New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

business statistics communicating

Statistics For Business And Economics 10th Edition David R. Anderson, Dennis J. Sweeney, Thomas A. Williams - Solutions

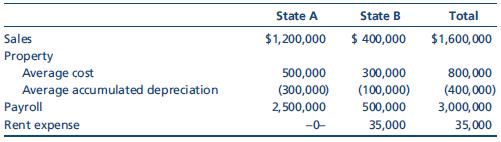

31. LO.5 Dillman Corporation has nexus in States A and B. Dillman’s activities for the year are summarized below.Determine the apportionment factors for A and B assuming that A uses a three-factor apportionment formula under which sales, property (net depreciated basis), and payroll are equally

30. LO.1 Flip Corporation is subject to tax only in State X. Flip generated the following income and deductions. State income taxes are not deductible for X income tax purposes.Sales $4,000,000 Cost of sales 2,800,000 State X income tax expense 200,000 Depreciation allowed for Federal tax purposes

29. LO.1 Perk Corporation is subject to tax only in State A. Perk generated the following income and deductions.Federal taxable income $300,000 State A income tax expense 15,000 Refund of State A income tax 3,000 Depreciation allowed for Federal tax purposes 200,000 Depreciation allowed for state

28. LO.1 For each of the following independent cases, indicate whether the circumstances call for an addition modification (A), a subtraction modification (S), or no modification(N) in computing state taxable income. Then indicate the amount of any modification.The starting point in computing State

27. LO.1 Use Figure 24.1 to provide the required information for Warbler Corporation, whose Federal taxable income totals $10 million.Warbler apportions 60% of its business income to State C. Warbler generates$3 million of nonbusiness income each year, and 20% of that income is allocated to C.

26. LO.1 Use Figure 24.1 to compute Balboa Corporation’s State F taxable income for the year.Addition modifications $29,000 Allocated income (total) 25,000 Allocated income (State F) 3,000 Allocated income (State G) 22,000 Tax credits 800 Federal taxable income 90,000 Subtraction modifications

25. LO.9 As the director of the multistate tax planning department of a consulting firm, you are developing a brochure to highlight the services it can provide. Part of the brochure is a list of five or so key techniques that clients can use to reduce state income tax liabilities. Develop this list

24. LO.2, 9 Your client, Ecru Limited, is considering an expansion of its sales operations, but it fears adverse resulting tax consequences. Write a memo for the tax research file identifying the planning opportunities presented by the ability of a corporation to terminate or create income tax

23. LO.9 Your client, HillTop, is a retailer of women’s clothing. It has increased sales during the holiday season by advertising gift cards for in-store and online use. HillTop has found that gift card holders who come into the store tend to purchase goods that total more than the amount of the

22. LO.8 List three or more taxes, other than the income and sales/use tax, that a state or local jurisdiction might levy.

21. LO.8 Create a PowerPoint outline describing the major exemptions and exclusions from the sales/use tax base of most states. Use your slides to discuss this topic with your accounting students’ club.

20. LO.8 HernandezCo wants to avoid the creation of sales/use tax nexus with State G.The HernandezCo sales representatives believe that they will lose customers because of an increase in their products’ prices due to the new tax obligations. Are the sales representatives correct to be concerned

19. LO.7 The Quail LLC operates solely in State W. As a pass-through entity, Quail does not pay any W taxes. Evaluate this statement.

18. LO.7 Chip and Dale are the only shareholders of VisitTime, a medical transportation firm that is organized as an S corporation. VisitTime makes quarterly estimated income tax payments, related to Chip’s stock ownership, to State Q, its headquarters state.Explain.

17. LO.6 Carmina operates a multinational business from Colorado, a state that applies the unitary theory and requires combined state income tax reporting. Most of her off-shore customers are located in the United Kingdom and Germany, where sales prices and property valuations are relatively high.

16. LO.6 Your client makes the comment, “Unitary corporate income taxation is a bad idea for the business community.” Is her characterization correct? Elaborate.

