Question: Please Help!!!! Bonus Problem 3 (Optional, 40 marks) We consider the mean variance portfolio selection with 1 riskfree asset and N risky asset (with N

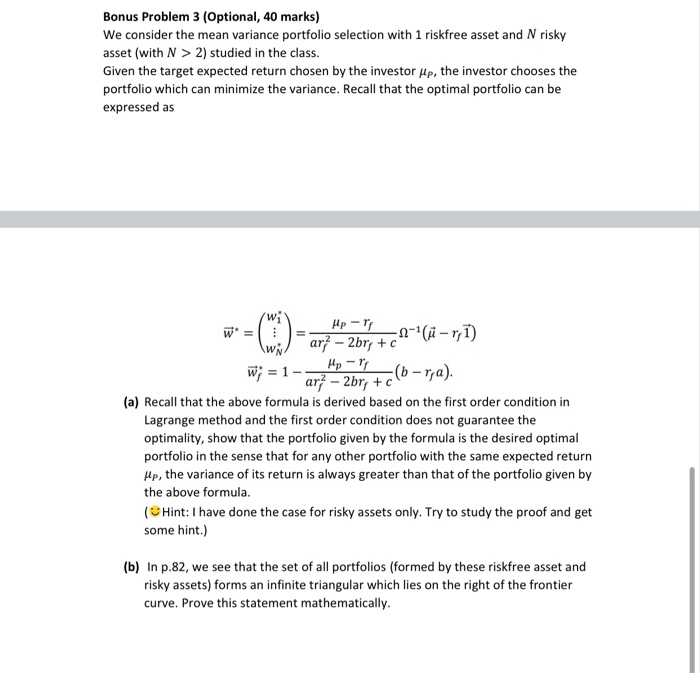

Bonus Problem 3 (Optional, 40 marks) We consider the mean variance portfolio selection with 1 riskfree asset and N risky asset (with N > 2) studied in the class. Given the target expected return chosen by the investor up, the investor chooses the portfolio which can minimize the variance. Recall that the optimal portfolio can be expressed as W1 Hp - \w; ar? - 2br + 2a- r;) Hp - " ( bra). ar? - 2bry +c" (a) Recall that the above formula is derived based on the first order condition in Lagrange method and the first order condition does not guarantee the optimality, show that the portfolio given by the formula is the desired optimal portfolio in the sense that for any other portfolio with the same expected return Hp, the variance of its return is always greater than that of the portfolio given by the above formula. (Hint: I have done the case for risky assets only. Try to study the proof and get some hint.) (b) In p.82, we see that the set of all portfolios (formed by these riskfree asset and risky assets) forms an infinite triangular which lies on the right of the frontier curve. Prove this statement mathematically. Bonus Problem 3 (Optional, 40 marks) We consider the mean variance portfolio selection with 1 riskfree asset and N risky asset (with N > 2) studied in the class. Given the target expected return chosen by the investor up, the investor chooses the portfolio which can minimize the variance. Recall that the optimal portfolio can be expressed as W1 Hp - \w; ar? - 2br + 2a- r;) Hp - " ( bra). ar? - 2bry +c" (a) Recall that the above formula is derived based on the first order condition in Lagrange method and the first order condition does not guarantee the optimality, show that the portfolio given by the formula is the desired optimal portfolio in the sense that for any other portfolio with the same expected return Hp, the variance of its return is always greater than that of the portfolio given by the above formula. (Hint: I have done the case for risky assets only. Try to study the proof and get some hint.) (b) In p.82, we see that the set of all portfolios (formed by these riskfree asset and risky assets) forms an infinite triangular which lies on the right of the frontier curve. Prove this statement mathematically

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts