New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

statistics for engineers and scientists

Introduction To Probability And Statistics 2nd Edition Narayan C. Giri - Solutions

Let X \, X 2, A"3 be independent identically distributed Bernoulli random variables with P(Xt = 1) = p. Show that 3Xx + X 2 + 2X3 is not sufficient for p.

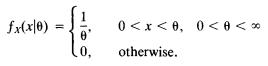

Let (Xi,...,Xn) be a sample of size n from a Cauchy distributionDoes 0 have a sufficient statistic? 1 T[1 + (x0)]' - fx(x|0) = 0, otherwise. > A > -

Let (X u ...,Xn) be a random sample from a population with beta distribution with parameter p = 0 > 0 and q = 2.Find the sufficient statistics for 0 .

Let ( X u ...,Xn) be a random sample of size n from the geometric distribution with pdfShow that 2" X t is sufficient for 0.Does belong to the exponential family? Px(x|0) => (1-0)*0, 10, x = 0,1,2,... otherwise.

Let ( X u ...,Xn) be a random sample of size n from the normal distribution with mean 0, variance a 2.Find the sufficient statistics for a 2.

Let ( X u ...,Xn) be a random sample of size n from the exponential family of distributions. Show that (2" Ti(Xi),...,'2l Tm(X,■)) is sufficient for 0 .

Let (X u ...,Xn) be a sequence of independently distributed normal random variables with unit variance and E(Xj) = j|x , |jl being unknown.Find the sufficient statistics for |x.

Let X be a Weibull random variable with pdfIf p is known, find the sufficient statistic for a on the basis of a random sample of size n. fx(x|,) Bar-exp(-ar), x>0, a>0, B > 0 (0, otherwise.

Prove Theorem 5.5.2 for the sequence (X u ...,Xn) of discrete random variables where the X t are independent and identically distributed.

Prove the Fisher-Neyman factorization theorem for discrete random variables.

Let X u...,Xn be a random sample of size n from the uniform distribution over the interval (a,p ), a < p.(a) Show that m a x ^ , . . . , ^ ) is a sufficient statistic for p if a is known.(b) Show that min(Xu ...,Xn) is sufficient for a if p is known.(c) Show that (min(2C,...,JC), max(Xu ...,Xn)) is

Let (X l9...,Xn) be a random sample of size n from the uniform distribution with pdfShow that max(Xl,...,Xn) is sufficient for 0 . fx(x|0) -{ 0

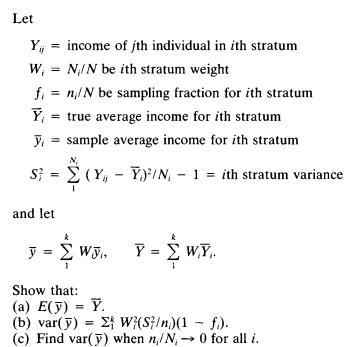

(Neyman allocation) Show that for stratified random sampling, var(y) *s minimized for fixed n if ni n = N,S N,S

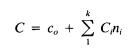

In Exercise 2 let C, denote the cost per unit for taking the sample from the ith stratum. The total cost for taking the sample iswhere c0 is the overhead cost. Show that given C, var(y) is minimum if rii is proportional to NiSjl V q. k C = c + Cn

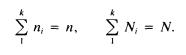

(Stratified sampling theorem) Let a population of N individuals be divided into k strata, N t being the size of the /th stratum. A stratified random sampling is used to draw a sample of size n, n, individuals being chosen from the ith stratum. Let -M- n; = n, ., = .

Let the events E ^ E 2,... be pairwise disjoint and exhaustive and let P(E.) > 0 for all i. Show that for any event A E U, Eh P(A) = P(A|E)P(E).

Let {Xn} be a sequence of independent random variables X n with E(X n) = n. Show that for any real numbersa, (3 (p > a), lim P{ a = x = "B} = * ^ = { = u - "X e-(1/2) dx.