15. LO.6 State A enjoys a prosperous economy, with high real estate values and compensation levels. State B’s economy has seen better days—property values are depressed, and unemployment is higher than in other states. Most consumer goods are priced at about 10% less in B than in A. Both A and

14. LO.6 The trend in state income taxation is for states to adopt a version of the unitary theory of multijurisdictional taxation in their statutes and regulations.a. Explain why some states are attracted to the unitary theory and a combined reporting scheme of multistate income taxation.b. Is the

13. LO.5 Keystone, your tax consulting client, is considering an expansion program that would entail the construction of a new logistics center in State Q. List at least five questions you should ask in determining whether an asset that is owned by Keystone is to be included in State Q’s property

12. LO.5 Megan is a telecommuter and works most days from her home in Tennessee.Twice a month, she travels to Georgia for a staff meeting at the Atlanta headquarters. In which state’s payroll factor should Megan’s compensation be included if:a. Megan is an employee and is covered by the

11. LO.5 Continue with the facts of Question 10. Another large shipment was made in May to a customer in South Dakota, a state that does not impose any corporate income tax.Is this sale to be included in SpillCo’s Iowa sales factor? Explain.

10. LO.5 In computing the corporate income taxes for Iowa-based SpillCo, should a single large sale in August, in which merchandise was shipped to a customer in Kentucky, be included in the Iowa sales factor?

9. LO.3 The trend in state income taxation is to move from an equal three-factor apportionment formula to a formula that places extra weight on the sales factor. Several states now use sales-factor-only apportionment. Explain why this development is attractive to the taxing states.

8. LO.3 Regarding the apportionment formula used to compute state taxable income, does each of the following independent characterizations describe a taxpayer that is based in state or out of state? Explain.a. The sales factor is positively correlated with the payroll, but not the property,

7. LO.3 Indicate whether each of the following items should be allocated or apportioned by the taxpayer in computing state corporate taxable income. Assume that the state follows the general rules of UDITPA.a. Profits from sales activities.b. Gain on the sale of a plot of land held by a real estate

6. LO.3 Albro, a C corporation, makes profitable sales in about a dozen U.S. states.It owns a headquarters building in one of those states and a fulfillment center in a different state. How does Albro determine the amounts of gross and taxable income that are subject to tax in each of the states in

5. LO.2 Continue with the facts of Question 4. Cheap Phones, one of Josie’s customers who is facing tight cash flow problems, wants to return about 100 defective cell phones.Talk2Me tells Josie to bring the phones back to headquarters. Fearing that she will lose Cheap Phones as a customer if she

4. LO.2 Josie is a sales representative for Talk2Me, a communications retailer based in Fort Smith, Arkansas. Josie’s sales territory is Oklahoma, and she regularly takes day trips to Tulsa to meet with customers. During a typical sales call, Josie takes the customers’current orders and, using

3. LO.2 In no more than three PowerPoint slides, list some general guidelines that a taxpayer can use to determine if it has an obligation to file an income tax return with a particular state. (Hint: Correctly use the terms nexus and domicile in your answer.)

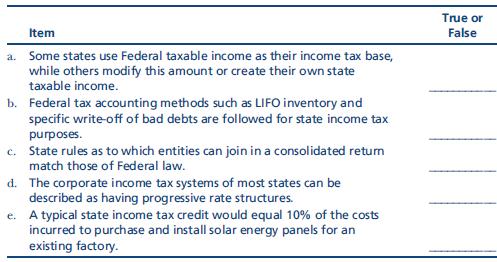

2. LO.1 Complete the following chart by indicating whether each item is true or false.Explain your answers by reference to the overlap of rules appearing in Federal and most state income tax laws. Item a. Some states use Federal taxable income as their income tax base, while others modify this

1. LO.1 You are working with the top management of one of your clients in selecting the U.S. location for a new manufacturing operation. Craft a plan for the CEO to use in discussions with the economic development representatives of several candidate states. In no more than two PowerPoint slides,

3. Determine whether the Kellogg Foundation is a private foundation.Print a copy of its Form 990 or Form 990–PF.

2. Heal, Inc., a tax-exempt hospital, was sold to its shareholders for $6.6 million. The IRS determined that the fair market value of the hospital was $7.8 million.An IRS agent is proposing that the tax-exempt status of the hospital be revoked because the sale of the hospital to the shareholders

