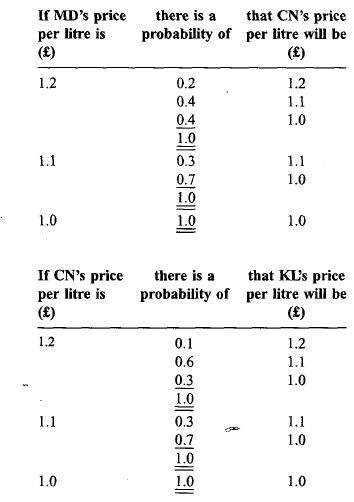

Expected value, maximin and regret criterion Stow Health Centre specialises in the provision of sports/exercise and medical/dietary advice to clients. The service is provided on a residential basis and clients stay for whatever number of days suits their needs. Budgeted estimates for the next year

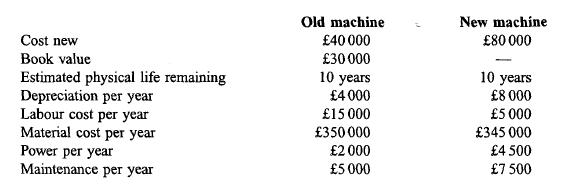

A company is preparing its capital budget for the year. A question has arisen as to whether or not to replace a machine with a new and more efficient machine. An analysis of the situation reveals the following based on operations at a normal level of activity.The expected scrap value of both the

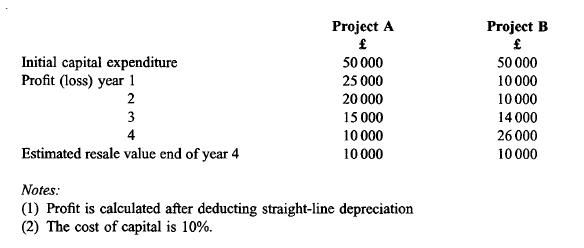

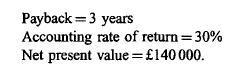

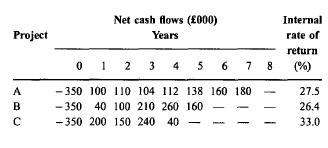

The following data is supplied relating to two investment projects, only one of which may be selected:Required: (a) Calculate for each project: (i) average annual rate of return on average capital invested; (ii) payback period; (iii) net present value. (12 marks) (b) Briefly discuss the relative

A machine with a purchase price of 14000 is estimated to eliminate manual operations costing 4000 per year. The machine will last five years and have no residual value at the end of its life. You are required to calculate: (a) the discounted cash flow (DCF) internal rate of return; (b) the level of

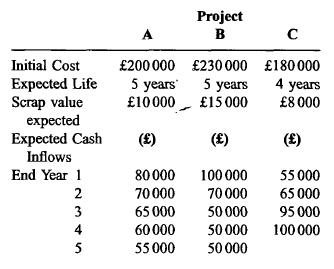

Payback, accounting rate of return and NPV calculations plus a discussion of qualitative factors The following information relates to three possible capital expenditure projects. Because of capital rationing only one project can be accepted.The company estimates its cost of capital is 18%.

Discussion of alternative investment appraisal techniques and the calculation of payback and NPV for two mutually exclusive projects (a) Explain why Net Present Value is considered technically superior to Payback and Account- ing Rate of Return as an investment appraisal technique even though the

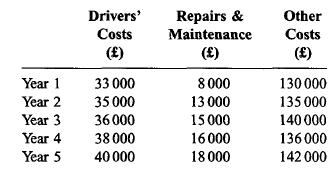

Calculation of payback, NPV and ARR for mutually exclusive projects Your company is considering investing in its own transport fleet. The present position is that carriage is contracted to an outside organization. The life of the transport fleet would be five years, after which time the vehicles

NPV and payback calculations You are employed as the assistant accountant in your company and you are currently working on an appraisal of a project to purchase a new machine. The machine will cost 55 000 and will have a useful life of three years. You have already esti- mated the cash flows from

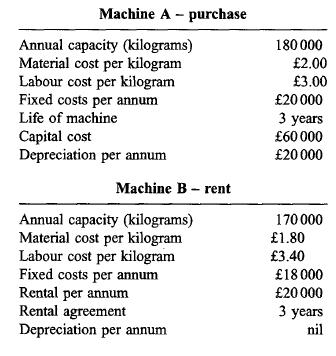

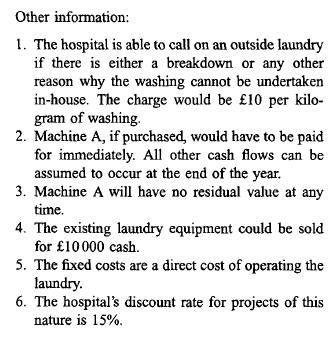

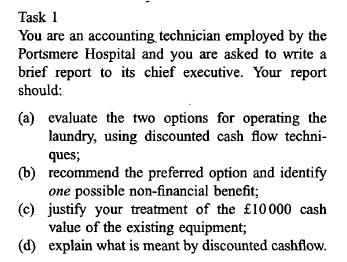

Present value of purchasing or renting machinery The Portsmere Hospital operates its own laundry. Last year the laundry processed 120 000 kilograms of washing and this year the total is forecast to grow to 132000 kilograms. This growth in laundry processed is forecast to continue at the same

Comparison of NPV and IRR and relationship between profits and NPV Khan Ltd is an importer of novelty products. The directors are considering whether to introduce a new product, expected to have a very short economic life. Two alternative methods of promot- ing the new product are available,

Evaluation of mutually exclusive projects using alternative appraisal methods Stadler is an ambitious young executive who has recently been appointed to the position of financial director of Paradis plc, a small listed company. Stadler regards this appointment as a temporary one, enabling him to

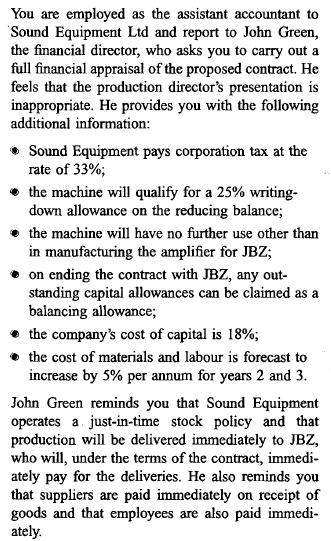

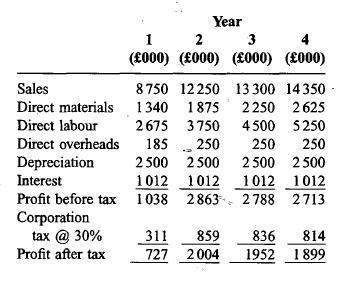

Computation of NPV and tax payable Sound Equipment Ltd was formed five years ago to manufacture parts for hi-fi equipment. Most of its customers were individuals wanting to assemble their own systems. Recently, however, the company has embarked on a policy of expansion and has been approached by

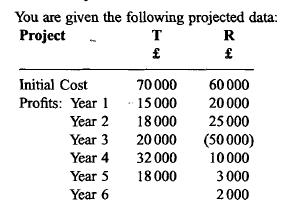

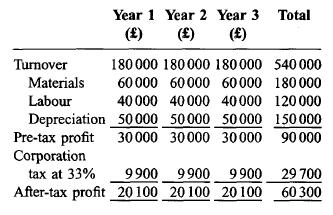

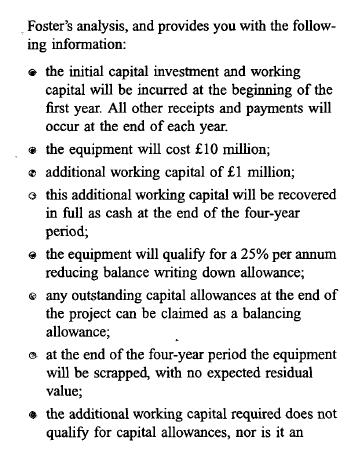

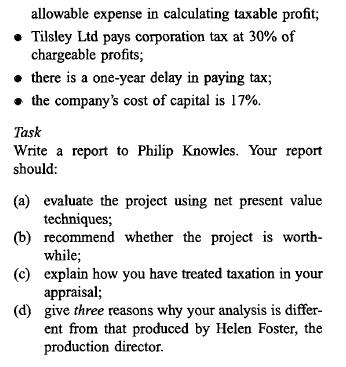

NPV calculation and taxation Data Tilsley Ltd manufactures motor vehicle com- ponents. It is considering introducing a new product. Helen Foster, the production director, has already prepared the following projections for this proposal:Helen Foster has recommended to the board that the project is

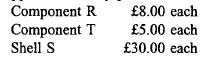

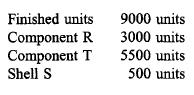

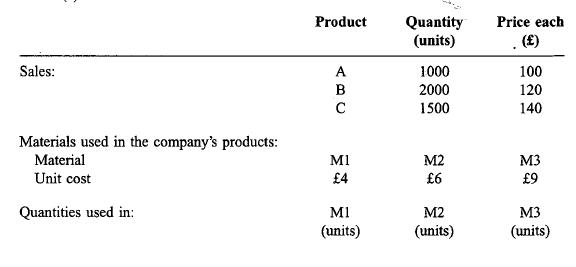

R Limited manufactures three products A, B and C. You are required: (a) Using the information given below, to prepare budgets for the month of January for (i) sales in quantity and value, including total value; (ii) production quantities; (iii) material usage in quantities; (iv) material purchases

understand how traditional cost systems, using only unit- level drivers, distort product and customer costs LO1

describe why factories producing a more varied and complex mix of products have higher costs than factories producing only a narrow range of products LO1

design an activity-based cost system by linking resource costs to the activities performed and then to cost objects, such as products and customers LO1

appreciate the role for choosing appropriate activity cost drivers when tracing activity costs to products and customers LO1

use the information from a well-designed activity-based cost system to improve operations and make better decisions about products and customers LO1

understand the importance of measuring the practical capacity of resources and the cost of unused capacity LO1

assign marketing, distribution, and selling expenses to customers LO1

analyze customer profitability LO1

appreciate the role for activity-based cost systems for service companies LO1

discuss the barriers for implementing activity-based cost systems and how these might be overcome LO1

What is the difference between production de¬ partments and service departments? (LO 1)

What are the two stages of cost allocations in conventional product costing systems? (LO 1)

Why are conventional two-stage cost allocation systems likely to systematically distort product costs? (LO 1, 2)5.4 What are two factors that contribute to cost dis¬ tortions resulting from the use of conventional, two-stage cost allocation systems? (LO 1, 2)

What fundamental assumption implicit in conventional two-stage cost allocation systems is rejected in activity-based costing systems? (LO 1, 2)

What do the terms activity cost driver and ac¬ tivity cost driver rates mean? (LO 3)

What major steps must be performed to deter¬ mine the activity cost driver rates? (LO 3, 4)

What are some special considerations in the design of cost accounting systems for service organizations? (LO 9)

When would you prefer to use the number of setups instead of the number of setup hours as the cost driver measure for the setup activity? (LO 4)

How do activity-based costing systems avoid distortions in tracing batch-related costs to products? (LO 3, 4)

Why do conventional product costing systems often exclude selling and distribution costs? (LO 1, 7)

What recent changes have made it more impor¬ tant to have nonmanufacturing costs assigned to products, product lines, or market segments? (LO 5, 7, 8)

Why are conventional product costing systems more likely to distort product costs in highly automated plants? How do activity-based cost¬ ing systems deal with such a situation? (LO 2)Activity-Based Cost Management Systems 191

"Conventional product costing systems are likely to overcost high-volume products." Do you agree with this statement? Explain. (LO 1, 2, 3)

How are cost drivers selected in activity-based costing systems? (LO 4)

In activity-based costing, what are the trade-offs made in choosing among transaction, duration, and intensity activity cost drivers? (LO 4)

Why is practical capacity recommended in cal¬ culating activity cost driver rates? (LO 6)

"Activity-based costing systems yield more ac¬ curate product costs than conventional systems because they use more cost drivers to assign support costs to products." Do you agree with this statement? Explain. (LO 3, 4)

Activity cost drivers Identify a cost driver for each of the following activities:(a) Machine maintenance(b) Machine setup(c) Utilities(d) Quality control(e) Material ordering(f) Production scheduling(g) Factory depreciation(h) Warehouse expense(i) Production supervision(j) Payroll accounting(k)

Revising an activity-based costing system Refer to the Cooper Pen example de¬scribed in the chapter. Suppose that some unrecorded resource expenses were just discovered at Cooper Pen. Inspection people costing $15,000 per quarter perform quality inspections at the start of each new production run

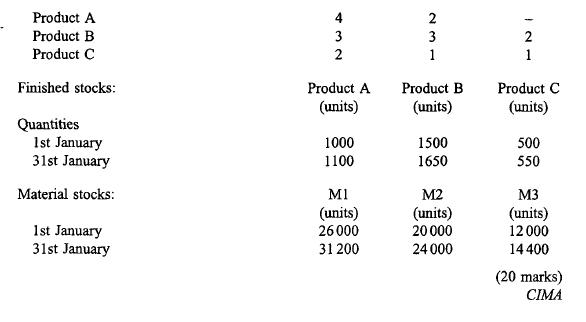

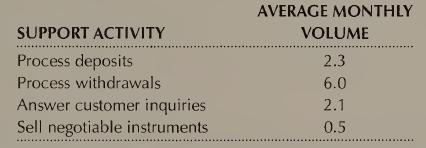

Activity-based costs Friendly Bank is developing an activity-based cost system for its teller department. A task force has identified five different activities: (1) process deposits, (2) process withdrawals, (3) answer customer inquiries, (4) sell negotiable instruments, and (5) balance drawers. By

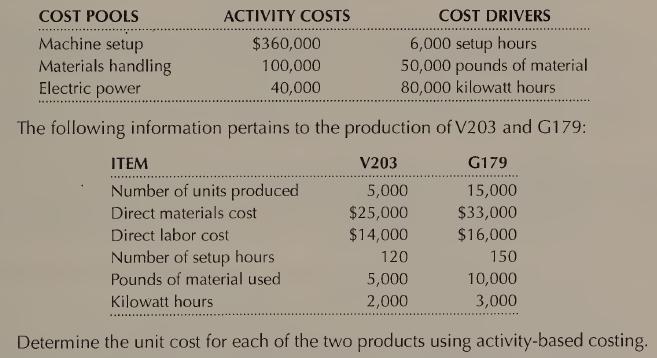

Activity-based costs VG Company has identified the following cost pools and cost drivers: COST POOLS Machine setup Materials handling Electric power ACTIVITY COSTS $360,000 100,000 40,000 COST DRIVERS 6,000 setup hours 50,000 pounds of material 80,000 kilowatt hours The following information

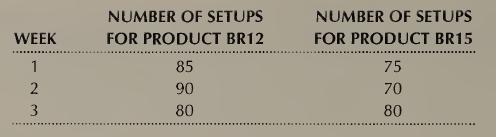

Activity cost driver rates Creathon Company's plant in Columbus, Ohio, manu¬ factures two products: BR12 and BR15. Product BR15 has a more complex de¬ sign and requires more setup time than BR12.Setups for BR12 require two hours on average; setups for BR15 require three hours. Creathon's setup

Carl's Cornerspot, a popular university eatery in a competitive market, has seat¬ing and staff capacity to serve about 600 lunch customers every day. For the past two months, demand has fallen from its previous near-capacity level. Concerned about his declining profit, Carl decided to take a

Customer profitability A credit card company has classified its customers into the following types for customer profitability analysis:1. Applies for credit card in response to a low introductory interest rate; transfers balance to new account, but when the low introductory rate expires, the cus¬

Refer to the Inkslinger, Inc. situation described in the "In Practice" box on page LO 10 185. What barriers to implementing an activity-based costing system can you identify? How would you respond to the managers' comments?

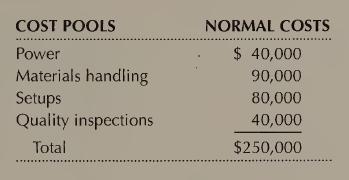

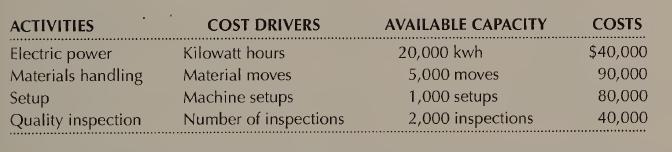

Comparison of two costing systems Normal manufacturing support costs of LO 1,3 Mclnnes Company for September 2000 are as follows:The present cost accounting system allocates support costs to final products based on machine hours. Estimated machine hours for September 2000 are 50,000. After losing

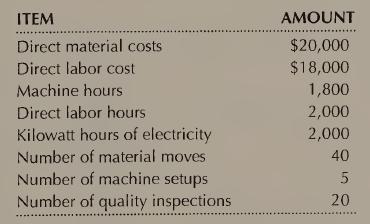

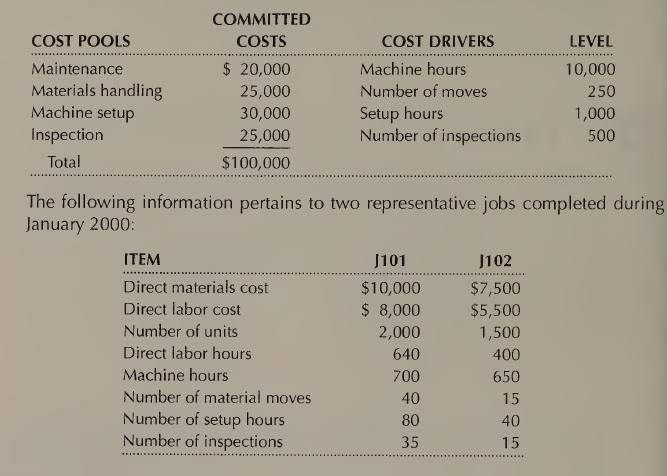

Cost distortions Ferreira Company has established the following cost pools for 2000:REQUIRED (a) Determine the unit cost of each job using machine hours to allocate all sup¬ port costs.(b) Determine the unit cost of each job using activity-based costing.(c) Which of the two methods produces more

Showing 2000 - 2100

of 5081

First

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Last

Step by Step Answers