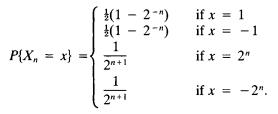

Let {Xn} be a sequence of independent random variables X n, n =1 ,2 ,..., defined by(a) Verify that the weak law of large numbers can be applied to the sequence {Xf\.(b) Examine whether the Lindeberg-Feller condition holds for the sequence {Xn}. P{X, x} = = (12") if x = 1 (12") if x = -1 if x = 2"

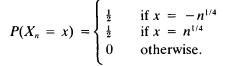

Examine whether the weak law of large numbers holds for the sequence{2C} of independent random variables X n, n = 1,2,..., defined by P(X = x) = -2-2 0 if x = -4 if x=n4 otherwise.

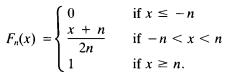

Let {Fn(x)} be a sequence of distribution functions Fn(x) defined byIs lim^oo Fn{x) a distribution function? 0 x + n F,(x) 2n 1 if x -n if-n

Prove the inequality (4.12).

Let A ^ . - . ^ b e a random sample of size n from a random phenomenon(the Xj take nonnegative values only) with finite mean |x. Show that the probability that 2 ?= t X { exceeds some constant a is not greater than n\±/a.

Let h(X) be a nonnegative and increasing function of a nonnegative random variable X and E(h(X)) 0, P{X E(X)> } E(h(X)) h(e)

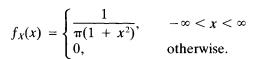

Let {Xn} be a sequence of independent and identically distributed Cauchy random variables with probability density functionLetA"„ = (1 ln){Xx +_•** + X n). Show that there does not exist a finite constant c to which X n converges in probability. fx(x) 0, 1 (1 + x)' x>x>x- otherwise.

Let {Xn} be a sequence of independent and identically distributed Poisson random variables with parameter X = 3 and let Y m =X x + ••• + X l00. Find P(100 < Y m < 200).

Let {Xn} (n = 1,2,...) be a sequence of independent random variables.Show that the probability of convergence of Sn = 2 ?=1 X t is either zero or one.

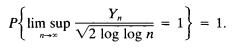

(Law of iterated logarithm) Let {Xn} (n = 1,2,...) be a sequence of independent and identically distributed binomial random variables with parameters n , p, and let q = 1 - /?, Yn = (Xn - n p ) l \ pq.Show that Y P{lim sup lim sup 2 log log n -1}=1 = 1.

Let {Xn} (n = 1,2,...) be a sequence of identically distributed random variables that have finite second moments equal to a 2.Let {Yn} (n =1 ,2 ,...) be a sequence of identically distributed random variables that are independent of the X n and take the values ± 1 each with probability i. Let Sn

Prove that if {X„} converges to X in probability and {Xn} converges to Y in probability, then P(X = Y) = 1.

Let {XJ converge to X in distribution and {Yn} converge to Y in distribution. Show that Fx{x) = FY(x) for all x.

(Slutsky’s theorem) Let {Xn} (n = 1,2,...) and {TJ (n = 1,2,...) be two sequences of random variables such that X n converges to a random variable X in distribution and {Yn} converges to C (constant) in probability. Show that {Xn + Yn} converges to X + C in distribution and X nYn converges to CX

Let {Xn} (n = 1,2,...) be a sequence of independent random variables converging to a constant c in distribution. Show that {.X „} converges to c in probability.

Show by an example that convergence in distribution does not necessarily imply convergence in probability.

Demonstrate by an example that the limit of a convergent sequence of distribution functions may not always be a distribution function.

Let X be a random variable with probability density function f(x) which is symmetric about 0 [i.e., f(x) = f ( - x ) for all jc]. Show that p( yk\ _ f 0 if A: is odd^ ' [finite if k even.

Let X x, X 2, X 3, X 4 be independently , identically distributed normal random variables with zero mean and unit variance. Let ax > 0, a2 > 0 andFind P(RX > R 2). R = aX + X, R =aVX+X.

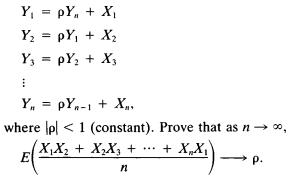

Suppose that the random variables X x,...,Xn are mutually independent and are identically normally distributed with zero mean and unit variance. Let Y = pY,, + X Y = pY, + X Y = pY + X3 = YpY+X. where p 1 (constant). Prove that as n , XX+ XX3 + + XX E n - p. P.

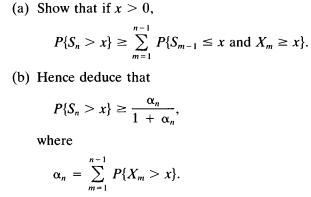

Suppose that the random variables X {,X2,... (ad infinitum) are nonnegative and independent. Define Sn = X\ + + X n with S0 = 0. (a) Show that if x > 0, P{S,>x} P{Sm-x and X x}. m=1 (b) Hence deduce that P{S > x} where - PLXm > x}, m-1

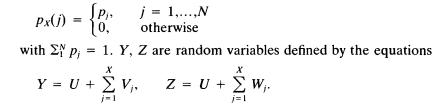

Let U,Vi,...,Vn and Wi,...,Wn be mutually independent random variables each with mean zero and variance a 2 (a) Show that X , Y Z are uncorrelated but not independent.(b) Find the correlation coefficient between Y and Z. [P = 1,...,N Px(j) (0, otherwise with p; = 1. Y, Z are random variables

Obtain the probability-generating function of qn: the probability that in n independent tosses of an unbiased coin no run of three heads occurs.

A population of N distinct elements in equal proportions is sampled with replacement. If Sr denotes the sample size necessary for acquisition of r distinct elements and if PH(r) = P(Sr = n), show thatHence or otherwise, derive the probability-generating function of Pn(r). PR+1(r) = 1 - 1 P (r) + Nr

In a sequence of n independent Bernoulli trials (with probability p of success), let En denote the probability of an even number of successes.Prove the recursion formula En = (1 - p)En_i + (1 - En_{)p.From this derive the probability-generating function of the random variable representing even

(Bienayme-Chebychev inequality) Let g{X) be a monotone function of a random variable X. Show that for every k > 0, P{g(X) > k}

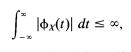

If ^(0 is the characteristic function of the random variable X andwhat can be inferred? |x(1) dt = ,

Let A" be a random variable with characteristic function (M /)- Let R(t)be the real part of (M /). Show that:(a) R(t) = E(cos(tX)).(b) R 2(t) < i[l + R(2t)].

Suppose that X , Y are independent random variables with distribution functions Fx(x), FY(y) and characteristic functions respectively. Show that the characteristic function of Z = X Y is given by *x(tx) dFx(x) *_ox(ty) dFx(y).

Determine whether or not the following are characteristic function and why.Variables, Distributions, and Functions 133(a)1 - t 21 + t2(b) cos t(c) log(e + |f|)(d) e -'4

Let the characteristic function of the random variable X be given by< M 0 = A (1 + 2eil + e2it)2.Find (a) P(1 < X < 4), and (b) P(X > 2).

Find the moment-generating function, the characteristic function, and the first and second central moments of the following distributions:(a) Uniform distribution over the interval (a,b)(b) Gamma distribution with parameters X, r(c) Geometric distribution(d) Negative binomial distribution with

Show that if X u...,Xn are independently distributed G(1,X), then Z = 2X 2?=i X t is distributed as xh39. Suppose that X , Y are independent gamma random variables with parameters X, 1 and X + J, 1, respectively. Show that the random variable 2\/XY has gamma distribution with parameters 2X, 1.

Let X x and X 2 be independently and identically distributed normal random variables with mean 0 and variance a 2.(a) Show that X xIX 2 has a Cauchy distribution.(b) Show that X \ + X \, X x(X\ + X l)~ vl are independent.

Let I b e a uniform random variable on the interval (1,3) and Y be an exponential random variable with parameter X such that V(X) =V(Y). Find X.

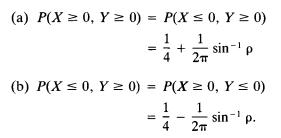

Let (X,Y) be a bivariate normal random variable with m x = m 2 = 0 and a? = a* = 1.Show that (a) P(X0, Y 0) = P(X 0, Y 0) 1 + sin-' p 2TT (b) P(X 0, Y = 0) = P(X = 0, Y 0) 14 1 2T sin-1 p.

Show that if the sum of n independent random variables is normally distributed then each variable is normally distributed. See Cramer(1937).

Let X , Y be independently and identically distributed normal random variables with mean 2 and variance 4.(a) Show that X + Y, X - Y are independent.(b) Show that (X + Y, X + 2Y) has a bivariate normal distribution with p = 3/VTo.

Suppose that the random variable X has a probability density function and is independent of another random variable Y. Show that X + Y has a probability density function.

Find the probability density function of Y = Fx (X) when X is a continuous random variable with distribution function Fx(x).

Let X , Y be independent and identically distributed geometric random variables. Let Z = max(X,Y). Find the distribution of Z.

Suppose that the random variables X , Y are independent and each has a uniform distribution over the interval (0,1). Find the probability density function of U = X + Y and V = XIY.

The random variable X is said to have log-normal distribution if log X has normal distribution; that is, its probability density function (with- o o 0) is given by(a) Find the mean and variance of X.(b) Show that if X is log-normal, so is X r.Show that if X , Y are random variables independently

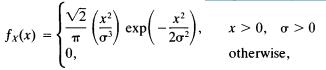

Show that if the random variable X has probability density functionthen X 2l v 2 has a chi-square distribution with 3 degrees of freedom. fx(x) == exp(- x>0, >0 20 0, otherwise,

Show that if the random variable X has uniform distribution over the interval (0,1), the random variable - 2 log X has a chi-square distribution with 2 degrees of freedom.

Show that if X , Y are independently distributed Poisson random variables with parameters X, p,, respectively, the conditional density function of X given X + Y = n is a binomial (n,p) with p = X/(|x + X).

Two discrete random variables X , Y have the joint probability density functionwhere X, p are constants with X > 0 and 0 (a) Find the marginal probability density functions of X and Y.(b) Find the conditional probability density function of X given Y. Px.x(x,y) e-p(1 - p) y! (x - y)! 0 if y 0,

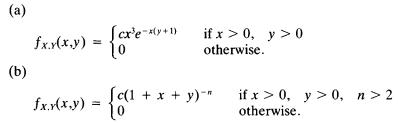

Let X , Y be two random variables having the following joint probability density functions:Find (a) the constant c; (b) the marginal probability density function of X and Y; (c) the conditional probability density function of X given Y = y. (a) fx.x(x,y) Sexe-(y+1) if x>0, y>0 otherwise. (b)

A box contains five tickets marked with the numbers 1, 2, 3, 4, and 5.Three tickets are drawn at random from this box one by one with replacement. Let X , Y denote the maximum and the minimum scores on the tickets drawn. Find the joint probability density function of X and y.

Consider two consecutive tosses of a coin. The random variable X takes on the value 0 or 1 according to whether a head or a tail appears as a result of the first toss. The random variable Y takes the value 0 or 1 according to whether a head or a tail appears as a result of the second toss. Are X ,

Prove that the joint distribution function FX,Y(X>>0 °f the random variables X , y is continuous in (x,y) if and only if each Fx(x), Fy(y) is continuous with respect to x and y, respectively.

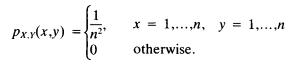

Let X, Y be a bivariate discrete random variables with joint probability density functionAre X and Y independent? Px.x(x,y) x 1,...,n, y1,....n = n otherwise.

Let the joint probability density function of the random variables X , Y be given byVerify that X , Y are not independent. fxx(x,y) (2. - 0 x 1, -(x 1) y (x 1) = otherwise.

