New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

statistics for engineers and scientists

Introduction To Probability And Statistics 2nd Edition Narayan C. Giri - Solutions

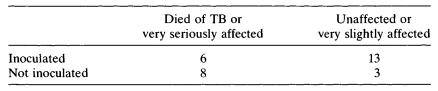

In experiments on immunization of cattle against tuberculosis (TB) the following results were obtained:Test the hypothesis that inoculation and susceptibility to tuberculosis are statistically independent. Inoculated Not inoculated Died of TB or very seriously affected 6 80 Unaffected or very

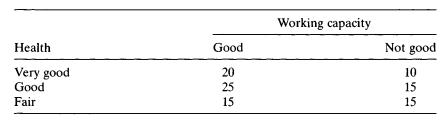

Test for independence between the two characteristics, health and working capacity, tabulated below. Health Very good Good Fair Good 55 25 15 20 Working capacity Not good 15 15 255 10

The following data show the distribution of digits 0,1,...,9 in telephone numbers chosen at random from the telephone numbers from the telephone directory of the Montreal area:Test whether the digits may be taken to occur equally frequently in the directory. Digit 0 1 2 3 4 5 6 7 8 9 972 964 853

A die was thrown 200 times and the following results were obtained.Are the results consistent with the hypothesis that the die is fair? (Take a = 0.05). Face up 1 2 3 4 5 6 Frequency 27 32 39 28 49 25

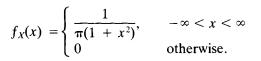

Let X x,..., X n be a random sample of size n from a random phenomenon specified by the exponential probability density functionwhere 0 > 0.Find an upper 100(1 - a)% confidence bound for 0. fx(x) Oe-x = (0. x0 otherwise,

Let X u ...,Xn, be a random sample of size n x from a random phenomenon specified by the normal distribution with mean and variance ct2; and let Y x,...,Yn^ be a random sample of size n2 from another random phenomenon specified by the normal distribution with mean|x2 and variance ct2.(a) Set up a

Let (X u Y l),...,(XrnYn) be a random sample of size n from a bivariate normal distribution with parameters jxj, |x2, ct2, ct2, p. Give a 90%confidence interval for the difference |Xj - \x2 of the means.

How would you modify the confidence interval given in Example 10.8.2? if the mean fx of the underlying normal distribution is unknown?

Give a 95% confidence interval for jut in Example 10.8.1 supposing that the variance a 2 of the underlying normal distribution is unknown.

Find an alternative 95% confidence interval for (jl in Example 10.8.1

A cigarette manufacturer sent each of two testing laboratories presumably identical samples of tobacco. Each laboratory made six determinations of nicotine content in milligrams as follows:Were the laboratories testing the same product? (Assume normality with the same variance.) Lab 1 24 26 20 20

Two random samples of sizes 12 and 14, respectively, are drawn from two normal populations with unknown means and a common but unknown variance a 2.Find an appropriate test for the equality of the two means. Draw a power curve of the test against(a) One-sided alternatives with a = 0.05.(b)

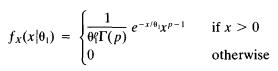

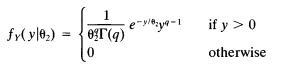

A random sample of size 12 is drawn from a random phenomenon specified by the probability density functionwith p = 16 and 0j > 0 and a second random sample of size 15 is drawn from another random phenomenon specified by the probability density functionwith q = 18 and 02 > 0.Find a suitable

A sample of size 11 is drawn from a normal distribution with an unknown mean jjl and unknown variance a 2.Construct the power curves for the two one-sided uniformly most powerful tests of(a) //o: a 2 = 25 against H x\ a2 < 25.(b) H (): cr2 = 25 against H x: a2 > 25.Take a = 0.05.

Suppose that we have two univariate normal distributions with means|xL, |x2 and variances 4, 9, respectively. Two samples of sizes 10 and 15, respectively, are taken from these two populations in order to test the equality of the means at the level of significance 0.025. Draw the power curve of the

With the inception of a new system of traffic control it is hypothesized that the number of daily road accidents will be reduced. For the last few years the average number of road accidents per day in a certain city has been 12.On the basis of current-year data, how do you propose to test the

On the basis of the results of the tossing of a coin 25 times it is to be tested whether or not the coin is biased. Give the suitable unbiased test procedure with a level of significance not exceeding 0.05. Draw the corresponding power curve to verify the unbiasedness of the test.Also consider the

Show that if (Xx,...,Xn) is the most powerful test of size a for testing the simple hypothesis H {): 0 = 0O against the simple alternative H x:0 = 0H then £ 0()() < £ 01()-

Let X u...,Xn be a random sample of size n from a normal distribution with mean 0 and unknown variance a2. Find the uniformly most powerful test of H {): a 2 = of} against H x: a 2 > of).