1. Allied Fund, a charitable organization exempt under § 501(c)(3), has branches located in each of the 50 states. Allied is not a private foundation. Rather than having each of the state units file an annual return with the IRS, Allied would like to file a single return that reports the

50. LO.8 Historic Burg is an exempt organization that operates a museum depicting eighteenth-century life. Sally gives the museum an eighteenth-century chest that she has owned for 10 years. Her adjusted basis is $55,000, and the chest’s appraised value is$100,000. Sally’s adjusted gross income

49. LO.7 Seagull, Inc., a § 501(c)(3) exempt organization, uses a tax year that ends on October 31. Seagull’s gross receipts are $600,000, and related expenses are $580,000.a. Is Seagull required to file an annual Form 990?b. If so, what is the due date?

48. LO.6 Crow, Inc., an exempt organization, owns a building that cost $800,000. Depreciation of $300,000 has been deducted. The building is mortgaged for $600,000. The mortgage was incurred at the acquisition date. The building contains 10,000 square feet of floor space. Crow uses 8,000 square

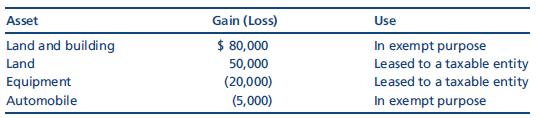

47. LO.6 Assistance, Inc., an exempt organization, sells the following assets during the tax year.Determine the effect of these transactions on Assistance’s unrelated business taxable income. Asset Land and building Land Equipment Automobile Gain (Loss) $ 80,000 50,000 (20,000) Use In exempt

46. LO.6 Tranquility, Inc., an exempt organization, leases factory equipment to Blouses, Inc. Blouses is a taxable entity that manufactures women’s clothing for distribution through upscale department stores. Blouses owns the land and building where it conducts its manufacturing operations. The

45. LO.6 Fish, Inc., an exempt organization, reports unrelated business taxable income of$500,000 (excluding the deduction for charitable contributions). During the year, Fish makes charitable contributions of $54,000, of which $38,000 are associated with the unrelated trade or business.a.

44. LO.6 Save the Squirrels, Inc., a § 501(c)(3) organization that feeds the squirrels in municipal parks, receives a $250,000 contribution from Animal Feed, Inc., a corporation that sells animal feed. In exchange for the contribution, Save the Squirrels will identify Animal Feed as a major

43. LO.6 For each of the following organizations, determine its UBTI and any related UBIT.a. Worn, Inc., an exempt organization, provides food for the homeless. It operates a thrift store that sells used clothing to the general public. The thrift shop is solely staffed by four salaried employees.

42. LO.6 For each of the following organizations, determine its UBTI and any related UBIT.a. AIDS, Inc., an exempt charitable organization that provides support for individuals with AIDS, operates a retail medical supply store open to the general public. The net income of the store, before any

41. LO.6 Perch, Inc., an exempt organization, has unrelated business taxable income of $4 million.a. Calculate Perch’s UBIT.b. Prepare an outline of a presentation you are going to give to the new members of Perch’s board on why Perch is subject to the UBIT even though it is an exempt

40. LO.6 Upward and Onward, Inc., a § 501(c)(3) organization that provides training programs for welfare recipients, reports the following income and expenses from the sale of products associated with the training program.Gross income from sales $850,000 Cost of goods sold 212,000 Advertising and

39. LO.6 The Open Museum is an exempt organization that operates a gift shop. The museum’s annual operations budget is $3.2 million. Gift shop sales generate a profit of$900,000. Another $600,000 of endowment income is generated. Both the income from the gift shop and the endowment income are

38. LO.5 The board of directors of White Pearl, Inc., a private foundation, consists of Charlyne, Beth, and Carlos. They vote unanimously to provide a $325,000 grant to Marcus, their business associate. The grant is to be used for travel and education and does not qualify as a permitted grant to

37. LO.5, 8 Otis is the CEO of Rectify, Inc., a private foundation. Otis invests $500,000(80%) of the foundation’s investment portfolio in derivatives. Previously, the $500,000 had been invested in corporate bonds with an AA rating that earned 7% per annum. If the derivatives investment works as