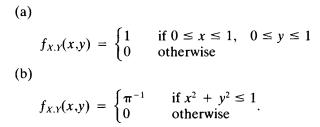

Suppose that the joint probability density function of the random variables X , Y is given byIn each case, find the marginal probability density function /*(*), fy(y)and the conditional probability density function /;r|y(*|y). (a) (b) fx.x(x,y) fx.v(x,y) - { = 0 if 0 x 1, 0 y 1 otherwise if x +

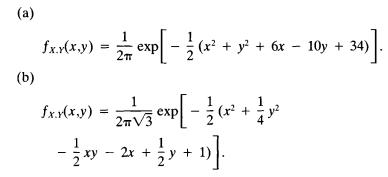

Find parameters m u m2, cr2, and p such that the following probability density functions can be written in the form of a bivariate normal density function. In each case, find the marginal probability density functions /*(x), f v( y ) and the conditional probability density function fx\v(x\y). (a)

The length of time (in minutes) X that a certain lady speaks on the telephone is a random variable with probability density function(a) Find the value of the constant c.(b) Find the probability that the duration of her conversation will be between 5 and 10 minutes. fx(x) Ice-x/5 = 1 if x 0

A filling station is supplied with gasoline once a week. If its weekly volume of sales (in thousand gallons) X has the following probability density function:what must be the capacity of its tank in order that the probability that its supply will be exhausted in a given week shall be 0.01? fx(x)

A bomber carrying three bombs flies directly over a railroad track. If a bomb falls within 40 feet of the track, the track will be sufficiently damaged to disturb the traffic. For a certain bomb site, the points of impact of a bomb have the probability density functionwhere x represents the

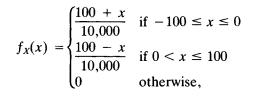

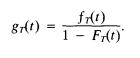

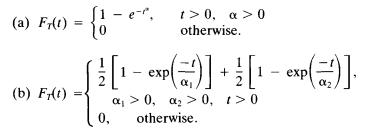

Let T represent the lifetime of a specific component of an electrical machine, and let fj{t), FT(t) be its probability density function and its distribution function, respectively. LetThe function gT(t) is called the failure rate of the component at time t. The distribution function FT(t) is called

Given that X is a normal random variable with mean 5 and variance 16, compute (a) P{\X - 5| > 3}; (b) P{\X - 4| < 2}; (c) P{X > 3}.

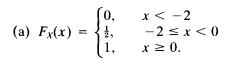

Verify that each of the following Fx(x) represents a distribution of a random variable X. Sketch the distribution function. Is the distribution function continuous? If so, find the corresponding probability density function. (a) Fx(x) = 1, X

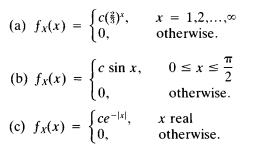

For each of the following find the constant c so that f x(x) satisfies the condition of being a probability density function or a probability mass function of a random variable X. (a) fx(x) = Sc(). 10. x = 1,2,...,x otherwise. (b) fx(x) (c) fx(x) == = [c sin x, lo. Sce-1x1 10. otherwise. x real

The Scholastic Aptitude Test scores in mathematics in a certain year vary from 200 to 800.Assume that they are normally distributed with mean 450 and variance (120)2.(a) What percentage of students score between 500 and 700?(b) What test score represents the 90th percentile?

Find the probability mass function of the random variable X , defined to be the sum of the two numbers showing in the toss of two dice.

For an infinite number of independent tosses of an unbiased coin, find the probability density function of the random variable U = number of tosses needed to get two heads together for the first time. Also find P{U > 4}.

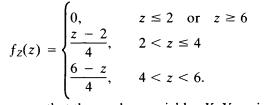

Let Z = min(Ar,y ). Find P(0 < Z < 3) for each of the following cases:(a) X , Y are independent, identically distributed normal random variables with mean 0 and variance 4.(b) X , Y are independent, identically distributed binomial random variables with parameters n = 10, p = 0.2.(c) X , y are

Two people toss an unbiased coin n times each. Find the probability that they will score the same number of heads.

Let X be a uniformly distributed random variable over the interval

Let X be a continuous random variable with probability density function, , s _ for x > 0 jx(x) - otherwise.Find, for any reala, P{X3 < a}.

The families in a community are divided into four income groups G x, G2, G3, G4, consisting of N u N 2, N3, NA families, respectively. Each group is composite in the sense that it consists of German, English, Canadian, and American families, their respective proportions for the group Gj being qn ,

An urn contains five white and six black balls.(a) Three balls are drawn from the urn one after another without replacement, and it is found that one of them is white and the other two are black. What is the probability that the first ball drawn was white? What is the probability that the first

Three urns f/i, U2, U3 contain, respectively, two white and three black balls, three white and four black balls, and one white and two black balls.(a) Two balls, one from urn U\ and the other from urn t/2, are drawn and placed in urn U3; thereafter one ball is drawn from U3 and is found to be

Two dice are tossed. Define the following events.A t: sum of the face values is /, i = 2,3,...,12, B x: difference of the face values is an odd integer, B2: difference of the face values is an even integer or 0.Prove the following.(a) A t C B\ if i is an even integer.(b) A t C B2 if i is an odd

An urn contains four balls numbered 1, 2, 3, 4.They are drawn one after another without replacement. If A t is the event that the /th ball appears at the ith draw, i = 1,2,3,4: _ _(a) Show that A x H A 2 fl A3C A4; A xPi A2fl A3C A 4.(b) Find each of the following sets.A x U A 2 U A3 U A4; ( Ax H A

Let S consist of all integers from 1 to 50.Define the following subsets of S: E x, all integers divisible by 5; E2, all integers divisible by 7; £ 3, all odd integers less than 36.Find each of the following sets.(a) E x D E2.(b) £, n e 2 n £ 3.(c) e x n e 2._(d) (£ , n e 2) n £3.(e) (£ , -

For a sequence of sets A n, prove the following relation:lim inf A n C lim sup A„.

Let A,B,C be any three events. Using the operations of union, intersection, and complementation, give an expression for the following events.(a) None of the events occurs.(b) All three events occur.(c) At least one event occurs.(d) Only A occurs.(e) Only A and B occur.(f) Exactly one of the events

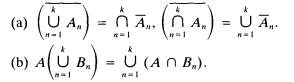

Show that (A) = U (a) (A) = (UA)=.. A (U B.) = U (An B.) (b) A (AB).

Let A,B,C ,..., be arbitrary sets. Verify the correctness or incorrectness of each of the following statements.(a) (A n B) - C = A fl B n C.(b) ( A U B ) - C = ( A - C ) U ( B - C).(c) (A U B)C = (A n C) U (B Pi C).(d) A U B = [A - (A n B)] U B.(e) (A n B) n (A n c ) = 0.(f) A U B U C = A U ( B - A

Verify the following relations for any sets A,B,C,....(a) A U B = A n B. _(b) A - B = A - (A n B) = A n B = (A U B) - B.(c) (A n B) U (A - B) = A.(d) (A n B) n (A — B) = 0.(e) ( A U B ) - ( A n B ) = ( A - B ) U ( B - A).(f) a n (B - c ) = (A n B) - (A n c).(g) (A u B) n c = c - c n (A u B).(h)

Prove that for arbitrary events A, B, C, the following statements do not hold in general:_(a) P(A\C) + P(A\C) = 1.(b) P(A\C) + P{A\C) = 1.(c) P(A U B\C) = P(A\C) + P(B\C).(d) P(A H B\C) = P(A\C)P(B\C).Investigate conditions, if any, under which each statement is correct.

Prove that if A and B are independent events, then:(a) A and B are independent events.(b) A and B are independent events.

Using unions, intersections, and complements of sets, and the definitions of total and compound events in terms of sets, prove by applying the axiomatic definition of probability that for any three arbitrary events A , B, C:(a) P(A U B U C) - P(A) + P(B) + P(C) - P(A OB) - P{B nc) - P(c n A ) +

Showing 3500 - 3600

of 5712

First

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

Last

Step by Step Answers