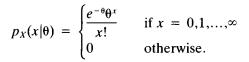

Let X x,...,X n) be a random sample of size 10 from a random phenomenon characterized by the probability mass functionFind the most powerful (randomized) test of H(]: 0 = 0.01 against H x:0 = 1 at level of significance a = 0.05. Px(x|0) = 0 x! if x = 0,1,...,x otherwise.

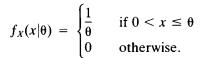

Let X u...,Xn be a random sample of size n from a random phenomenon specified by probability density functionFind the uniformly most powerful test of (a) F/o: 0 = 0() against H x: 0 > 0().(b) / / (): 0 = 0O against H x: 0 fx(x0) 0 if 0 < x 0 otherwise.

Let X j,..., X n be a random sample of size n from a random phenomenon specified by the probability density functionFind the most powerful test of size 0.05 of H0: 8 = 80, (3 = p0 against H x: 8 = 8! ^ P Pi ^ Po. h it uniformly most powerful for testing / / 0 against the composite alternatives 8

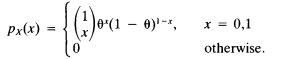

Let X x,...,Xn (n sufficiently large) be a random sample of size n from a random phenomenon specified by the Bernoulli distribution with parameter 0, that is,Find the most powerful test of size 0.05 of (a) H0: 0 = \ against H x:0 = i; (b) H 0: 0 = J against H 0: 0 = i Px(x) = 0 :)or(1 0 (1-0), x =

Let X {,..., X n be a random sample of size n from a random phenomenon specified by the probability density functionFind the most powerful test of (a) / / 0- 0 = 2 against H x\ 0 = 4; (b)H {): 0 = 2 against H x: 0 = 1. fx(x0) = 0 0 < x < x otherwise.

Let X !,..., X n be a random sample of size n from a random phenomenon specified by a normal distribution with unknown mean |jl and variance 4.(a) For testing H0: |x = 0, show that each of the following critical regions is of the same size a = 0.05.1.2X_ > 1.645 2.2 X < -1.645 _ 3.2 X < - L960 and

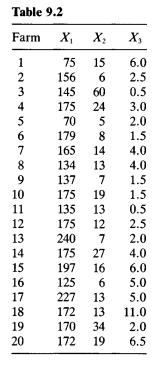

The variability in the price of farmland per acre is to be studied in relation to three factors which are assumed to have a major influence in determining the selling price. For 20 randomly selected firms, the price (in dollars) per acre (Xf), the depreciated cost (in dollars) of building per acre

Let = (XaU...,Xapy , a = be a random sample of size N from A/p(|x,2 ).(a) Find the maximum likelihood estimator of |jl when S is known.(b) Find the maximum likelihood estimator of 2 when |jl is known. Is it unbiased? Table 9.2 Farm X X X 123 75 15 156 145 4 175 5682 6.0 2.5 60 0.5 24 3.0 5 70 5 2.0

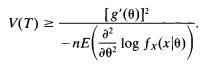

Show that Rao-Cram er inequality can be written as [g'(0)] V(T) -nE - log fx(x0))

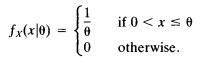

Let (X u ...,Xn) be a random sample of size n from a random phenomenon specified by the uniform probability density function(a) Show that Y = max(Ar1,...,ATw) is a consistent estimator of 0 .(b) Show that (n + 1 )Y is the minimum-variance unbiased estimator of 0 . fx(x|0) = 0 0 if 0 < x 0

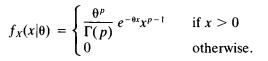

Consider a random phenomenon specified by the probability density function (with p known)For any random sample ( X u ...,X n) from this let us define X n by(a) Show thatis an unbiased, consistent, sufficient estimator of 0 .(b) Find the efficiency of the most efficient estimator of 0 . fx(x|0) =

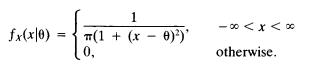

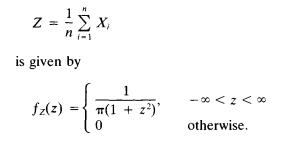

Let (Xu ...,Xn) be a random sample of size n from a random phenomenon specified by the Cauchy distribution with probability density functionIs X n = (1 In) 2? X t a consistent (weakly) estimator of 0 ? Find a consistent estimator of 0.{Hint: X n has the same Cauchy distribution.) 1 - (1 + (x = 0))'

Consider a random phenomenon specified by the exponential probability density functionFind the most efficient estimator of g(X) = 1/X on the basis of a random sample of size ft. Is it consistent? fx(x|) = So, x 0 x > 0.

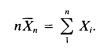

Let ( Xu ..., JC) be a random sample of size n from a Poisson distribution with param eter X. Find the most efficient estimator of X. Is it strongly consistent?

Let (JC ,...,JQ be a random sample of size n from a random phenomenon specified by binomial distribution with parameter (N,p). Find the most efficient estimator of p. Is it strongly consistent?

Let I lv . , I „ b e a random sample of size n from a normal distribution with mean |x and variance a 2.LetShow that 5 2 is a weakly consistent estimator of a2. nS} = (. - ), .. = .. 1

Suppose that Tu T2, T3 are unbiased estimators of the parameter 0 and Ti is the minimum-variance unbiased estimator of 0.Assume that V(T2) = V(T3) = \ V ( T {), X > 1.Show that the coefficient of correlation p satisfies(a) p(Tl9T2) = p(T uT3) = X 1/2.(b) P( r 2 , r 3) = (1/X)(2 - X).

Let Xi,...,Xn be n independent, identically distributed random variables, distributed uniformly on the integers, 1 ,2,...,TV, where N is unknown. Show that T = m a x ^ G ,...,^ ) is a sufficient estimator for N.

Let X u...,Xn be a random sample from a normal distribution with mean 0 , - o o < 0 < oo? and variance 1.Let n X = 2" X h Show that X 2 — (l//t) is a minimum-variance unbiased estimator of 02.

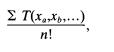

Let (Xi,...,Xn) be a random sample of size n from a distribution with parameter 0 , and let T(Xu ...,Xn) be a minimum-variance unbiased estimator of g(0). Denote by (xa,xb,...) a permutation of (xu ...,xn).There are n\ such permutations of x u ...,xn. Show thatwhere the summation is over all

Let X x,...,Xn be a random sample of size n from a normal distribution with mean p, and variance a 2.Let c be a given constant such that EXERCISES nX = 2 x h S2 = 2 (X, - x y .p = P(X > c).Find the best unbiased estimator of p. [Hint: LetThen E{T) = p. Use Exercise 7 and the Rao-Blackwell

Let X u...,Xn be a random sample of size n from a normal distribution with mean p, and variance a 2.Let Tx = ^ djXh T — S" Xj. Show that the complete sufficient statistic T is independent of Tx if and only if

Let X = ( X l,...,Xp)' be a random /7-vector, normally distributed with mean p, = (p ,!,...,^ )' and covariance matrix I (identity matrix). Let X a = (Xal,...,Xapy , a = 1, ,7V, be a random sample of size N from this distribution. Show that X = X J N is a complete sufficient statistic for |x.

Let ( X x,...,Xn]), ( y l5. . . , y j be two random samples from two different normal distributions with the same mean p, and variances 0 7 , 0 -5 , respectively. Let Show that T is sufficient for 0 = (p,,a2,cn), but that T is not a complete sufficient statistic.

Let ( X u ...,Xn) be a random sample from the normal distribution with mean p, and variance a 2.LetShow that (^r,52) is a complete sufficient statistic for 0 = (p,,a2), — 00 0 . .. - .. S = (x, - X).

Show that for a normal population with mean jjl and variance a 2, sample mean is the minimum-variance unbiased linear estimator for |j l .

Let X u...,Xn be n independent normally distributed random variables with E(Xj) = (jl and var(X{) = 1/i. Find the minimum-variance linear unbiased estimator of |j l .

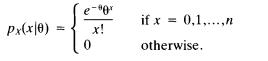

Let (jtj,... ,xn) be a random sample from a random phenomenon specified by the probability mass functionFind an unbiased estimator of 0 2.Does 0 -2 have an unbiased estimator? e-90 if x = 0,1,...,n otherwise. Px(x|0) = x! 0

Let (xx„) be a random sample from a Bernoulli distribution with P(X, = 1) = 0 = 1 — P(X, = 0), where 0 < 0 < 1.Find an unbiased estimator of 0 2.Compare this result with Example 9.1.4. Show that 1 / 0 " does not have an unbiased estimator for any integer r > 0 .

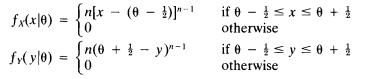

In Exercise 1 show that the probability density functions of X = m ax^,^X h Y = m in ^,^ A',- are given byFind the probability density function of X + Y. fx(x|0) [n[x (0)]-1 fv(y|0) === [n(0 + y)"-1 - 0 if 0 x0 + 1 otherwise if 0 sys0 + } otherwise

Let ( X x,...,Xn) be a random sample of size n from a random phenomenon characterized by the uniform probability density functionShow that (a) 2" X tln, (b) (m ax^,^ X { -f m in ^ ,^ X )l 2 are unbiased estimators of 0 . [1 fx(x|0) == + 0 > x > } - 0 J! otherwise.

Let X u ...,Xn+l be independently and identically distributed random variables with pdf f x(x) = e x p (-x ), x > 0.LetShow that Y l9...9Yn form the first n order statistics from a uniform distribution over interval (0 ,1 ). . Y = i = 1,...,n.

(Continuation of Exercise 10: Koimogorov-Smirnov theorem) Let Dn = sup _* lim P(VnD, O 0, A 0.

(Glivenko-Cantelli theorem) Let S„(x) denote the empirical distribution function of a sample of size n from a random phenomenon specified by the distribution function Fx(x). Show that Sn(x), - o o oo with probability 1.

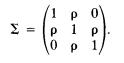

Let ( X UX 2) follow a bivariate normal distribution with E ( X 0 = E ( X 2) = 0, V(X x) = V(X2) = 1.Let the coefficient of correlation between X x and X 2 be equal to p.Find the distribution of Y2 — Y u where Y2 = max(XuX 2), Y x = m i n ^ , ^ ) .Calculate the probability P{Y2 > 0}. Show that

Consider Example 8.3.1. Define Z, = Y, - Y{_u 1 — i — n (Y 0 = 0).Show that Z u...,Zn are mutually independent and that (n - i + 1)Z„i = 1 has chi-square distribution with 2 degrees of freedom.

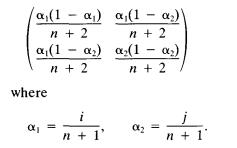

Let Yu...,Yn denote the order statistics of a random sample of size n from a random phenomenon specified by the continuous distribution function F. Show that the variance and covariance matrix of the random vector (UhUj), 1 a(1 a) a (1)\ where n + 2 n + 2 ) (1) n + 2 n + 2 i n+1' 02- = n + 1'

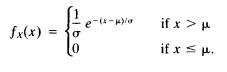

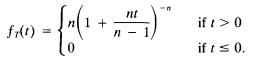

Let y l 9 . . . , y n denote the order statistics of a random sample of size n from the continuous probability density functionLetShow that the probability density function of T is given by e-(x-1)/a fx(x) if x> p if x = p.

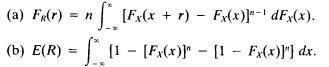

(Continuation of Exercise 4) Show that for R = Yn - Y x\ (a) Fx(r) = n {*_ [Fx(x + r) Fx(x)]' dFx(x). (b) E(R) = - [1 - [Fx(x)}" [1 Fx(x)]"] dx.

Let y l9...,y w denote the order statistics of a random sample of size n from a population specified by the continuous distribution function F.let V =Fx(Y). V = Fx(Y) - Fx(Y-1), i = 2,...,n. Find the joint probability density functions of (i) V....,V,, and (ii) VV, kn.

Show that the probability density function of Yk+l is symmetric about Yk + l = |x and deduce that E ( Y k + l) = |x.

Let Yk+l denote the median of a random sample of size 2k -f 1 from the normal distribution with mean |x and variance a

Find the probability that the range of a random sample of size 5, from a uniform probability density function on (0 ,1 ), is greater than

Let Yj,...,Y5 denote the order statistics of a random sample of size 5 from a random phenomenon specified by the probability density functionShow that Y2/ Y 4 and Y4 are independent random variables. fx(x) 3x, 10, 0 < x < 1 otherwise.

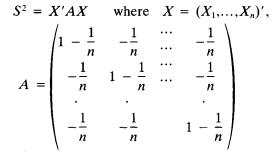

Let X u...,Xn be independently and identically distributed normal random variables with mean |x and variance a 2.(a) Show thatis an n x n idempotent matrix of rank n - 1 .(b) Using Exercise 12, show that S2 /cr2 is distributed as chi-square with n — 1 degrees of freedom. S = X'AX where x =

Let X be distributed as Ep(|jl,2), and let(a) Show that the joint distribution of (eu ...,ep) is Dirichlet with pdf(b) The pdf of L isand L is independent of (eu ...,ep). i=1.....p. L = X'X.

Do Exercise 15 when E (Y ) = X$, (3 = ((3i,...,(3p)' and E(Y —X $)(Y - Xpy = a 2/. Show that cov(( X(X'X)-'X')Y) = o(I - X(X'X)-'X').

Let Y = (Yu ...,Yn)' be normally distributed n vector with zero means and covariance matrix I (n x n identity matrix) and let X be a n x p matrix of rank p(

Let Z be a matrix of dimension p x k (p /c) and is of rank k, and let X be distributed as Np(0,I).(a) Show that Z (Z 'Z )_1Z ' is an idempotent matrix.(b) Find E { X ’(I - Z (Z 'Z ) ~ lZ ')X ).

Let X be distributed as Np(\l ,1). Show that two semipositive definite quadratic forms X ' A X , X ’B X (with A, B symmetric matrices) are independently distributed if and only if A B = 0.

Prove that if A" is distributed as ^Vp(0,S), a necessary and sufficient condition for the quadratic form X'AX, with A a p x p symmetric matrix, to have a chi-square distribution with k degrees of freedom is that XA be an idempotent matrix of rank k.

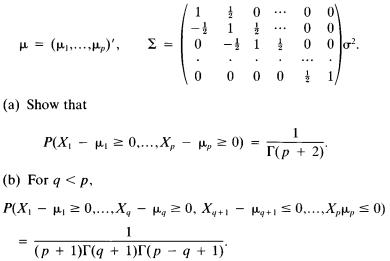

Let X = (Ar„...,Ar,)' be Np(|x,2), where = (....Hp)', = M 0 -1 0 ... 10 000 0 0 00 0 02. -10+ (a) Show that 1 - P(X 0.....Xp - Mp0) == (p + 2) (b) For q

Let X = (Xi,X2y be N2(|jl,S), where p, = (p,1?p,2)',(a) Show that Z = - yn)/(X2 - P2) has pdf(b) Find the distribution of (Xx + X 2, X x - X 2)'. -1

Let X = be iVp(|x,2). Show that E ( X ’A X ) = p/Ap, + tr XA.

Let X = (XU...,XPY be distributed as A^(0,a2/). Show that for any p x p symmetric matrix A , E { X ’A X ) = a 2 tr A.

(Symmetric normal distribution) The random vector X = ( X u ...,Xp) f is said to have a symmetric normal distribution if it is distributed as Np(p-,2), where p. = (p-i andthat is, var(A",) = cr2, cov(Xi,Xj) = pa2 for all i 7^ j = 1 Let 0 be an orthogonal p x p matrix and be defined byand let ’y =

Let X be normally distributed with mean 0 and variance 1.DefineShow that Y is N(0,1) and the joint distribution of X , Y is not a bivariate normal. -x Y = X, if-1 X 1 otherwise.

In Exercise 4, assume that a is random vector independent of X satisfying P(a'Xa = 0) = 0.Show that F is N(0,1) and F is independent of a.

Let X = (X u ...,Xp)f be Np(|x,2), and let a = (au ...,ap)' be a fixed vector. Show that F = a’{X - |x ) ! \ f a'Xa is normally distributed with mean 0 and variance 1 provided that a'Xa > 0 .

Let X = ( ^ , 2 ^2 ,2 0 ' be distributed as N3(0,2), whereFind the value of p so that X x + X 2 4- X 3 and X x - X 2 — X 3 are independent. 1 p 0 1 1/

Let Z = (X u X 2)f with pdfShow that the marginal distributions of X x and X 2 are normal but X is not a bivariate normal. 0, exp[-(x + x)] if x,x2 > 0 otherwise.

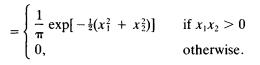

Let X = (Xi,X2) ’ be a bivariate random vector with pdf(a) Find the marginal pdf of X x and X 2.(b) Calculate E ( X x), E ( X 2) cov(A"). fx(x) = 1 43 [(x,-2) +(x3) (x - 2)(x2 - - 3)1}.

Shots are fired at a vertical circular target of unit radius. The distribution of the horizontal and the vertical deviations of the shots from the center are normal, with zero means, unit variances, and correlation coefficient p. Show that the probability of heating the target is 1-p T x * "*" (1

Let X , y be two independent normal random variables with means m u m2 and variances cr?, respectively, and letShow that U is normally distributed with mean zero and unit variance. U 47 m - mZ GZ3)/2 Z =

Let X u...,Xn be a random sample of size n from a random phenomenon specified by the uniform probability density function fx(x) and let 071 if 0 < x

Let X i,... ,Xn be a random sample of size n from a random phenomenon specified by the Cauchy probability density functionShow that the probability density function of the random variable fx(x) 1 (1 + x)' otherwise.

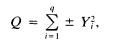

If Q is a quadratic form of rank q (?) in X U...,XP, show that Q can be expressed aswhere Yj is a linear function of X u ...yX p for / = 1,...,^. Q IM- Y.

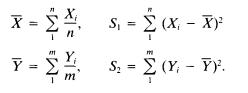

Let X u...,Xn be a sample of size n from a normal population with mean v and variance a 2, and let Y x,...,Ym be a sample of size m from a normal population with mean v and variance a 2.Assume that{XU...,X,) are independent of Write(a) Show that X — Y is independent of S2 + S2-(b) Find the

(Infinitely divisible distribution) A random variable X is said to be infinitely divisible if for every n, X can be written aswhere the random variables X u...,Xn are independent and have the same distribution function Fn( X ) (depending on n). The distribution function of an infinitely divisible

(One-parameter exponential family) Let 0 be a real parameter. The distribution of the random variable X having probability density functionis said to belong to the exponential family of distributions. Show that the gamma distribution, the normal distribution with known variance, the normal

(Pearson probability distribution) Distributions where the probability density functions f x(x) satisfy the differential equationwherea, 6(), b u b2 are real constants, are called Pearson probability distributions.(a) Show that if ixA = E(X - E(X))k, thenwhere A = 10|x4|jl2 - 1 8 ^ - 12|X5.(b) Show

(Logistic distribution) A random variable X is said to have logistic distribution function Fx(x) ifwhere a > 0, b are real constants. Show that the corresponding probability density function is Fx(x)=(1+e(ax+b))-1, x > x>x-

Show that if X , Y are two independent chi-square random variables with m, n degrees of freedom, respectively, the random variables X +Y and X/Y are independent.

Show that if X , Y are independent and identically distributed normal random variables with mean 0 and variance 1 , then:(a) X 2 + Y 2 and X/Y are independent random variables.(b) X /Y has Cauchy distribution.

Show that if X , Y are independent random variables (univariate) such that X + Y is independent of X - Y, then both X and Y are normal random variables.

Let X u...,Xn be independently, identically distributed N(|x,a2). Show that U = 2, 2y {Xj - Xj)2 and W = 2f=1 X t are independent. Find the distribution of U.

Let X u...,Xn be independently distributed random variables and let Sm = Sjij X h m < n. Show that the joint distribution of X t and Sm does not depend on i < m.6 . Let X u...,Xn be independently and identically distributed normal random variables with E(X]) = |xt, var(AT/) = 1 for i = 1 Let 8 2

Let Xi,...,X„ be independently and identically distributed jV(|ji,ct2).Define(a) Show that X is independent of (b) Using (a) show that X, S2 = 2 ,"=1 (Xt - X ) 1 are independent. X = X; == X; Z=X-X, i = 1,...,n.

Let X, Y be independent where X is 7V(|x,a2) and Y is jV(0,T2). Let Z = X + Y. Find the conditional pdf of X given Z = z.

Let X, Y be two independent gamma random variables with pdf G(l,n), G(l,n + 5 ), respectively. Show that Z = 2^/XY is distributed G(l,2n).

Let X, Y be two independent beta random variables with pdf B {p l,ql), respectively. Find the joint distribution of Y, = X , Y2 =Y(1 - X).

Showing 3400 - 3500

of 5712

First

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

Last

Step by Step Answers