36. LO.5 Egret, Inc., a private foundation, has been in existence for 10 years. During this period, Egret has been unable to satisfy the requirements for classification as a private operating foundation. At the end of 2011, it had undistributed income of $320,000. Of this amount, $170,000 was

35. LO.5 Gray, Inc., a private foundation, reports the following items of income and deductions.Interest income $ 29,000 Rent income 61,000 Dividend income 15,000 Royalty income 22,000 Unrelated business income 80,000 Rent expenses (26,000)Unrelated business expenses (12,000)Gray is not an exempt

34. LO.4 Pigeon, Inc., a § 501(c)(3) organization, received support from the following sources.Governmental unit A for services rendered $ 6,300 Governmental unit B for services rendered 4,500 Fees from the general public for services rendered(each payment was $100) 75,000 Gross investment income

33. LO.3 Respond, Inc., a § 501(c)(3) organization, receives the following revenues and incurs the following expenses.Grant from Gates Foundation $ 60,000 Charitable contributions received 700,000 Expenses in carrying out its exempt mission 740,000 Net income before taxes of Landscaping, Inc., a

32. LO.3, 6, 8 Roadrunner, Inc., is an exempt medical organization. Quail, Inc., a sporting goods retailer, is a wholly owned subsidiary of Roadrunner. Roadrunner inherited the Quail stock last year from a major benefactor of the medical organization. Quail’s taxable income is $550,000. Quail

31. LO.2, 3 Innovation, Inc., a § 501(c)(3) medical research organization, makes lobbying expenditures of $1.1 million. Innovation incurs exempt purpose expenditures of $15 million in carrying out its medical research mission.a. Determine the tax consequences for Innovation if it does not elect to

30. LO.7 Shane and Brittany are treasurers for § 501(c)(3) exempt organizations. Neither exempt organization is a church. Each year, Shane’s exempt organization files a Form 990 while Brittany’s exempt organization files a Form 990–PF. Discuss the public disclosure requirements for each

29. LO.1, 7 Abby Sue recently became the treasurer of First Point Church. The church has been in existence for three years and has never filed anything with the IRS.a. Identify any reporting responsibilities that Abby Sue might have as church treasurer.b. Would your answer in (a) change if First

28. LO.1, 7 Tom is the treasurer of the City Garden Club, a new garden club. A friend who is the treasurer of the garden club in a neighboring community tells Tom that it is not necessary for the garden club to file a request for exempt status with the IRS. Has Tom received correct advice? Explain.

27. LO.6 Define each of the following with respect to unrelated debt-financed property.a. Debt-financed income.b. Debt-financed property.c. Acquisition indebtedness.d. Average acquisition indebtedness.e. Average adjusted basis.

26. LO.6 An exempt organization is considering conducting bingo games on Thursday nights as a way of generating additional revenue to support its exempt purpose. Before doing so, however, the president of the organization has come to you for advice regarding the effect on the organization’s

25. LO.6 Sight, Inc., a tax-exempt organization that trains the visually impaired to restore and tune pianos, receives pianos as contributions. When the number of pianos on hand exceeds 15, Sight sells the excess; the pianos used in the training program the longest are sold first. Is the revenue

24. LO.1, 6 To which of the following tax-exempt organizations may the UBIT apply?a. Red Cross.b. Salvation Army.c. United Fund.d. College of William and Mary.e. Rainbow, Inc., a private foundation.f. Louisiana State University.g. Colonial Williamsburg Foundation.h. Federal Land Bank.i. University

23. LO.6, 8 Second Church is going to operate a gift shop and bookshop that will include only religious articles in its inventory. The shop will be staffed by employees who are not church members. These employees will be paid the minimum wage except for the gift shop and bookshop manager, whose

22. LO.6 An exempt municipal hospital operates a pharmacy that is staffed by a pharmacist 24 hours per day. The pharmacy serves only hospital patients. Is the pharmacy an unrelated trade or business?

21. LO.6 What type of activity by a church is likely to be subject to the unrelated business income tax? What factors must be present for this activity to be classified as an unrelated trade or business?

20. LO.6 Less, Inc., a § 501(c)(3) organization, has unrelated business taxable income of$600,000 and total earnings of $1 million. Why is only the $600,000 subject to Federal income tax? What is the Federal income tax liability?

19. LO.6 Winston recently became the treasurer of Homeless, Inc., a § 501(c)(3) organization that feeds the homeless. One of the entity’s directors has proposed that Homeless purchase and operate a fast-food franchise as part of Homeless, Inc., to raise additional revenue (a projected increase

18. LO.4, 5 Really Welcome, Inc., a tax-exempt organization, receives 30% of its support from disqualified persons. Another disqualified person has agreed to match this support if Really Welcome will appoint him to the organization’s board of directors. What tax issues are relevant to Really

17. LO.5 Sunset, Inc., a § 501(c)(3) exempt organization that is classified as a private foundation, generates investment income of $600,000 for the current tax year. This amount represents 20% of Sunset’s total income.a. What type of tax is imposed on Sunset associated with its investment

16. LO.5What types of taxes may be levied on a private foundation? Why are the taxes levied?

15. LO.4 Describe the external support test and the internal support test for a private foundation.

14. LO.4 Which of the following exempt organizations could be private foundations?a. Bruton Parish Episcopal Church.b. Our Lady Catholic Church.c. Port Allen Community Hospital.d. National Football League (NFL).e. Southeastern Louisiana University Alumni Association.f. United Fund.g. Lee’s

13. LO.4, 5 What is a private foundation? What are the disadvantages of an exempt organization being classified as a private foundation?

12. LO.3 What types of activities are not subject to the tax imposed on feeder organizations?

11. LO.3 Service, Inc., an exempt organization, owns all of the stock of Blue, Inc., a retailer of boating supplies. Blue remits all of its profits to Service. According to a policy adopted by Service’s board, 60% of the amount received from Blue is to be spent annually in carrying out

10. LO.3 The IRS can impose intermediate sanctions on a public charity if its gross unrelated business income exceeds 50% of its gross income or if less than two-thirds of its net unrelated business income is used in carrying out its tax-exempt mission. Evaluate this statement.

9. LO.3 Under what circumstances can an exempt organization engage in lobbying activities?What types of exempt organizations are eligible for this treatment?

8. LO.3 Can a church make an election that will enable it to engage in lobbying on a limited basis without incurring any negative tax consequences? Explain.

7. LO.3 Good, Inc., a § 501(c)(3) exempt organization, engages in a § 503 prohibited transaction. What negative tax consequences may be associated with Good engaging in a§ 503 prohibited transaction?

6. LO.3 Walter contributes $3,000 to an exempt organization. Addie contributes $3,000 to a different exempt organization. Why might Addie be permitted a $3,000 charitable contribution deduction in calculating her itemized deductions when Walter is not?

5. LO.2 What are the common characteristics shared by many exempt organizations?

4. LO.1 Identify the statutory authority under which each of the following is exempt from Federal income tax.a. Kingsmill Country Club.b. Shady Lawn Cemetery.c. Amber Credit Union.d. Veterans of Foreign Wars.e. Boy Scouts of America.f. United Fund.g. Federal Deposit Insurance Corporation.h. Bruton

3. LO.1 Which of the following organizations qualify for exempt status?a. Tulane University (a private university).b. Virginia Qualified Tuition Program.c. Red Cross.d. Disneyland.e. Ford Foundation.f. Houston Chamber of Commerce.g. Colonial Williamsburg Foundation.h. Professional Golfers

2. LO.1 Why are certain organizations either partially or completely exempt from Federal income tax?

1. LO.1, 6 Eggshell, Inc., a C corporation, operates a rental clothing store, and its profits are subject to double taxation. First Church of the States operates a retail gift shop and bookshop and is not subject to taxation. What is the explanation for this difference in Federal income tax

3. Outline the Treasury Department’s tax reform proposal to treat passthrough entities as corporations. Summarize your findings in an e-mail to your instructor.

2. Sam is selling his S corporation, Superbody Fitness, Inc. He will receive 80% cash and 20% of another S corporation fitness center. As part of this transaction, should Sam liquidate Superbody Fitness? Outline your analysis in an e-mail to your instructor.

1. Bushong, Inc., a calendar year S corporation, has a “tax cash-flow” provision in its shareholder agreement. Bushong must make annual distributions by the December 31 following a tax year in which there is an income pass-through. Each distribution must be in an amount sufficient to enable

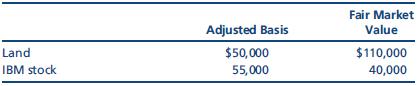

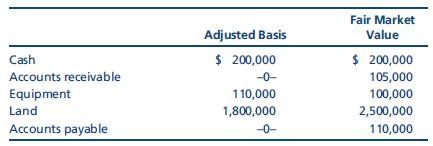

52. LO.10 Blue Corporation elects S status effective for calendar year 2011. As of January 1, 2011, Blue holds two assets.Blue sells the land in 2012 for $120,000. Calculate Blue’s recognized built-in gain, if any, in 2012. Land IBM stock Adjusted Basis $50,000 55,000 Fair Market Value $110,000

51. LO.11 Ruby is the owner of all of the shares of an S corporation. Ruby is considering receiving a salary of $80,000 from the business. She will pay 7.65% FICA taxes on the salary, and the S corporation will pay the same amount of FICA tax. If Ruby reduces her salary to $40,000 and takes an

50. LO.11 Friedman, Inc., an S corporation, holds some highly appreciated land and inventory and some marketable securities that have declined in value. It anticipates a sale of these assets and a complete liquidation of the company over the next two years.Arnold Schwartz, the CFO, calls you,

49. LO.5, 6, 11 Bonnie and Clyde each own one-third of a fast-food restaurant, and their 13-year-old daughter owns the other shares. Both parents work full-time in the restaurant, but the daughter works infrequently. Neither Bonnie nor Clyde receives a salary during the year, when the ordinary

48. LO.4, 10, 11 Sweetwater, Inc., is an S corporation in Sour Lake, Texas.a. In 2012, Sweetwater’s excess net passive income is $42,000. Sweetwater holds $31,000 of accumulated earnings and profits from a C corporation year. It reports $58,000 of taxable income and AMT adjustments of $17,000 for

47. LO.10 Rodeo, Inc., a cash basis S corporation in College Station, Texas, formerly was a C corporation. Rodeo records the following assets and liabilities on January 1, 2012, the date its S election is made.During 2012, Rodeo collects the accounts receivable and pays the accounts payable. The

46. LO.5, 6, 8 Emeline, Inc., of Auburn, Alabama, is an accrual basis S corporation with three equal shareholders. The three cash basis shareholders have the following stock basis at the beginning of the year: Andre, $12,000; Crum, $22,000; and Barbara, $31,000.Emeline reports the following income

45. LO.5, 6, 8, 9 A calendar year S corporation has an ordinary loss of $80,000 and a capital loss of $20,000. Ms. Freiberg owns 30% of the corporate stock and has a $24,000 basis in her stock. Determine the amounts of the ordinary loss and capital loss, if any, that flow through to Ms. Freiberg.

44. LO.6, 9 In Problem 43, how much of the Whitman loss belongs to Ann and Becky?Becky’s stock basis is $41,300.

43. LO.6, 9 At the beginning of the year, Ann and Becky own equally all of the stock of Whitman, Inc., an S corporation. Whitman generates a $120,000 loss for the year (not a leap year). On the 189th day of the year, Ann sells her half of the Whitman stock to her son, Scott. How much of the

42. LO.5, 6, 11 Red Lion, Inc., is an S corporation with a sizable amount of AEP from a C corporation year. The S corporation has $400,000 of investment income and $400,000 of investment expense in 2012. The company makes cash distributions to enable its sole shareholder to pay her taxes. What are

41. LO.8 Assume the same facts as in Problem 39, except that Jeff’s share of corporate taxable income is only $8,000 and there is no distribution. However, the corporation repays the $10,000 loan principal to Jeff. Discuss the tax effects. Assume that there was no corporate note (i.e., only an

40. LO.8 Assume the same facts as in Problem 39, except that there is no $15,000 distribution but the corporation repays the loan principal to Jeff. Discuss the tax effects.

Showing 300 - 400

of 7675

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers