New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

management accounting

Management Accounting 3rd Edition Anthony A. Atkinson, Robert S. Kaplan, S. Mark Young, Rajiv D. Banker, Pajiv D. Banker - Solutions

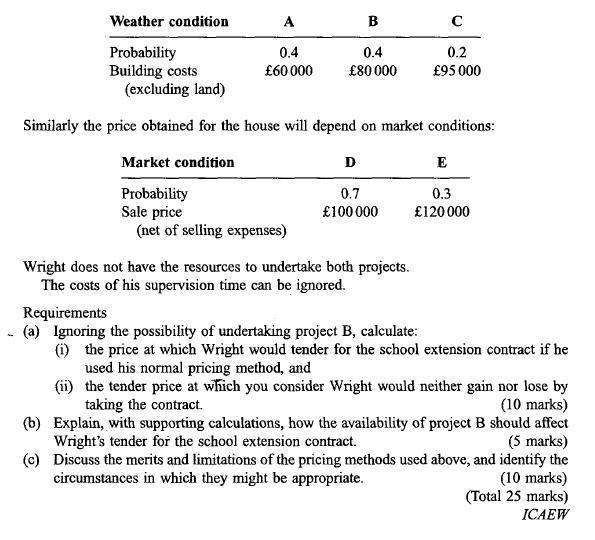

Wright is a builder. His business will have spare capacity over the coming six months and he has been investigating two projects. Project A Wright is tendering for a school extension contract. Normally he prices a contract by adding 100% to direct costs, to cover overheads and profit. He calculates

Discuss the extent to which cost data is useful in the determination of pricing policy. Explain the advantages and disadvantages of presenting cost data for possible utilization in pricing policy deter- mination using an absorption, rather than a direct, costing basis. (14 marks)

'In providing information to the product manager, the accountant must recognize that decision- making is essentially a process of choosing between competing alternatives, each with its own combination of income and costs; and that the relevant concepts to employ are future incre- mental costs and

It has been stated that companies do not have profitable products, only profitable customers. Many companies have placed emphasis on the concept of Customer Account Profitability (CAP) analysis in order to increase their earnings and returns to shareholders. Much of the theory of CAP draws from the

Discussion of pricing strategies A producer of high quality executive motor cars has developed a new model which it knows to be very advanced both technically and in style by comparison with the competition in its market segment. The company's reputation for high quality is well-established and its

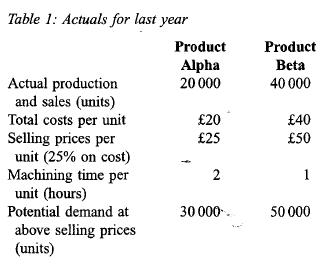

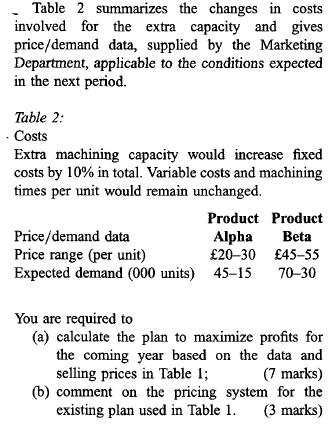

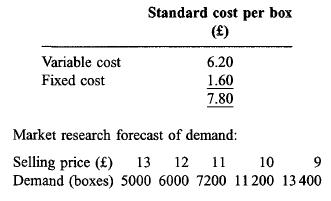

Limiting factor analysis and a discussion of cost-plus pricing AB p.l.c. makes two products, Alpha and Beta. The company made a 500 000 profit last year and proposes an identical plan for the coming year. The relevant data for last year are summarized in Table 1.Fixed costs were 480 000 for the

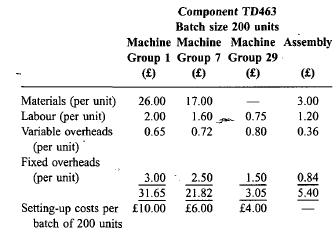

Computation of minimum selling price and optimum price from price-demand relationships In an attempt to win over key customers in the motor industry and to increase its market share, BIL Motor Components plc has decided to charge a price lower than its normal price for component TD463 when selling

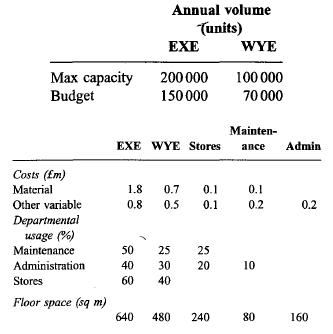

Calculation of cost-plus selling price and an evaluation of pricing decisions A firm manufactures two products EXE and WYE in departments dedicated exclusively to them. There are also three service departments, stores, maintenance and administration. No stocks are held as the products deteriorate

Cost-plus and relevant cost information for pricing decisions Josun plc manufactures cereal based foods, includ- ing various breakfast cereals under private brand labels. In March the company had been approached by Cohin plc, a large national supermarket chain, to tender for the manufacture and

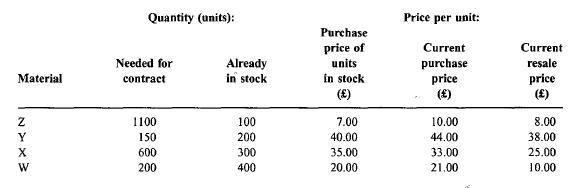

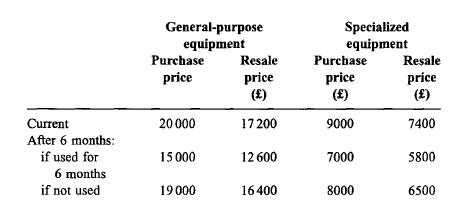

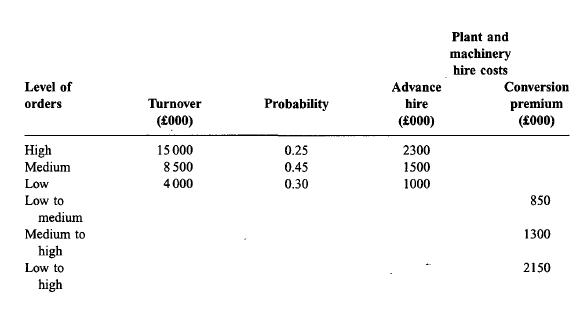

Siteraze Ltd is a company which engages in site clearance and site preparation work. Information concerning its operations is as follows: (i) It is company policy to hire all plant and machinery required for the implementation of all orders obtained, rather than to purchase its own plant and

Why are costs estimated for individual jobs? (LO 1, 2)

What information is presented in a typical job bid sheet? (LO 1, 2)

What is the source of the information to esti¬ mate the cost of materials? (LO 1, 2)

What is the source of the information to esti¬ mate the direct labor cost? (LO 1, 2)

How are support cost driver rates determined? (LO 1, 2)

How is support cost estimated for individual jobs? (LO 1, 2)

What is the markup rate? On what factors does it depend? (LO 1, 2)

What is a cost pool? Why are multiple cost pools required? (LO 3)

What problem arises when cost driver rates are based on planned or actual short-term usage instead of normal usage? Why? (LO 3)

What is the normal cost of a support activity? What is the normal usage level of a cost driver? (LO 3)

What are cost pools? How is the appropriate number of cost pools selected? (LO 5)

What is the managerial use of tracking actual costs of individual jobs? (LO 5)RIALS

Why are predetermined cost driver rates used when recording actual job costs? (LO 5)

What does the term conversion costs mean? (LO 6)

What is the basic procedure for determining product costs in continuous processing plants? (LO 6)

What are the similarities and differences between job order costing and multistage process costing systems? (LO 7)

(Appendix) What is the difference between pro¬ duction departments and service departments? (LO 8)

(Appendix) What are the two stages of cost allo¬ cations in conventional product costing sys¬ tems? (LO 8)

(Appendix) Why do conventional product cost¬ ing systems allocate service department costs first to the production departments before assigning them to individual jobs? (LO 8)

(Appendix) What are the different situations for which direct, sequential, and reciprocal alloca¬ tion methods are designed? (LO 8)

(Appendix) Why are conventional two-stage cost allocation systems likely to systematically distort product costs? (LO 8)

(Appendix) What are two factors that contribute to cost distortions resulting from the use of conventional, two-stage cost allocation systems? (LO 8)

Job order costing, consulting McDonald Consulting computes the cost of each consulting engagement by adding a portion of firm-wide support costs to the labor cost of the consultants on the engagement. The support costs are assigned to each consulting engagement using a cost driver rate based on

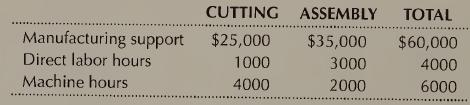

Single rate versus departmental rates Wright Wood Products has two produc¬ tion departments: cutting and assembly. The company has been using a single pre¬ determined cost driver rate based on plant-wide direct labor hours. That is, the plant-wide cost driver rate is computed by dividing

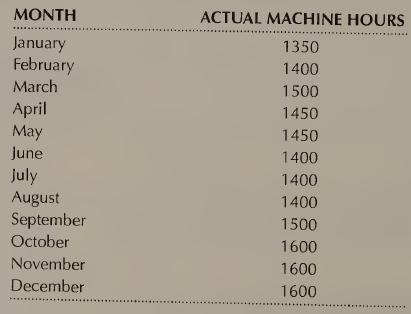

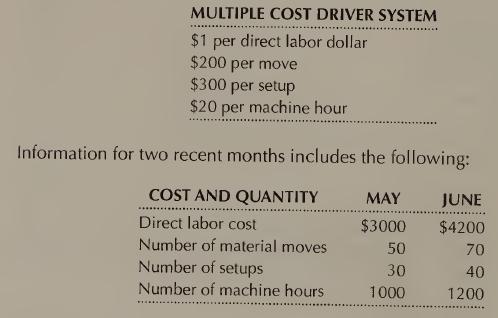

Fluctuating cost driver rates, effect on markup pricing Toki Company carefully records its costs because it bases prices on the cost of the goods it manufactures. Toki also carefully records its machine usage and other operational information. Manufacturing costs are computed monthly and prices for

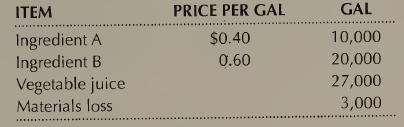

Process costs Health Foods Company produces and sells canned vegetable 10 6 juice. The ingredients are first combined in the blending department and then packed in gallon cans in the canning department. The following information per¬ tains to the blending department for January 2000.Conversion

Process costs Washington Chemical Company manufactures and sells Goody, a LOG product that sells for $10 per pound. The manufacturing process also yields one pound of a waste product called Baddy in the production of every 10 pounds of Goody. Disposal of the waste product costs $1 per pound. During

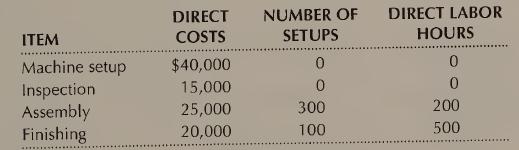

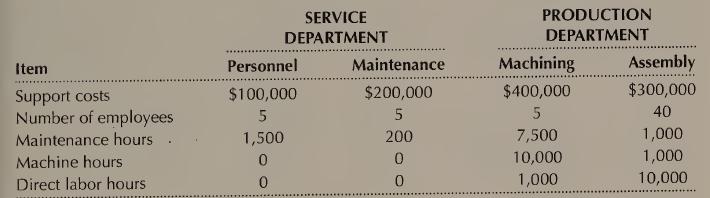

Service department cost allocation, direct method (Appendix) San Miguel LO 8 Company has two production departments, assembly and finishing, and two service departments, machine setup and inspection. Machine setup costs are allocated on the basis of number of setups while inspection costs are

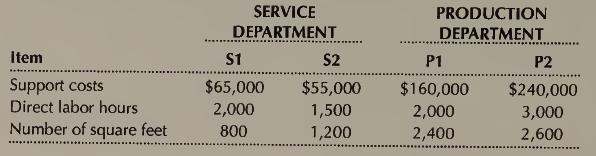

Sequential allocation (Appendix) Cooper Company has two service departments and two production departments. Information on annual manufacturing support costs and cost drivers follows:The company allocates service department costs using the sequential method. First, SI costs are allocated based on

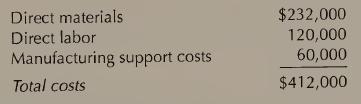

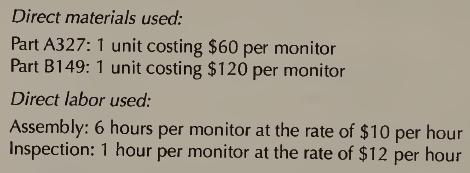

Job cost sheet Portland Electronics, Inc. delivered 1000 custom-designed com¬puter monitors on February 10 to its customer, Video Shack; they had been ordered on January 1. The following cost information was compiled in connection with this order:In addition, manufacturing support costs are

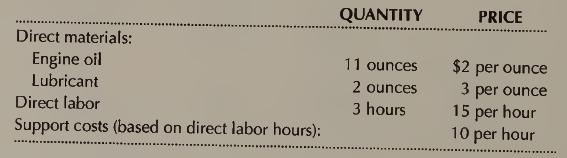

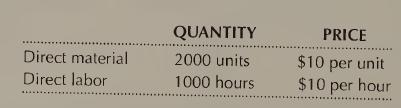

Job cost sheet The following costs pertain to job 379 at Baker Auto Shop.Prepare a job cost sheet for Baker Auto Shop. Direct materials: Engine oil Lubricant Direct labor Support costs (based on direct labor hours): QUANTITY PRICE 11 ounces $2 per ounce 2 ounces 3 per ounce 3 hours 15 per hour 10

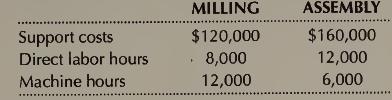

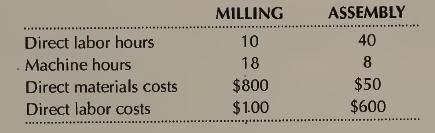

Job cost sheet, markup> single rate versus departmental rates Duluth Metal¬works Company has two departments, milling and assembly. The company uses a job costing system that employs a single, plant-wide support cost driver rate to apply support costs to jobs on the basis of direct labor hours.

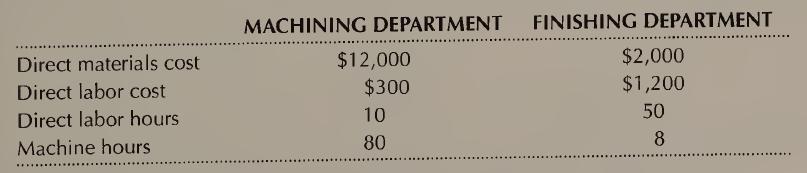

Job costing The Gonzalez Company uses a job order costing system at its Green Bay, Wisconsin, plant. The plant has a machining department and a finishing department. The company uses two cost driver rates for allocating manufacturing support costs to job orders: one on the basis of machine hours

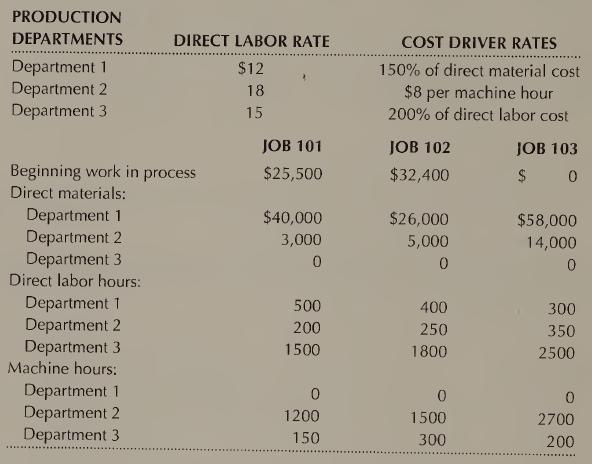

Job costing The Goldstein Company employs a job order cost system to account for its costs. There are three production departments. Separate departmental cost driver rates are employed because the demand for support activities for the three departments is very different. All jobs generally pass

Job costs and bids; comparing actual and estimated costs Brumelle Electronic Company manufactures a variety of electronic components. In April 2000, the company received an invitation from Takayama, Inc. to bid on an order of 1000 units of component ICB371 that must be delivered by August 16, 2000.

Job bid sheet, direct and sequential allocations (Appendix) Sanders Manufacturing LO 1, 2, 3, 8 Company produces electronic components on a job order basis. Most business is gained through bidding on jobs. Most firms competing with Sanders bid full cost plus a 30% markup. Recently, with the

Direct, sequential, and reciprocal allocation (Appendix) Boston Box Company has two service departments, maintenance and grounds, and two production departments, fabricating and assembly. Management has decided to allocate maintenance costs on the basis of machine hours used by the departments

Single rate versus departmental rates Bravo Steel Company supplies structural steel products to the construction industry. Its plant has three production depart¬ ments: cutting, grinding, and drilling. The estimated support activity cost and direct labor and machine hour levels for each

Charging for service activity costs Airporter Service Company operates sched¬uled coach service from Boston's Logan Airport to downtown Boston and to Cam¬ bridge. A common scheduling service center at the airport is responsible for ticketing and customer service for both routes. The service

Job bid price, direct, sequential, and reciprocal allocations (Appendix) Sherman LO 1, 2, 3, 8 Company manufactures and sells small pumps made to customer specifications. It has two service departments and two production departments. Information on March 2000 operations follows:Separate cost

Alternative job costing systems Over the past 15 years, Anthony's Autoshop LO 1,2,3, has developed a reputation for reliable repairs and has grown from a one- 4, 5 person operation to a nine-person operation including one manager and eight skilled auto mechanics. In recent years, however,

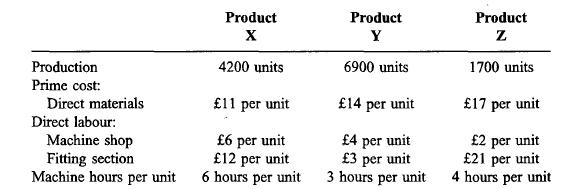

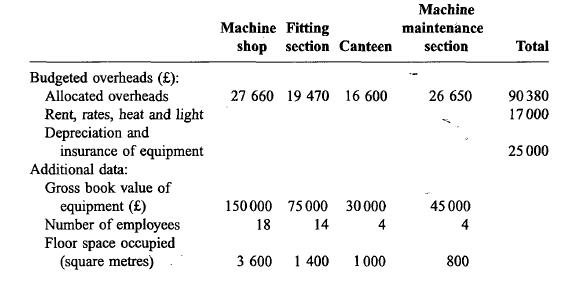

Bookdon Public Limited Company manufactures three products in two production departments, a machine shop and a fitting section; it also has two service departments, a canteen and a machine maintenance section. Shown below are next year's budgeted production data and manufacturing costs for the

Shown below is next year's budget for the forming and finishing departments of Tooton Ltd. The departments manufacture three different types of component, which are incorporated into the output of the firm's finished products.The forming department is mechanized and employs only one grade of

What are some different uses of cost informa¬ tion? (LO 1)

Why do different types of cost information need to be reported to support different managerial purposes and decisions? (LO 1)

What is a cost object? (LO 1)

How is it possible to distinguish direct costs from indirect costs? (LO 1)

Explain the difference between flexible costs and capacity-related costs. (LO 3)

Are flexible costs always direct costs? (LO 1, 3)

Are capacity-related costs always indirect costs? (LO 1, 3)

How are costs in a manufacturing firm classi¬ fied for external reporting? (LO 1, 3)

Describe the difference between costs and ex¬ penses. (LO 1, 3)

What are the two principal categories into which manufacturing costs are classified? (LO 1, 3)

What are six categories of costs, classified by function, that are included in nonmanufactur¬ ing costs for external reporting? (LO 1, 3)

Why do traditional cost accounting systems tend to analyze manufacturing costs in greater detail than they do other functional categories of costs? (LO 1, 3)

What are two broad purposes for which costs are used inside an organization? (LO 1)

Explain why you agree or disagree with the fol¬ lowing statement: "An organization should have the most accurate and complete cost sys¬ tem possible." (LO 1)

What is an opportunity cost? (LO 1, 4)

What is the distinction between short run costs and long run costs? (LO 2, 3)

How has the composition of manufacturing costs changed in recent years? How has this change affected the design of cost accounting systems? (LO 1, 3)

What are the five categories of production ac¬ tivities? Explain the differences among them (LO 1, 3)

Why have customer-related costs attracted in¬ creasing attention in recent years? (LO 1, 3)

What are the five stages in a typical product's life cycle? What is the cost focus in each staee?(1.0 5)

Cost classification by function Classify each of the following costs as manufac¬ turing or nonmanufacturing. Further classify nonmanufacturing costs as distribu¬ tion, selling, marketing, after-sales, research and development, or general and administrative costs.(a) Direct labor(b) Sales

Components of manufacturing costs Classify each of the following manufactur¬ ing costs as direct or indirect for products.(a) Insurance on manufacturing equipment(b) Steel plates used in making an automobile body(c) Wages of assembly workers(d) Salaries of plant security personnel(e) Rubber used

Cost classification by activity type Classify the following costs as unit-related, batch-related, product-sustaining, or business-sustaining activity costs.(a) Direct materials(b) Setup labor wages(c) Salaries of plant engineers responsible for executing engineering change orders(d) Building

Cost classification by activity type Classify the following costs as unit-related, batch-related, product-sustaining, or business-sustaining activity costs.(a) Packing labor wages(b) Materials-handling labor wages(c) Part administrators'salaries(d) Plant management salaries(e) Production scheduling

Classification of flexible and capacity-related costs Classify each of the follow¬ ing as a flexible or capacity-related cost.(a) Salaries of production supervisors(b) Steel used in automobile production(c) Wood used in furniture production(d) Charges for janitorial services(e) Commissions paid to

Classification of flexible and capacity-related costs Classify each of the follow¬ ing as a flexible or capacity-related cost.(a) Paper used in newspaper production(b) Wages of production workers(c) Salary of the chief executive officer(d) Glue used in furniture production(e) Depreciation of

Customer-related costs Nehls Company is concerned about its growing cus¬ tomer-related expenses. The company currently allocates customer capacity-104 Chapter 3 related support costs on the basis of revenues, at a rate of 30% of sales revenue. After discovering that ordering patterns vary quite

Cost classification The L.A. Dress Shop manufactures dresses and decorates LO!,3 them with custom designs for retail sales on the premises. The shop sold 5000 dresses last month. Costs incurred during the last month include the following:Apportion the rent into different categories based on the

Cost behavior, cost classifications Shannon O'Reilly is trying to decide whether to continue to take public transportation to work or to purchase a car. Before making her decision, she would like to compare the cost of using public trans¬ portation and the cost of driving a car.REQUIRED(a) What

Single drivers vs. multiple drivers Eagan Electrical Instruments Company esti¬mates manufacturing support as 950% of direct labor costs. Eagan's controller, Jim Becker, is concerned that the actual manufacturing support activity costs have differed substantially from the estimates in recent

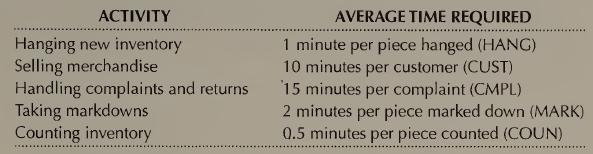

Planning activity workloads The Abby Corporation, a chain of department stores, estimates the standard workload at its retail outlets in terms of the time required for the activities of (1) hanging new inventory; (2) selling merchandise; (3) handling complaints, inquiries, and returns: (4) taking

Cost behavior and decisions Second City Airlines operates 35 scheduled round- trip flights between New York and Chicago each week. It charges a fixed one¬ way fare of $200 per passenger. Second City Airlines can carry 150 passengers per flight. Fuel and other flight-related costs are $5000 per

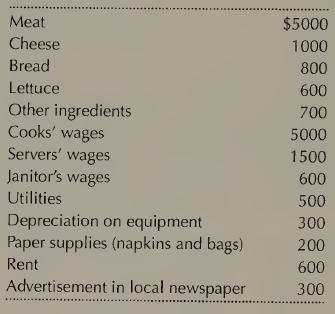

Cost classification Poker's is a small hamburger shop catering mainly to students at a nearby university, it is open for business from 11 a.m. until 11 p.m., Monday through Friday. The owner, Chip Poker, employs two cooks, one server, and a part-time janitor. Because there is no space for dining

Commitment and consumption of activity resources Classic Containers Com¬ pany specializes in making high-quality customized containers to order. Its agree¬ ment with the labor union ensures employment for all its employees and a fixed payroll of $80,000 per month including fringe benefits. This

Each job requires four labor hours for machine setup and 0.05 labor hours per container. Flexible costs comprise $1.60 per container for materials and $8.00 per labor hour for manufacturing support expenses. In addition, the firm must pay $20,000 per month for selling, general, and administrative

Commitment of activity resources Crown Cable Company provides cable tele- LO 1, 2, 3 vision service in the Richfield metropolitan area. The company hires only full¬ time service persons working 40 hours a week at $18 per hour including fringe benefits. Service persons handle additional service

Flexibility in committing activity resources Dr. Barbara Barker is the head of LO 1, 2, 3 the pathology laboratory at Barrington Medical Center in Mobile, Alabama.Dr. Barker estimates the amount of work for her laboratory staff by classifying the pathology tests into three categories: simple

Commitment and consumption of activity resources Steel max, Inc. sells of¬fice furniture in the Chicago metropolitan area. To better serve its business customers, Steelmax recently introduced a new same-day service. Any order placed before 2 p.m. is delivered the same day.Steelmax hires five

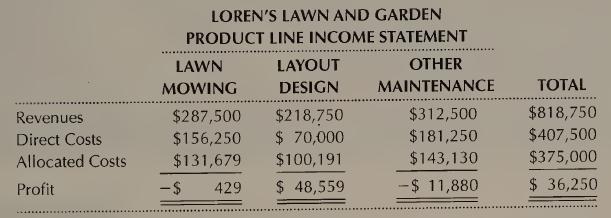

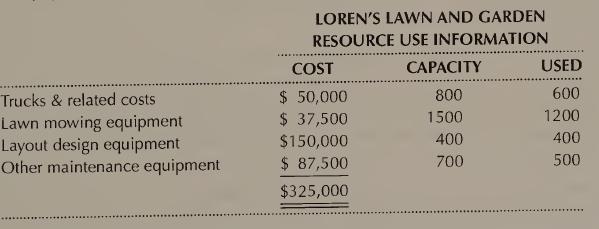

Commitment and consumption of activity resources Loren s Lawn and Gar- LO 1, 2, 3 dening performs various lawn and garden maintenance activities, including lawn mowing, tree and shrub pruning, fertilizing and treating for pests. Unlike other lawn and garden businesses in the city, Loren also

understand job order costing systems LO1

understand how using job bid sheets is effective for estimating product costs in a job order costing system LO1

use cost driver rates to apply support activity costs to products LO1

discuss why cost systems with multiple cost driver rates give different cost estimates than cost systems with a single rate LO1

evaluate a cost system to understand whether it is likely to distort product costs, explain the importance of recording actual costs, and compare them with estimated costs LO1

appreciate the importance of conversion costs and the measurement of costs in multistage continuous-processing industries LO1

understand the significance of differences between job order costing and multistage-process costing systems LO1

understand the two-stage allocation process and service department allocation methods LO1

Showing 2200 - 2300

of 5081

First

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

Last

Step by Step Answers