New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

banking

An Introduction to Derivative Securities Financial Markets and Risk Management 1st edition Robert A. Jarrow, Arkadev Chatterjee - Solutions

What is a wash sale? Can you explain why the IRS (tax authorities) prohibits the use of wash sales?

What is front running? Explain why an investor should be concerned if his stockbroker front runs his trades.

What is dual trading? Why should an investor be concerned about a specialist dual trading?

What are the three conditions that the law requires to prove manipulation? Are these hard or easy to prove?

What is a short squeeze, and under what circumstances does it occur?

What is an arbitrage opportunity across time? Give an example.

What is a bear raid? How does a bear raid relate to trading on inside information?

What is the law of one price?

Explain the pricing principle “nothing comes from nothing.”

Suppose a two-year Treasury note is trading at its par value $1,000. You examine the cash flows, and if you sell them individually in the market, you get $47.85 for the six-month coupon, $45.79 for the one-year coupon, $43.81 for the one-and-a-half-year coupon, $41.93 for the two-year coupon, and

Suppose a two-year zero-coupon bond has a price of $0.90 and a three-year zero has a price of $0.85. A bank allows you to borrow or lend at 4 percent, compounded once a year. Show two ways that you can make arbitrage profits from these prices.

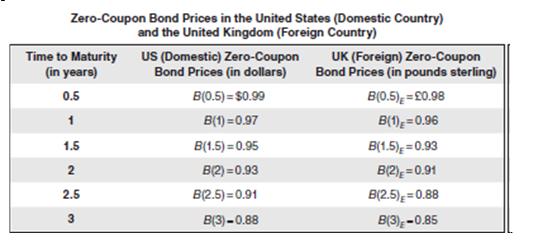

You can trade Boring Unreliable Gadget Inc.’s stock for $77 per share in the United States and for €50 in Europe. Assume a brokerage commission of $0.10 per share in the United States and €0.10 in Europe. A foreign exchange dealer quotes a bid price of $1.5000 for each euro and offers them

What is an efficient market, and what does it mean for a market to be weak-form, semi strong-form, and strong-form efficient?

If the market is weak-form efficient, do arbitrage opportunities exist? Explain your answer. Do you think arbitrage opportunities exist? Explain your answer.

Briefly describe a plain vanilla interest rate swap. Is the notional principal paid out at the swap’s beginning and maturity?

How can one use a currency swap to hedge currency risk?

How can one use an interest rate swap to change a fixed rate loan into a floating rate loan?

How can a savings and loan bank use an interest rate swap to match its long-term fixed rate investments with the risks of its short-term floating rate demand deposit obligations?

What is an equity swap? What is a commodity swap?

Suppose an investor is precluded from investing in a country’s stocks by government regulations but can invest in the country’s government bonds. Design a swap to overcome these regulations.

What is a forex swap? Explain how it works.

In chapter 2, we described how the US Treasury STRIPS worked. Explain how Wall Street firms had financially engineered a product similar to STRIPS.

What is a callable bond? When would it be used?

What is a put able bond? When would it be used?

What is a convertible bond? How would you break it down into simpler parts and price it?

Briefly describe a currency swap. Is the notional principal paid out at the swap’s beginning and maturity?

Check the Internet or other sources and answer the following questions:a. Briefly describe the Troubled Asset Relief Program (TARP) program of the US Government.b. What was the derivative used in the program? Why would the US government trade such a “Toxic thing” as a derivatives contract?c.

How does a plain vanilla interest rate swap differ from a currency swap?

Calculate the gross payments involved and indicate who pays what in this swap deal.

Calculate the net payments involved and indicate who pays what in this swap deal if the bbalibor takes on the values 7.00 percent, 6.50 percent, 7.00 percent, 7.50 percent, and 6.00 percent at the end of the first, second, third, fourth, and fifth year, respectively. • The automakers enter into

Using zero-coupon bond prices (maturing every six months) given below, compute the value of this swap

Where and when was the world’s first modern futures exchange founded? Explain how trading took place on this exchange.

Using Table 8.5, looking at the open, high, and low prices on the June futures contract, what can you tell about the trend of futures prices on this contract during the day?

Using Table 8.5, which three futures contracts have the most trading activity?

Briefly discuss the history of the first interest rate derivatives contract.

What were the first cash-settled futures contracts and are they still trading today?

Where and when were the first index futures contracts traded? Discuss the factors that contributed to the success or failure of this contract.

Today, are futures contracts only traded on US exchanges? Explain your answer.

Is trading in futures contracts mainly for hedging, or speculation, or both? Explain your answer.

Explain why forward contracts have been trading for centuries. What economic function do they perform? What improvement did futures contracts provide over forward contracts? Explain your answer.

Discuss the four different categories into which the history of futures contracts since 1970 has been classified, giving two examples of some of the major developments under each of the four categories.

The following questions concern the doomsters and the boomsters.a. What were the opposing views promoted by Professors Ehrlich and Simon? b. Describe the wager between Professors Doomster and Boomster and the outcome of this bet.

What are the three different levels of mechanization of futures trading? Give examples of each such system.

Briefly explain the pros and cons of daily price limits in futures markets.

Explain the difference between closing price and settlement price. Are they the same or different? Which price is used for marking-to-market?

Why were the early regulators of US commodity futures markets directly under the control of the US Department of Agriculture? How did this change in 1974?

If regulation is bad for business, why does the National Futures Association put a significant amount of regulation on its members?

Consider the gold futures contract traded in the COMEX division of the CME Group. What is the trading unit size and minimum tick size?

On an exchange floor, what is a floor broker?

Ignoring credit risk, if interest rates are constant and equal to zero, do forward prices equal futures prices? Why?

What is the basis of a futures contract? Give a simple example to explain your answer. What does convergence of the basis mean with respect to a futures contract?

Ignoring credit risk, when interest rates are random, must forward prices and futures prices be equal? Explain why or why not.

Suppose you notice that the April gold futures price is $1,518, while that for December is $1,535 (all prices are per ounce). Historically, this spread has been around $10. Explain the workings of a spread strategy that you may set up in the hope that the spread would revert to its historical level.

In January, May futures for sugar (world) trades for 7 cents per pound, while sugar (domestic) trades for 22 cents per pound. You consult technical charts and conclude that their spread is going to widen to 20 cents per pound. a. Suggest a trading strategy for exploiting such opportunities. b. If

Suppose you go short one contract of gold at today’s closing futures price of $1,300 per ounce. Suppose that your brokerage firm requires an initial margin of 5 percent of the position size ($130,000 in this example) and sets the maintenance margin at 80 percent of the initial margin.

Track the margin account payments to a trader holding long position in two contracts when the euro takes the following values (in terms of US dollars): 0.8450, 0.8485, 0.8555, 0.8510, 0.8480, 0.8423, 0.8370, 0.8300, 0.8355,

Track the margin account payments to a trader holding short position in one contract when the euro takes the following values (in terms of US dollars):0.8450, 0.8485, 0.8555, 0.8510, 0.8480, 0.8423, 0.8370, 0.8300, 0.8355.

Suppose that the platinum futures price is $1,580 per ounce and the gold futures price for a contract expiring in the same month as platinum is $1,500 per ounce. Hoping that the spread will narrow to $50 in a month’s time, set up a spread trading strategy, discuss all possible outcomes for the

Explain the difference between cash- settled and physical- settled futures contracts.

What is the open-outcry method of trading futures contracts? What are the benefits of the open-outcry method relative to a computer-based transaction?

Who pays the counterparty when a futures trader defaults?

How is a futures contract trade executed on an exchange?

What is a closing transaction on a futures contract? Do you need to take delivery to terminate a futures contract position?

For physical delivery of a futures contract, explain the three-day delivery process.

What does marking-to-market mean?

What risk do margin accounts on futures contracts and marking-to-market minimize? Explain your answer.

What is the difference between initial margin and variation margin of a futures contract? Provide a simple example to explain your answer.

Explain what a margin call is and when it occurs on a futures contract.

Give two reasons why futures markets may not be started on a commodity. Give an example of such a commodity to support your answer.

Summarize what happened in the Great Western Food Distributors manipulation case.

Summarize what happened in the Hunts silver case.

Summarize what happened in the Salomon Brothers manipulation.

Why is the possibility of manipulation bad for the trading of futures contracts? Give an example of what can go wrong.

Given the existence of the OPEC cartel, is the market for the spot price of oil a competitive market, or not? Do you think the OPEC cartel activities affect the futures price of oil? Explain why or why not

Why are onion futures not traded?

Is selling an insurance contract speculating? Is buying an insurance contract hedging? Are insurance contracts a benefit to society? Explain why or why not.

Explain why speculation in futures trading is analogous to selling insurance contracts. Does this imply that speculation with futures is beneficial or harmful to the economy? Explain your answer.

Do futures contracts need to be regulated? If yes, what can go wrong without regulation? Give an example to explain your answer.

Can you identify common features in the three manipulation stories involving forward or futures markets? How can “authorities” intervene and break squeezes in a typical situation?

Can you identify common features in the three manipulation stories involving forward or futures markets? How can “authorities” intervene and break squeezes in a typical situation? Discuss.

What is price discovery with respect to the trading of a futures contract? Give an example of its use.

Briefly describe the events and developments that led to a spectacular increase in oil prices in the new millennium. In your answer, discuss the role of speculators.

Explain why hedging and speculation are like “two sides of the same coin.”

Why were the early regulators of US commodity futures markets directly under the control of the US Department of Agriculture? How did this change in 1974? Discuss.

What is the National Futures Association and how does it differ from the CFTC?

If regulation is bad for business, why does the National Futures Association put a significant amount of regulation on its members? Discuss.

Suppose that you are an economist working for the CFTC and an exchange has proposed to introduce futures trading on individual stocks. Would you accept this proposal? Give reasons for your answer.

Suppose that it is five minutes to the close of trading for the day and you are a trader on the exchange floor. Your client gives you a sell order for one thousand contracts. You are holding one hundred contracts long. How can you take advantage of this situation?

Today’s price of gold in the spot market is $1,500 per ounce. The price of a zero- coupon bond maturing in one year is $0.95. What will be the one- year forward price for gold?

State the key result of the cost- of- carry model in your own words.

Today is January 1. Forward prices for gold forward maturing on April 1 is $1,500 per ounce. The simple interest rate is 6 percent per year. What would be the forward price for a forward contract on gold maturing on August 1?

Today is January 1. Forward prices for contracts maturing on April 1 and on October 1 are $103 and $109, respectively. The simple interest rate is 8 percent per year. Assuming the spot price. is $100 today, demonstrate two ways in which you can make arbitrage profits from these prices.

Today is January 1. Forward prices for contracts maturing on April 1 and on October 1 are $103 and $109, respectively. On April 1, the price of a zero-coupon bond maturing on October 1 is $0.97. Assuming that the underlying interest rate is a constant interest rate, demonstrate one way of making

State the equation for the valuation of a forward contract in your own words.

Suppose you bought a forward on January 1 that matures a year later. The forward price was $214 at that time, and the simple interest rate was 7 percent per year. Six months have passed, and the spot price is now $150. What is the value of your forward contract today?

Suppose you trade a forward contract today that matures after one year. The forward price is $105, and the simple interest rate is 7 percent per year. If, after six months from today, the spot price is going to be $150 and the value of the forward contract is $20, demonstrate how you can make

The value of a forward contract that you have been holding for the last six months is $50 today. It matures in three more months. If today’s spot price is $100 and the underlying interest rate is 5 percent, what was the forward price that you had negotiated when you purchased the contract six

Explain the difference between the forward price and the value of a forward contract. How are they related?

What is the relation between forward prices of different maturities on the same underlying?

The current price of Your Beloved Machine’s stock is $109. The continuously compounded interest rate is 5.25 percent per year. What will be the fi ve-month forward price for YBM stock?

Showing 3000 - 3100

of 5862

First

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

Last

Step by Step Answers