New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

business statistics communicating

Statistics For Business And Economics 10th Edition David R. Anderson, Dennis J. Sweeney, Thomas A. Williams - Solutions

48. LO.6, 7 In 2000, Alan purchases a commercial single premium annuity. Under the terms of the policy, Alan is to receive $120,000 annually for life. If Alan predeceases his wife, Katelyn, she is to receive $60,000 annually for life. Alan dies first at a time when the value of the survivorship

47. LO.6 In 2007, Peggy, a widow, places $3 million in trust, life estate to her children, remainder to her grandchildren, but retains the right to revoke the trust. In 2011, when the trust is worth $3.1 million, Peggy rescinds her right to revoke the trust. Peggy dies in 2012 when the trust is

46. LO.6, 9 At the time of his death, Garth was involved in the following arrangements.• He held a life estate in the Myrtle Trust with the remainder passing to Garth’s adult children. The trust was created by Myrtle (Garth’s mother) in 1984 with securities worth $900,000. The Myrtle Trust

45. LO.4, 6, 7 In 2005, using $2.5 million in community property, Quinn creates a trust, life estate to his wife, Eve, and remainder to their children. Quinn dies in 2009 when the trust is worth $3.6 million, and Eve dies in 2012 when the trust is worth $5.6 million.a. Did Quinn make a gift in

44. LO.4, 6 Before her death in early 2012, Katie made the following transfers.• In 2008, purchased stock in Green Corporation for $200,000, listing title as follows:“Katie, payable on proof of death to my son Travis.” Travis survives Katie, and the stock is worth $300,000 when Katie dies.•

43. LO.6, 7 At the time of Matthew’s death, he was involved in the following transactions.• Matthew was a participant in his employer’s contributory qualified pension plan. The plan balance of $2 million is paid to Olivia, Matthew’s daughter and beneficiary. The distribution consists of the

42. LO.6 Assume the same facts as in Problem 41 with the following modifications.• Mitch is killed in a rock slide while mountain climbing in November 2012, and the insurer pays Alicia’s estate $400,000.• Bert’s executor did not make a QTIP election.• Alicia’s IRAs were the Roth type

41. LO.6 At the time of her death on September 4, 2012, Alicia held the following assets.Fair Market Value Bonds of Emerald Tool Corporation $ 900,000 Stock in Drab Corporation 1,100,000 Insurance policy (face amount of$400,000) on the life of her father, Mitch 80,000*Traditional IRAs 300,000* Cash

40. LO.6, 7 At the time of his death on September 2, 2012, Kenneth owned the following assets.Fair Market Value City of Boston bonds $2,500,000 Stock in Brown Corporation 900,000 Promissory note issued by Brad(Kenneth’s son) 300,000 In October 2012, the executor of Kenneth’s estate received the

39. LO.5 Using property she inherited, Myrna makes a gift of $6.2 million to her adult daughter, Doris. The gift takes place in 2012. Neither Myrna nor her husband, Greg, has made any prior taxable gifts. Determine the gift tax liability if:a. The § 2513 election to split gifts is not made.b. The

38. LO.4 Jesse dies intestate (i.e., without a will) in May 2011. Jesse’s major asset is a tract of land. Under applicable state law, Jesse’s property will pass to Lorena, who is his only child. In December 2011, Lorena disclaims one-half of the property. In June 2012, Lorena disclaims the

37. LO.4, 7 In May 2011, Dudley and Eva enter into a property settlement preparatory to the dissolution of their marriage. Under the agreement, Dudley is to pay Eva $6 million in satisfaction of her marital rights. Of this amount, Dudley pays $2.5 million immediately, and the balance is due one

36. LO.4 Carl made the following transfers during 2012.• Transferred $900,000 in cash and securities to a revocable trust, life estate to himself and remainder interest to his three adult children by a former wife.• In consideration of their upcoming marriage, gave Lindsey (age 21) a $90,000

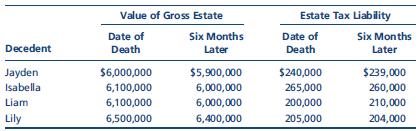

35. LO.3 In each of the following independent situations, indicate whether the alternate valuation date can be elected. Explain why or why not. Assume that all deaths occur in 2012. Value of Gross Estate Estate Tax Liability Six Months Date of Six Months Date of Decedent Death Later Death Later

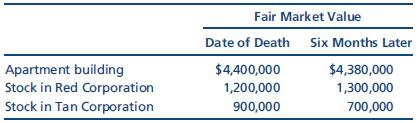

34. LO.1, 3, 6, 7 Arlene’s estate includes the following assets.Accrued rents on the apartment building are as follows: $70,000 (date of death) and $60,000 (six months later). To pay expenses, the executor of Arlene’s estate sells the Tan stock for $600,000 five months after her death.a. If the

33. LO.9 In terms of the generation-skipping transfer tax, comment on the following.a. A GSTT termination event and a GSTT distribution event look very similar.b. A direct skip can occur only in gift situations, not in testamentary situations.c. Spouses may be of different generations if there is

32. LO.7, 8 Abby dies in the current year. In determining her Federal estate tax liability, comment on the relevance of each of the following.a. Abby made taxable gifts in 1975 and 2008.b. Abby held a life estate in a trust created by her late husband.c. State death taxes paid by Abby’s estate.d.

31. LO.4, 6 Using the legend provided, classify each of the following transactions.Legend NT = No transfer tax imposed GT = Subject to the Federal gift tax ET = Subject to the Federal estate taxa. Hal establishes a bank checking account listing ownership as “Hal and Darlene, joint tenants with

30. LO.8 Three unmarried and childless sisters live together. All are of advanced age and in poor health, and each owns a significant amount of wealth. Each has a will that passes her property to her surviving sister(s) or, if no survivor, to their church. Within a period of two years and on

29. LO.7 Bernice dies and, under a will, passes real estate to her surviving husband. The real estate is subject to a mortgage. For estate tax purposes, how will any marital deduction be determined? Can Bernice’s estate deduct the mortgage under § 2053? Explain.

28. LO.6, 7 Due to the negligence of the other driver, Adam’s car is completely destroyed, and he is seriously injured. Two days later, Adam dies from injuries suffered in the accident.a. What, if any, are the estate tax consequences of these events?b. Are there any income tax consequences to

27. LO.6 With regard to “life insurance,” comment on the following.a. What the term includes (i.e., types of policies).b. The meaning of “incidents of ownership.”c. When a gift occurs upon maturity of the policy.d. The tax consequences when the owner of the policy predeceases the insured

26. LO.6 At the time of Emile’s death, he was a joint tenant with Colette in a parcel of real estate. With regard to the inclusion in Emile’s gross estate under § 2040, comment on the following independent assumptions:a. Emile and Colette received the property as a gift from Douglas.b. Colette

25. LO.6 Discuss the estate tax treatment of each of the following. In all cases, assume that Mike is the decedent and that he died on July 5, 2012.a. Interest on State of South Dakota bonds paid on August 1, 2012.b. Cash dividend on Puce Corporation stock paid on August 10, 2012. Date of record

24. LO.3, 6, 7 Distinguish between the following.a. The gross estate and the taxable estate.b. The taxable estate and the tax base.c. The gross estate and the probate estate.

23. LO.4 In each of the following independent situations, indicate whether the transfer is subject to the Federal gift tax.a. Asa contributes to his mayor’s reelection campaign fund. The mayor has promised to try to get some of Asa’s property rezoned from residential to commercial use.b. Mary

22. LO.5 In connection with the filing of a Federal gift tax return, comment on the following.a. No Federal gift tax is due.b. The gift is between spouses.c. The § 2513 election to split gifts is to be used.d. The donor uses a fiscal year for Federal income tax purposes.e. The donor obtained from

21. LO.5 Regarding the gift-splitting provision of § 2513, comment on the following.a. What it was designed to accomplish.b. The treatment of any taxable gifts previously made by the nonowner spouse.c. The utility of the election in a community property jurisdiction.

20. LO.4 Qualified tuition programs under § 529 enjoy significant tax advantages. Describe these advantages with regard to the Federal:a. Income tax.b. Gift tax.c. Estate tax.

19. LO.4 The Randalls have a married son and four grandchildren (ages 15, 17, 18, and 19). They establish a trust under which the income is to be paid annually to the grandchildren until the youngest reaches age 25. At that point, the trust terminates and the principal (corpus) is distributed to

18. LO.4 Derek dies intestate (i.e., without a will) and is survived by a daughter, Ruth, and a grandson, Ted (Ruth’s son). Derek’s assets include a large portfolio of stocks and bonds and a beach house. Ruth has considerable wealth of her own, while Ted has just finished college and is

17. LO.4, 6 At a local bank, Jack purchases for $100,000 a five-year CD listing title as follows:“Meredith, payable on death to Briana.” Four years later, Meredith dies. Briana, Meredith’s daughter, then redeems the CD when it matures. Discuss the transfer tax consequences if Meredith is:a.

16. LO.4 Addison provides all of the support of her dependent father, Walter, who lives with her. Because Walter is very proud and wants to appear independent, Addison gives him the money to pay his medical bills. Is Addison subject to the Federal gift tax as a result of these transfers? Explain.

15. LO.4 Gus (age 84) and Belle (age 18) are married in early 2012. Late in 2012, Belle confronts Gus about his failure to transfer to her the considerable amount of property he previously promised. Gus reassures Belle that she will receive the property when he dies. Because the transfer occurs at

14. LO.4 Corinne wants to sell some valuable real estate to her son on an installment arrangement. Because related parties are involved, she fears that the IRS may question the selling price and contend that a portion of the transfer is a gift.a. Are Corinne’s concerns realistic? Explain.b. How

13. LO.3 What type of ownership interest is appropriate in each of the following?a. A father wants to provide for his daughter during her life but wants to ensure that her younger husband (i.e., the son-in-law) does not inherit the property if he survives her.b. A married couple buys a home and

12. LO.3 Hugo dies in 2012, leaving a large estate. Among other provisions in his will are charitable and marital bequests. When Hugo’s executor elects the alternate valuation date, it has the effect of decreasing the marital deduction and increasing the charitable deduction of the estate. How

11. LO.3 As to the alternate valuation date of § 2032, comment on the following.a. The justification for the election.b. The main heir prefers the date of death value.c. An estate asset is distributed to an heir three months after the decedent’s death.d. Effect of the election on income tax

10. LO.3 Regarding the formula for the Federal estate tax (see Figure 27.2 in the text), comment on the following.a. The gross estate may include property interests not owned by the decedent at the time of death.b. The gross estate may include assets that are not part of the probate estate (i.e.,

9. LO.2, 4, 5 Regarding the formula for the Federal gift tax (see Figure 27.1), comment on the following observations.a. Only post-1976 taxable gifts must be considered in determining the tax on a current gift.b. A credit is allowed for the gift taxes actually paid on prior gifts.c. A deduction for

8. LO.2 A new out-of-state client, Robert Ball, has asked you to prepare a Form 709 for a large gift he made in 2011. When you request copies of any prior gift tax returns he may have filed, he responds, “What do gifts in prior years have to do with 2011?” Send a letter to Robert at 4560 Walton

7. LO.1 In what manner does an inheritance tax differ from an estate tax?

6. LO.1 To avoid both state and Federal transfer taxes (i.e., estate, inheritance, and gift), Gary (a U.S. citizen) has moved to Costa Rica. Furthermore, he plans to limit his investments to non-U.S. assets (e.g., foreign stocks and bonds and real estate). Will Gary accomplish his objective?

5. LO.1 Carlos, a citizen and resident of Chile, would like to buy stock in General Electric and make gifts of the shares to his children. Will the Federal gift tax pose a problem for him? Explain.

4. LO.1 Kim, a wealthy Korean national, is advised by his physicians to have an operation performed at the Mayo Clinic. Kim is hesitant to come to the United States because of the possible tax consequences. If the procedure is not successful, Kim does not want his wealth to be subject to the

3. LO.1 Eight years ago, Alex made gifts of all of his assets to family and friends. Although the transfers would have generated gift taxes, none were paid and no gift tax returns were filed. At present, no one knows where Alex is or even if he is still alive. The IRS has discovered that the gifts

2. LO.1 Over the years, the tax treatment of transfers by gift and by death has not been consistent. In this regard, what were the policy considerations supporting the original rules and the changes made?

1. LO.1 Why can the unified transfer tax be categorized as an excise tax? In this regard, how does it differ from an income tax?

3. Find an article in which a tax professional describes the confidentiality privilege available under the Code for a CPA tax adviser. Then construct a list of “Confidentiality Dos and Don’ts for the CPA.” Summarize the article in an e-mail to your professor.

2. In 2008, Gupta sold some shares of Wingo, a private U.S. corporation, for $40 million. On his Form 1040 Schedule D for 2008, Gupta showed the basis of the stock as $11 million, thereby reporting a $29 million capital gain. Gupta filed his return on October 1, 2009, after properly receiving an

1. Your firm is preparing the Form 1040 of Norah McGinty, a resident, like you, of Oklahoma. You have contracted for the last three filing seasons with a firm in India, Tax Express Bangalore, to prepare initial drafts of tax returns using tax software that you provide to Tax Express. You find that

47. LO.8 You are the chair of the Ethics Committee of your state’s CPA Licensing Commission.Interpret controlling AICPA authority in addressing the following assertions by your membership.a. When a CPA has reasonable grounds for not answering an applicable question on a client’s return, a brief

46. LO.8 Compute the preparer penalty the IRS could assess on Gerry in each of the following independent cases.a. On March 21, the copy machine was not working, so Gerry gave original returns to her 20 clients that day without providing any duplicates for them. Copies for Gerry’s files and for

45. LO.8 Discuss which penalties, if any, might be imposed on the tax adviser in each of the following independent circumstances. In this regard, assume that the tax adviser:a. Suggested to the client various means by which to acquire excludible income.b. Suggested to the client various means by

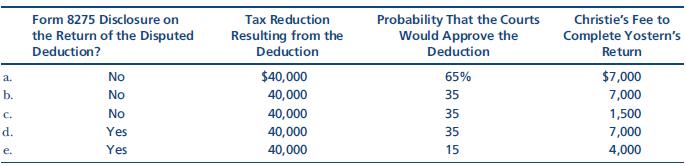

44. LO.8 Christie is the preparer of the Form 1120 for Yostern Corporation. On the return, Yostern claimed a deduction that the IRS later disallowed on audit. Compute the tax preparer penalty that could be assessed against Christie in each of the following independent situations. Form 8275

43. LO.8 Rod’s Federal income tax returns (Form 1040) for the indicated three years were prepared by the following persons.Year Preparer 2011 Rod 2012 Ann 2013 Cheryl Ann is Rod’s next-door neighbor and owns and operates a pharmacy. Cheryl is a licensed CPA and is engaged in private practice.

42. LO.7 Chee owed $4,000 in Federal income tax when she filed her Form 1040 for 2012.She attached a sticky note to the 1040 that read, “My inventory computations on last year’s (2011) return were wrong, so I paid $1,000 too much in tax.” Chee then included a check for $3,000 with the Form

41. LO.5, 7 On April 3, 2009, Mark filed his 2008 income tax return, which showed a tax due of $80,000. On June 1, 2011, he filed an amended return for 2008 that showed an additional tax of $10,000. Mark paid the additional amount. On May 18, 2012, Mark filed a claim for a 2008 refund of $45,000.a.

40. LO.7 Loraine, a calendar year taxpayer, reported the following transactions, all of which were properly included in a timely return.a. Presuming the absence of fraud, how much of an omission from gross income is required before the six-year statute of limitations applies?b. Would it matter if

39. LO.7 What is the applicable statute of limitations in each of the following independent situations?a. No return was filed by the taxpayer.b. The taxpayer incurred a bad debt loss that she failed to claim.c. A taxpayer inadvertently omitted a large amount of gross income.d. Same as (c), except

38. LO.6 The Leake Company, owned equally by Jacquie (chair of the board of directors)and Jeff (company president), is in very difficult financial straits. Last month, Jeff used the $300,000 withheld from employee paychecks for Federal payroll and income taxes to pay a creditor who threatened to

37. LO.6 Kold Services Corporation estimates that its 2013 taxable income will be$500,000. Thus, it is subject to a flat 34% income tax rate and incurs a $170,000 liability.For each of the following independent cases, compute Kold’s 2013 minimum quarterly estimated tax payments that will avoid an

36. LO.6 Trudy’s AGI last year was $200,000. Her Federal income tax came to $65,000, which she paid through a combination of withholding and estimated payments. This year, her AGI will be $300,000, with a projected tax liability of $45,000, all to be paid through estimates.a. Ignore the

35. LO.6 Moose, a former professional athlete, now supplements his income by signing autographs at collectors’ shows. Unfortunately, Moose has not been conscientious about reporting all of this income on his tax return. Now, the IRS has charged him with additional taxes of $100,000 due to

34. LO.6 The Eggers Corporation filed an amended Form 1120, claiming an additional$400,000 deduction for payments to a contractor for a prior tax year. The amended return was based on the entity’s interpretation of a Regulation that defined deductible advance payment expenditures. The nature of

33. LO.6 Singh, a qualified appraiser of fine art and other collectibles, was advising Colleen when she was determining the amount of the charitable contribution deduction for a gift of sculpture to a museum. Singh sanctioned a $900,000 appraisal, even though he knew the market value of the piece

32. LO.6 Compute the undervaluation penalty for each of the following independent cases involving the value of a closely held business in the decedent’s gross estate. In each case, assume a marginal estate tax rate of 35%.Reported Value Corrected IRS Valuationa. $ 20,000 $ 25,000b. 100,000

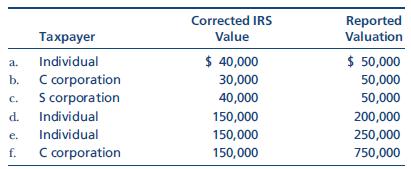

31. LO.6 Compute the overvaluation penalty for each of the following independent cases involving the fair market value of charitable contribution property. In each case, assume a marginal income tax rate of 35%. a. Taxpayer Individual C corporation Corrected IRS Value $ 40,000 Reported Valuation $

30. LO.6 LaVon underpaid her taxes by $250,000. A portion of the underpayment was shown to be attributable to LaVon’s negligence ($200,000). A court found that a portion of that deficiency constituted civil fraud ($50,000). Compute the total fraud and negligence penalties incurred.

29. LO.6 Maureen, a calendar year taxpayer, files her 2011 return on November 4, 2013.She did not obtain an extension for filing her return, and the return reflects additional income tax due of $15,000.a. What are Maureen’s penalties for failure to file and to pay?b. Would your answer change if

28. LO.6 Olivia, a calendar year taxpayer, does not file her 2011 return until December 12, 2012. At this point, she pays the $40,000 balance due on her 2011 tax liability of $70,000.Olivia did not apply for and obtain any extension of time for filing the 2011 return.When questioned by the IRS on

27. LO.6 Compute the failure to pay and failure to file penalties for John, who filed his 2011 income tax return on December 20, 2012, paying the $10,000 amount due at that time. On April 1, 2012, John received a six-month extension of time in which to file his return. He has no reasonable cause

26. LO.6 Wade filed his Federal income tax return on time but did not remit the balance due. Compute Wade’s failure to pay penalty in each of the following cases. Assume the IRS has not issued a deficiency notice.a. Four months late, $3,000 additional tax due.b. Ten months late, $4,000 additional

25. LO.6 Rita forgot to pay her Federal income tax on time. When she actually filed, she reported a balance due. Compute Rita’s failure to file penalty in each of the following cases.a. Two months late, $1,000 additional tax due.b. Five months late, $3,000 additional tax due.c. Eight months late,

24. LO.5 Gordon paid the $10,000 balance of his Federal income tax three months late.Ignore daily compounding of interest. Determine the interest rate that applies relative to this amount, assuming that:a. Gordon is an individual.b. Gordon is a C corporation.c. The $10,000 is not a tax that is due,

23. LO.6, 8 In no more than three PowerPoint slides, list at least four of the Code’s penalties that could be assessed against paid preparers of tax returns. Name the violation that triggers the penalty, and explain how the dollar amount of the penalty is determined.

22. LO.8 Indicate whether each of the following parties could be subject to the tax preparer penalties.a. Tom prepared Sally’s return for $250.b. Theresa prepared her grandmother’s return for no charge.c. Georgia prepared her church’s return for $500 (she would have charged an unrelated party

21. LO.8 Give the Circular 230 position concerning each of the following situations sometimes encountered in the tax profession.a. Taking an aggressive pro-taxpayer position on a tax return.b. Not having a quality review process for a return completed by a partner of the tax firm.c. Purposely

20. LO.8 In no more than five PowerPoint slides, prepare a presentation to your school’s Accounting Alumni Club titled “How the IRS Keeps Track of Tax Preparers.” Include the application of the PTIN and of Circular 230 in your remarks.

19. LO.7 Why should the taxpayer be “let off the hook” and no longer be subject to audit exposure once the applicable statute of limitations has expired? Do statutes of limitations protect the government? Other taxpayers?

18. LO.6 While working on the Federal income tax return for your client Best Wishes LLC, you discover that the payroll office was lax in its procedures. You found that the office allowed some employees to reduce their withholding taxes by overstating the number of exemptions to which they were

17. LO.4, 6 In each of the following cases, distinguish between the terms.a. Offer in compromise and closing agreement.b. Failure to file and failure to pay.c. 90-day letter and 30-day letter.d. Negligence and fraud.e. Criminal and civil tax fraud.

16. LO.4, 5, 7 Indicate whether each of the following statements is true or false.a. The government never pays a taxpayer interest on an overpayment of tax.b. The IRS can compromise on the amount of tax liability if there is doubt as to the taxpayer’s ability to pay.c. The statute of limitations

15. LO.6 On October 30, Cameron determines that his tax for the year will total $10,000.If his employer is scheduled to withhold only $6,500 in Federal income taxes, what can Cameron do to avoid any underpayment penalty?

14. LO.6 Yonkers Corporation recomputes its research credit for the prior tax year and, as a result, claims a $100,000 refund. The IRS reviews the claim and allows only $20,000 of the requested refund. If Yonkers does not appeal, is this matter finished? Is Yonkers certain to receive the full

13. LO.6 The IRS assesses special penalties when a taxpayer misreports the value of property that was the subject of a deduction or that was subject to a gift/estate tax. How are these penalties computed? Hint: Include the term gross misstatement in your answer.

12. LO.6 Which of the valuation penalties is likely to arise when an aggressive taxpayer reports:a. A charitable contribution?b. A business deduction?c. A decedent’s taxable estate?

11. LO.5 For about 15 months, Ian has been negotiating a settlement with the IRS concerning a disputed tax deduction. The IRS and Ian have agreed to the amount of prioryear taxes he must pay. Ian asks you whether he also is liable now for interest charges on his underpayment and, if so, how that

10. LO.4 Describe the conditions under which your client Lee Anne might approach the IRS with an offer in compromise.

9. LO.3 Describe the three broad types of IRS audits. Give an example of an issue that each type of audit might address, and indicate how frequently such audits are conducted by the IRS.

8. LO.3, 4 Lori wants to establish that her niece Suzette actually qualifies for a dependency exemption. After the issue is raised by the IRS on audit, Lori could argue the matter with the agent, an IRS Appeals officer, or the Tax Court. Give Lori advice about how to handle her tax dispute.

7. LO.3 When can an individual taxpayer feel certain that his or her tax return will not be audited by the IRS? One year after it is filed? Two years? Five years? Explain.

6. LO.3 Gloria and Maria work together in an insurance office. Gloria’s Form 1040 seems to be audited two out of every three years, while Maria never has been audited. How does the IRS select tax returns for audit? List some of the factors that might result in the different treatment of

5. LO.2 Describe the process the IRS uses to collect the tax that is found to be due after an audit is completed. Assume that the IRS findings are not appealed but that the taxpayer does not pay the amount due as determined by the audit. Illustrate the process with no more than four PowerPoint

4. LO.2 Your client is litigating in the Tax Court concerning a tax credit that she claimed and the IRS has denied. Who bears the burden of proof regarding the litigation?

3. LO.2 Your tax research has located a Tax Court case that supports the claiming of a deduction by a client, while an IRS letter ruling holds to the contrary. The pertinent facts of both the case and the ruling match those of the client. Which holding should be followed in preparing the client’s

2. LO.1 Recently, a politician was interviewed about fiscal policy, and she mentioned reducing the “tax gap.” Explain what this term means. What are some of the pertinent political and economic issues relative to the tax gap?

1. LO.1 An article in USA Today refers to the “audit lottery” and how one’s chances of being audited are higher under the current IRS leadership. What is the audit lottery?How should a tax professional view the statistics about a taxpayer’s audit likelihood?

3. For your analysis, choose 10 countries, one of which is the United States. Create a table showing whether each country applies a worldwide or territorial approach to international income taxation. Then list the country’s top income tax rate on business profits. Send a copy of your table to

2. Polly Ling is a successful professional golfer. She is a resident of a country that does not have a tax treaty with the United States. Ling plays matches around the world, about one-half of which are in the United States. Ling’s reputation is without blemish;in fact, she is known as being

Showing 600 - 700

of 7675

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers